Global Airlines James Bolegoh Mauro Horie Richard Konings

Global Airlines James Bolegoh Mauro Horie Richard Konings Zhe Liu Robbie Lydon

Agenda § § § Introduction Southwest airlines Singapore airlines

Airline Products § Provides fast passenger transportation, both nationally and internationally § Freight can also be transported quickly § Substitutes: – Car or bus – Train – Boat

Industry Characteristics § Cyclical in nature, with over expansion during upturns, and large cutbacks during downturns § Only marginally profitable § A special case due to: – Defense – Economic – Flag

Revenue Structure § The two main sources of revenue for Airlines are from: – Passenger fares – Cargo

Flight Crew 7. 1% Fuel and Oil 12.")

Cost Structure DIRECT OPERATING COST (DOC) Flight Crew 7. 1% Fuel and Oil 12. 1% Landing Fees and En-Route Charges 8. 8% 28. 0% Maintenance 10. 4% Depreciation/Rentals/Insurance 13. 2% Total DOC 51. 6% INDIRECT OPERATING COST (IOC) Station and Ground 11. 7% Passenger Services Cabin Attendants 7. 2% Other PAX Services 6. 7% Ticketing, Sales and Promotion General and Administrative Total IOC 13. 9% 16. 6% 6. 1% 48. 4%

World Airline Profits 1992 -2002

Adverse Industry Effects § 9/11, SARS, and Iraq war § The industry was already entering a down period prior to this catastrophic event § Increasing fuel costs began late 2000 § Huge losses and layoffs were announced shortly afterwards § Large decline in the number of passengers

Industry Outlook § § § Recovery from industry shocks Expansion into developing markets Increased use of Alliances

Strategic Alliances § Sharing of resources § Seamless global network § Competitive advantage

International Air Transport Association Market Share

Regulatory Environment § Two key organizations that affect the international airlines are: – International Civil Aviation Organization § Composed of representatives from member countries – International Air Transport Association § Comprised of International Airlines

– To encourage a competitive air")

US Regulatory Impact § Airline Deregulation Act (1978) – To encourage a competitive air transportation system § International Air Transport Competition Act (1979) – 3 goals § Open Skies Agreements

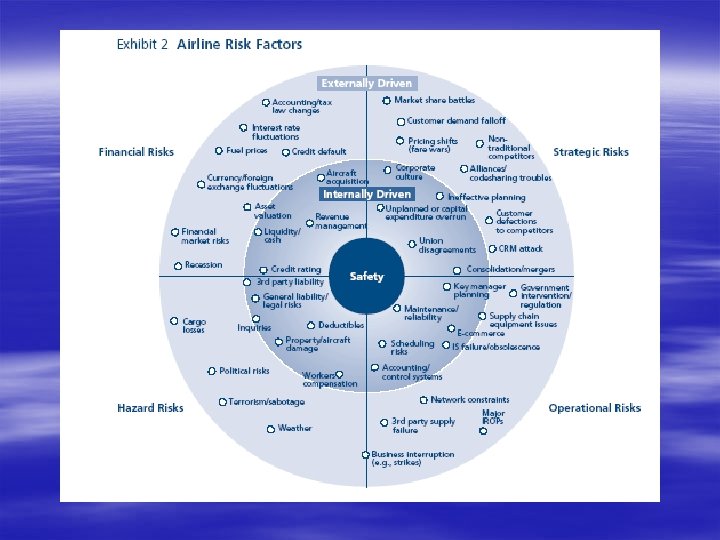

Airline Risk Factors § Financial risk – Variability of revenue and costs § Strategic risk – Business design choices § Operational risk – Tactical aspects of running the business § Hazard risk – Safety of physical assets

What Risks are Hedged? § § Fuel Costs Foreign Exchange Risk Interest Rates Credit Card Guarantees

Southwest Airlines

Section Overview § § § Company background Major risks and risk management Stock options

Company Background § Founded in 1971 with flights between Dallas, Houston and San Antonio § Has become the forth largest major airline in the United States in terms of revenues as of Dec. 2002 § Has been the number one carrier in terms of domestic boardings in the U. S. since May 2003 § Transports more than 64 million passengers per year to more than 58 cities in 30 states

Southwest Route Map

Fact Sheet Daily Departures: 2, 800 flights per day Employees: 33, 000 throughout the system Common Stock: Traded under the symbol LUV at NYSE 2003 Financial Statistics: • • • Net Income: Total Passengers Carried: Total RPMs: Total Operating Revenue: Passenger Load Factor: $442 million $65. 7 million $47. 9 million $5. 9 billion 66. 8%

")

Company Fleet Profile § Southwest operated 388 Boeing 737 Jets (as of Dec, 2003) § Company fleet has an average of 9. 5 years Type Number Seats 737 -200 23 122 737 -300 194 137 737 -500 25 122 737 -700 146 137

$5, 937 $5, 522")

LUV Financial Position 2003 2002 Change Operating Revenues (in millions) $5, 937 $5, 522 7. 5% Operating Expenses (in millions) $5, 454 $5, 104 6. 9% Operating Income (in millions) $483 $418 15. 6% Operating Margin 8. 1% 7. 6% 0. 5 pts Net Income (in millions) $442 $241 83. 4% Net Margin 7. 4% 4. 4% 3. 0 pts Net Income per Share (basic) $0. 56 $0. 31 80. 6% Net Income per Share (diluted) $0. 54 $0. 30 80. 0% Stockholders’ Equity $5, 052 $4, 422 14. 2% 8. 7% 5. 7% 3. 0 pts Return on Equity

LUV Financial Position 2003 2002 Change Revenue Passengers Carried 65, 673, 945 63, 045, 988 4. 2% Revenue Passengers Miles (RPMs) (000 s) 47, 943, 066 45, 391, 903 5. 6% Available Seat Miles (ASMs) (000 s) 71, 790, 425 68, 886, 546 4. 2% Passenger Load Factor 66. 8% 65. 9% 0. 9 pts Passenger Revenue Yield per RPM 11. 97¢ 11. 77¢ 1. 7% Operating Revenue Yield per ASM 8. 27¢ 8. 02¢ 3. 1% Operating Expenses per ASM 7. 60¢ 7. 41¢ 2. 6% 388 375 3. 5% 32, 847 33, 705 (2. 5%) Size of Fleet at Yearend Number of Employees at Yearend

5 -Year Stock Price Evolution 9/11 SARS

Years Ended December 31 2003 Passenger 2002 2001 $5, 741")

Revenue Source (In Millions) Years Ended December 31 2003 Passenger 2002 2001 $5, 741 $5, 379 94 85 91 Other 102 96 85 Total 5, 937 5, 522 5, 555 Freight

Growth § For the five years ended 2001, the average annual capacity growth was 10% § 2002 - over 5% § After 2002, the estimated annualized growth rate over the next 10 years is roughly 8%

Cost Structure Interest expenses 1. 7% 2. 1% 1. 4%

Major Types of Risk Market risk – Fuel price risk – Financial market risk § Interest rate risk § Credit risk § Liquidity and financing risk

Fuel Price Risk § Fuel price risk – Estimated 1. 2 B gallons of jet fuel for 2004. A change of $0. 01 in fuel prices would impact fuel expenses by $12 M – Makes cash flow and earnings unpredictable § Southwest solution - fuel hedging – – Not for trading purposes Effective commodities - crude oil and heating oil Short-term and long-term Mixture of call options, collar structures, and fixed price swap agreements – Hedged 80% of 2004 fuel requirement, 60% of 2005, and portions of 2006 -2007 as of Dec. 31, 2003

Fuel Price Risk Fuel hedging results – Recognized gains of $171 M in fuel expense (Table 1) and unrealized gains of $123 M, net of tax – A net asset of $251 M at the end of 2003 (Table 2) – Sensitivity analysis: 10% change in commodity prices would change fair value of derivative instruments by approximately $125 M and more or less than $125 M of changes in cash flows (as of Dec. 31, 2003)

Fuel Price Risk In Millions 20 20 20 03 02 01 Gains in fuel expense 17 44. 79. 1 5 9 Total 83 76 results 77 fuel Fuel hedging expense 0 2 1 - Table 1

Fuel Price Risk Fuel hedging results - Table 2

Financial Market Risk § Financial market risk – – – Interest Rate Risk Credit Risk Liquidity and Financing Risk § Southwest strategy – – Capitalize conservatively Grow capacity steadily and profitably Strong B/S and modest financial leverage High credit rating - “A” with S&P’s rating; “Baa 1” with Moody’s rating on senior unsecured fixed-rate debt

Interest Rate Risk § Debt § Short-term investment § Leasing

– Changes in interest rate affect")

Interest Rate Risk § Interest rate risk (debt) – Changes in interest rate affect I/S and cash flow; may result in insolvency and bankruptcy § Southwest solution – Low debt strategy § Total debt - $1. 55 B; low D/E ratio: 0. 30 (AMR: 12. 86, DAL: 16. 33, JBLU: 1. 65) – Market sensitive instruments § Fixed rates and modest financial leverage ($475 M) § Interest rate swaps ($760 M) § Prepayment, redemption or termination for floatingrate debt ($222 M)

– Agreement 1: pay LIBOR")

Interest Rate Risk § Interest rate swap agreements (2003) – Agreement 1: pay LIBOR + a margin every 6 month and receive 6. 5% every 6 month on $385 M senior unsecured notes; due Mar-2012 – Agreement 2: pay LIBOR + a margin every 6 month and receive 5. 496% every 6 month on $375 M, 5. 496% pass-through certificates; due Nov-2006

– Total cash and cash")

Interest Rate Risk § Interest rate risk (short-term investment) – Total cash and cash equivalents of $1. 87 B as of Dec. 31, 2003 – Parallel closely with floating interest rates – Affects earnings and cash flow § Southwest solution – Invests in certificates of deposit, highly rated money markets, and investment grade commercial paper – No additional actions to cover interest rate market risk and other material market interest rate risk management activities

– Total PV of leasing payments")

Interest Rate Risk § Interest rate risk (leasing) – Total PV of leasing payments (2004 after): § Capital leasing - $91 M § Operating leasing - $2. 5 B – Aircraft leases can be renewed at the end of the lease term for one to five years – However, leases are not considered market sensitive financial instruments and not included in the interest rate sensitivity analysis

Interest Rate Risk § Results – No significant exposure to changing interest rates on fixed-rate debt – A liability of $18 M - interest rate swap – Sensitivity analysis: 10% percent change would affect net earnings and cash flows by less than $1 M (floating-rate debt, invested cash, and shortterm investments) – An increase in rates has a net positive effect

Credit Risk § Credit risk – Nonperfomance by the counterparties associated with outstanding financial derivative instruments – Results in credit loss § Southwest solution – Selects and periodically reviews counterparties based on credit ratings – Limits the exposure to a single counterparty – Monitors the market position – Agreements with seven counterparties (early termination rights, bilateral collateral provisions, security requirements) § Results – No counterparties fail to meet their obligations

Liquidity and Financing Risk § Liquidity and financing risk – – Agreements with financial institutions (credit card transactions) Credit facility Outstanding debt agreements May reduce the availability of cash or increase the costs to keep the agreements § Southwest responsibility – Maintaining minimum credit ratings – Maintaining minimum assets fair values – Achieving minimum covenant ratios for available or outstanding debt agreements § Results – The company met or exceeded the minimum standards set forth in the agreements

Risk Management Governance § No specific committee or RMO for Southwest’s risk management.

Other Potential Risks and Uncertainties § War risk § Competitive factors § General economic conditions § Factors to control costs § Operational disruptions

Stock Options § Stock-Based Employee Compensation covers: – Majority of employee groups – Board of directors – Plans related to certain contracts with certain executive officers of the company

Stock Options § Two classes of employee stock plans: – Collective bargaining plans § Subjective to collective bargaining agreements § Granted at or above pair value § Normally have terms ranging from 6 to 12 years § No executive nor member of the Board of Directors are eligible to participate in this plan § Not required to be approved by Shareholders

Stock Options – Other employee plans § Not subjective to collective bargaining agreements § Granted at fair market value § Have 10 -year terms and become fully exercisable after three, five or ten years § Need to be approved by shareholders

Stock Options Outstanding Options Exercisable Range of Exercise Prices Options outstanding at 12/31/02 (000 s) Weighted average exercise price Options exercisable at 12/31/02 9000 s) Weighted average exercise price $3. 30 to $4. 99 50, 811 $4. 05 38, 717 $4. 01 $5. 11 to $7. 41 3, 341 5. 85 2, 586 5. 91 $7. 86 to $11. 73 14, 247 9. 84 6, 548 9. 94 $12. 11 to $18. 07 61, 369 13. 85 14, 738 14. 01 $18. 26 to $23. 94 8, 404 19. 65 3, 068 19. 91 $3. 30 to $23. 94 138, 172 9. 99 65, 657 7. 67

Weighted average exercise")

Stock Options Outstanding Options Exercisable Options outstanding at 12/31/02 (000 s) Weighted average exercise price Options exercisable at 12/31/02 (000 s) Weighted average exercise price Collective Bargaining Plans 104, 020 $9. 51 52, 733 $6. 77 Other Employee Plans 34, 152 $11. 47 12, 924 $11. 33 $3. 30 to $23. 94 138, 172 9. 99 65, 657 7. 67 Option Plan Shares Outstanding: 790 million Stock Price: $14. 33

Singapore Airlines

Section Overview § § Background Financials Risks Stock options

SIA Facts § Founded in 1972 § SIA’s passenger network covers 60 cities in 33 countries § Singapore Airlines Cargo offers a network linking 68 cities in 36 countries, making it the 2 nd largest international cargo airline § Average number of employees: 14, 418 § Passengers carried: 15, 326, 000

The Group § Subsidiaries and Associated Companies – Singapore Airlines Cargo – SIA Engineering Company (SIAEC) – Singapore Airport Terminal Services (SATS) – Silk. Air – Singapore Flying College – Singapore Aircraft Leasing Enterprise (SALE)

Awards and Accolades § Forbes – Made the world’s best companies ranking – Top 10 travel and transport companies § Fortune – Ranked 21 st in world’s most admired companies – Most admired airline

Group Fleet Profile Owned Leased Total in use On order On option Aircraft operated by SIA 78 18 96 31 51 Aircraft operated by SIA Cargo 9 3 12 5 9 Aircraft operated by Silk. Air 8 1 9 7 2 95 22 117 43 62 Group Total

Average Fleet Age

Revenue Composition

Cost Structure The Group 2002 -03 2001 -02 EXPENDITURE Staff costs 22. 9% 21. 0% Fuel costs 19. 0% 20. 9% Depreciation 11. 1% 11. 5% Provision for impairment of fixed assets 0. 4% 0. 0% Aircraft maintenance and overhaul costs 8. 0% 6. 6% Commission and incentives 6. 9% Landing, parking and overflying charges 5. 9% 6. 3% Handling charges 5. 3% 6. 5% Rentals on lease of aircraft 3. 7% Material costs 3. 2% 3. 7% Inflight meals 2. 2% 2. 6% Advertising and sales costs 2. 1% 2. 3% Insurance expenses 1. 8% 1. 2% Company accommodation and utilities 1. 4% 1. 7% Other passenger costs 1. 3% 1. 4% Crew expenses 1. 0% 1. 2% Other operating expenses 3. 7% 2. 6%

Passenger and Cargo Carried

Company Revenue and Expenditure

5 -Year Stock Price Evolution SIAL. SI 9/11 SARS

Temasek Holdings (Private) Limited 691, 451, 172")

Major Shareholders Number of shares % 1) Temasek Holdings (Private) Limited 691, 451, 172 56. 76 2) Raffles Nominees Pte Ltd 138, 233, 298 11. 35 3) DBS Nominees Pte Ltd 103, 163, 701 8. 47 4) HSBC (Singapore) Nominees Pte Ltd 44, 419, 799 3. 65 5) Citibank Nominees Singapore Pte Ltd 41, 961, 826 3. 44 6) DB Nominees (S) Pte Ltd 24, 130, 937 1. 98 7) United Overseas Bank Nominees Pte Ltd 21, 890, 687 1. 8 8) Oversea-Chinese Bank Nominees Pte Ltd 6, 917, 092 0. 57 9) Morgan Stanley Asia (Singapore) Securities Pte Ltd 6, 661, 881 0. 55 10) Chang Shyh Jin 3, 929, 000 0. 32 1, 082, 759, 393 88. 89% Total

Financial Risk Management Objectives and Policies § Financial and commodity risk – Market risk § Jet fuel price risk § Foreign currency risk § Interest rate risk § Market price risk – Counterparty risk – Liquidity risk § Other possible risk

Market Risk § Jet fuel price risk – A change in price of US$0. 01 per American gallon of jet fuel affects the Group’s annual fuel costs by US$13. 1 million § Jet fuel price risk management – Swaps and options contracts hedged up to 24 months forward

Market Risk cont. § Foreign currency risk – Foreign currency 78. 4% of total revenue – Largest exposures are from USD, UK Sterling Pound, Japanese Yen, Euro, Swiss Franc, Australian Dollar, New Zealand Dollar, Indian Rupee, Hong Kong Dollar, Taiwan Dollar, Chinese Yuan, Korean Won, Thai Baht and Malaysian Ringgit (surplus) – Exposure from USD (deficit) due to capital expenditure, leasing costs and fuel costs

Market Risk cont. § Foreign currency risk management – Matching policy, as far as possible, receipts and payments in each individual currency – Surpluses of convertible currencies are sold, as soon as practicable, for USD and SGD – Forward foreign currency contracts to hedge

Market Risk cont. Derivative Financial Instruments 2003 2002 6 months or less 524. 4 268. 6 Over 6 months to 24 months 363. 0 314. 4 887. 4 583. 0 6 months or less 399. 5 304. 3 Over 6 months to 24 months 233. 9 176. 8 633. 4 481. 1 (33. 4) 14. 4 Foreign currency contracts Jet fuel swap/option contracts (Losses)/gains not in FSs

Market Risk cont. § Interest rate risk – Changes in interest rates impact interest income and expense from short-term deposits and other interest-bearing financial assets and liabilities

Market Risk cont. § Interest rate risk management – Interest-bearing financial liabilities with maturities above one year have predominantly fixed rates of interest – If this is not the case they are hedged by matching interest-bearing financial assets in which case interest rate swaps are used to convert interest income into the same floating interest rate basis as interest expense – Interest swap agreements are in place with notional amounts ranging from $50. 8 million to $70. 2 million whereby SIA pays a fixed rate of interest and receives a variable rate linked to LIBOR

Market Risk cont. § Market price risk – Potential loss resulting from a decrease in market prices – The Group owned $454. 6 million (down 1. 5% from 2002) in quoted equity and non-equity investments – Estimated market value of these investments was $522. 9 million

Counterparty Risk § Surplus funds invested in interest-bearing bank deposits and other high quality short-term liquid investments § Counterparty risks are managed by limiting aggregated exposure on all outstanding financial instruments to any individual counterparty, taking into account its credit rating § These exposures are regularly reviewed, and adjusted as necessary

Liquidity Risk § The Group had cash and short-term deposits of $819. 9 million (down 25% from 2002) § Available short-term credit facilities of $1, 550 million (down 8. 8% from 2002) § These are expected to be sufficient to cover the cost of all firm aircraft deliveries due in the next financial year § Additional financing through structured leases, bank borrowings, or public market funding

Financial and Commodity Risk cont. Derivative Financial Instruments Total carrying amount on Balance Sheet Aggregate net fair value 2003 2002 Long-term investments 569. 6 590. 4 637. 8 631. 1 Short-term investments 148. 3 34. 2 148. 4 37. 4 1, 100. 0 1, 197. 8 1, 086. 2 Financial assets Financial liabilities Notes payable Derivative financial instruments Foreign currency contracts * * (31. 1) (3. 4) Jet fuel swap contracts * * 9. 2 17. 6 Jet fuel options contracts * * (11. 5) 0. 2 * No balance sheet carrying amounts are shown as these are commitments as at year end.

Other Possible Risk § Risk management committee’s of the different subsidiaries and associated companies create the ability to react to unforeseen events such as – 9 -11 – SARS – Iraq war – Bali bombing

Risk Management Governance SIA Board of Directors Board Audit and Risk Committee SIA Group Risk Management Committee SIAEC SATS Group Silk. Air SIA Cargo Other Subsidiary RMC RMC RMC

Stock Options § SIA Share Option Plan – Employee Share Option Scheme § 99. 1% of options offered in 2002 – Senior Executive Share Option Scheme § 0. 9% of options offered in 2002

Stock Options cont. § All Stock Options – Terms no longer than 10 years – Price is determined by average 5 days prior to date of grant – Timing § Employee – must wait 2 years to exercise § Senior Executive – 1 year wait for access to 25%, and an additional 25% per year thereafter

Exercisable Price")

Stock Options cont. Date of Grant Exercisable Period Balance (Dec 31. 03) Exercisable Price March 28, 2000 March 28, 2001 – March 27, 2010 13, 126, 430 $15. 34 July 3, 2000 July 3, 2001 – July 2, 2010 11, 868, 350 $16. 65 July 2, 2001 July 2, 2002 – July 1, 2011 13, 173, 990 $11. 96 July 1, 2002 July 1, 2003 – June 30, 2012 13, 658, 152 $12. 82 51, 826, 922 $14. 17 Total Outstanding & Average Price 609, 072, 000 shares in the market

Stock Options cont. § SIA Subsidiaries Share Option Plan – SATS § 61, 799, 200 outstanding 100, 588, 000 shares in the market – SIAEC § 60, 301, 000 outstanding 100, 444, 000 shares in the market

Summary § Industry overview § Firm specific examples – Southwest Airlines – Singapore Airlines

? ? ? ? Questions ? ? ? ?

- Slides: 82