Finance 30210 Managerial Economics Consumer Demand Analysis We

$10 2.")

2. 3 3")

$5 1.")

1. 6 2.")

= $4/lb. Q(Bananas) = 10")

= $4/lb. P(Apples)")

= $2/lb. Q(Bananas) = 25 lbs P(Apples)")

Choice A Q(Bananas) =")

measures the amount of Y you require to")

Business + Recreation Aggregate LN(Quantity) We")

- Slides: 85

Finance 30210: Managerial Economics Consumer Demand Analysis

We can begin our representation of the consumer with a demand function… Is a function of… Quantity demanded Price Income Price $20 40 Quantity Prices of Substitutes Prices of Compliments

Given a demand function we can characterize the behavior of demand with elasticity. . Price elasticity will always be a negative number $20 $15 40 60 Quantity

Given a demand function we can characterize the behavior of demand with elasticity. . Income elasticity will generally be a positive number Price $20 40 56 Quantity

Given a demand function we can characterize the behavior of demand with elasticity. . Cross price elasticity will be a positive number for substitutes Price $20 40 44 Quantity

Given a demand function we can characterize the behavior of demand with elasticity. . Cross price elasticity will be a negative number for compliments Price $20 32 40 Quantity

Note that if the demand relationship is linear, elasticity is not constant

For example…. Price $80 $30 100 Quantity

Let’s try something a little more complicated…a non-linear demand relationship Price $2916 $400 Quantity 68

Sometimes we use demand functions that are linear in logs… Price $12 40 Quantity 3. 7 LN(Quantity)

Price $12 40 Quantity

A little math trick…recall the derivative of the natural log This just says that the difference in logs is a percentage change Therefore, if we start with elasticity

Sometimes we use demand functions that are linear in logs… Price $12 3. 7 LN(Quantity)

Sometimes we use demand functions that are linear in logs… Price LN(Price) $10 2. 3 3 Quantity

Sometimes we use demand functions that are linear in logs… LN(Price) 2. 3 3 Quantity

Sometimes we use demand functions that are linear in logs… Price LN(Price) $5 1. 6 8. 8 Quantity 2. 2 LN(Quantity)

Sometimes we use demand functions that are linear in logs… LN(Price) 1. 6 2. 2 LN(Quantity) Log linear demand curves have constant elasticities!

Suppose that you setting prices for US Air. You know that you face the following demand curve for the New York/Chicago Shuttle… Price $200 $80, 000 400 Quantity If you wanted to increase revenues, should you increase or decrease your price?

If you wanted to increase revenues, should you increase or decrease your price? Price Why didn’t revenue go up by $400? $200 $199 $80, 396 400 404 Quantity You should decrease price. A $1 price decrease will raise revenues by $400

Suppose that you wanted to maximize revenues? Price $200 $150 $90, 000 400 600 Quantity

Now, let’s go about this a little differently… Price $200 $80, 000 400 Quantity Every 1% drop in price will raise revenues by 1%

Using the point elasticity gives you the same answer… Why didn’t revenues go up by 10%? Price $200 $180 $86, 400 480 Quantity

We could also maximize revenues using elasticity… When the elasticity hits -1, revenues stop growing when you lower your price. Price $150 $90, 000 600 Quantity

Obviously, the more information you have, the better decisions you will make… However, knowing a few elasticities is quite helpful as well! The best pricing decisions would come from a demand curve Price Revenue maximizing price $250 $200 $150 $140 $90, 000 $50 600 Quantity

Suppose that you setting prices for US Air. You know that you face the following demand curve for the New York/Chicago Shuttle… Suppose that median income is equal to $50, 000. Income in thousands Price Suppose that a recession causes a 20% drop in income. How much would we have to lower our price if we wanted to keep sales constant? $125 $75, 000 600 Quantity

Suppose that a recession causes a 20% drop in income. How much would we have to lower our price if we wanted to keep sales constant? Price $125 $120 $72, 000 600 Quantity Now income is $40, 000

Now, again with elasticity… Suppose that median income is equal to $50, 000. Price $125 Suppose that a recession causes a 20% drop in income. How much would we have to lower our price if we wanted to keep sales constant? $75, 000 600 Quantity

Suppose that a recession causes a 20% drop in income. How much would we have to lower our price if we wanted to keep sales constant? Price $125 $123 $73, 800 600 Quantity

Again, the more information you have, the better decisions you will make… However, knowing a few elasticities is quite helpful as well! The best pricing decisions would come from a demand curve Price $125 $75, 000 600 Quantity

Now, suppose that you realized that you actually faced two types of customers : Recreational and business travelers. Could you do better? Business Recreational Price $400 $200 $150 $75, 000 $15, 000 500 Quantity 100 Quantity

Recall the aggregate demand curve we had previously…. what we had was actually a piece of what aggregate demand really looked like Price $400 At a price above $200, recreational travelers don’t fly. The only demand is coming from business travelers. At a price below $200, we now have two types of demanders flying. $200 + $150 $90, 000 400 600 Quantity Could we do better?

Suppose that we decided to ignore recreational travelers and cater to business clients… Price $400 $200 $80, 000 400 600 Quantity No…that’s not a good idea!

Why don’t we just charge them different prices? Recreational Business Price $400 $200 $100 $80, 000 $20, 000 400 Quantity 200 Quantity

The real question is: Is this feasible to do empirically? Price $400 This is “the Truth”. Two types of individuals making purchasing decisions. Individual decisions added up across all individuals create an aggregate demand curve. $200 Quantity

If you do a linear estimation, what you end up with something like this…not really what we want Price $400 $200 Quantity

However, if you put a dummy variable in the regression for business/recreational traveler, you could get at the truth… Price $400 $200 YES! We can do this! Quantity

Now, lets change it up a little…. Business Recreational Price $600 $150 $200 $67, 500 $150 $22, 500 450 Quantity 150 Quantity

Now, if we charge different prices…. Recreational Business Price $600 $300 $200 $90, 000 $100 $30, 000 300 Quantity

Again, we have to ask: Is this feasible to do empirically? This is “the Truth”. Two types of individuals making purchasing decisions. Individual decisions added up across all individuals create an aggregate demand curve. Price $600 $300 $200 + Quantity

If you do a linear estimation, what you end up with something like this… Price $600 $200 Quantity

What if we tried the dummy variable trick… Price $600 $200 We’re Screwed! Time to try something else. Quantity

Here’s the process that takes place in the economy… P P D D Q Q P P Individual consumers have preferences over a variety of goods…they have limited incomes and face market prices. Consumers make choices on what to buy D D Q Q Individual decisions can be represented by individual demand curves P The market aggregates those decisions into a market demand curve D Q

Here is the problem we face… P We can estimate a market demand curve… D Q The problem is that the market demand often tells us very little about what is happening in the background… P P D D Q Q

So, here is how we attack the problem… P P D D Q Q P P D We see if we can come up with a numerical representation of preferences… Q D We then derive the resulting demand curves that come from the consumer choice problem… P We then aggregate the individual demand curves to get a market demand. This we can compare to aggregate data to see if we are correct D Q

How do we get an understanding of consumer preferences? We observe what they do! Television A Cost = $500 Television B Cost = $2500 Suppose you walk into the store with a choice between two TVs. Suppose that you choose Television A Either you prefer Television A or you can’t afford Television B Suppose that you choose Television B You must prefer Television B

Suppose that you observed the following consumer behavior P(Bananas) = $4/lb. Q(Bananas) = 10 lbs P(Apples) = $2/Lb. Q(Apples) = 20 lbs P(Bananas) = $3/lb. Q(Bananas) = 15 lbs P(Apples) = $3/Lb. Q(Apples) = 15 lbs Choice A Choice B What can you say about this consumer? Choice B Is strictly preferred to Choice A How do we know this?

Consumers reveal their preferences through their observed choices! Choice A P(Bananas) = $4/lb. P(Apples) = $2/Lb. P(Bananas) = $3/lb. Choice B Q(Bananas) = 10 lbs Q(Bananas) = 15 lbs Q(Apples) = 20 lbs Q(Apples) = 15 lbs Cost = $80 Cost = $90 P(Apples) = $3/Lb. B Was chosen even though A was the same price!

What about this choice? Choice C P(Bananas) = $2/lb. Q(Bananas) = 25 lbs P(Apples) = $4/Lb. Q(Apples) = 10 lbs Q(Bananas) = 15 lbs Choice B Cost = $90 Q(Apples) = 15 lbs Q(Bananas) = 10 lbs Choice A Choice C Cost = $100 Q(Apples) = 20 lbs Is strictly preferred to Choice B Is choice C preferred to choice A?

Choice B Choice C Is strictly preferred to Choice A Is strictly preferred to Choice B C>B>A Choice C Is strictly preferred to Choice A Rational preferences exhibit transitivity

Consumer theory begins with the assumption that every consumer has preferences over various combinations of consumer goods. Its usually convenient to represent these preferences with a utility function Set of possible consumption choices “Utility Value”

Using the previous example (Recall, C > B > A) Choice A Q(Bananas) = 10 lbs Q(Apples) = 20 lbs Choice B Q(Bananas) = 15 lbs Q(Apples) = 15 lbs Choice C Q(Bananas) = 25 lbs Q(Apples) = 10 lbs

We require that utility functions satisfy a few basic properties There is a definite ranking of all choices (i. e. transitivity) A C B This tells us that indifference curves can’t cross on another

Suppose that indifference curves did cross… We run into a problem! C A B

We require that utility functions satisfy a few basic properties More is always better! C A B

We require that utility functions satisfy a few basic properties People Prefer Moderation! 15 A C 10 5 B 5 10 15 Note: This is a result of diminishing marginal utility…this guarantees that demand curves slope down!

What if we didn’t have decreasing marginal utility? People prefer extremes! A C B Increasing marginal utility produces some weird decisions!!

We can characterize preferences with a few statistics. First, how does a consumer prefer one good relative to another. Marginal Utility of X Marginal Utility of Y The marginal rate of substitution (MRS) measures the amount of Y you need to be get in order to give up a little of X

The marginal rate of substitution (MRS) measures the amount of Y you require to give up a little of X If you have a lot of X relative to Y, then X is much less valuable than Y MRS is low!

The elasticity of substitution measures the curvature of the indifference curve Elasticity of substitution measures the degree to which your valuation of X depends on your holdings of X

The elasticity of substitution measures the curvature of the indifference curve If the elasticity of substitution is small, then small changes in x and y cause large changes in the MRS If the elasticity of substitution is large, then large changes in x and y cause small changes in the MRS

Elasticity of Substitution measures the degree in which you can alter the mix of goods. Consider a couple extreme cases: Perfect substitutes can always be traded off in a constant ratio Perfect compliments have no substitutability and must me used in fixed ratios Y Y Elasticity is Infinite Elasticity is 0 X X

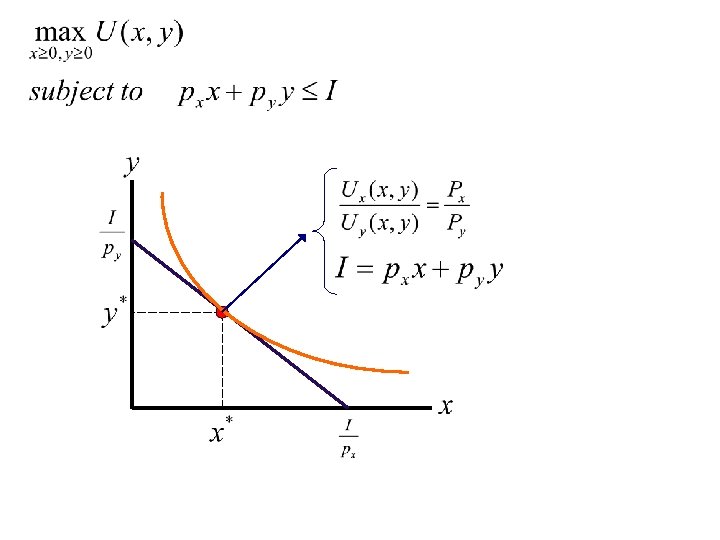

Consumers solve a constrained maximization – maximize utility subject to an income constraint. As before, set up the lagrangian…

First Order Necessary Conditions

Individual demand Curves represent a summary of the individual consumer choice problem

The marginal rate of substitution controls the height of the demand curve Willingness to pay is low Willingness to pay is high

The elasticity of substitution will effect the price elasticity of the demand curve D

Elasticity of Substitution vs. Price Elasticity

Perfect Complements vs. Perfect Substitutes

An Example: Cobb-Douglas Utility Recall, Marginal Rate of Substitution measures the relative value of x. This will determine the intercept of the demand curve

Recall, elasticity of substitution is measuring the degree of flexibility in the consumption of X and Y and will determine the slope of the demand curve

An Example: Cobb-Douglas Utility Marginal Rate of Substitution

An Example: Cobb-Douglas Utility

Constant price elasticity

Zero cross price elasticity

Constant income elasticity

Log-linear demand curves…

Returning to our airline example…suppose we used a customer survey or some other method and came up with preferences of airline travelers Business Airline Travel Recreational Everything Else Different intercepts but the same slope…

Returning to our airline example…suppose we used a customer survey or some other method and came up with preferences of airline travelers Business Airline Travel Everything Else Recreational

We end up with something like this… LN(Price) Business + Recreation Aggregate LN(Quantity) We could estimate a log linear demand curve with a dummy variable to check this

Suppose that we wanted different slopes… The Cobb-Douglas utility function is a special case of the CES (Constant elasticity of substitution) utility functions… The parameter alpha will govern the marginal rate of substitution which influences the intercept of the demand curve The parameter rho will govern the elasticity of substitution which influences the slope of the demand curve

Suppose that we wanted different slopes… The Cobb-Douglas utility function is a special case of the CES (Constant elasticity of substitution) utility functions… The resulting demand curve looks like this… A price index comprised of both good’s prices

Returning to our airline example…suppose we used a customer survey or some other method and came up with preferences of airline travelers Business Different intercepts and different slopes… Recreational

Returning to our airline example…suppose we used a customer survey or some other method and came up with preferences of airline travelers Business Recreational

Now, we have something like this… Business + Recreation Price Aggregate We could estimate a log linear demand curve to check this Quantity