Florida Office of Financial Regulation Bureau of Financial

Florida Office of Financial Regulation Bureau of Financial Investigations

Ponzi vs Pyramid l History/basics of the “Ponzi” scheme l Basics of the “Pyramid” scheme l Warning signs l Why is it important for you to know?

History of Ponzi Schemes Type of illegal pyramid scheme named after Charles Ponzi l Duped thousands of New England residents into investing in postage stamp speculation in the 1920 s(trading in postal coupons for US stamps then exchanged for US Currency) l Created The Security and Exchange Company; offered 40% return to investors in 90 days later increasing return to 100% in 90 days and 50% in 45 days (taking in $1 Million in one 3 hr period…. in 1921 !!!), however, only 30 postal coupons were purchased l

How the Ponzi Scheme Works l l l Works on the “rob-Peter-to-pay-Paul” principle Offers high returns and/or “get rich quick” Money from the new investors is used to pay earlier investors and squandered by the creators of the scheme Although money from the beginning is used to convince others to invest, it eventually fails Results in…………………. .

Most if not all investors never collect the original investment much less the interest promised

Pyramid Scheme A pyramid scheme is a fraudulent system of making money which requires an endless stream of recruits for success. Recruits (a) give money to recruiters and (b) enlist fresh recruits (downline) to give them money. l Promise of “sky-high” returns for doing nothing but handing over you money l Promoters go to great lengths to look like a legit “multi-level” marketing (MLM) program l Claim to have and a product or service to sell l

Pyramid Schemes “Affinity Fraud" when con artists target members of their own race, nationality or religious and job affiliations. l Luke 6: 38: "Give, and it shall be given unto you. " Many claim that law does not apply to them because the investments were "gifts" and the payments to investors, called "blessings, " were not subject to taxes. l

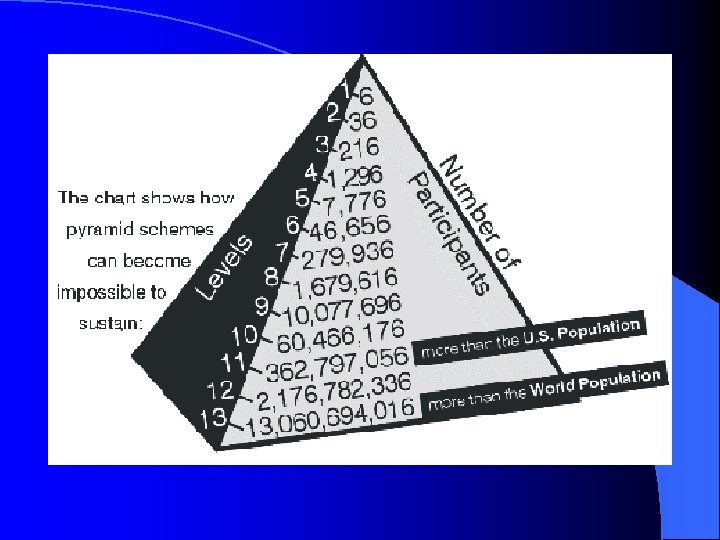

Pyramid Schemes It is true that MLM as practiced by Amway is not an illegal pyramid scheme. Amway has been taken to court for being an illegal pyramid and the courts have ruled that since Amway does not charge people either for joining Amway or for the privilege of recruiting others as distributors, it is not an illegal pyramid. Illegal pyramids and chain letters have no product. l Illegal pyramid schemes are impossible to sustain…there just isn’t enough world population to keep them going and you must continually recruit. l It only takes a few participants to not recruit to cause the entire program to fail l

Warning Signs of Programs l l l l Commissions for recruiting Ask distributors to purchase products/marketing materials Make money through growth of your “downline” Claim to sell miracle products or promise enormous earnings Look for shills- “decoy” references Don’t sign anything in an “opportunity meeting” (High Pressure) Check BBB, State Attorney, State Regulators prior to joining REMEMBER: No matter how good a product or how solid a MLM plan may be, you will have to invest time and money for your investment to pay off.

Why is this important to you? l Believe it or not, you could be the first line of defense l It is the internal auditor/CPA who sometimes sets the internal controls and can be the first to detect the fraud being committed by management or employees.

Case Examples l l l Company “XYZ” operating out of Blue Water Bay (north of Niceville) Collected over $29, 000. 00 in a offshore “Bank Debenture” program Employed CPAs and “book keepers” After seizure of company, employees admitted to knowing what was happening (felt they had no choice) Monitored directed money to off-shore banks and knew investor returns came from new investors Audits occurred but limited by management to investment contracts and invested funds, very limited access to disbursement of company funds

Case Examples l l l Company “ABC” operating out of Ohio, South Florida, and Gulf Breeze, FL. Collected over $110, 000. 00 in a Viatical Settlement Investments Fraud with “Clean and Dirty Sheeting” insured Employed CPAs and Auditors; also used banks to create trust fund accounts to escrow investor dollars Scary part of this case was the fact that bank auditors did not catch the fraudulent activity (fictitious documents; Trust was set up as the beneficiary of the insured policy, funds collected exceeded the face amount of the policy) Bank officer prosecuted for Conspiracy CPAs and Bookkeepers also prosecuted for Conspiracy

Case Examples Red Flags l l l l Overvalued assets; Asset theft or no assets at all Executive corruption False financial statements Conflict of interest (management owned the off-shore banks) Fictitious disclosures to investors (fully insured, trust account, etc…) False statements not related to the financial well being of the company Auditors and CPAs ignored the fact that documents were missing or not provided

Factors contributing to Fraud One WORD!! l GREED Intimidation of employees l Bribery (nice homes, fancy cars, best schools, big paychecks/bonus) l Trust (believed in what the managers/owners were doing, was right and honest) l Criminal intentions (easy money) l

CRIMES INVESTIGATED BY BUREAU OF FINANCIAL INVESTIGATIONS Sale of Unregistered Securities Unlicensed Check Cashers Sale of Securities by Unregistered Persons/Entities Unlicensed Foreign Currency Exchangers Securities Fraud Unlicensed Payment Instrument Sellers Investment Fraud Unlicensed Mortgage Brokers Unlicensed Mortgage Lenders Mortgage fraud Loan Fraud Advance Fee Scams Unlicensed Finance companies Fraud in connection with loan transactions Usury Credit Fraud (limited to the extension of credit & rates) Unlicensed Funds Transmitters/Couriers Deferred Presentment Providers Money Laundering Illegal Banks Bank Fraud Illegal Conduct by Officers/Directors of State Chartered Banks or Credit Unions Retail Sales Fraud (Autos, Mobile Homes, Furniture, etc. . )

453 -7908 Supervisor:")

Pensacola Office 4900 Bayou Blvd, Suite 103, Pensacola, FL, 32503 (850) 453 -7908 Supervisor: Jeff Gulsby Support: Mary Jane Craven Investigators: Kirk Rexroad Jim Strickland Janice Warren Johanne “Jo” Robichaud

FL Department of Financial Services Karen Mason Outreach Coordinator Division of Consumer Services

The Merger A constitutional amendment approved by Florida voters in 1998 consolidated the elected cabinet offices of the treasurer and comptroller, creating the new cabinet post of chief financial officer. In the past, the state treasurer oversaw the Dept of Insurance and served as the state fire marshal. The state comptroller served as the head of the Dept of Banking and Finance. As a result of the merger on 1/7/03, the duties and responsibilities of both departments will fall under the newly formed Department of Financial Services (DFS).

The DFS • Oversees the state’s accounting and auditing functions. • Assists consumers with problems related to financial services, including banking, securities, and insurance. • Appointed regulators oversee rates and regulations in the insurance, banking and finance industries. • Investigates Insurance Fraud, Investment Fraud, and White Collar Crimes.

The Office of Insurance Regulation Public protection is implemented through regulatory oversight of the following: • company solvency • policy forms and rates • market conduct performance • new company entrants to the Florida market.

Division of Consumer Services The Division of Consumer Services serves and protects by providing education, information, and assistance to consumers. The division accomplishes this mission through community outreach programs, a toll-free Consumer Help. Line, and by serving as a mediator between consumers and insurance companies. 1 -800 -342 -2762

Hurricane Season 2004 l Charley l Francis l. Ivan l Jean Over six months later, and we’re still recovering.

The Four Storm Aftermath l Insurance Issues l Recovery Fraud l What did we learn?

Insurance Issues l l l Companies Overwhelmed and Unprepared to handle the number of claims as a result of four hurricanes in one season Adjuster Issues Slow-pay and Low-balling Flood damage vs. wind damage Most claims (93%) have been paid, however…

Recovery Fraud l Contractors: – Taking 75% - 85% Up-front, then skipping town with consumers’ money – Unlicensed in the state / county – even if they do the job, it might not pass county inspection or be insurable unless they are properly licensed! – Not covered by Worker’s Compensation – if the contractor gets hurt while working on your property, you can be held responsible for medical bills!

More Fraud Double Invoicing : l the homeowner submits a phony contractor invoice claiming $2000 from the insurance company for a job that will actually cost only $500. The homeowner and contractor split the extra $1500. If caught, the homeowner and the contractor could both face fraud charges! l Are these guys licensed? ? ?

Consumer Fraud State Charges Cocoa Beach Man with Hurricane Insurance Fraud Tallahassee Democrat, Associated Press 3/10/2005 COCOA BEACH, Fla. - A Cocoa Beach man was charged with insurance fraud for claiming renovation work done to his oceanfront home was the result of damage from Hurricane Frances, state officials said. Robert Milliken, 60, was arrested Tuesday by investigators with the Division of Insurance Fraud, which operates under the state Department of Financial Services. Milliken faces up to five years in prison if convicted. He filed a $60, 000 claim with Citizens Property Insurance Corp. , saying Hurricane Frances caused damage to his home. But state officials determined a contractor had begun work on his home starting Aug. 10, nearly a month before the Sept. 5 storm. The work involved the removal of all of Milliken's furniture as well as the roof and windows.

What did We Learn and what should we do…as Consumers? l Review Your Policy Once a Year and Make Sure You Are Clear on What Coverage You Have – You need to buy enough insurance to protect your insurable interest -- your home and your belongings.

Consumers Had Issues with… l Hurricane Deductibles – $550 or 2%-5% of the Dwelling Value as stated in your policy l Ex: $150, 000 coverage w/2% = $3000 deductible Replacement coverage vs. Actual Cash Value l Your Vehicle is covered by Auto Insurance never by a Homeowner’s Policy l Debris Removal – unless a tree falls on a covered structure, you’ll get little or nothing for this l Claim checks made out to the consumer and their mortgage company l

Consumers Had Issues with… Flooding – for several decades, defined by the insurance industry, at both the state and federal level, as “rising water. ” If water comes up to and over your threshold, regardless of what caused it, the damage is considered flood. Storm surge is included in this flood definition. l Many consumers with flood damage were underinsured or uninsured when it came to flood coverage. l

What Did the Insurance Industry Learn? Before the next Hurricane Season – help consumers understand, in plain English, exactly what their policy covers, and exactly what it does not cover! l When the next hurricane hits, be prepared with: l – Increased number of available Adjusters skilled in Florida building codes and prices – Increased staff, phone, and computer capabilities to handle the increased volume of calls and the increased claim related workload

Hurricane Season Begins June 1, 2005 – Are We Prepared?

- Slides: 33