Financial Accounting Lesson 8 Liabilities and Present Value

Financial Accounting Lesson 8: Liabilities and Present Value Ben Trnka/Boz Bostrom www. benandboz. com

Liabilities will differ by company and industry

Overview Understand how to account for liabilities Understand how to compute future value of a single amount and an annuity Understand how to compute present value of a single amount and an annuity

Current vs. Long-Term Liabilities Current liabilities are those expected to be paid with current assets Thus, expected to be paid off within one year Most creditors expect to be paid off within one year, thus the majority of liabilities are current Exceptions for certain loans/bonds, leases, pensions, and deferred taxes

Accounts Payable Items purchased but not paid for right away with cash – purchased “on account” Generally paid off within 30 days and not-interest bearing Most often used when a company purchases inventories, supplies, and services Example: Walgreens purchases $1, 000 of medicine from Johnson & Johnson and will make payment next month Dr Cr Inventory Accounts Payable Cash $1, 000

Accrued Expenses/Liabilities Recorded when a company receives services/supplies by the end of a period, but does not pay until the next fiscal period Often used with estimates for a bill that has not yet been received Goal is to match expense with financial statement income Example: Walgreen’s electric bill is estimated to be $2, 000 for the month of September, but the bill won’t be received until mid-October Dr Cr Utilities Expense Utilities payable Cash $2, 000

Income Taxes Payable Tax expense is recorded when a company earns income, and not when the cash is paid to the government. Example, Walgreens earned pre-tax income of $6 billion for its year ended August 31, 2018 and pays tax at a rate of 21% Dr Cr Income Tax Expense Income Taxes Payable Cash $1. 26 B

Compensation Companies record compensation expense in the period in which it was earned. Example: Assume a worker earns $200 per day and on December 31 st hasn’t been paid for 5 days of work. Also assume the worker has earned but not been paid for 2 days of vacation and a $150 bonus. Dr Wages expense $1, 000 ($200 * 5) Dr Bonus expense $150 Dr Vacation expense $400 ($200 * 2) Cr Dr Cr Wages and benefits payable Cash $1, 550

Payroll Taxes Employees have certain deductions withheld from their paychecks Payroll taxes Social security tax – 6. 2% of the first $128, 400 of their wages Medicare tax – 1. 45% of their wages Employer must match these amounts Federal and state income taxes withheld Health insurance, Retirement savings, and many others

Payroll Taxes - Example An employee earns $1, 000. The employer withholds payroll taxes, $100 of federal income taxes, $50 of state income taxes, and $85 of health insurance premium Gross Wages $1, 000. 00 Social security taxes ($62. 00) Medicare taxes ($14. 50) Federal income taxes ($100. 00) State income taxes ($50. 00) Health insurance premiums ($85. 00) Take home pay $688. 50

Payroll Taxes - Journal entries Dr Wages Expense Cr Payroll taxes withheld and payable $76. 50 (Social security + Medicare) Cr Income taxes withheld and payable $150 (State and Federal) Cr Health insurance withheld and payable $85 Cr Cash $688. 50 Dr Cr Thus, the company’s total expense is $1, 076. 50 Payroll tax expense Payroll taxes payable $1, 000 $76. 50

Payroll Taxes - Journal entries Dr Payroll taxes withheld and payable $76. 50 Dr Income taxes withheld and payable $150 Dr Health insurance withheld and payable $85 Dr Payroll taxes payable $76. 50 Cr Cash $388

Revenues When a company receives cash before it delivers the goods or")

Unearned (Deferred) Revenues When a company receives cash before it delivers the goods or provides the services, it must setup a temporary liability account The company has an obligation to deliver goods / provide services Example: Boeing receives $100 M from Delta Airlines for a 737 plane to be delivered next year Dr Cr Cash Unearned Revenues $100 M

Accrued Warranties Many companies offer warranties on products they sell. If the product is defective, the company will fix or replace it Record estimated warranty expense at the time of sale, not when the warranty claim is made Example: Toyota provides a limited warranty whenever it sells a vehicle. Each time it sells a Camry, it estimates warranty cost of $800 Dr Cr Warranty expense Accrued warranties Cash $800

Short term debt / Current portion of long-term debt Companies frequently borrow funds with payment due more than one year away. Initially, record Long-term note payable or Long-term Debt. When amount becomes due in one year or less, reclassify the amount as current Example: Walgreens borrows $2 M on a 5 -year loan to construct a new store. Dr Cr Cash $2 M Long-term Debt Current portion of Long-term Debt $2 M $2 M

Leases of Fixed Assets Accounting depends on the term of the lease, and other factors Short term classified as operating leases – record expense each year Long term classified as capital leases – accounted for as a fixed asset and loan payable Will learn more about leases in intermediate accounting courses

Contingent Liabilities Companies may face lawsuits, and the question is when to record anticipated expenses/payments If payment is probable and can be reasonably estimated – record the expense If payment is probable but amount can’t be estimated – disclose in footnotes If payment is reasonably possible – disclose in footnotes If chance of payment is remote – no recording/disclosure

Contingent Liabilities Wal-Mart paid bribes to government officials in Mexico in order to help generate business. That is illegal and they are subject to fines. For many years, Wal-Mart could not estimate the amount of the fine and thus simply disclosed the issue in the financial statement footnotes. But in its January 31, 2018 financials, Wal-Mart accrued a fine of $283 million. Dr Cr Fines and penalties expense Fines and penalties payable Cash $283 M

Additional Long-Term Liabilities Deferred income taxes Recorded in order to match income tax expense against financial statement income Covered in intermediate accounting or tax courses Pension liabilities A company may promise to pay a former/retired an employee a set amount per month/year for the rest of their lives. Usually a cash payment, and may also include health benefits

Notes Payable A company may borrow cash from the bank to fund operating needs, capital investments, acquisitions, expansions, etc. Notes are formal written agreements Contain a repayment schedule with specific dates and interest rates Journal entry upon borrowing: Dr Cr Cash Notes Payable

Notes Payable On March 31, 2018, a company borrows $10, 000 at a 10% annual interest rate. Principal/interest due on September 30, 2018 March 31: Dr Cr September 30: Dr Note Payable $10, 000 Dr Interest Expense $500 ($10, 000 * 10% * 6/12) Cr Cash Note Payable Cash $10, 000 $10, 500

Notes Payable On March 31, 2018, a company borrows $10, 000 at a 10% annual interest rate. Principal/interest due on March 31, 2019 March 31, 2018: Dr Cash Cr $10, 000 Note Payable $10, 000 Dr Interest Payable $750 Dr Interest Expense $250 ($10, 000 * 10% * 3/12) $750 ($10, 000 * 10% * 9/12) Cr Dr Note Payable December 31, 2018: Dr Interest Expense March 31, 2019: Interest Payable $750 Cr Cash $11, 000

Future Value and Present Value Concepts Many transactions involve paying/receiving money in the future As a company can earn interest on investments, the general theory is that a dollar today is worth more than a dollar in the future For example, a company would rather have $100 today than one year from now. Even if it could just earn 1% interest, taking $100 today an investing it would give the company $101 one year from now. Conversely, a company would rather pay $100 one year from now than today. At a 1% interest rate, a company could take $99 today, invest it for a year, and pay the $100 in a year.

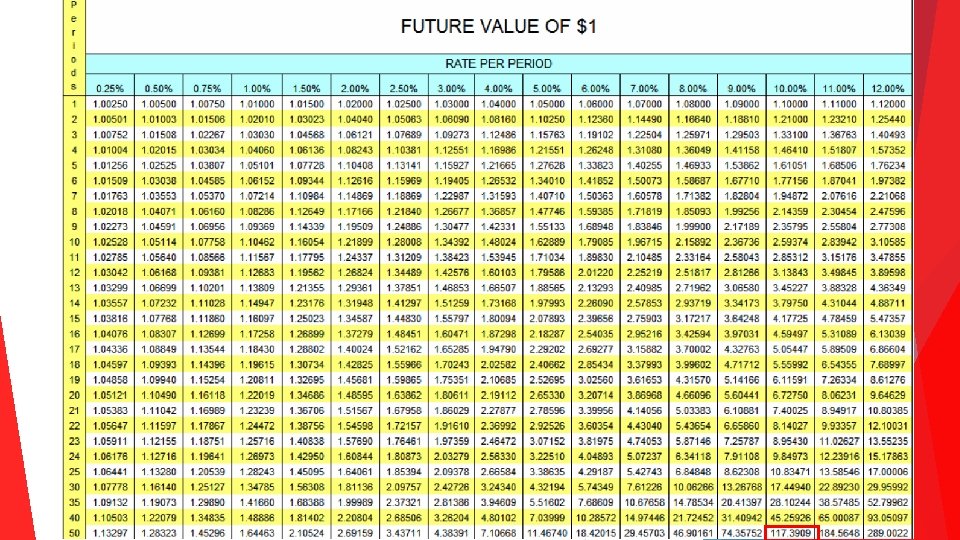

Future Value of $1 Current amount * Factor = FV If a first year college student invests $1, 000 today, how much will they have when they retire in 50 years? Assume the investment earns a 10% interest rate.

Future Value of $1 Current amount * Factor = FV If a first year college student invests $1, 000 today, how much will they have when they retire in 50 years? Assume the investment earns a 10% interest rate. $1, 000 * 117. 3909 = $117, 390. 90 balance - $1, 000. 00 invested $116, 390. 90 interest earned

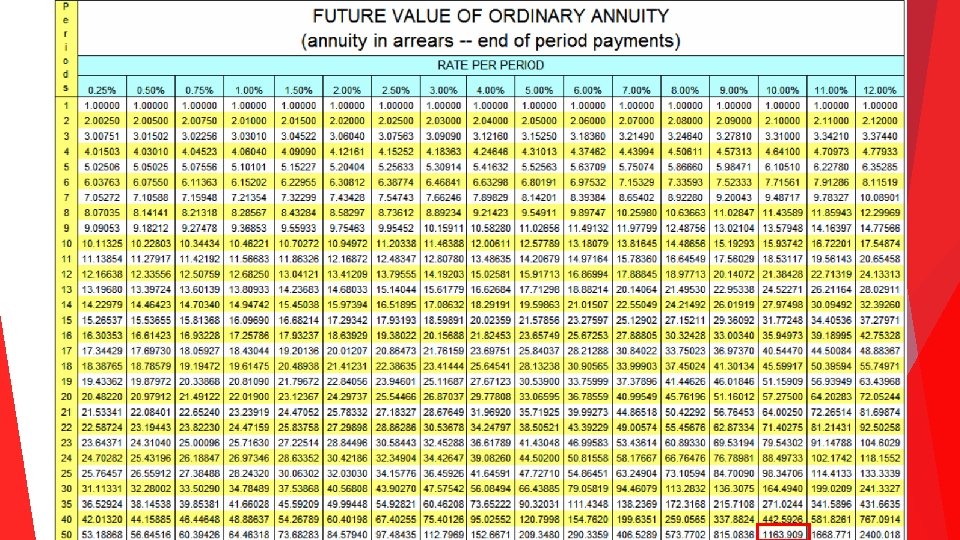

Future Value of an Annuity An annuity is a series of equal payments Annuity amount * Factor = FV of annuity If a first year college student invests $1, 000 at the end of each of the next 50 years, how much will they have when they retire in 50 years? Assume they can earn a 10% interest rate.

Future Value of an Annuity An annuity is a series of equal payments Annuity amount * Factor = FV of annuity If a first year college student invests $1, 000 at the end of each of the next 50 years, how much will they have when they retire in 50 years? Assume they can earn a 10% interest rate. $1, 000 * 1163. 909 = $1, 163, 909 - $50, 000 invested ($1, 000 per year * 50 years) $1, 113, 909 balance interest earned

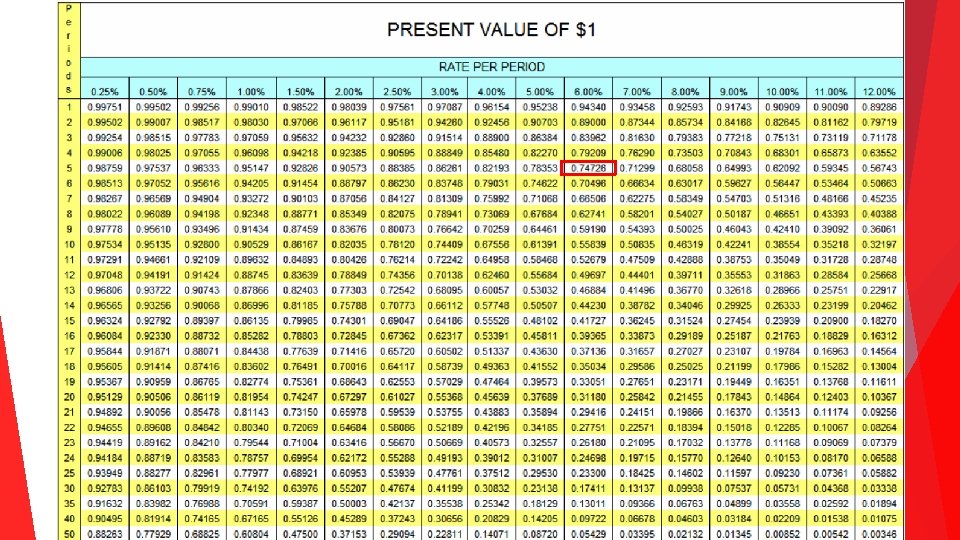

Present Value of $1 Future amount * Factor = PV If a couple expects to pay $30, 000 to purchase a new car in five years, how much would they need to set aside today? Assume they can earn a 6% interest rate.

Present Value of $1 Future amount * Factor = PV If a couple expects to pay $30, 000 to purchase a new car in five years, how much would they need to set aside today? Assume they can earn a 6% interest rate $30, 000 * 0. 74726 = $22, 417. 80 $30, 000. 00 balance - $22, 417. 80 invested today $7, 582. 20 interest earned

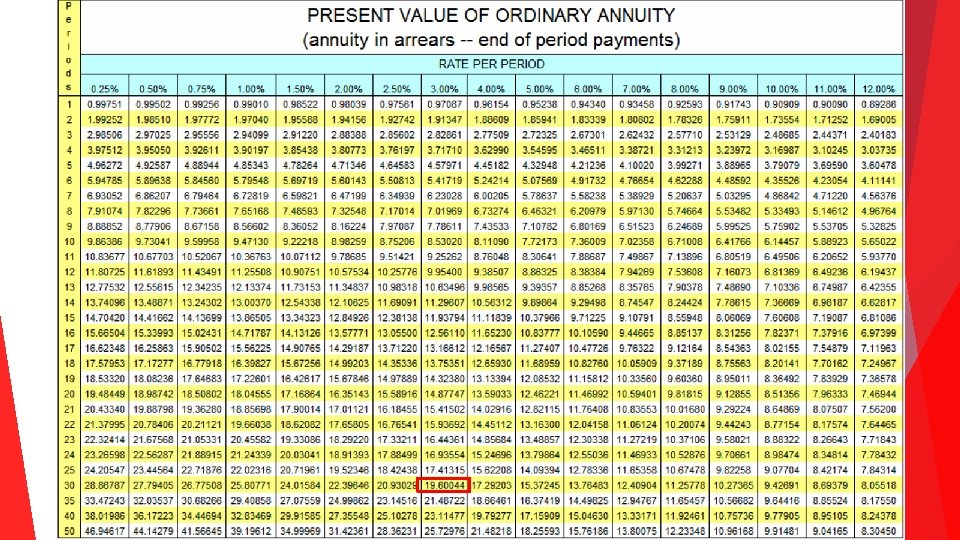

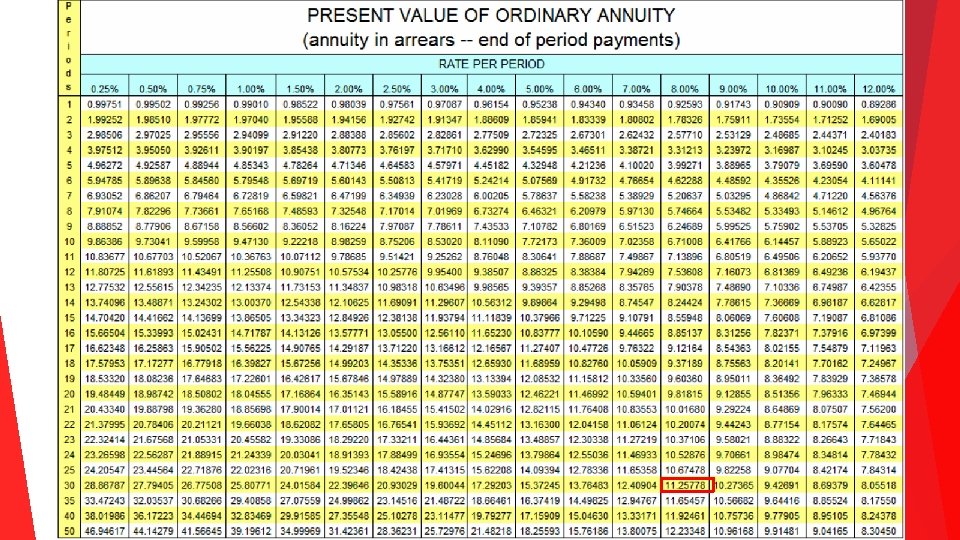

Present Value of an Annuity Amount of each future annuity payment * Factor = PV of Annuity If you play (and win) the Powerball, you could either receive $40. 6 M today or $2. 37 M per year for the next 30 years ($71. 1 M total). If you believe an appropriate interest rate is 3%, which option should you choose?

Present Value of an Annuity Amount of each future annuity payment * Factor = PV of Annuity If you play (and win) the Powerball, you could either receive $40. 6 M today or $2. 37 M per year for the next 30 years ($71. 1 M total). If you believe an appropriate interest rate is 3%, which option should you choose? $2. 37 M * 19. 60044 = $46. 45 M. Choose the annuity option! If you believe an appropriate interest rate is 8%, which option should you choose?

Present Value of an Annuity Amount of each future annuity payment * Factor = PV of Annuity If you play (and win) the Powerball, you could either receive $40. 6 M today or $2. 37 M per year for the next 30 years ($71. 1 M total). If you believe an appropriate interest rate is 3%, which option should you choose? $2. 37 M * 19. 60044 = $46. 45 M. Choose the annuity option! If you believe an appropriate interest rate is 8%, which option should you choose? $2. 37 M * 11. 25778 = $26. 68 M. Choose the cash now option!

Key Takeaways Liabilities are recorded when it is probable that a company will need to make a payment, or provide goods/services The future value of a dollar is worth more than a dollar today, and the future value is greater the higher the interest rate The present value of a future cash flow is less than the amount of that future cash flow, and the present value is lower the higher the interest rate Thanks for tuning in!

- Slides: 38