Financial Management RPTS 209 Financial Management includes all

are used to monitor the budget over the")

is useful when you have")

- Slides: 29

Financial Management RPTS 209

Financial Management includes all activities relating to the acquisition and disbursement of funds; budgeting (for a fiscal period or for an event or activity), and analysis and control of fiscal operations.

Budgets are usually seen as limits on funds available for operating an agency or a program—i. e. , you must operate within the budget parameters. Budgets may have discrete categories and transfer of funds from one to another may be prohibited. Categories may include personnel, equipment, supplies, contracted services, utilities, etc. —each has an important role in the overall operation.

Budgets should be balanced—that is, the expenditures should not exceed the income or available funds, and timing of fund availability can impact planning for events. For example, if an event is to be funded through entrance fees, difficulties may be encountered on expenditures needed prior to the event. In such cases, advance ticket sales or sponsorships may be required.

Monitoring the Budget Various instruments (reports) are used to monitor the budget over the designated time periods (annual, seasonal, quarterly, event duration, etc. ) These include the Balance Sheet, Income Statement, Budget and Cash Flow Statements, Project/Program Reports and Break-Even Analysis.

The Balance Sheet--sometimes called the “bottom line”—displays assets, liabilities, and equity. Assets are anything of value, including land, inventory, accounts receivable, and cash on hand. While such things as “good will” and “community support” are assets, they are not financial assets and do not appear on the balance sheet. Liabilities include anything owed—unpaid mortgage or bond indebtedness, bills accrued but not yet paid (“Accounts Payable”), etc. Equity represents the difference between the two—it is the value of the assets in excess of the liabilities.

• On the balance sheet then, the Assets are equal to the Liabilities plus Equity. In the case of independent events (such as a community fair or festival) the balance sheet will be for the event rather than an agency. • Question: Can Equity be a negative figure? If so, what are the implications?

Consider the Balance Sheet for the Francisville July 4 th Celebration shown on the next slide. Land utilities for the event are provided by the Francisville Parks & Recreation Department for a nominal fee of $1, 500, payable after the event. Payments due by vendors and/or sponsors amount to $7, 531; unused supplies have a value of $256; and there is $5, 244 in cash in a local bank account. Equipment valued at $2, 500 (principally a protected fireworks launching pad and secure storage container) will be retained for next year. Accounts payable includes $1, 600 owed to performers and $8, 000 to the fireworks distributor.

Francisville July 4 th Celebration Balance Sheet as of July 31, 2019 Assets Liabilities Current Assets Current Liabilities Accounts Payable $ 9, 600 Cash and investments $ 5, 245 $ 7, 350 Municipal Fees $ 1, 500 Inventory $ 255 Total Current Liabilities $11, 100 Total Current Assets $12, 850 Fixed Assets Equipment $ 2, 500 Equity $ 4, 250 Total Assets $15, 350 Total Liabilities and Equity $15, 350 Accounts receivable

Income Statement • An Income Statement is another instrument used to show the profitability of a facility or program over a specified period of time. • This would include a listing of all major categories of Revenues and of Expenditures. • For the July 4 th Celebration above, the Income Statement might look like this on the following slide.

Francisville July 4 th Celebration Income Statement--July 1 -31, 2019 Revenues Sponsorships/Donations Vendor/Concessions Fees Rentals Total revenues Expenditures Municipal Fees Fireworks Marketing Speaker & Demonstrator Fees Cleanup/Maintenance Volunteer Incentives (T-shirts, drinks, etc. ) Staffing $21, 095 $ 18, 500 $ 1, 200 $40, 795 $ 1, 500 $22, 500 $ 1, 500 $ 2, 000 $ 2, 800 $ 6, 500

Break-Even Analysis • A Break-even Analysis is often used to determine whether or not to offer a program. Consider the following scenario: • A proposal is made to offer a craft course to citizens through the Francisville Park & Recreation Department (art, basket-weaving, or whatever). It will be offered in a room at the Francisville Recreation Center during normal operating hours. The rental of the center operations has been determined to be $30 per hour for the room—including utilities and maintenance. Assume that the course will last two hours per week for 6 weeks. There is then a fixed cost of $360 for the room for this program. Participants will each use approximately $10 in supplies over the 6 weeks (a variable cost), and the cost of the instructor will be billed at $18/hour ($216 total—also a fixed cost). Assume that the program, if offered, will require a minimum of 15 people and can hold no more than 25. The fee charged is $50 per participant.

• This is a chart of the Break-even analysis.

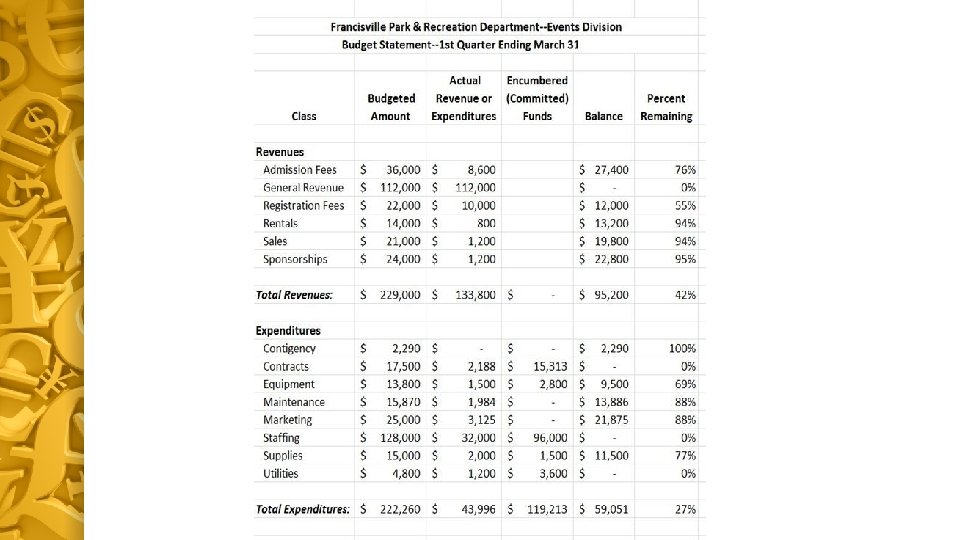

Budget and Cash Flow Statements To effectively manage operations, it is essential to have current information on the budget before the end of the fiscal period. A Budget Statement and a Clash Flow Statement are two tools that enable you to manage more effectively. The Budget Statement is a periodic report which identifies the funds budgeted, the actual amounts received (for revenues) or spent (for expenditures), any commitments on unexpended funds, the remaining balance, and the percent spent or committed.

As the year progresses, you want the Percent Remaining to move toward 0% in each category. Deficits in one area will need to be offset by savings in another. Contingencies will occur, so, if allowed, you may want to include a percentage of your budget in this category. Some funds—such as staffing—may be earmarked for specific positions and are therefore considered to be encumbered when received. Funds for Contract Services would also be considered as encumbered or committed if the contracts have been negotiated or signed.

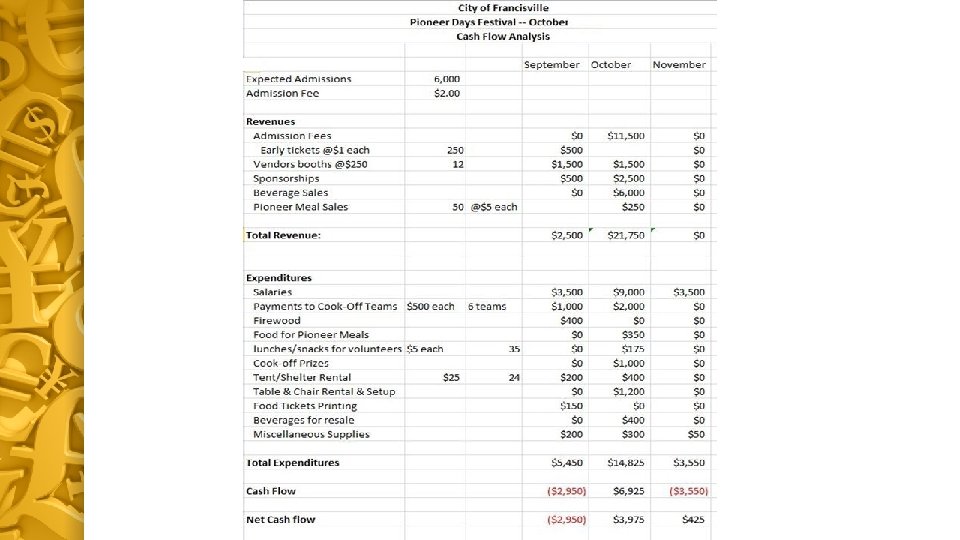

A Cash Flow Statement (a projection or an analysis) is useful when you have a program that is designed to be selfsupporting through user/entrance/admission fees and charges. Since the bulk of your income will be derived from the event itself, you will need to control expenditures before the income flow begins. For a continuing event (annual festival, for example), you may have funds carried over from prior years. For a new event, you will need to secure sponsors (backers) to fund the start-up costs.

The City of Francisville will be sponsoring a Pioneer Days Festival in October. Revenues from early ticket sales and vendor booth reservations as well as limited sponsorship funding will be received in September, but the bulk of revenues will be generated in October. Expenditures will begin in September and continue through November. The following Cash Flow Statement depicts a negative cash flow for September and November, but a positive cash flow for October which will offset those losses and leave a surplus (profit) of $425.

A final fiscal management tool is the project or program report. This will be a report that includes all relevant fiscal information as well as a narrative outline of the project or event, an evaluation of its successes/failures, and notes to guide program directors in the future. This may form part of the overall program evaluation filed where it may be easily retrieved for subsequent events.

The Budget Process Budgets are for a specific period of time with a beginning date and an ending date. These might correspond with the calendar year, the Federal Budget year (October-September), or any other set of dates. In some cases, multiple budgets may be prepared: a revenue budget (expected revenues from taxes, sales, or other), an expenditure budget (which details spending categories and items), a capital budget (for purchase of long-term investments such as land or machinery), project budgets (for various undertakings or events), or a marketing budget (for promotion, advertising, information services).

There are three phases to the budget process: Preparation, Adoption, and Implementation. The format of the final budget will vary, but essentially it will include revenue estimates as well as proposed expenditures, and the two should be balanced. For private or business corporations, profits result when the income exceeds the expenses. In public entities, if income exceeds expenditures, the excess normally reverts to the governing body.

Most budgets will be in the format of the line item budget with object classifications. The following tables and charts on the following pages show the budget for the City of Francisville. Terms used include: Base Budget Zero-Based Budget Beginning Fund Balance Ad Valorem Tax

Base Budget--funds provided to a department, agency, or division at the start of each budget period. The base budget includes funds to maintain the department functions, and is derived from the previous year's budget and any necessary adjustments (such as inflation). Zero-based Budget—Differs from traditional budget in that it is not based on previous budgets—all items must be thoroughly re-evaluated and started fresh from a zerobase. It is based on needs and benefits rather than past history.

Beginning Fund Balance—For the entity as a whole, unspent funds from the previous year’s budget are carried over into the next fiscal budget. For departments or divisions, there will usually be no carryover except for encumbered funds. Ad Valorem Tax—it is a tax based on the value of real estate or (less frequently) personal property. The term technically includes sales taxes, value-added taxes, inheritance taxes, tariffs, and “stamp” taxes. In Parks and Recreation operations, it usually refers only to the “Property Tax”, a major municipal source of revenue.

Sources of Revenue • Revenues can be obtained from: • Compulsory income (property & sales taxes) • Gratuitous income (gifts, grants, sponsorships, bequests) • Earned income (fees, charges and licenses) • Investment income (bank accounts, stocks, etc. ) • Contractual receipts (concessions, etc. ) Funds for major capital expenditures may be obtained by borrowing such as in the sale of bonds.

% of Category General City Budget City of Francisville General Fund Summary Beginning Fund Balance $13, 492, 150 Revenues: Ad Valorem Tax Sales Tax Mixed Drink & Franchise Taxes Licenses & Permits Parks and Recreation Other Charges for Services Fines, Forfeits & Penalties Investment Earnings Miscellaneous Utility Transfer Total Revenues: Total Funds available: $17, 875, 000 $22, 500, 000 $2, 759, 000 $1, 110, 000 $125, 000 $2, 500, 000 $2, 800, 000 $62, 000 $245, 000 $9, 250, 000 $59, 226, 000 $72, 718, 150 30. 2% 38. 0% 4. 7% 1. 9% 0. 2% 4. 7% 0. 1% 0. 4% 15. 6% $17, 750, 000 $14, 500, 000 $8, 200, 000 $5, 955, 000 $1, 100, 000 $3, 150, 000 $3, 950, 000 $3, 010, 000 $4, 600, 000 $62, 215, 000 27. 2% 22. 2% 12. 6% 9. 1% 1. 7% 4. 8% 6. 1% 4. 6% 7. 0% $1, 000 $55, 000 $1, 400, 000 $0 $80, 000 $500, 000 $3, 035, 000 1. 5% 0. 1% 2. 1% 0. 0% 0. 1% 0. 8% Expenditures: Police Department Fire Department Public Works Department Parks & Recreation Department Public Library Planning & Development Services Information Technology Fiscal Services General Government Total Operating Expenditures Other: Public Agency Funding Consulting Services Capital Projects Property Sales/Purchases Other Contingency Total Other Uses Total Expenditures: Ending Fund Balance: $65, 250, 000 $7, 468, 150

Expenditure by Division Parks and Recreation Budget City of Francisville Parks & Recreation Budget Summary Administration Recreation Special Facilities Parks Operations Cemetery Total Current Year $589, 915 $786, 585 $5, 965 $4, 104, 330 $468, 205 Previous Year % Change $490, 851 20. 2% $756, 802 3. 9% $8, 414 -29. 1% $3, 375, 193 21. 6% $403, 283 16. 1% $5, 955, 000 $5, 034, 543 18. 3% Expenditure by Classification Salaries & Benefits Supplies Maintenance Purchased Services Capital Outlay Indirect Costs $3, 130, 780 $551, 060 $856, 225 $1, 245, 150 $79, 425 $92, 360 $2, 521, 880 $330, 154 $647, 078 $1, 353, 033 $97, 373 $85, 025 24. 1% 66. 9% 32. 3% -8. 0% -18. 4% 8. 6% Total $5, 955, 000 $5, 034, 543 18. 3% Personnel (FTE) Administration Recreation Special Facilities Park Operations Cemetery 8. 50 6. 60 0. 00 40. 75 4. 00 8. 50 6. 60 1. 00 37. 50 4. 00 0. 0% -100. 0% 8. 7% 0. 0% Total 59. 85 57. 60 3. 9%