Focus on Financial Vulnerability Responding to Financial Vulnerability

Focus on Financial Vulnerability Responding to Financial Vulnerability in Nottingham 25 th May 2018

Purpose of today’s workshop • • • To make sure NCC uses its funds effectively to help people affected by financial difficulty / money problems To look at how the City as a whole can work to help people at risk or experiencing financial difficulty To listen to your feedback, and your ideas

Agenda 9: 35 am Why is financial vulnerability important? 9: 55 am The current situation in Nottingham 10: 20 am Workshop 1: What’s being delivered / where are the needs? 11: 00 am BREAK 11: 15 am Tackling financial vulnerability – scope of work 11: 35 am Workshop 2: Making the most of efforts and resources 12: 15 pm Open discussion – reflections and commitments Peter Morley and Shade Agboola, CPH Bobby Lowen, Emma Bates, Geoff Oxendale and Peter Morley, Bobby Lowen, Dr Shaun French, Veronica Fairley

Why is Financial Vulnerability Important?

Issues Affecting Citizens in Poverty or who are Financially Vulnerable Emotional Health Bereavement Sexual Exploitation Eviction Persistent Runaways Physical Health Learning Difficulties Mental Health Debt Smoking Cold housing Drugs & Alcohol Financial Vulnerability Neglect Poor Nutrition Poor Parenting School Exclusion NEET Teenage Pregnancy School Exclusion Worklessness Anti-Social Behaviour Non School Attendance Offending Behaviour

Services That Could be Involved With Citizens in Poverty or who are Financially Vulnerable Social Care (Referrer) Police (Referrer) APAS (Alcohol Service) Elected Member Connexions ASB Team Job Centre Plus Welfare & Debt Advice Service Secondary School Primary School Paediatrician Youth Service Counselling Education Welfare (Referrer) Environmental Health Probation Youth Inclusion Project Womens Aid Behaviour Support Team Who is taking responsibility? Diabetes Nurse Financial Vulnerability Youth Offending Team Private Landlord Lead? Co-ordination?

Links between Health and Financial Vulnerability Shade Agboola

What is financial vulnerability? • the degree to which a person is capable of being injured financially when an adverse event happens. • Characteristics include low financial capability, low financial resilience, poor physical or mental health or a disruptive life event. • Half of adults in the UK display at least one characteristic signalling their potential vulnerability to financial harm (FCA)

How does financial vulnerability affect health and wellbeing? • Marmot: Fair Society, Healthy Lives - that action on health inequalities requires action across all of the social determinants of health • Wilkinson: Spirit Level - How almost everything - from life expectancy to mental illness, violence to illiteracy - is affected not by how wealthy a society is, but how equal it is • Skapinakis et al: Longitudinal Study, Socio-economic position and common mental disorders • Stringhini et al: Metanalysis, Socioeconomic status and the determinants of premature mortality • Step. Change survey of debt and health – debt is a contributor to poor health and has been linked to chronic fatigue and obesity

Financial Vulnerability and Poor Health Outcomes in Nottingham Health and Wellbeing Strategy Financial Difficulty: • The most common issue affecting people’s health and happiness in Nottingham (15% of all responses; ‘social isolation’ 2 nd at 12%) • most commonly mentioned barrier to good health and wellbeing (14% of all responses; ‘mental health’ recorded as main barrier in only 5% of all replies) • Common themes: • health ‘not a priority’ • healthy eating / lifestyles ‘too expensive’ • decisions / people not knowing how to manage their money • ‘poverty is the root of all this’

What can we all do? • Access to specialist help • Greater joint working between professionals • Better understanding of the impact of poor health on financial vulnerability and the two way relationship • Ideas from this event!

The Links Between Indebtedness and Other Issues

How we Can Help People in Financial Crisis ‘’Debt advice works, and the earlier people access it the better their chance of reaching good outcomes for themselves and their creditors. We know that high quality debt advice increases an individual’s wellbeing, it improves collection rates for creditors and it boosts the health of communities. The challenge is that most over-indebted people don’t access advice. ’’ (Indebted Lives)

Financial Vulnerability in Nottingham

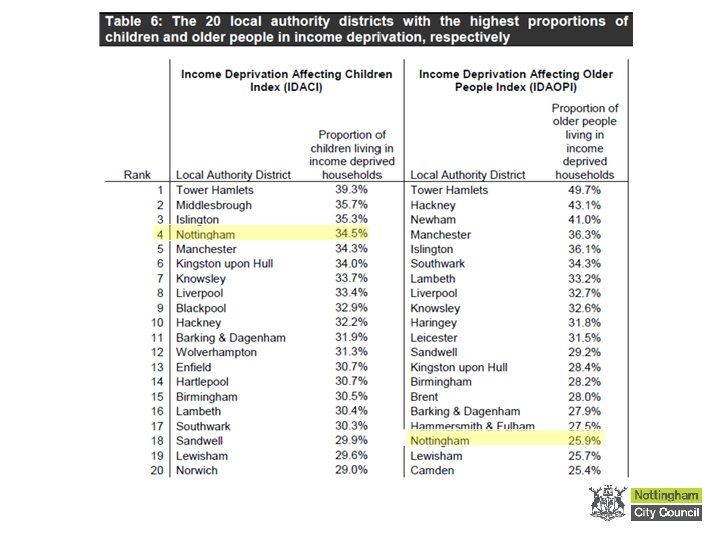

• • • Nottingham ranks 8 th most deprived")

Indices of Multiple Deprivation (2015) • • • Nottingham ranks 8 th most deprived out of the 326 districts in England. 61 of the 182 (one third) City Lower Super Output Areas (LSOAs) fall amongst the 10% most deprived in the country. 110 are in the 20% most deprived. In the Employment Deprivation domain, 54 SOAs rank amongst the 10% most deprived, compared to 34 in 2010 and 35 in 2007. One ward – Aspley – has all LSOAs in the most deprived 20%.

Other measures • Indebted lives: the complexities of life in debt (Money Advice Service, 2013) – 2 nd most over-indebted population (43. 1%) • Levels of over-indebtedness in the UK (MAS & CACI 2017) – 4 th most over-indebted population (21. 9%)

Source: Levels of over-indebtedness in the UK Technical Report, MAS 2017

Source: A Picture of Over-Indebtedness, MAS March 2016

Nottingham Citizens’ Survey Headline: 23. 6% struggling or not keeping up with bills 90% 79. 8% 80% 70% 68. 7% 71. 7% 76. 4% 60% 50% 40% 31. 4% 30% 28. 4% 20. 2% 23. 6% 20% 10% 0% 2014 2015 Keeping up with all bills - without any difficulties 2016 2017 Struggling or not keeping up with bills

Nottingham Citizens’ Survey Headline: 23. 6% struggling or not keeping up with bills Struggling or not keeping up with bills by age 40% 35% 30% 25% 20% 15% 10% 5% 0% 16 -24 25 -34 35 -44 45 -54 55 -64 65 -74 75 and over

Nottingham Citizens’ Survey Headline: 23. 6% struggling or not keeping up with bills Struggling with bills by disability 35% 30% 25% 20% 15% 10% 5% 0% Disabled Not disabled

Nottingham Citizens’ Survey Headline: 23. 6% struggling or not keeping up with bills Struggling with bills by employment status Otherwise not in paid work Retired Full-time education Unemployed Employed/self-employed 0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

Nottingham Citizens’ Survey Headline: 23. 6% struggling or not keeping up with bills Struggling with bills - children under 18 30% 25% 20% 15% 10% 5% 0% Household with children under 18 Without children under 18

Nottingham Citizens’ Survey Headline: 23. 6% struggling or not keeping up with bills • Other factors: • 22. 3% of males, 24. 9% females • 23. 5% of White British people, 23. 8% of people of all other BME backgrounds • 35. 7% of social renters, 19. 8% of private tenants • Nationally: children, lone parents, disability, worklessness, some ethnic groups in particular

Nottingham Citizens’ Survey Headline: 31. 5% don’t know or are unsure of where to get help Understanding where to get help I know where to go Not sure No I don't need help 0% 10% 20% ‘Know where to go’: • 67% White British / 57% BME • 74. 5% social rents / 55. 8% private rents • 53% of 16 -24 year olds • Low in areas 3 & 4 30% 40% 50% 60% 70%

The following slides 31 -50 are from a presentation by Emma Bates, detailing research carried out in Nottingham with people who had recently experienced financial vulnerability.

Helping Prevent and Improve Money Problems; Ensuring We hear People Resident’s perspectives in Nottingham neighbourhoods Research report April 2018, Emma Bates NOTTINGHAM FINANCIAL RESILIENCE PARTNERSHIP

Background • Nottingham Financial Resilience Partnership – one of five underpinning principles: continuous community dialogue • Awards for All funded NOTTINGHAM FINANCIAL RESILIENCE PARTNERSHIP

Aims • hear from people who had struggled with money problems in the last year, to inform work in the city and the local areas, to prevent and address issues • identify how we can continue to enable people’s own voices to be heard, and establish mechanisms for this NOTTINGHAM FINANCIAL RESILIENCE PARTNERSHIP

Method • Semi-structured interviews with people struggling with money in last year, in four areas: - Aspley - Bestwood & Bulwell - Clifton & Meadows - St Ann’s & Sneinton • 38 interviews carried out NOTTINGHAM FINANCIAL RESILIENCE PARTNERSHIP

Main reasons that led to the money problems • Errors, overpayments, confusion • Impact of family members/ relationships • Insufficient income (many with debts + arrears coming out of income) • Job loss • Depression • Moving house • Having existing debts before a financial shock • Indebtedness NOTTINGHAM FINANCIAL RESILIENCE PARTNERSHIP

Whether people had problems affording essential items in last year The extent of the negative impacts of this upon people’s physical and mental health and upon their relationships with friends and family is documented in the report. NOTTINGHAM FINANCIAL RESILIENCE PARTNERSHIP

What could have helped prevent? Benefits related Employment, and more or better employment Better financial capability for younger people Not being over-indebted Need for help and assistance (including knowing about help). • Living costs • Financial abuse • Other • • • NOTTINGHAM FINANCIAL RESILIENCE PARTNERSHIP

What could have stopped it getting worse? • Accessing services • Debt and credit issues • Financial capability Also: • Benefit issues • Better help with work • Money • Not having pressures from friends, family, partner NOTTINGHAM FINANCIAL RESILIENCE PARTNERSHIP

What people felt would help them become more resilient financially/ better able to withstand financial shocks • Income/ job • Financial capability • Saving • Paying off debt and avoiding future debt • Removing the factors (caused by agencies) that hinder people’s ability to plan their money and be financially capable – ie notice, information, stability NOTTINGHAM FINANCIAL RESILIENCE PARTNERSHIP

What people felt would help them become more resilient financially/ better able to withstand financial shocks Also: • Support • Advice and information • Family circumstances NOTTINGHAM FINANCIAL RESILIENCE PARTNERSHIP

Other • It was apparent that many people did not know about local services that could help. Frequently at the close of interview, the interviewer had to give out service contact information. NOTTINGHAM FINANCIAL RESILIENCE PARTNERSHIP

Ways to ensure we hear people’s voices in the future • Range of options needed. Different things work for different people. • Favourites: - Meeting with others in local community; - Regular money drop in sessions; - Facebook page (Nottingham, with links to local area pages) NOTTINGHAM FINANCIAL RESILIENCE PARTNERSHIP

Recommendations 1. DWP, HMRC, NCC Council Tax and social housing providers embed, as an underpinning principle, clear communication and dialogue with their customers throughout their work. Nottingham services to take every step to ensure that their communication never hinders financial capability. 2. Role of relationship dynamics within financial capability considered for further research. NOTTINGHAM FINANCIAL RESILIENCE PARTNERSHIP

Recommendations 3. High profile campaign to increase awareness and understanding of high cost credit versus more affordable sources rolled out. To be effective, both city-wide and within individual neighbourhoods. Also increased access to affordable credit sources in the city. 4. Continued work supporting people to access employment, on campaigning for an increase in Living Wage employers and on continuing to ensure people access benefits they are entitled to. NOTTINGHAM FINANCIAL RESILIENCE PARTNERSHIP

Recommendations 5. Public health services should work closely alongside financial resilience services in view of the direct impacts of financial difficulty upon physical and mental health. 6. Urgent continued action needed by services addressing food poverty, to prevent instances of poor nutrition from occurring. NOTTINGHAM FINANCIAL RESILIENCE PARTNERSHIP

Recommendations 7. Services must work together, to effectively tackle underlying causes of long term food bank use. 8. A high profile, on-going publicity campaign on services that help around money, be rolled out in the city and within neighbourhoods. It should use multiple methods. The Money and Work page on the Ask Lion website should also be linked in to this. Publicity needs to be delivered in such a way that it ‘normalises’ the concept of getting help with money. NOTTINGHAM FINANCIAL RESILIENCE PARTNERSHIP

Recommendations 9. Financial capability provision is both needed and required in Nottingham. Effective approaches should be identified and delivered, drawing from what works. In addition, financial education in schools should continue to be expanded. Specific support should be available for young adults linking in with the current work from Money Advice Service around vulnerable young people. NOTTINGHAM FINANCIAL RESILIENCE PARTNERSHIP

Recommendations 10. The Nottingham Financial Resilience Partnership should explore ways to support people on low incomes to save easily. 11. Making best use of community services and workers, as sources of help and support, should be further explored. NOTTINGHAM FINANCIAL RESILIENCE PARTNERSHIP

Recommendations 12. Regular money drop in sessions/ money hubs combined with opportunities to meet with other local people should be developed in each local area. 13. A Nottingham, city-wide Facebook page on money help should be developed, with possible links to local area specific pages. NOTTINGHAM FINANCIAL RESILIENCE PARTNERSHIP

Recommendations “Importance is if there is any action. This exercise will be pointless if nothing is done. ” (Interviewee) Emma Bates emma@financialinclusionsupport. co. uk 01332 460466 NOTTINGHAM FINANCIAL RESILIENCE PARTNERSHIP

Current Services Provided or Commissioned by NCC • Citizens Advice – City • WRS – Bulwell / City • St. Ann’s • Meadows • Clifton • Law Centre – Hyson Green • Bestwood Outreach Basford, Bestwood, Bilborough (several locations), Aspley, Broxtowe, Beechdale, Strelley, Sneinton

Service Performance – Internal and External 2017/18 £ 18. 9 m in benefits raised £ 4. 2 m in debts managed 16, 164 citizens served £ 1. 6 m cost of internal and external service 17/18 • £ 1 spend = £ 11. 81 benefits raised • £ 1 spend = £ 2. 63 in debts managed • • 2% 21% 41% 35% Assisted Information General help Casework

Current and Future Resource Pressures • NCC lost 2/3 funding over the last five years of austerity • Public Health funding -£ 44 K (Impact in 2018/19) • Mainstream budget -£ 100 K (Impact in 2019/20) • Deaf Society and Refugee Forum

THE NOTTINGHAM JOBS HUB – Linking employers and communities

Mission & Vision Mission To support inclusive economic growth in Nottingham by enabling employers to create and fill sustainable employment and apprenticeship opportunities. To enable these to be accessible to all Nottingham residents, particularly those leaving full-time education and from priority communities. Vision To be a proactive, innovative and sustainable local labour brokerage service providing high-quality account management to employers for all their workforce development and recruitment needs, whilst promoting employment and training opportunities to local jobseekers.

Our Services • Targeted recruitment & vacancy management – free recruitment services for employers with pre-employment training (sbwas), work experience and advertisement of vacancies via our website: www. nottinghamjobs. com, as well as via job centres and partner organisations • Inclusive recruitment and a representative workforce – engaging local employers on their CSR and E&D agendas to encourage positive action in the community and the hiring of staff from groups that are underrepresented in the workforce • Nottingham Jobs Fund (Plus) – Grants of up to £ 3, 500 for employers to create new job opportunities for unemployed city residents that are either apprenticeships or have a specific barriers to accessing employment (e. g. mental health, ex-offenders, long-term unemployed, lone parents, BAME)

The Nottingham Jobs Model LOCAL EMPLOYERS REFERRALS SKILLS REFERRALS JOBSEEKER REFERRALS DWP NATIONAL ACCOUNTS COLLEGES & TRAINING PROVIDERS NCC POLICIES & INFLUENCE DIRECT ENGAGEMENT EMPLOYER ENGAGEMENT TEAM UNIVERSITIES OTHER SPECIALIST / COMMUNITY PARTNERS CASELOAD DEVELOPMENT TEAM DWP JOB CENTRES NOTTINGHAM JOBS COMMUNITY TEAM (NCC) FUTURES - NCS FUTURES – YPT & NOTTINGHAM WORKS COMMUNITY –ABG & NOTTINGHAM WORKS PLUS PROVIDERS

Jobs Hub achievements 2016/17 • Worked with over 450 employers • Delivered over 2, 750 jobs and NJF placements • Supported over 3, 500 work experience placements • Secured over 900 apprenticeships • Helped over 1, 600 individuals to receive accredited training • Winner in the world-wide Financial Times FDI awards 2016 for ‘Recruitment Support’ • Top 5 in any Google search that includes the words ‘Jobs’ + ‘Nottingham’

Ongoing Welfare Pressures • 6, 700 working age DLA claimants to be reassessed for PIP • Benefits freeze – continuing until 2020. • Benefits Cap – currently affecting 520 households • Reduced benefits for new claimants (ESA work related, Child Tax Credit etc)

Universal Credit • Full Service begins in October 2018 – all new claimants of JSA (income based), ESA (income based), Income Support, Tax Credits and Housing Benefit. Also any existing claimant whose circumstances change. • Full transition of existing claimants by 2022. • Around 65, 000 working age adults and 50, 000 dependent children will claim Universal Credit at full rollout. • UC less generous for some groups – families, especially those with more than 2 children, some disabled people, self employed etc. • Greater conditionality for many claimants particularly lone parents and working claimants.

Impacts of UC • Initial 5 week delay, transition to monthly payments, HB element paid to claimant - Rent arrears - Landlords reluctant to rent to UC clients - Reduced payments as advances and arrears recovered through UC - Council Tax arrears - Eligibility for Free School Meals

Impacts of UC • Administered online - Access to internet - Affordability - Digital skills • Self Employed - Inability of UC to adapt to irregular earnings, minimum income floor • Moving existing payments to UC - Shift to monthly payments for those with low/no savings

Knock on impacts • Increased debt. • Increased demand for services – advice, housing, budgeting, health, foodbanks, childcare, libraries, employment etc. • Reduced income and higher costs for Council, NCH, Housing Associations. • Wider range of people engaging with services • New skills needed within services.

Ongoing Welfare Issues • 6, 700 working age DLA claimants to be reassessed for PIP • Benefits freeze – continuing until 2020. • Benefits Cap – currently affecting 520 households • Reduced benefits for new claimants (ESA work related, Child Tax Credit etc)

Universal Credit • Full Service begins in October 2018 – all new claimants of JSA (income based), ESA (income based), Income Support, Tax Credits and Housing Benefit. Also any existing claimant whose circumstances change. • Full transition of existing claimants by 2022. • Around 65, 000 working age adults and 50, 000 dependent children will claim Universal Credit at full rollout. • UC less generous for some groups – families, especially those with more than 2 children, some disabled people, self employed etc. • Greater conditionality for many claimants particularly lone parents and working claimants.

Initial impacts of UC • 20% of claims turned down due to errors • 5 week delay before first payment - high proportion in rent arrears - Council Tax arrears - debt - future payments reduced to cover arrears and advances

Future Impacts • Landlords reluctant to rent to UC claimants – pressure on social housing, homelessness, temporary accommodation • Reduced payments for larger families • Reduced eligibility for free school meals • Self employed receive limited support after first year • Conditions for working claimants • Transfer of existing long term claimants to UC

Impacts for Advice services • Increased demand for services – advice, housing, budgeting, health, foodbanks, childcare, libraries, employment etc. • New benefit system to negotiate • Demands for digital skills, IT infrastructure • Reduced income and higher costs for Council, NCH, Housing Associations. • Wider range of people engaging with services

Workshop 1 – Mapping available help against needs Who is at risk? What are the issues on the horizon? Where are the gaps in support? How do other services (not advice services) consider and address poverty and financial vulnerability? How could this be done better? • Are there any emerging trends around people at risk and/or the issues that people present with? • Please feedback on the service map on your table. Are there any additions? Are there any services that have ended? What’s missing? • •

Tackling Financial Vulnerability: Making the Most of our Efforts and Resources

The Scope of the commissioning Review • Mitigate the impact of the reduction in resources and future demand pressures – Making the best use of available resources • Raise the profile of financial vulnerability and the links to other vulnerabilities • Improve knowledge and skills of frontline staff (across the board) to advise and signpost re financial vulnerability and poverty • Understand the value of the service provided by internal and external services • Seek alternative funding • Improve support into employment • The system will identify and support people earlier, before crisis

Wider opportunities – a programme for change • • • Not just about the advice services / NCC contribution (financial) Wider implications – health, attainment, crime, etc …and wider solutions Opportunities: • Changing behaviours – campaigns, awareness raising

: • Other partners doing their part – landlords, health providers / commissioners,")

Opportunities (cont’d): • Other partners doing their part – landlords, health providers / commissioners, social care, DWP • Leveraging other support – corporate social responsibility, charities, local groups • Leadership – raising the profile across organisations with influence; incorporating in strategies; ‘bringing it together’

Dr Shaun french University of Nottingham")

Nottingham Financial Resilience Partnership (NFRP) Dr Shaun french University of Nottingham

What is Financial Resilience? • Financial resilience • people’s resilience against financial shocks and pressures and ability to withstand these. It is also about resources to make financial choices and improve financial well-being for the longer term. • Financial inclusion • people able to access mainstream financial services, products and advice/ removing barriers • people being having the capability to deal with money well.

Timeline • October 2014: ‘Sorting out Money: How can we improve money problems in Bestwood’ (Bestwood Advice Centre). Action plan and group. • May 2015: ‘Financial Inclusion planning for Nottingham’ (Advice Nottingham, St Ann’s) • Summer 2015: Financial Resilience Core Group: • • • Emma Bates (Financial Inclusion Support) Debbie Webster (Advice Nottingham) Ella Ferris (Nottingham City Credit Union) Shaun French (University of Nottingham) Michael Rowley (Nottingham City Council)

Timeline • Summer 2015: Financial capability and education scoping reports, and meeting • Autumn 2015: Local Financial Resilience events. • • St Ann’s & Sneinton Clifton & Meadows Aspley Bulwell (Jan 2017) • April 2016: Draft Financial Resilience Plan produced. • ‘Improving People’s Financial Resilience in Nottingham’ event (St Nic’s Church) 26 April

Timeline • Summer 2016: Financial Resilience Steering Group established; meeting one a quarter. • February 2017: First Banking Summit (Chaired by Councillor Chapman). • July 2017: the Partnership formally signed up to the Money Advice Service Impact Charter • October 2017: Second Banking Summit • March 2018: Third Banking Summit

Our Vision • Adopting an ‘upstream’ approach to build the financial resilience of individuals and communities – work that prevents people from developing difficulties or from worsening financial difficulties • Key principles: • • • Continuous community dialogue Hub and spoke model High level strategic commitment Cross-sector commitment approach Measuring our impact

NFRP Action Plan • AIMS: 1. Increase income level of people on low income 2. Reduce high cost credit prevalence and use and increase access to low cost ethical credit 3. Increase bank account holding and reduce barriers to accessing banking 4. Increase saving amongst people on low incomes 5. Both children and adults are equipped to be able to deal with money well throughout their life 6. Reduce level of over-indebtedness in the city • OUTCOMES: 7. People able to afford to eat nutritious meals 8. Ensure there is access to affordable warmth

Key Objectives • 1. Increase income levels; • Increase Living Wage Employers. • Increase benefit uptake. • 2. Reduce high-cost and increase responsible credit use; • Increase awareness and publicity campaign. • 3. Reduce barriers to accessing banking; • Raise awareness of ID requirements • Promote basic bank accounts

Key Objectives • 4. increase saving amongst people on low incomes; • Promote children’s savings clubs • Incentivised savings schemes • 5. Improve financial capability; • Promote financial education to all primary schools • Support/training for secondary schools • Increase range of types of financial education approaches available • 6. Reduce level of over-indebtedness in the city; • Increase uptake of debt advice • Increase accessibility, awareness and promote debt advice services.

Changing priorities • First phase of NFRP: • Clear gaps in service provision: • Communities like Aspley • Primary school saving schemes and financial education • Existing ecology of services: e. g. debt advice and financial capability training • Issues: • How to better connect services (Ask. Lion) • How to improve access and take-up Second phase of NFRP: • Awareness and publicity remain real problems • But, service provision is increasingly becoming the most pressing issue; • Significant increase in demand: Universal Credit; Hardship Fund • < Financial Capability provision: e. g. Closure of ‘Sound as a Pound’ programme • < Advice Services: NCC decommissioning of services

Other proposals • Nottingham Charter of Financial Rights/ Financial Citizenship: • • • Right to a Basic Bank Account, Right to save, Right to a financial education and debt advice, Right to responsible credit, Right to financial security. • Fund to abolish Nottingham ‘predatory’ debt: • Establish a local branch of the Hoe Street Central Bank (Walthamstow) (https: //bankjob. pictures/) • Local debt jubilee: Raise money to buy debt of NG residents. • £ 50 K to abolish £ 1 m of local ‘predatory’ debt (in secondary debt market)

• Establish a Nottingham £: • Cf. Bristol Pound • A system of ‘community credit’ • Put unused skills and time to work for community initiatives and services • Value ‘unpaid’ labour • Network of Community Engagement Hubs: • Use community led and trusted spaces like foodbanks to build a ‘one-stop’ shop • Build interlinked network across the city to increase awareness and access to services: debt advice, financial capability, basic bank accounts etc.

• THANK YOU

Children and Families - Impact • Priority Families and social care – new focus on financial vulnerability / capability • Changed practice in rent arrears cases • Upskilled frontline staff working with families • Impact…

Workshop 2 – What Should we be Doing Differently? • How do we use our reduced resources in the best way? • What do we need to prioritise and what is less of a priority? • What could we do more efficiently? • Could we leverage in other sources of funding by working together? • What more can partners do? How can we encourage them? • What else could we (as a city) be doing to tackle financial difficulty? What belongs in our programme?

Open Discussion • Reflections on discussions – key points • What else can you / your organisation do to make your service better equipped to support citizens who are financially vulnerable?

Contact: Bobby Lowen, Commissioning Lead Nottingham City Council alan. lowen@nottinghamcity. gov. uk 0115 876 3571 Peter Morley, Commissioning Manager Nottingham City Council peter. morley@nottinghamcity. gov. uk 0115 876 5163

- Slides: 92