Financial Institutions Who likes what best Savers Simple

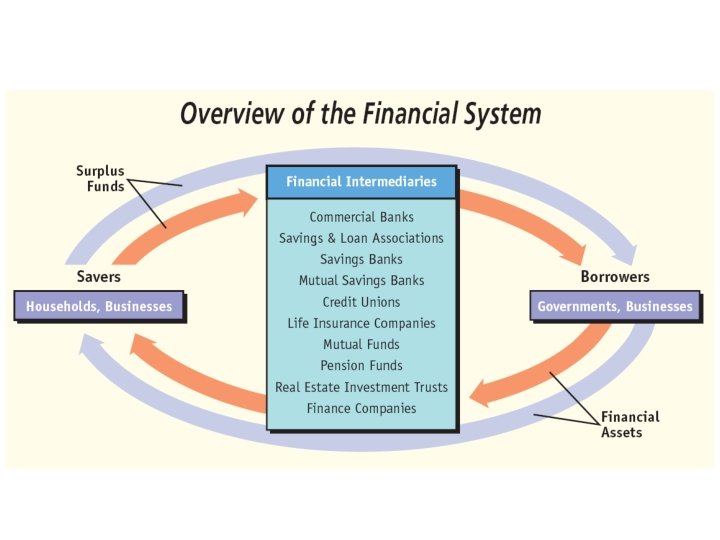

Financial Institutions

Who likes what best? ? • Savers • Simple Interest • Borrowers • Compound Interest

The GREATER the risk, the GREATER the possible return. • • In careers. In relationships. In sports. In investments.

: like a savings account you agree not")

Investment Options • CD (Certificate of Deposit): like a savings account you agree not to withdraw from for a certain period of time. • Mutual Fund: a corporation that exists only to buy stock in other corporations (easy way to diversify) • IRAs & 401(k)s: tax sheltered retirement plans • Bond: JUST A LOAN – to corporation (corporate bond) – to government (Treasury bond) – to local government (municipal bond)

Risk vs. Return Activity • • Risk Return Bonds Stocks Savings Acct’s CD’s Mutual Funds Treasury Bonds

Basic Investment Considerations - Continued The Relationship Between Risk & Return Stocks Bonds Mutual Funds Risk CD’s Savings Accounts Return

Not A Gamble: U. S. Stock Market History • S&P 500 was at 400 in 1993; at 1100 on Feb. 18. If you bought 100 shares of Vanguard 500 in 1993 it was worth $40, 000. today it would be worth $110, 000. Ten shares could have been bought for $4000 and 7 today would be worth $11, 000.

• • • Small Company")

Why Stay with Stocks? Long-Term Annual Returns (1925 -2008) • • • Small Company Stocks: Large Company Stocks: Long Term Corp. Bonds: US Treasury Bills: Inflation: 11. 7% (most risk) 9. 6% 5. 9% 3. 7% (least risk) 3. 0%

Consider Investment Options Around the Room Move to the point in the room that best represents your desired mixture of investments between the ages of 20 and 30.

Consider Investment Options Around the Room Move to the point in the room that best represents your desired mixture of investments between the ages of 50 and 60.

• If you choose to invest money, your two big options are stocks and bonds. • Why is this guy recommending what he’s recommending?

Clicker Quiz

A man has $100 to invest and hopes to receive 10 times the")

1) A man has $100 to invest and hopes to receive 10 times the amount back ($1, 000) by the end of 5 years. This could be BEST accomplished by • A placing the money in a savings account • B depositing the money in a CD • C purchasing $100 worth of stock in a start-up company • D buying $50 worth of bonds and investing $50 in a mutual fund

Bob has $25, 000 that he would like to invest in a diversified")

2) Bob has $25, 000 that he would like to invest in a diversified manner. Bob's BEST investment option to accomplish this goal would be to • A. purchase $25, 000 worth of one company's stock. • B. purchase $25, 000 worth of corporate bonds. • C. purchase $25, 000 worth of shares in a mutual fund. • D. purchase $25, 000 worth of U. S. government securities.

Eric has $2, 000 that he wants to place in a savings account.")

3) Eric has $2, 000 that he wants to place in a savings account. He has researched two accounts, and both pay 3. 5% interest. Account X pays simple interest. Account Y pays compound interest. Eric should choose • A. account X because it would pay tax free interest. • B. account Y because it would pay interest on interest. • C. account X because the interest rate would increase over time. • D. account Y because the interest rate would decrease over time.

Why does consistent investing over long time periods yield large returns for investors?")

4) Why does consistent investing over long time periods yield large returns for investors? • A) Simple Interest • B) Compound Interest

Bonds are most like • • A) stocks B) insurance C) savings accounts")

5) Bonds are most like • • A) stocks B) insurance C) savings accounts D) loans

Which would be the best deal for the borrower on a 2 year")

6) Which would be the best deal for the borrower on a 2 year loan for $5, 000: • A) 7% simple interest • B) 7% compounded monthly • C) 7% compounded quarterly

Which would be the best deal for the lender on a 2 year")

7) Which would be the best deal for the lender on a 2 year loan for $5, 000: • A) 7% simple interest • B) 7% compounded monthly • C) 7% compounded quarterly

End

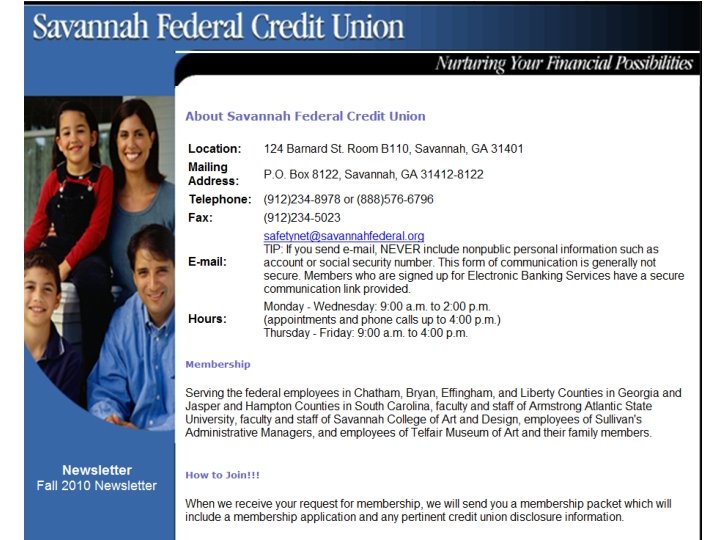

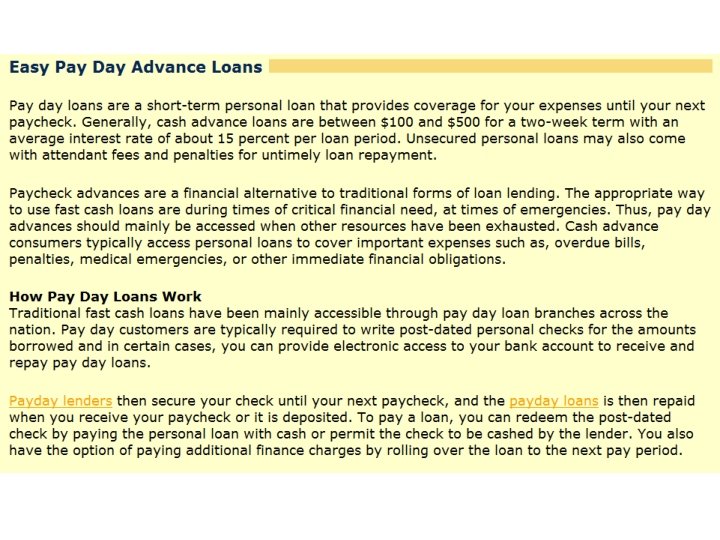

Financial Institutions • Credit Unions – – like banks owned by depositors exclusive club higher rates on savings, lower rates on loans • Payday Loan Company – make small loans at high interest/fees (15% common) – usually, you leave them a post-dated check • Savings & Loan – banks that primarily offer savings accounts & mortgages

Speaker Phone Time Let’s Call These Places

Personal Loan Ranges & Rate Ranges • Payday Loan ________Rate______ • Car Title Pawn ________Rate______ • Finance Company ______Rate______ • Bank ________Rate______ • Credit Union ______Rate______

Current Rate On A $10, 000 5 yr CD • Bank Rate: ____ • Credit Union Rate: _______

Let’s Compare CD Rates. Which one is the bank, and which one is the credit union? A B

The Spread • Interest paid on savings acct’s is < interest charged on loans. • The difference is called the SPREAD.

The Spread • A bank pays 5% interest on its savings account. • The bank takes some of the money deposited in savings accounts, & loans that money out. • On average, the bank charges 11% on its loans. • What’s the spread? Why does the bank do this?

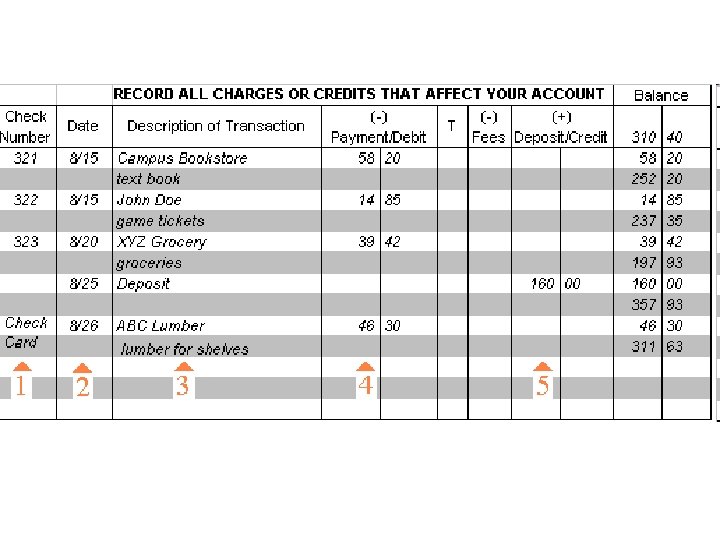

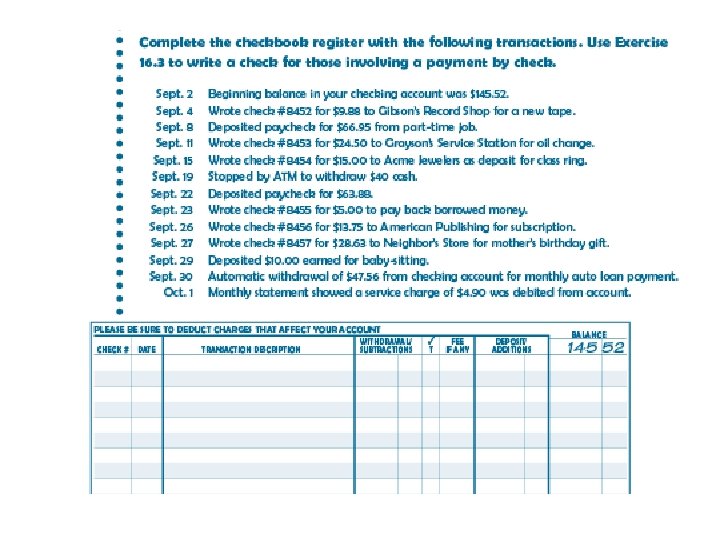

Instructions/Assignments for Thursday & Friday • Checkbook balance worksheet. • Economics Haiku (Draw For Topic) • Use Key To Grade Your Benchmark – mark DGI and SM • Risk/Return Essay • Review Picture (Use Haiku Topic)

Haiku Example • If not for the cat, • And the scarcity of cheese, • I could be content.

“Can I Afford It? ” Video Clip

Borrowers & Lenders Find Your Match!

Who’s Your Middle-Man? ? ?

Financial Institutions Clicker Quiz

1. The interest a bank pays on its savings accounts is generally _____ the interest it earns on loans. • A) the same as • B) lower than • C) higher than

2. A woman is considering purchasing a new lawn mower that costs $120. While employed, the woman does not currently have enough money in her account to pay for this item. Which of the following financial institutions would be the MOST likely to help her buy the lawn mower? • • A payday loan company B credit union C savings and loan D commercial bank

3. Which business would be most likely to offer financing through a finance company? • • A) a dollar store B) a grocery store C) a restaurant D) a furniture store

The main difference between a credit union and a commercial bank is that")

4) The main difference between a credit union and a commercial bank is that • A. only commercial banks offer checking account services to its members. • B. commercial banks make loans, but don't offer checking or savings account services. • C. credit unions don't make home and car loans, whereas commercial banks do make home and car loans. • D. credit unions are only available to specific customers, but commercial banks are available to the everyone.

In order for a bank to have the chance to make a profit,")

5) In order for a bank to have the chance to make a profit, they must • A. charge borrowers a lower interest rate than they charge depositors. • B. pay depositors a lower interest rate than they charge borrowers. • C. charge borrowers a higher fee than they charge to depositors. • D. charge borrowers and depositors the same interest rates.

A bank pays an average of 2% interest on it’s savings accounts and")

6) A bank pays an average of 2% interest on it’s savings accounts and CD’s. The same bank charges an average of 8% on loans. What is the spread? • • A) 2% B) 6% C) 8% D) 10%

End

Federal Reserve Bank of Atlanta What is a bank? Private, for-profit businesses Make loans Hold deposits 11/5/2020 47

Federal Reserve Bank of Atlanta Why Should You Use a Bank? 1. Keep your money safe from loss or theft 2. Make payments easily and inexpensively 3. Maintain records of your financial transactions 4. Deposit your paycheck directly 5. Build savings and earn interest 6. Establish credit 7. Access mortgage loans, car loans, and other products 11/5/2020 48

Federal Reserve Bank of Atlanta Banks help you meet your goals 11/5/2020 Access to: 1. Car loans 2. Credit cards 3. Mortgage loans 4. Student loans 5. Business loans & services 6. Money management services 7. Retirement Savings Accounts 49 8. Remittances & wire

Federal Reserve Bank of Atlanta How do overdrafts and bounced checks happen? When you 11/5/2020 § Write a check, § Withdraw money from an ATM § Use your debit card to make a purchase, or § Make an automatic bill payment or other electronic payment for more than the amount in your checking account, you overdraw 50

Federal Reserve Bank of Atlanta How can you avoid overdraft fees? • Keep track of how much money you have in your checking account by keeping your account register up-to-date • Pay special attention to your electronic transactions. • Don’t forget about automatic bill payments you may have set up for utilities, insurance, or loan payments • Keep an eye on your account balance • Review your account statements each month 51 11/5/2020

Federal Reserve Bank of Atlanta What are “courtesy overdraftprotection plans”? The bank is “covering” your check or withdrawal allowing the check or transaction to clear. You will still pay an overdraft fee or a bounce coverage fee to the bank for each item. You will avoid the merchant’s returned-check fee and will stay in good standing with the people with whom you do business. 11/5/2020 52

Federal Reserve Bank of Atlanta What are other ways to coverdrafts? 1. Link your checking account to a savings account you have with the bank. 2. Set up an overdraft line of credit with the bank. 3. Link your account to a credit card you have with the bank 11/5/2020 53

Federal Reserve Bank of Atlanta Ways to cover your overdrafts Example of possible cost for each overdraft* Good account management $0 Link to savings account $5 transfer fee Overdraft line of credit $15 annual fee + 12% APR Link to cash advance on credit card $3 cash-advance fee + 18% APR Courtesy pay overdraft-fee $20 to $42 (PER CHECK) Bounced check $40 to $60 ($20 to $30 bank fee + $20 to $30 merchant fee PER CHECK) * These costs are only examples. Ask your bank, savings and loan, or credit union about its fees. 11/5/2020 54

Federal Reserve Bank of Atlanta FDIC • Federal Deposit Insurance Corporation • Insures the deposits in commercial banks against loss. • Since its inception in 1933 no depositor has ever lost one cent of FDIC-insured funds Source: www. fdic. gov 11/5/2020 55

Federal Reserve Bank of Atlanta FDIC Basic Coverage Limits: 1. Single Accounts (owned by one person): $250, 000 per owner 2. Joint Accounts (two or more persons): $250, 000 per coowner 3. IRAs and other certain retirement accounts: $250, 000 per owner 4. These limits will expire 1/1/2014 Source: www. fdic. gov/edie/fdic_info. html 11/5/2020 56

Federal Reserve Bank of Atlanta The “Unbanked” and “Underbanked” • 25. 6 percent of American households (about 60 million adults) are unbanked or underbanked. • A breakdown by race shows that 43. 3 percent of Hispanic households, 44. 5 percent of American Indian/Alaskan households and nearly 54 percent of black households are unbanked or underbanked. • At least 71 percent of un- and underbanked households have incomes of $30, 000 per year or less. • The most common reason people offered for not having a bank account was feeling that they did not have enough money to justify one. • About two thirds of unbanked households use one or more of these financial tools: non-bank money orders & check cashing, payday loans, pawn shops, rent-to-own agreements and refund anticipation loans. • About one quarter of unbanked households use none of the aforementioned services, which suggests that cash is their go-to commerce tool. Source: FDIC Report 12/2009 11/5/2020 57

Federal Reserve Bank of Atlanta What Do You Know? 11/5/2020 58

1. People are able to make deposits to and withdrawals from both savings accounts and checking accounts. 1. True 2. False 11/5/2020 59

2. Check-cashing services charge small fees for cashing checks. 1. True 2. False 11/5/2020 60

Federal Reserve Bank of Atlanta FALSE: The fees for check-cashing services vary, but these companies charge either a percentage of the check amount or a minimum fee to cash a check-typically up to $10 each time a check is cashed. If your check is for $100 and you have to pay a $10 fee, you are paying 10 percent of your earnings in fees. 11/5/2020 61

3. Usually, people are able to cash checks for free or for a much reduced fee (less than a few dollars a month) at the bank where they have a savings or checking account. 1. True 2. False 11/5/2020 62

Federal Reserve Bank of Atlanta TRUE: Often students can take advantage of the low or no monthly fees that many banks and credit unions offer to students. A student who has a no-fee student checking account would not pay a fee to cash a check. If savings or checking accounts do have fees, they rarely add up to more than a few dollars a month. Therefore, the monthly fees, if any, for a basic savings or checking account are usually less than the fee charged by a check-casing service to cash just one check. 11/5/2020 63

4. There are fees or costs associated with savings and checking accounts. 1. True 2. False 11/5/2020 64

Federal Reserve Bank of Atlanta TRUE: There are fees associated with checking accounts. For example, there are fees for ordering checks and fees if you bounce a check, i. e. , have an “overdraft, ” or use a debit card when there isn’t enough money in the account. There may also be fees if you are required to keep a certain amount (a “minimum balance”) in your account and you don’t. If you lose a check and ask the bank to issue a “stop-payment order” for the check so that someone doesn’t find it and then forge your name and 11/5/2020 65 cash it, you’ll also be charged a fee.

5. Savings accounts pay interest on the balance in the account. 1. True 2. False 11/5/2020 66

Federal Reserve Bank of Atlanta TRUE: Keeping your savings in an account that earns interest is a way to make your savings grow. 11/5/2020 67

6. It isn’t legal for companies to require employees to use “direct deposit. ” 1. True 2. False 11/5/2020 68

Federal Reserve Bank of Atlanta FALSE: It is legal and many companies do have this requirement. Businesses actually consider direct deposit to be an employee benefit because direct deposit is considered to be more convenient, safer and more efficient then cashing paper checks. 11/5/2020 69

7. With a checking account, you can write checks to pay for many types of goods and services. 1. True 2. False 11/5/2020 70

Federal Reserve Bank of Atlanta TRUE: If you want to write a check to pay for your school yearbook, you can do so if you have a checking account. If you have to pay your own car insurance, you can write a check. 11/5/2020 71

8. There are no fees associated with savings accounts. 1. True 2. False 11/5/2020 72

Federal Reserve Bank of Atlanta FALSE: There may be fees associated with a savings account. You may be required to have a minimum balance. If the amount in your account falls below that amount, you may be charged a fee. There may be a limit on how often you may make a withdrawal from a savings account. If you make a withdrawal more often, you may be charged a fee. 11/5/2020 73

9. You may use an ATM or debit card with both savings and checking accounts. 1. True 2. False 11/5/2020 74

Federal Reserve Bank of Atlanta TRUE: You can make arrangement with your bank to have a debit card that you can use to make withdrawals and deposits from both checking and/or savings accounts. 11/5/2020 75

10. Banks are a safe place to keep your money. 1. True 2. False 11/5/2020 76

insures deposits")

Federal Reserve Bank of Atlanta TRUE: The Federal Deposit Insurance Corporation (FDIC) insures deposits in bank accounts up to $250, 000 person per institution. 11/5/2020 77

- Slides: 77