How Economists Work Chapter 2 LIPSEY CHRYSTAL ECONOMICS

(146.")

")

Annual savings 1 70, 000 10, 000 2 30, 000")

. • This")

- Slides: 60

How Economists Work Chapter 2 LIPSEY & CHRYSTAL ECONOMICS 12 e

Introduction • Economics seeks to understand many important issues in the world around us and ask the following questions, amongst others: • What makes some countries grow richer when others seem to get poorer? • Why do we sometimes have recessions? • When should the government try to influence markets? What are the costs and benefits of globalization? • Will some new technology eliminate many jobs?

• In order to get a handle on such big issues, economists have developed ways of setting out and testing their theories • They also seek to use what they have learned in order to provide advice on how things could be improved.

Learning outcomes • By the end of the lecture you should have a good understanding of: – The difference between positive and normative statements – How economists set out their theories – How economic data are handled and graphed – How economic relationships are represented in diagrams.

Positive and normative statements • Economists give advice on a wide variety of topics. Advice comes in two broad types: • Normative • Positive

Normative advice • Normative advice depends upon a value judgement and it tells others what they ought to do.

Positive advice • Positive advice is where the adviser is saying, ‘If this is what you want to do, then here are ways of doing it. ’

Positive and Normative statements

• It is difficult to have a rational discussion of issues if positive and normative issues are confused. • Much of the success of modern science depends on the ability of scientists to separate their views on what does, or might, happen in the world, from their views on what they would like to happen.

Note! Distinguishing what is true from what we would like to be, or what we feel ought to be, depends to a great extent on being able to distinguish between positive and normative statements.

To clarify • Normative statements depend on value judgments. They involve issues of personal opinion, which cannot be settled by recourse to facts. • In contrast, positive statements do not involve value judgments. They are statements about what is, was, or will be; that is, statements that are about matters of fact.

Economic theorizing • In order to address the problems that we face economists have developed an approach that involves developing theories and building models. • These help the economist to understand problems and find realistic and practical solutions where possible!

Theories • Theories are constructed to explain things! • These theories are built around definitions, assumptions, and predictions. • They simplify the problem in hand allow the economist to observe the problem first hand.

Definitions • The basic elements of any theory are its variables. • A variable is a magnitude that can take on different possible values.

Endogenous and exogenous variables • An endogenous variable is a variable that is explained within a theory. • An exogenous variable influences endogenous variables but is itself determined by forces outside theory.

Assumptions • A theory’s assumptions concern motives, physical relationships, lines of causation, and the conditions under which theory is meant to apply, as well as the direction of causation! • The variable that does the causing is called the independent variable and the variable that is caused is called the dependent variable.

Predictions • A theory’s predictions are the propositions that can be deduced from it. • These propositions are then taken as predictions about real-world events.

Models • Economists often proceed by constructing what they call economic models. • More often, a model means a specific quantitative formulation of a theory. • The term ‘model’ is often used to refer to an application of a general theory in a specific context.

Evidence • Economists make much use of evidence, or, as they usually call it, empirical observation. • Such observations can be used to test a specific prediction of some theory and to provide observations to be explained by theories.

Testing the evidence • A theory is tested by confronting its predictions with evidence. • Are events of the type contained in theory followed by the consequences predicted by theory?

Note! Generally, theories tend to be abandoned when they are no longer useful. A theory ceases to be useful when it cannot predict better than an alternative theory. When a theory consistently fails to predict better than an available alternative, it is either modified or replaced.

Theories about human behaviour • So far we have talked about theories in general. • But what about theories that purport to explain and predict human behaviour? • A scientific study of human behaviour is only possible if humans respond in predictable ways to things that affect them. • Is it reasonable to expect such stability?

Think about this! • We humans have free will and can behave in capricious ways if the spirit moves us. • This thus implies human behaviour really is unpredictable! • How is it that human behaviour can show stable responses even though we can never be quite sure what one individual will do?

• Successful predictions about the behaviour of large groups are made possible by the statistical ‘law’ of large numbers. • Very roughly, this ‘law’ asserts that (under a carefully specified set of conditions) random movements of a large number of items tend to offset one another.

Note! • Individuals may do peculiar things that, as far as we can see, are inexplicable. But the group’s behaviour will nonetheless be predictable, precisely because the odd things that one individual does will tend to cancel out the odd things that some other individual does.

Why do economists often disagree? • When all their theories have been constructed and all their evidence has been collected, economists still disagree with each other on many issues.

Sources of disagreement? • There are five possible sources that results in economists disagreeing: – – – Different benchmarking. Different time frames being used. Lack of knowledge. Different values held by economists. Both sides of the problem are justified.

Economic data • Economists seek to explain observations made of the real world. • Real-world observations are also needed to test the predictions of economic theories.

Collecting data • Political scientists, sociologists, anthropologists, and psychologists all tend to collect much of the data they use to formulate and test their theories. • Economists are unusual among social scientists in mainly using data collected by others, often government statisticians.

• In economics there is a division of labour between collecting data and using it to generate and test theories. – The advantage is that economists do not need to spend much of their scarce research time collecting the data they use. – The disadvantage is that they are often not as well informed about the limitations of the data collected by others, as they would be if they collected the data themselves.

Index Numbers • Once data are collected they can be displayed in various ways. • Where we are interested in relative movements rather than absolute ones, the data can be expressed in index numbers.

• Comparisons of relative changes can be made by expressing each price series as a set of index numbers. • To do this we take the price at some point of time as the base to which prices in other periods will be compared. • We call this the base period.

• The formula of any index number is: Value of index in period t = (value in period t/value in base period) × 100

Index numbers – An example Price of cocoa and coffee (average price in each quarter; US cents per kg) Period Cocoa Coffee 2001 (Q 1) 100. 4 146. 7 2001 (Q 2) 104. 5 146. 4 2001 (Q 3 100. 8 129. 7 2001 (Q 4) 121. 8 126. 4 2002 (Q 4) 149. 0 136. 6

Calculation of an index of coffee prices Period Coffee Index 2001 (Q 1) (146. 7/146. 7)x 100 2001 (Q 2) (146. 4/146. 7)x 100 99. 8 2001 (Q 3 (129. 7/146. 7)x 100 88. 4 2001 (Q 4) (126. 4/146. 7)x 100 86. 2 2002 (Q 4) (136. 6/146. 7)x 100 93. 1

Index of cocoa and coffee prices Period Cocoa Index Coffee Index 2001 (Q 1) 100 2001 (Q 2) 104. 1 99. 8 2001 (Q 3 100. 4 88. 4 2001 (Q 4) 121. 3 86. 2 2002 (Q 4) 148. 4 93. 1

Index numbers as averages • Index numbers are particularly useful if we wish to combine several different series into some average. This can be done by: – An un-weighted index – An output-weighted index

Note! An index that averages changes in several series is the weighted average of the indexes for the separate series, the weights reflecting the relative importance of each series.

Price indexes • Economists make frequent use of indexes of the price level that cover a broad group of prices across the whole economy. • One of the most important of these is the retail price index, RPI, which covers goods and services that individuals buy.

• All price indexes are calculated using the same procedure. • First, the relevant prices are collected. Then a base year is chosen. Then each price series is converted into index numbers. • Finally, the index numbers are combined to create a weighted average index series where the weights indicate the relative importance of each price series.

Index of cocoa and coffee prices Period Equal weights Coffee = 0. 9; Cocoa = 0. 1 2001 (Q 1) 100 2001 (Q 2) 101. 9 100. 2 2001 (Q 3 94. 2 89. 6 2001 (Q 4) 103. 7 89. 7 2002 (Q 4) 120. 7 98. 6

Graphing economic data • A single economic variable such as unemployment or GDP can come in two basic forms: • Cross-section • Time-series

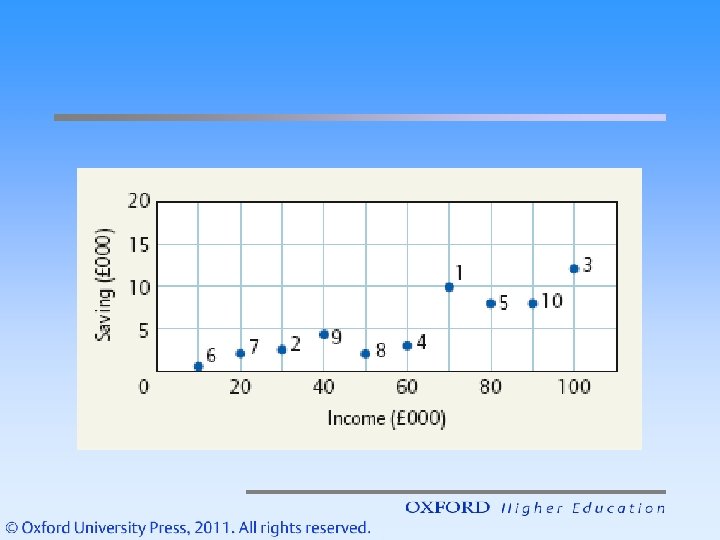

Scatter diagrams • Another way in which data can be presented is in a scatter diagram. • This type of chart is more analytical than those shown previously. • It is designed to show the relationship between two different variables.

• To plot a scatter diagram, values of one variable are measured on the horizontal axis and values of the second variable are measured on the vertical axis. • Any point on the diagram relates a specific value of one variable to a corresponding specific value of the other.

Households Annual income (£) Annual savings 1 70, 000 10, 000 2 30, 000 2, 500 3 100, 000 12, 000 4 60, 000 3, 000 5 80, 000 8, 000 6 10, 000 500 7 20, 000 2, 000 8 50, 000 2, 000 9 40, 000 4, 200 10 90, 000 8, 000

Graphing economic relationships • Theories are built on assumptions about relationships between variables. • How can such relationships be expressed?

• When one variable is related to another in such a way that to every value of one variable there is only one possible value of the second variable, we say that the second variable is a function of the first. • When we write this relationship down, we are expressing a functional relationship between the two variables.

Note! • A functional relationship can be expressed in words, in a numerical schedule, in an equation, or in a graph.

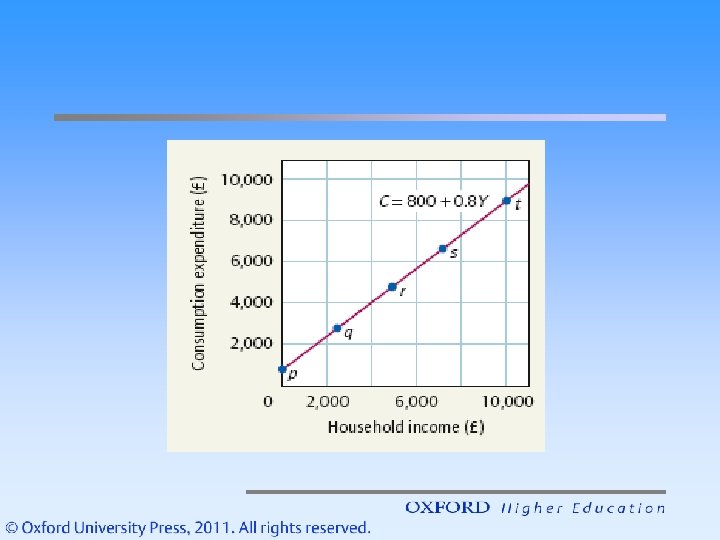

Annual Income Consumption Reference letter 0 800 p 2, 500 2, 800 q 5, 000 4, 800 r 7, 500 6, 800 s 10, 000 8, 800 t

Functions • Let us look in a little more detail at the algebraic expression of this relationship between income and consumption spending. • To state the expression in general form, detached from the specific numerical example shown previously, we use a symbol to express the dependence of one variable on another.

• Using ‘f’ for this purpose, we write C = f(Y). • This is read ‘C is a function of Y’. Spelling this out more fully, it reads ‘The amount of consumption spending depends upon the household’s income. ’

• The variable on the left-hand side is the dependent variable, since its value depends on the value of the variable on the right-hand side. • The variable on the right-hand side is the independent variable, since it can take on any value.

Graphing relationships • Different functional forms have different graphs - When income goes up consumption goes up. • In such a relationship the two variables are positively related to each other.

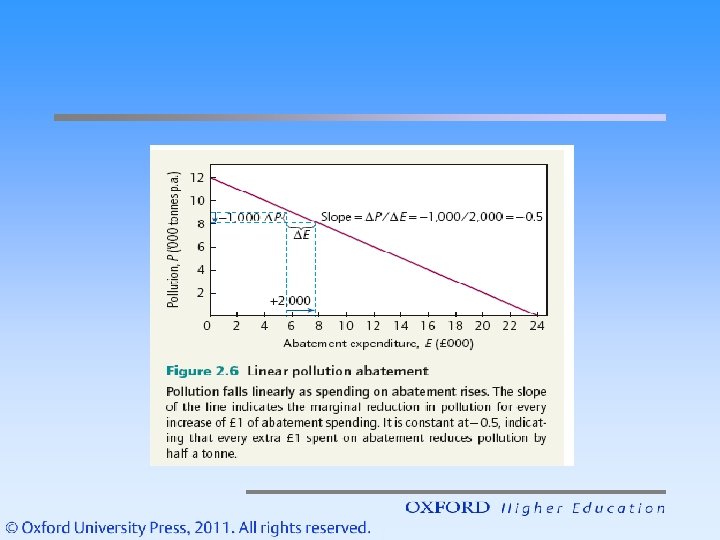

The slope of a straight line • Slopes are important in economics. • They show you how fast one variable is changing as the other changes. • The slope is defined as the amount of change in the variable measured on the vertical or yaxis per unit change in the variable measured on the horizontal or x-axis.

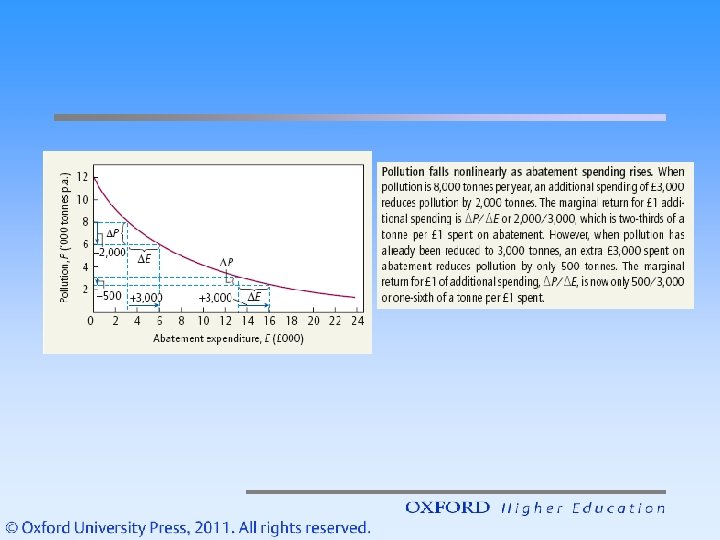

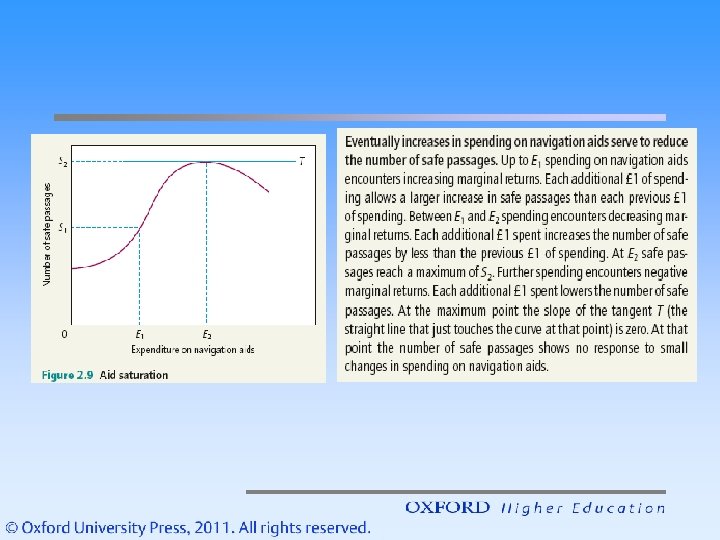

Maxima and minima • So far, all the graphs we have shown have had either a positive or negative slope over their entire range. • But many relationships change direction as the independent variable increases.