General Ledger General ledger accounts The general ledger

- Slides: 18

General Ledger

General ledger accounts • The general ledger is a detailed summary of all the account a business has and what transactions has taken place in that account. • Each general ledger accounts looks as shown below Account Name Debit Side Credit Side

The rules that apply to the accounting equation applies to the general ledger:

Owners Equity

• Remember Accounts increase on the + side and decrease on the – side. • The + and – is determined by the rules shown in the previous slides • In the following slides we are going to show you the steps of completing a general ledger 1. Identify the accounts (assets, liabilities, owners equity) and on which side it increases and decreases. 2. Post the opening balances. 3. Post al CRJ transactions 4. Post al CPJ transactions 5. Close all the accounts

Remember the following • When posting from the CRJ debit bank and credit all other accounts • When posting form the CPJ credit bank and debit all other accounts

CASH RECEIPTS JOURNAL OF INQAYIZIVELE TRADERS – JUNE 2011 Doc Day 001 1 CRR 3 002 13 CRR Details Analysis Bank of receipts Sales Cost Sundry Accounts of Amount Fol Sales Details 50 000 Capital A. S Mapeka Sales 50 000 3 400 Makopo B. G Sales 3 000 5 000 8 000 5 000 4 000 2 500 2 000 45 000 CRR 22 Sales 003 27 A. S Mapeka 3 400 2 720 3 000 45 000 108 900 10 900 8 720 98 000 Commissio n income Capital

STEP 1 : IDENTIFY THE ACCOUNTS AND ON WHAT SIDE IT INCREASES AND DECREASES.

Step 2: Post the CRJ. DEBIT BANK in details write total receipts we use the total at the end of the month

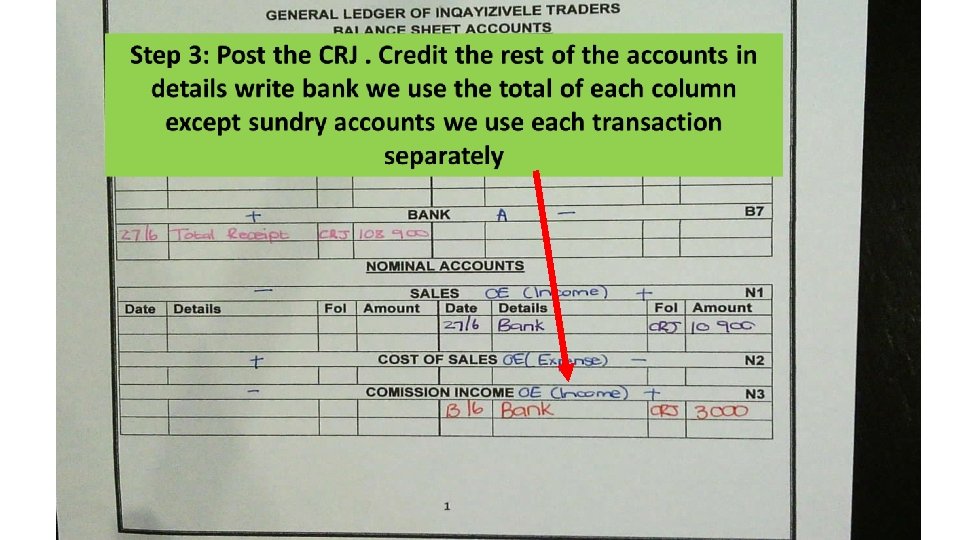

Step 3: Post the CRJ. Credit the rest of the accounts in details write bank we use the total of each column except sundry accounts we use each transaction separately

Step 3: Post the CRJ. Credit the rest of the accounts in details write bank we use the total of each column except sundry accounts we use each transaction separately

In the CRJ cost of sales and Trading stock are recorded separately they always work together like shown below

CASH PAYMENTS JOURNAL OF BOITUMELONG– JUNE 2011 Doc Day Details 100 2 101 3 102 6 Municipality N. T Hlongwane Mogane Bank Tradin Equipm Sundry Accounts g ent Amou Fol Details stock nt 350 Trading licence 1 800 1 500 300 Stationary 2 000 4 150 2 000 1 500 650

STEP 1 : IDENTIFY THE ACCOUNTS AND ON WHAT SIDE IT INCREASES AND DECREASES.

Step 2: Post the CPJ. CREDIT BANK in details write total payments we use the total at the end of the month

Step 3: Post the CPJ. DEBIT the rest of the accounts in details write bank we use the total of each column except sundry accounts we use each transaction separately

Step 3: Post the CPJ. DEBIT the rest of the accounts in details write bank we use the total of each column except sundry accounts we use each transaction separately