Finansal Analiz Bir iletmenin mali tablolarn en bata

Finansal Analiz Bir işletmenin mali tablolarını en başta işletme yöneticileri olmak üzere bankalar, alıcılar, satıcılar, devlet ve kamu isteyecektir. Bu mali tablolar işletmenin geçmiş bilgilerini gösterir. Bu bilgilerden yola çıkarak gelecek hakkında tahminde bulunmak ya da işletme ilişkiler kurmak isteyen kişiler bazı analizler yapacaktır. İşte bu incelemeye, finansal analiz denir. Finansal analiz ile birtakım oranlar ve göstergeler kullanılarak işletmenin geleceği hakkında bazı çıkarsamalarda bulunulabilir.

Finansal Analiz Araçları; Finansal analizin araçları, Mali Tablolardır. Finansal tablolar; A- TEMEL FİNANSAL TABLOLAR • Bilanço • Gelir Tablosu • Bilanço ve Gelir Tablosu Dipnotları B- EK FİNANSLA TABLOLAR a) Fon Akım Tabloları b) Özkaynak Değişim Tablosu c) Kar Dağıtım Tablosu, d) Satışların Maliyet Tablosu

TMS 1 Göre Finansal Tablolar Seti; • Bilanço • Gelir Tablosu • Bilanço ve Gelir Tablosu Dipnotları • Özkaynak Değişim Tablosu • Nakit Akış Tablosu

Mali Analiz Sınıflandırılması; 1 - KİMİN İÇİN YAPILDIĞINA GÖRE • İç Analiz : İşletme Personeli Tarafında Yapılan Analiz, • Dış Analiz : 3. Kişi veya Kurumlar Tarafında yapılan Analiz, 2 - KAPSAMINA GÖRE • Statik Analiz : Tek Bir Dönemin Analiz Edilmesi, (Dikey Analiz Tekniği Bir Statik Analizdir. ) • Dinamik Analiz: Birden Fazla Dönemin Analiz Edilmesi, (Karşılaştırmalı ve Trend Analiz Tekniği gibi) 3 - AMACINA GÖRE ANALİZ • Kredi Analizi : Banka Ve Finans Kurumlarınca Yapılır, • Yönetim Analizi : İşletme Yönetimi İçin Yapılan Analiz Türü, • Yatırım Analizi : İşletmeye Yatırım Yapanlar Yapmış Olduğu,

Finansal Tablo Analizlerinde Dikkat Edilecek Durumlar; • • İşletmenin likidite Durumu, İşletmenin Finansal Durumu, İşletmenin Karlılık Durumu, İşletmenin Faaliyet Etkinliği Durumu, ve Gerçeklik…

FİNANSAL ANALİZDE KULLANILAN YÖNTEMLER 1. Oran Analizi 1. 1. Likidite Oranları 1. 2. Mali Yapı Oranları 1. 3. Varlık Kullanım Oranları 1. 4. Kârlılık Oranları 2. Karşılaştırmalı Tablolar Analizi 3. Yatay Yüzde Analizi (Eğilim Yüzdeleri-Trend Analizi) 4. Dikey Yüzde Analizi

1. Finansal Analizde Kullanılan Temel Mali Tablolar • Bilanço • Gelir Tablosu 1. Bilanço İşletmenin belirli bir tarihteki varlıklarını ve kaynaklarını gösteren temel mali tabloya bilânço denir.

Bilânçonun Biçimsel Yapısı; Bilânço biçim olarak dört bölümden oluşmaktadır. • Bilanço başlığı • Aktif tarafı • Pasif tarafı • Bilânço dipnotları • Bilânço sunuş biçimine göre iki değişik şekilde hazırlanabilir. Bunlar: • Hesap tipi • Rapor tipi

AKTİF DV PASİF KVYK UVYK Du. V Öz. K

AKTİF 31. 12. 200. . . TARİHLİ. . . . İŞLETMESİ BİLANÇOSU PASİF 1 -DÖNEN VARLIKLAR 3 -KISA VADELİ YABANCI KAYNAKLAR 2 -DURAN VARLIKLAR 4 -UZUN VADELİ YABANCI KAYNAKLAR 5 -ÖZ KAYNAKLAR AKTİF TOPLAMI NAZIM HESAPLAR PASİF TOPLAMI NAZIM HESAPLAR Hesap Tipi Bilanço

Rapor Tipi Bilanço AKTİF DÖNEN VARLIKLAR DURAN VARLIKLAR AKTİF TOPLAMI NAZIM HESAPLAR PASİF KISA VADELİ YABANCI KAYNAKLAR UZUN VADELİ YABANCI KAYNAKLAR ÖZ KAYNAKLAR PASİF TOPLAMI NAZIM HESAPLAR

BİLANÇODA YER ALAN VARLIK VE KAYNAKLARIN TANIMI • Dönen Varlıklar; Nakit olarak işletme kasasında ya da bankada Tutulan paralar ile bir yıl veya daha kısa süre içinde paraya çevrilebilecek değerler dönen varlıklar grubunda yer alır. Örneğin; • Nakit Para, ( 100 KASA HESABI) • Vadesiz Banka mevduatı, ( 102 BANKALAR HESABI) • Bir Yıldan Kısa Vadeli Alacaklar, (120 TİCARİ ALACAKLAR) • İşletmenin Ticari Malları ( 150 STOKLAR veya 153 TİCARİ MALLAR …. 100 HESAPTA BAŞLAYAN VE 199 HESABA KADAR OLAN BÖLÜM…

Duran Varlıklar; Normal şartlarda bir yıl içinde elden çıkarılması düşünülmeyen, faydaları bir yıl içinde tükenmeyecek varlıklar bu grupta yer alır. Örneğin; (200 HESAP İLE 299 HESAP ARASI) • Demirbaşlar, (255 DEMİRBAŞLAR) • Makinalar, (253 MAKİNALAR ) • Bina, (252 BİNALAR) • Taşıtlar, (254 TAŞITLAR) • Bir yıldan uzun vadeli alacaklar, hisse senedi ve tahviller. (245 BAĞLI ORTAKLIKLAR). . GİBİ. .

Duran Varlıklar; Normal şartlarda bir yıl içinde elden çıkarılması düşünülmeyen, faydaları bir yıl içinde tükenmeyecek varlıklar bu grupta yer alır. Örneğin; (200 HESAP İLE 299 HESAP ARASI ) • Demirbaşlar, (255 DEMİRBAŞLAR) • Makinalar, (253 MAKİNALAR ) • Bina, (252 BİNALAR) • Taşıtlar, (254 TAŞITLAR) • Bir yıldan uzun vadeli alacaklar, hisse senedi ve tahviller. (245 BAĞLI ORTAKLIKLAR). . GİBİ. .

Kısa Vadeli Yabancı Kaynaklar; Bir yıl içinde ödenmesi gereken borçlar kısa vadeli yabancı kaynaklar olarak adlandırılır. Örneğin: • Mali Borçlar, (300 KREDİLER), • Ticari Borçlar, (320 SATICILAR) • Diğer Borçlar, (331 ORTAKLARA BORÇLAR • Borç ve Gide Karşılıkları Gibi. . • … 300 Hesap ile 399 Hesap Arası. .

Uzun Vadeli Yabancı Kaynaklar; Bir yıldan fazla uzun süre içerişinde ödenmesi gereken borçlar Uzun vadeli yabancı kaynaklar olarak adlandırılır. Örneğin: • Mali Borçlar, (400 BANKA KREDİLER), • Ticari Borçlar, (420 SATICILAR) • Diğer Borçlar, (431 ORTAKLARA BORÇLAR • Borç ve Gide Karşılıkları Gibi. . • … 400 Hesap ile 499 Hesap Arası. .

Özkaynaklar; İşletme sahiplerinin veya ortaklarının bilanço tarihinde işletmeye yapmış oldukları sermaye yatırımlarının tutarını gösteren ödenmiş sermaye, sermaye yedekleri, kâr yedekleri, geçmiş yıl karları ve dönem net kârını kapsar. Kısacası; 500 ile 599 arası hesaplar kapsar.

Gelir Tablosu İşletmenin bir faaliyet dönemi içerisinde elde ettiği gelir ve giderleri gösteren faaliyet durum tablosudur. Gelir tablosu hesaplarının alacak tarafı gelirleri, borç tarafı ise giderleri gösterir.

(Karlar) 1. Esas Faaliyetlere (Satışlar) 1. Esas Faaliyetlerden (Satışlar)")

GELİR TABLOSU GİDERLER GELİRLER (Zararlar) (Karlar) 1. Esas Faaliyetlere (Satışlar) 1. Esas Faaliyetlerden (Satışlar) 2. Diğer Olağan Faaliyetlere 2. Diğer Olağan Faaliyetlerden 3. Diğer Olağandışı Faaliyetlere 3. Diğer Olağandışı Faaliyetlerden Gider> Gelir ise ZARAR Gider < Gelir ise KAR Bir işletmenin belirli bir dönemde elde ettiği gelirler ile bunlar için katlandığı giderleri ve bunun sonucunu (K/Z) gösteren mali bir rapordur.

GELİRLER 60 BRÜT SATIŞLAR 600 YURTİÇİ SATIŞLAR 601 YURTDIŞI SATIŞLAR 602 DİĞER GELİRLER 64 DİĞER FAALİYETLERDEN OLAĞAN GELİR VE KARLAR 640 İŞTİRAKLERDEN TEMETTÜ GELİRLERİ 641 BAĞLI ORTAKLIKLARDAN TEMETTÜ GELİRLERİ 642 FAİZ GELİRLERİ 643 KOMİSYON GELİRLERİ 644 KONUSU KALMAYAN KARŞILIKLAR 645 MENKUL KIYMET SATIŞ KARLARI 646 KAMBİYO KARLARI 647 REESKONT FAİZ GELİRLERİ 648 ENFLASYON DÜZELTMESİ KARLARI 649 DİĞER OLAĞAN GELİR VE KARLAR 67 OLAĞANDIŞI GELİR VE KARLAR 671 ÖNCEKİ DÖNEM GELİR VE KARLARI 679 DİĞER OLAĞANDIŞI GELİR VE KARLAR GİDERLER 61 SATIŞ İNDİRİMLERİ (-) 610 SATIŞTAN İADELER (-) 611 SATIŞ İSKONTOLARI (-) 612 DİĞER İNDİRİMLER (-) 62 SATIŞLARIN MALİYETİ (-) 620 SATILAN MAMÜLLER MALİYETİ (-) 621 SATILAN TİCARİ MALLAR MALİYETİ (-) 622 SATILAN HİZMET MALİYETİ (-) 623 DİĞER SATIŞLARIN MALİYETİ (-) 63 FAALİYET GİDERLERİ (-) 630 ARAŞTIRMA VE GELİŞTİRME GİDERLERİ (-) 631 PAZARLAMA SATIŞ VE DAĞITIM GİDERLERİ (-) 632 GENEL YÖNETİM GİDERLERİ (-) 65 DİĞER FAALİYETLERDEN OLAĞAN GİDER VE ZARARLAR (-) 653 KOMİSYON GİDERLERİ (-) 654 KARŞILIK GİDERLERİ (-) 655 MENKUL KIYMET SATIŞ ZARARLARI (-) 656 KAMBİYO ZARARLARI (-) 657 REESKONT FAİZ GİDERLERİ (-) 658 ENFLASYON DÜZELTMESİ ZARARLARI (-) 659 DİĞER GİDER VE ZARARLAR (-) 66 FİNANSMAN GİDERLERİ (-) 660 KISA VADELİ BORÇLANMA GİDERLERİ (-) 661 UZUN VADELİ BORÇLANMA GİDERLERİ (-) 68 OLAĞANDIŞI GİDER VE ZARARLAR (-) 680 ÇALI Ş MAYAN KISIM GİDER VE ZARARLARI (-) 681 ÖNCEKİ DÖNEM GİDER VE ZARARLARI (-) 689 DİĞER OLAĞANDIŞI GİDER VE ZARARLAR (-)

VARLIKLAR GELİRLER VE VE KAYNAKLAR GİDERLER BİLANÇO GELİR TABLOSU 1– 2– 3– 4– 5 6

1 -DEVAMLI SERMAYE ; Uzun vadeli finansman kaynaklarının toplamıdır DEVAMLI SERMAYE= UZUN VADELİ YAB. KAYNAK. +ÖZKAYNAKLAR 2 -NET ÇALIŞMA SERMAYESİ; Kısa Vadeli Borçlar ödendikten sonra, geriye kalan ve İşletmenin faaliyetlerinin sürdürülebilmesinde kullanılan sermayenin büyüklüğünü göstermektedir. NET ÇALIŞMA ERMAYESİ: DÖNEN VARLIKLAR - KVYK

(%17)")

Kaynak Dağılımı Ne Olmalıdır? Kısa Vadeli Yabancı Kaynak Uzun Vadeli Yabancı Kaynak (%33) (%17) Öz Kaynak (%50)

Devamlı Sermaye (%67) Öz Kaynak (%50)")

Devamlı Sermaye Nedir? UVYK (%17) Devamlı Sermaye (%67) Öz Kaynak (%50)

1 -ORAN ANALİZİ Statik bir analizdir. Oran analizinde amaç işletmenin likidite durumu, borç ödeme gücü, finansman şekli gibi bazı önemli bilgilere ulaşmaktır. • LİKİDİTE ORANLARI • FİNANSAL YAPI ORANLARI • FAALİYET ORANLARI • K RLILIK ORANLARI

1 -LİKİDİTE ORANLARI İşletmenin kısa süreli borçlarını ödeyebilme gücünü ve çalışma sermayesinin yeterli olup olmadığını saptayabilmek için kullanılır. En çok kullanılan analiz türüdür. • Cari Oran • Asit - Test Oranı • Nakit Oranı • Stok Bağımlılık Oranı olmak üzere dört farklı likidite oranı vardır.

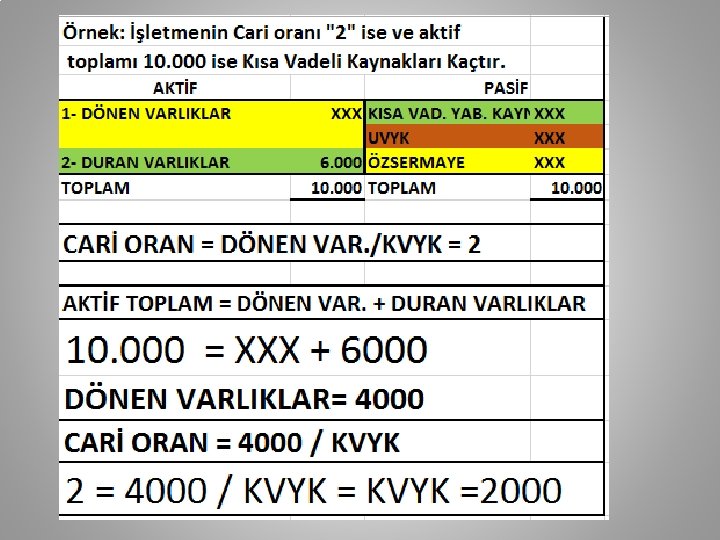

Cari Oran Kısa vadeli borçların ödenmesine bir zorluğun olup olmadığını gösterir. Dönen Varlıklar Cari Oran = -------------------- = 2 olması beklenir. Kısa Vadeli Yabancı Kaynaklar

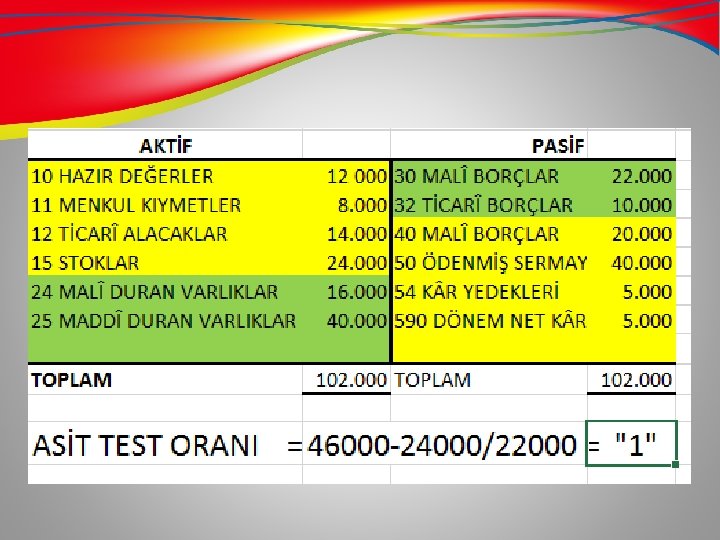

Asit - Test Oranı Dönen varlıklardan stokların çıkarılması sonucu elde edilen değerin kısa vadeli yabancı kaynaklara bölünmesi ile bulunur. Asit –Test oranı 1 olması beklenir. ( Dönen Varlıklar – Stoklar) Asit - Test Oranı = --------------------= 1 Kısa Vadeli Yabancı Kaynaklar

Nakit Oran İşletmeye hiçbir nakit girişi olmaması durumunda elde bulunan nakitler ve menkul kıymetlerle kısa vadeli borçların ne kadarının ödenebileceğini gösterir. Nakit oranının diğer adı disponibilite oranı dır. Oranın 1. 00'ın üzerinde olması arzu edilir. (Hazır Değerler + Menkul Kıymetler) Nakit Oranı =-------------------------= 0, 20 Kısa Vadeli Yabancı Kaynaklar

Stok Bağımlılık Oranı Asit - test oranının 1'den küçük çıkması durumunda kısa vadeli borçların ödenebilmesi için stokların yüzde kaçının satılması gerektiğini belirtir. Yani Nakit İhtiyacı İçin Stokları Yüzde Kaçına İhtiyaç Vardır. [Kıs. Vad. Yab. Kay. - (Hazır Değ. + Menkul Kıy. )] Stok Bağımlılık Oranı =--------------------------- = Stoklar

Bir işletme hakkında kesin bir yargıya varmak")

2 -Faaliyet Oranları (Varlık Kullanım Oranı) Bir işletme hakkında kesin bir yargıya varmak için vade yapısı da izlenmelidir. Örnek= Bir Firmanın Y 1, Y 2, Y 3 yılları aşağıda ki gibi. .

3 -Mali Yapı Oranları Borç ödeme gücünün analizinde kullanmaktadır.

4 - KARLILIK ORANI İşletmenin belirli bir dönemde karlı çalışıp çalışmadığını gösteren oranlardır.

2 -KARŞILAŞTIRMALI ANALİZ TEKNİĞİ İşletmenin birbirini izleyen dönemlerine ait finansal tablolarında yer alan kalemlerdeki değişimlerin değerlendirilmesi için yapılan analiz tekniğidir.

ANALİZİ Eğilim yüzdelerinin yorumu, bilanço veya gelir tablosundaki bir tek")

3 -EĞLİM YÜZDELERİ (TREND) ANALİZİ Eğilim yüzdelerinin yorumu, bilanço veya gelir tablosundaki bir tek kalemin eğilimi esas alınarak yapılmaz. Aralarında anlamlı ilişki kurulabilen, çeşitli kalemlerin eğilimleri bir arada değerlendirilir. Örnek; Satışlar-stoklar; dönen varlıklar-kısa vadeli yabancı kaynaklar;

4 -DİKEY YÜZDE ANALİZİ İşletmenin tek bir Dönemine ait finansal Tablosunda yer alan kalemlerin aynı Tabloda yer alan grup toplamına oranlanarak hesaplanır. Gelecekteki finansal Yapı ve faaliyet Sonuçları analiz edilir.

www. saimgul. com. tr

- Slides: 40