Financial Control Measures Financial Control Measures v Concept

PFM in general incorporates the management of government")

28+3 Thematic Groups and Indicators Score IV.")

28+3 Thematic Groups and Indicators Score C.")

of control § Physical, § Human, § Information")

v")

- Slides: 32

Financial Control Measures

Financial Control Measures v Concept v Objectives v Process v Tools v Exercise 2

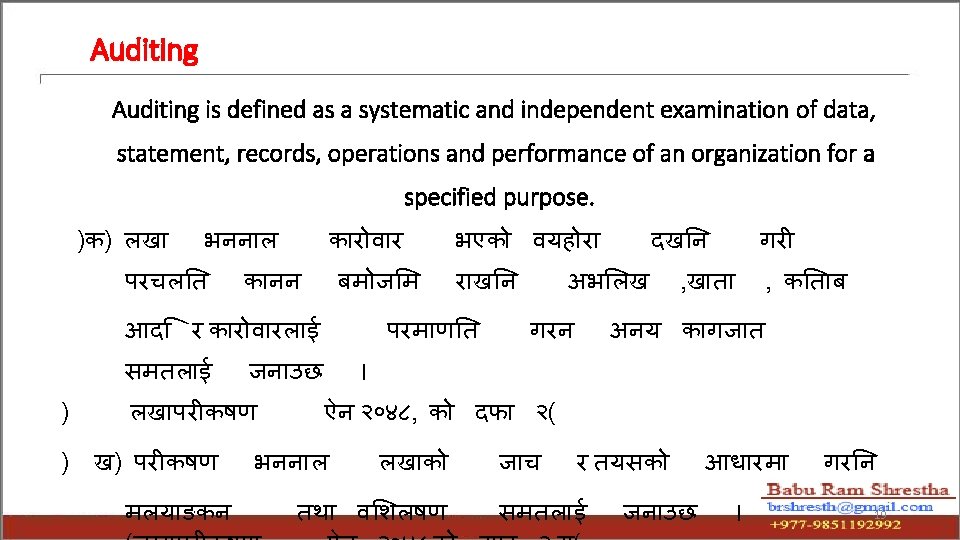

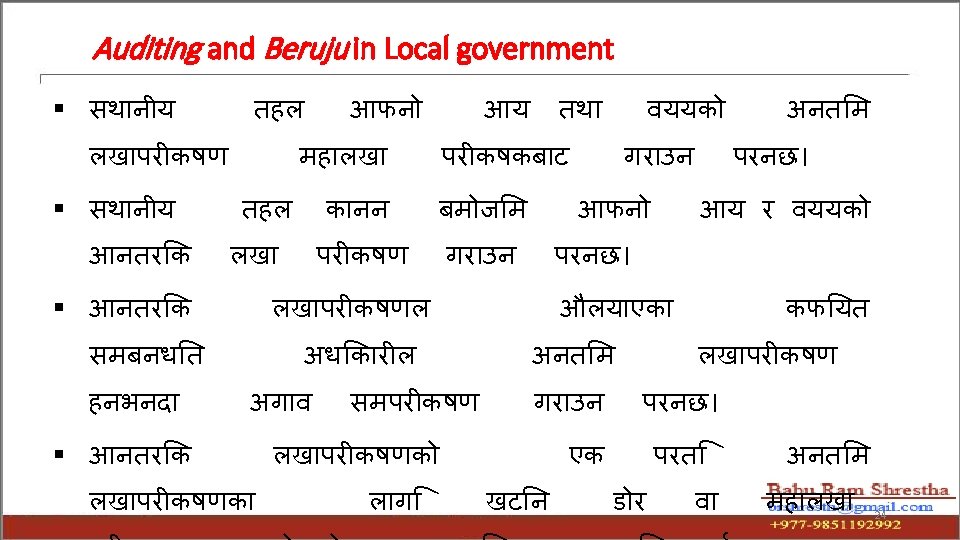

Concept of Public Financial Management (PFM) PFM in general incorporates the management of government revenue, budget, expenditure, deposit, debt, reimbursement, procurement and other important aspects of financial management such as accounting, recording and reporting. It also includes internal control, final audit and external scrutiny of the financial transactions.

Objective of PFM • Fiscal Discipline • Strategic Allocation of Resources • Effective Service Delivery

Concept of Financial controls Financial control is concerned with tracking and reporting on allocation, disbursement, and utilization of financial resources, using the tools of budgeting, accounting and auditing. Financial controls are the means by which an organization’s resources are directed, monitored, and measured.

Objectives Financial controls are the means by which an organization’s resources are directed, monitored, and measured v Optimum usages of financial resources v Value for money is achieved v There exists effective accountability measure v Financial transactions and events are made transparent 6

Objectives v Make sure the continued reliability of accounting systems v Confirming the accuracy of reporting v Ensure to reduces financial risk to the organization. 7

Objectives To achieve entity’s objectives related tooperations, reporting, and compliance v Objective identified v Control Designed v Controls in Place v Objectives Achieved 8

Process v Establishing Standards v Measuring actual performance v Comparing performance with standards v Corrective action 9

PEFA : PFM High Level Performance Indicators Performance High Level Indicators A. PFM OUTTURNS B. KEY CROSSCUTTING ISSUES Performance Indicators (PI) Score Method I. CREDIBILITY OF THE BUDGET PI-1 Aggregate expenditure outturn compared to original approved budget M 1 PI-2 Composition of expenditure outturn compared to original approved budget M 1 PI-3 Aggregate revenue outturn compared to original approved budget M 1 PI-4 Stock and monitoring of expenditure payment arrears M 1 II. COMPREHENSIVENESS AND TRANSPARENCY PI-5 Classification of the budget M 1 PI-6 Comprehensiveness of information included in budget documentation M 1 PI-7 Extent of unreported government operations M 1 PI-8 Transparency of inter-governmental fiscal relations M 2 PI-9 Oversight of aggregate fiscal risk from other public sector entities M 1 Public access to key fiscal information M 1 PI-10 C. BUDGET Thematic Groups and Indicators III. POLICY- BASED BUDGETING

Performance High Level Indicators Performance Indicators (PI) 28+3 Thematic Groups and Indicators Score IV. PREDICTABILITY AND CONTROL IN BUDGET EXECUTION C. BUDGET CYCLE PI-13 Transparency of taxpayer obligations and liabilities M 2 PI-14 Effectiveness of measures for taxpayer registration and tax assessment M 2 PI-15 Effectiveness in collection of tax payments M 1 PI-16 Predictability in the availability of funds for commitment of expenditures M 1 PI-17 Recording and management of cash balances, debt and guarantees M 2 PI-18 Effectiveness of payroll controls M 2 PI-19 Competition, value for money and controls in procurement M 2 PI-20 Effectiveness of internal controls for non-salary expenditure M 1 PI-21 Effectiveness of internal audit M 1 V. ACCOUNTING, RECORDING and REPORTING PI-22 Timeliness and regularity of accounts reconciliation M 2 PI-23 Availability of information on resources received by service delivery units M 1 PI-24 Quality and timeliness of in-year budget reports M 1 PI-25 Quality and timeliness of annual financial statements M 1

Performance High Level Indicators Performance Indicators (PI) 28+3 Thematic Groups and Indicators Score C. BUDGET CYCLE VI. EXTERNAL SCRUTINY AND AUDIT PI-26 Scope, nature and follow-up of external audit M 1 PI-27 Legislative scrutiny of the annual budget law M 1 PI-28 Legislative scrutiny of external audit reports M 1 DONOR PRACTICES D. DONOR PRACTICES PI-29 Predictability of Direct Budget Support M 1 PI-30 Financial information provided by donors for budgeting and reporting on project and program aid Proportion of aid that is managed by use of national procedures M 1 PI-31 M 1

Budget Cycle 5. Audit and External Scrutiny §Auditor General §Public Accounts Committee §Parliament 4. Accounting, Reportin g and Monitoring §Monthly and Trimistrial Reports §(Expenditures and Outputs) §Integrated Financial Reporting §Annual Review. 6. Evaluation and Policy Review §Outcome Evaluation §Annual Review and Policy Updation §NPC/NDC 3. Budget Execution §Release of the Funds §Expenditure Control §Program Implementation §Revenue/ receipts §Treasury Operation §Cash Management 1. Policy and Planning §Fiscal Targets 3 years §Policy targets §Resource Management §Expenditure Priorities 2. Budget Preparation and Aproval §Revenue and Expenditure Projection §Financial Plan §Ministerial Allocations §Legislative Approval 13

How Financial Control is being exercised? Policies, Process, Procedures and through top Management v Laws, rules and regulations, directives, guidelines etc. v Internal checking, internal control and internal audit Through external enquiry and audit v External audit v Public society engagement 14

Control in different Level Area (Activities) of control § Physical, § Human, § Information and § Financial Resource 15

Level of control § Strategy, Tactical and Operation Stage of types of control § Based on time - Feed Forward, Back Forward and Concurrent

v Checking that every thing is running the right track v Detecting errors and areas for improvement v Implement preventive measures v Communicate with and motivate employees v Take action where required

Financial Control Through Preventive controls are design to prevent problems rather than identify them. v Use of passwords to gain access to computer application system, v Required approval for all purchase orders over a certain rupee threshold. v Separation of Duties v Access Controls v Physical Audits v Standardized Documentation v Trial Balance v Periodic Reconciliations v Approval Authority 18

Auditing Approaches v Compliance Audit: Principles, Procedures and prevailing rules and regulation v Financial Statement Audit: Financial statement v Performance Audit: Economy, Efficiency and Effectiveness 20

v Risk Based Audit • Understanding • Identifying and evaluating risk • Answering to identified risk • Concluding on areas of risk

Auditing Process v Notification v Planning v Opening Meeting ( Entry Meeting ) v Management Representation Letter –Picture 1. jpg v Field work (Audit Techniques) : Examination of Record, Inquiry, Inspection, Comparison, Confirmation, Computation, Observation and Physical Examination. 22

Auditing Process v Communication v Report Drafting v Management Response v Closing Meeting (Exit Meeting- Minute must be done/Prepared ) v Report Distribution (Preliminary Report /Management Letter), v Final Report v Follow up v Quality Assurance 23

Thank You