GCU Since 1892 GCU is a familyoriented organization

")

- Slides: 23

GCU Since 1892

GCU is a family-oriented organization with a rich history; committed to serving the foundational financial interests of members of all ages. Its roots extend back to 1892, when a little over 700 immigrants from East Central Europe combined their meager assets of about $600 to form the Fraternal Benefit Society. Their guiding principle was to help each other in time of need. Since 1892, GCU has successfully managed its assets, thus earning the trust of its members. They, in turn, respond by introducing others to the benefits of GCU membership. GCU may have grown to a billion dollar company, but its goals today are still the same as the vision of its founders. GCU actively protects families by offering insurance products that insure the lives of its valued members, and annuity products that protect a family’s financial future as well. GCU also offers fraternal programs that gives members the chance to collaborate in social, athletic and fundraising activities. Many of the fundraising efforts are aimed at improving services in our members’ local communities. Many things have changed since its founding in 1892, but GCU’s fundamental goals remain the same. As its mission statement reads:

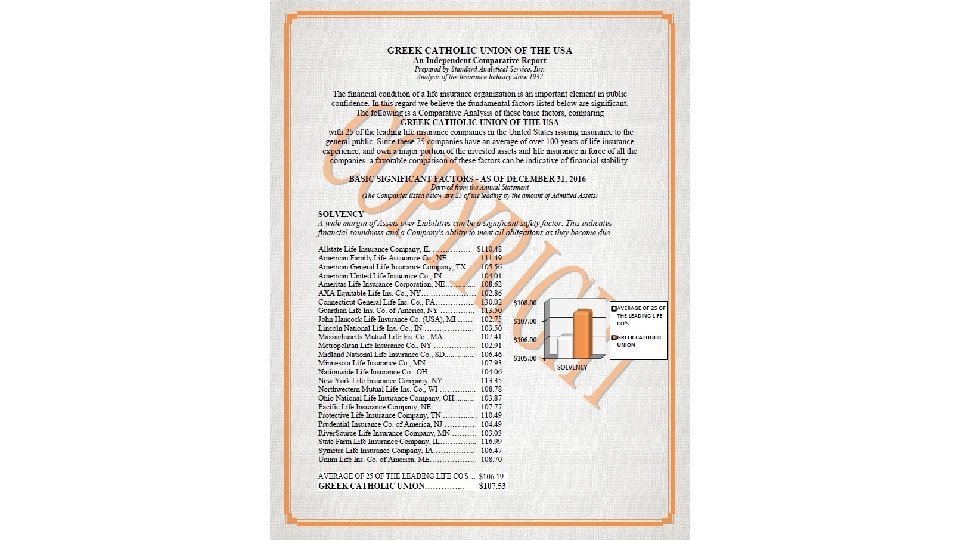

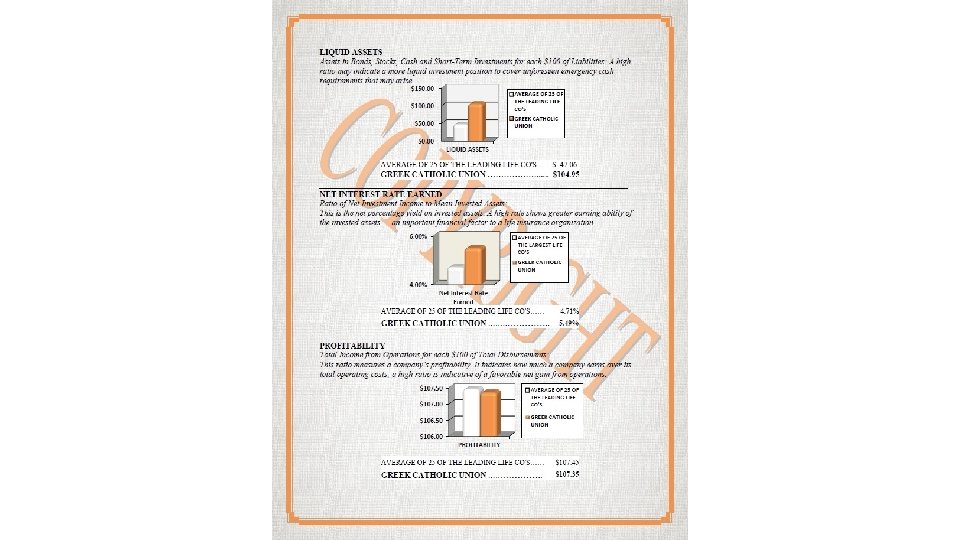

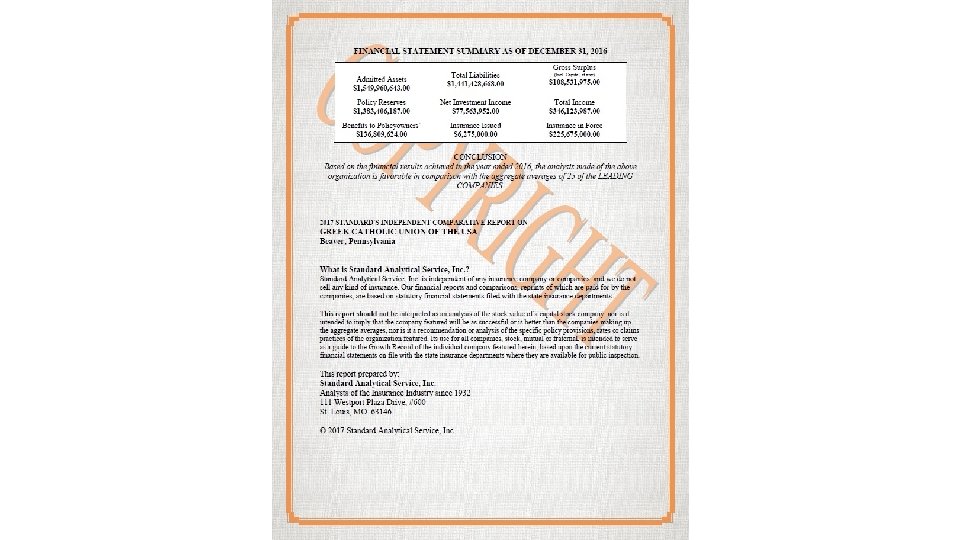

Summary of Financial Statistics Ending Second Quarter 6/30/17 6/30/16 $1, 673, 179, 000 $1, 451, 037, 000 $119, 718, 000 $100, 766, 000 107. 9% 107. 5% Assets Surplus (Net Worth) Normal Solvency Solvency (Inc Spec Reserves) 110. 7% 110. 0%

Note: NV, KS, MO and TX approved for Annuity Only

Life Insurance • • Single Premium Whole Life Ordinary Whole Life 20 Year Payment Whole Life Annual Renewable Term 10 Year Renewable and Convertible Term 20 and 30 Year Level Term Irrevocable Life Insurance Burial Trust for Final Expense Planning Simplified Issue Whole Life Program

• Annuities • • • Option A One Plus Four Triple Advantage Five Year Advantage Flex 8 • Single Premium Immediate Annuities • Life Income Options • Fixed Period Certain Options

The following slides contain an overview of GCU’s Annuity Products. *Issue ages are based on “age LAST birthday”. *SPIA contracts are based on “age CLOSEST birthday”. *Individual Contracts may be subject to certain annual deposit limits. *As a “Membership Group”, GCU Annuities: 1. May only have a single annuitant (Except Joint and Survivor SPIAs). 2. May only have a single individual or entity as owner. 3. Ownership may be assigned. 4. Where eligible, surrender charge free withdrawals are ALWAYS based on the account’s value at the BEGINNING of that contract year. 5. All Investments are backed by the Company’s Reserves. 6. GCU complies with all standards set forth for a Legal Reserve Company.

Option A *Minimum Single Premium Deposit: $5, 000 *Issued to Age 121 *Complete Liquidity from Day One! (NO Surrender Charges) *Guaranteed Minimum Crediting Rate of 1. 0% *Actual Crediting Rate Can change on a month to month basis, based on the “New Issue Rate”. *Interest Distributes at least at the end of every contract year. *Client may elect monthly, quarterly, semi, or annual direct deposit of their interest. *May not accumulate interest on a deferred basis. *NO Early Distribution Penalty for ages under 59 ½. *Can NOT be added to. (But a client could have multiple accounts. ) *May only be used for Non-Qualified Funds. *Partial Withdrawals Permitted! ($50 min withdrawal. May not draw account below $5, 000 without closing)

One Plus Four *Technically, a 5 Year Chassis *Issued to Age 121 *Guaranteed Minimum of 1. 0%. *Minimum initial deposit: $300. May be added to at any time, subject to any limits that are in place. *30 Day “Window” (13 th Contract Month). During the window, the client may: 1. Surrender the contract without surrender charge. 2. Surrender the contract and go into a new One Plus Four. 3. Surrender and go into any other GCU Annuity that they age qualify for. 4. Continue in the contract for the remaining 4 years. *No surrender charge free withdrawals permitted during the first 12 months. *Clients who continue the contract for the remaining 4 years have 10% surrender charge free withdrawals in years 2 to 5 based on the account value at the beginning of the contract year. *May be used for Qualified and Non-Qualified Funds.

Triple Advantage *36 Month Contract with all 3 Years guaranteed at the initial crediting rate. *Issued thru age 95. *Guaranteed minimum rate of 1. 0%. *Minimum initial deposit: $300. May be added to at any time, subject to any limits that are in place. *No surrender charge free withdrawals permitted during the first 12 months. *Years 2 and 3, 10% surrender charge free withdrawals are permitted. *May be used for Qualified and Non-Qualified Funds.

Five Year Advantage *Issued thru age 88. *Minimum initial deposit: $300. May be added to at any time, subject to any limits that are in place. *Guaranteed Minimum rate of 2. 0% *Initial Crediting Rate Guaranteed for the first 2 contract years. 1. Years 3 to 5 are guaranteed at the contractual minimum. 2. GCU has NEVER failed to pay the initial crediting rate in all 5 years. *10% Surrender Charge Free Withdrawals in year 1. *20% Surrender Charge Free Withdrawals in years 2 – 5. *Excellent for clients who wish to begin systematic withdrawal of interest! *May be used for Qualified and Non-Qualified Funds.

Flex 8 *Issued thru age 80. *Minimum initial deposit: $300. May be added to at any time, subject to any limits that are in place. *Guaranteed Minimum rate of 3. 0% *Initial Crediting Rate is guaranteed for the first 12 contract months. 1. Months 13 to 96 The rate may NEVER go below 3%. May change on a month to month basis based on the new issue crediting rate to the Flex 8 Contract. *Responds to a rising interest rate environment with no action required by the client! *10% Surrender Charge Free Withdrawals in EACH contract year. *Excellent for clients who wish to begin systematic withdrawal of interest! *May be used for Qualified and Non-Qualified Funds.

Annuity Crediting Rates – December 2017

GCU Single Premium Whole Life *Issued through age 85 ½. *Minimum Face Amount: Issue Age 0 to 21 - $25, 000; 22+ = $15, 000 *Excellent for Final Expense and Wealth Transfer Planning! *Wealth Transfer 1. Excellent Initial Death Benefit per dollar of premium. 60 Yr Old, Male, Non-Tobacco Usage, with $100, 000 Premium = $201, 613 of Initial Death Benefit. 2. If IDB is $100, 000+, the Guaranteed Surrender Value will equal the deposit by the end of year 2! 3. As a result, Guaranteed Surrender Values at subsequent years tends to be higher than other companies. 4. Max Deposit is $150, 000 without prior H. O. approval.

GCU’s Irrevocable Life Insurance Burial Trust The GCU Irrevocable Life Insurance Burial Trust (IBT) provides much needed life insurance planning for final expenses, while offering protection from unforeseen expenses later…. It’s ADVANCED final expense planning! Currently, this is a full-underwriting program, but you will find a great death benefit per dollar of premium. In conjunction with The Shoreline Agency and Marketing Group, GCU is working on a limited underwriting version. May be used with SPWL, Ordinary Whole Life and 20 Year Payment Life.

GCU’s Irrevocable Life Insurance Burial Trust WHY it’s a good idea: * Assets in an IBT are not considered “countable” assets by Medicaid. * Your clients can pre-pay for a funeral without choosing a specific funeral home, or even visiting one. * Funded with Whole Life insurance, an IBT has immediate, tax free growth. * Death benefits avoid probate. * An IBT cannot be surrendered, dissolved, or reversed. * Your client’s wishes are carried out. * Your clients work directly with YOU, their trusted advisor. Features: * Avoid “Medicaid Spend down” issues. * Completely portable. * Tax free and bypasses probate * Irrevocable

GCU’s Simplified Issue Whole Life Program * * * No Medical Exam Simplified Underwriting Process Minimum Issue of $5, 000 Up to $25, 000 in Coverage Issued ages 50 to 80 (Age Closest Birthday) Available in AZ, CA, CT, FL, IN, MD, MI, MN, NJ, OH, PA, WV, WI, and VA, with other states coming soon! * NO annual certificate fee

Single Premium Immediate Annuities *Single Life Income Options Life – No Refund Life w/ 5, 10, 15, 0 r 20 Years Certain. *Joint and Survivor Income Options. 100%, 66%, and 50% Survivor. Period Certain Options Available. *Fixed Period Certain Options from 2 to 20 Years. *Current “Settlement Rate” generates an excellent “Payout Rate” based on age and gender. *No period certain may extend past the annuitant’s Life Expectancy based on the IRS Life Expectancy Tables.

Why YOU Should Become Appointed With GCU Through The Shoreline Agency and Marketing Group • EXPERT Training and Guidance on GCU Products and Procedures (One of our principals is the former VP of Sales and Marketing, and our Agency has accounted for over $200, 000 in GCU production!) • BEST Commissions! If you go direct with GCU, commissions are up to 33% LESS than what Shoreline can make available to you.

Thank You! The Shoreline Agency and Marketing Group West Coast Office 27201 Puerta Real, Suite 300 Mission Viejo, CA 92691 877 -322 -0407 Jeff@SAMGMarketing. com East Coast Office 1106 Ohio River Blvd, Suite 604 Sewickley, PA 15143 844 -322 -0407 Scott@SAMGMarketing. com Info@SAMGMarketing. com The Shoreline Agency and Marketing Group is dedicated to providing you with the most expert advice on GCU products, and offering you the highest commissions available!