FIN 30220 Macroeconomics Labor Markets The US Labor

FIN 30220: Macroeconomics Labor Markets

The US Labor Market by the numbers…* • • “Ineligible to work” • 71 M Under 16 years old Inmates of institutions (penal, mental, homes for the aged) Active duty military Total Population 325 M Employed 152 M Unemployed Not Participating 94. 4 M *As reported by the household survey (Bureau of Labor Statistics) 7. 6 M • To be considered “unemployed”, you must have looked for work over the last 30 days. Otherwise, you are “not participating”

The US Labor Market by the numbers…* Civilian Employment-Population Ratio “Ineligible to work” 70 M Total Population Total employment divided by the eligible population Eligible Population = Employed + Unemployed + Not Participating 153 *100 = 60. 0% 255 “Official” Unemployment Rate (U-3) 325 M Employed Unemployment divided by the Labor Force 153 M Labor Force = Employed + Unemployed Not Participating 95. 1 M *As reported by the household survey (Bureau of Labor Statistics) 6. 9 M 6. 9 *100 = 4. 3 % 159. 9 Participation Rate labor force divided by the eligible population 159. 9 *100 = 62. 7% 255

Unemployment in the US 12. 0 December 1982 10. 8% October 2009 10. 0% Unemployment Rate 10. 0 8. 0 6. 0 Average = 5. 8% Current = 4. 3% 4. 0 2. 0 0. 0 1948 May 1953 2. 5% 1953 1958 1963 1968 1973 1978 1983 1988 NBER Recession Dates 1993 1998 2003 2008 2013 *Source: Bureau of Labor Statistics

Alternate Measures of Unemployment in the U. S. To be considered “employed” you only need to have a job (no distinction between full time or part time)To be considered “unemployed”, you must have looked for work over the last 30 days. Otherwise, you are “not participating”. Discouraged Workers • Persons who are not in the labor force • Want to and are available to work • Have looked for work over the year, but not over the last 4 weeks • Specific reason cited for not looking for work is that they don’t believe there is a job available Marginally Attached Workers Part Time for Economic Reasons • Persons who are not in the labor force • Want to and are available to work • Have looked for work over the year, but not over the last 4 weeks • Any reason cited for lack of job search • Working less than 35 hours per week • Want to and are available to work full time • Gave an economic reason (Hours cut, unable to find full time work) for lack of a full time job

Alternate Measures of Unemployment in the U. S. Category May 2017 Eligible Population 255 M Labor Force 159. 9 M Employed 153 M Unemployed 6. 9 M Discouraged Workers 355, 000 Marginally Attached Workers 1. 48 M Part time for Economic Reasons 5. 22 M *From the latest household survey, BLS Recall, the “official” (U-3) unemployment rate is 4. 3% U-4 Unemployment Rate Unemployed plus discouraged workers divided by the labor force plus discouraged workers 7. 26 *100 = 4. 5% 160. 2 U-5 Unemployment Rate Unemployed plus discouraged workers plus marginally attached divided by the Labor Force + discouraged workers + marginally attached 8. 74 *100 = 5. 4% 161. 7 U-6 Unemployment Rate Unemployed plus discouraged workers plus marginally attached workers plus part time for economic reasons divided by the Labor Force + discouraged workers + marginally attached workers Note: U-1 unemployment deals with long term unemployment and U-2 deals with temporary jobs 14. 0 *100 = 8. 7% 161. 7

The U 6 unemployment rate includes underemployed, marginally attached workers, and discouraged workers 18. 0 16. 0 14. 0 U 6 Unemployment Rate 12. 0 Current 8. 7% 10. 0 8. 0 U 3 Unemployment Rate 6. 0 Current 4. 3% 4. 0 2. 0 0. 0 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

The Difference between the U 3 and U 6 unemployment rates would capture those that are underemployed, marginally attached, or discouraged. This is a new phenomena. 8. 0 7. 0 Average = 6. 0% 6. 0 5. 0 Average = 4. 0 3. 0 2. 0 1. 0 0. 0 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Let’s look at the US over the years since the last recession… 11. 0 Peak = 10. 0% October 2009 10. 0 9. 0 8. 0 7. 0 6. 0 5. 0 Current = 4. 8% January 2007 4. 6% 4. 0 2007 2008 2009 Recession 2010 2011 2012 2013 Recovery 2014 2015 2016 2017

Monthly change in payrolls June 2009 600 Average = 165, 000/mo. 400 Average = -361, 000/mo. 200 0 2008 2009 2010 2011 2012 2013 2014 2015 2016 -200 -400 -600 -800 -1000 8 million jobs lost during the recession 12 million jobs gained since the end of the recession 2017

Let’s do a back of the envelope calculation…. population grows at around 1. 5% per year. Let’s assume everybody enters the workforce at 16 and retires after 45 years. Eligible population = 110 M 1. 1% x 110 M = 1. 21 M Entering the workforce 61 Years ago (1956) 1. 21 M retiring 45 years ago (1972) 16 years ago (2001) Now (2017) Eligible population = 216 M 1. 2% x 216 M = 2. 59 M Entering the workforce 2. 59 M – 1. 21 M = 1. 38 M / 12 = 115, 000 per month!

June 2009 600 Average = 165, 000/mo. 400 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 -200 -400 -600 -800 -1000 8 million jobs lost during the recession 156, 000 Jobs created 165, 000 to. Jobs created - 126, 000 satisfy population growth - 33, 000 115, 000 to satisfy population growth lost jobs recovered per month 50, 000 lost jobs recovered per month To get back to “normal” 8, 000 50, 000 = 160 months (~13 years - 2022)

For comparison purposes, during the recovery following the 81 -82 recession, we created almost twice as many jobs per month 1200 1000 800 Average = 265, 000 Jobs created - 123, 000 to satisfy population growth 142, 000 lost jobs recovered per month 600 400 200 Average = -177, 000 0 1981 1982 -200 1983 1984 1985 3, 000 142, 000 = 21 months (~2 years) -400 -600 To get back to “normal” 3, 000 jobs lost

Lets compare the current recession/recovery to the last few 2 years Recession Beginning of recovery

Dumbest Tweet Ever!! R. David Edelman Special Assistant to the President for Economic and Technology Policy The streak of consecutive months with positive private sector job growth was ended in May 2016 (the streak was 74 months) Liz Allen Deputy Communications Director at the White House

Let’s look at the US over the years since the last recession… Recovery Recession January 2007 October 2009 May 2017 Category Jan 2007 Category Oct 2009 Category May 2017 Eligible Population 230 M Eligible Population 237 M Eligible Population 255 M Labor Force 153 M Labor Force 154 M Labor Force 159. 9 M Employed 146 M Employed 139 M Employed 153 M Unemployed 7 M Unemployed 15 M Unemployed 6. 9 M Employment Rate 63. 5% Employment Rate 58. 6% Employment Rate 60. 0% Unemployment Rate 4. 6% Unemployment Rate 10. 0% Unemployment Rate 4. 3% Participation Rate 66. 5% Participation Rate 64. 9% Participation Rate 62. 87% The primary reason for the decline in the unemployment rate over the past 6 years is the drop in labor force participation! If we had the same participation rate today as we did in 2007, the unemployment rate would be 10%!

This decline in labor force participation began it’s decline prior to the last recession…. . Peak = 67. 2% January 2001 68. 0 66. 0 64. 0 Current= 62. 7% Beginning of Women’s Liberation Movement (1967) 62. 0 59. 7% 60. 0 58. 0 56. 0 1948 1953 1958 1963 1968 1973 1978 1983 1988 1993 1998 2003 2008 2013 Recession

Female vs. Male Participation Labor Participation Rate - Men Labor Participation Rate - Women 65. 0 91. 0 60. 0 86. 0 55. 0 Beginning of Women’s Liberation Movement (1967) 81. 0 59. 7% 50. 0 45. 0 76. 0 40. 0 71. 0 35. 0 30. 0 1948 1956 1964 1972 1980 1988 1996 2004 2012 66. 0 1948 1956 1964 1972 1980 1988 1996 2004 2012

Some people claim that the drop is participation is baby boomers taking early retirement…not the case!! Labor Participation Rate: 25 - 54 85. 0 Labor Participation Rate: 55+ 45. 0 43. 0 80. 0 41. 0 39. 0 75. 0 37. 0 35. 0 70. 0 33. 0 31. 0 65. 0 29. 0 27. 0 60. 0 1948 1958 1968 1978 1988 1998 2008 25. 0 1948 1956 1964 1972 1980 1988 1996 2004 2012

A decline is participation isn’t the only thing “new” about our current situation… *From the Nov. 2000 household survey, BLS *From the May 2017 household survey, BLS Category Oct 2000 Unemployed (5. 3%) Category May 2017 6. 9 M 100% Less than 5 weeks 2. 1 M 30% 40% Between 5 and 14 weeks 2. 0 M 29% 0. 6 M 9% Between 15 and 26 weeks 1. 1 M 16% 0. 7 M 6% Over 27 weeks 1. 7 M 25% 6. 6 M 100% Less than 5 weeks 3 M 45% Between 5 and 14 weeks 2. 3 M Between 15 and 26 weeks Over 26 weeks Unemployed (4. 3%) 35 50 45 40 35 30 25 20 15 10 5 0 < 5 weeks 5 -14 weeks 15 -26 weeks 15% >26 weeks < 5 weeks 5 -14 weeks 15 -26 weeks >26 weeks 40%

Duration Example JAN FEB MAR APR MAY JUNE Category Unemployed JULY AUG SEPT NOV DEC 2. 2 M 8 M 6. 5 weeks 2. 2 M 13 weeks 2. 3 M 26 Weeks 1. 3 M 52 weeks 2. 2 M 1. 3 M 2. 2 M 2. 3 M 2. 2 M Total = 8. 0 Duration of Unemployment Category OCT Total % for Unemployed 31. 6 M 100% 6. 5 weeks 17. 6 M 56% 13 weeks 9. 2 M 29% 26 Weeks 2. 6 M 8% 52 weeks 2. 2 M 7% Length of unemployment spell % of total unemployed in a year 2. 2 M

It’s currently taking people almost twice as long as it used to find a job… 45. 0 40. 0 35. 0 30. 0 Duration of unemployment Current = 25 weeks 25. 0 20. 0 Average = 15 weeks 15. 0 10. 0 5. 0 0. 0 1948 1953 1958 1963 1968 1973 1978 1983 1988 1993 1998 2003 2008 2013

Wages in the US…* Dara Khosrowshahi $23, 6509/hr. Leslie Moonves $14, 100/hr. Philippe Dauman $13. 525/hr. Average hourly compensation $25/hr. Average CEO Pay** $7, 000/hr. Minimum wage for tipped employees **According to data compiled by the AFL-CIO, the average CEO pay at 327 of the nation's biggest companies All Time Record: Tim Cook (2011) Minimum wage (Federal) $7. 25/hr. $188, 000/hr. $2. 13/hr. *In 2014, Based on a 40 hour work week, 50 weeks per year

Recall that since the late 1970’s we have seen the emergence of a “wage gap”. That is, we see a difference between productivity and wages. This has been a major driver of income inequality. 450 Index: 1947 = 100 400 350 300 250 200 150 From the late 1970’s on, we have developed a “wage gap” 100 50 0 1947 1957 1967 Real GDP Per Hour 1977 1987 1997 Real Compensation Per Hour 2007

900 880 Jan. 1979 $830/wk. (~$20. 75/hr. *)")

Median Weekly Real Earnings (2016 Dollars) 900 880 Jan. 1979 $830/wk. (~$20. 75/hr. *) 860 Jan. 2000 $825/wk. (~$20. 63/hr. *) Recall the increase in participation by women? This has a lot to do with it! Current $860/wk. (~$21. 50/hr. *) 840 820 800 780 760 740 720 1979 1984 1989 1994 1999 2004 2009 2014 *Assuming a 40 hour week

Women’s % of Men 1000 85 950 80")

Median Weekly Real Earnings (2016 Dollars) Women’s % of Men 1000 85 950 80 900 850 Men $885/wk. (~$22/hr. ) 75 800 750 70 700 650 Women $724/wk. (~$18/hr. *) 65 600 550 1979 60 1984 1989 1994 1999 2004 2009 2014 *Based on a 40 hour week

Average Weekly Hours in the US 40. 0 39. 0 1964 38. 2 hrs. /wk. 38. 0 37. 0 12. 5% 36. 0 35. 0 Current 33. 7 hrs. /wk. 34. 0 33. 0 32. 0 31. 0 30. 0 1964 1969 1974 1979 1984 1989 1994 1999 2004 2009 2014

10000 9000 8000 7000 6000 5000 4000")

Part Time For Economic Reasons (1964 -2017) 10000 9000 8000 7000 6000 5000 4000 3000 2000 1000 0 1964 1969 1974 1979 1984 1989 1994 1999 2004 2009 2014

60000 January 1999 $57, 909")

Real Median Household Income in the US (2015 Dollars) 60000 January 1999 $57, 909 58000 Current (2016) $56, 516 56000 January 1989 $53, 000 54000 52000 50000 48000 46000 1984 1989 1994 1999 2004 2009 2014

")

Recall, that we are interested in understanding the business cycle… Recession (Below Trend Growth) Recovery (Above Trend Growth) GDP Trend (Average growth) Peak Trough The business cycle is a repeated pattern of recessions followed by recoveries Time

After removing the long term trend, we end up with a series that looks like this (% deviation from trend) % Deviation From Trend Recovery Recession Peak GDP 0 Trough Time

Total Employment is highly pro-cyclical… 3 Peak 6 2 4 1 2 0 2007 2009 2011 2013 0 -2 -1 -4 -6 -2 -8 Correlation =. 77 -10 -12 Trough Employment -3 -4 Industrial Production Employment (% Deviation from Trend) Industrial Production (% Deviation from Trend) 8

Real wages are pro-cyclical…. barely! 3 Peak 2 Deviation from Trend 1 0 2007 2009 2011 2013 -1 -2 -3 Trough -4 Real Wages Real GDP Correlation =. 12

Recall the apple orchard story…. OR At some point in time, you have a fixed number of trees (Capital) and workers Those workers/capital combine with productivity to produce apples (output) For a given capital stock and productivity level, labor markets determine total employment Those apples are allocated either towards consumption or investment (planting them to grow new trees)

Labor Markets Real wages Households choose how much to work Equilibrium real wage Businesses choose how many hours to hire Equilibrium employment Total employment (total hours worked)

Labor Markets If real wages are too high, we have excess supply of labor…this should put downward pressure on wages If real wages are too low, we have excess demand for labor…this should put upward pressure on wages

Labor Markets Recall that Output = Income Labor Income + Capital Income = = Labor Income Employment will determine total production (GDP) Predetermined

Labor Demand We assume that labor markets are populated by perfectly competitive firms Why is this important? These firms are making hiring decisions to maximize profits. Price of Output (fixed) Nominal Wage rate (fixed) Capital costs (fixed)

These firms use a production process that exhibits diminishing marginal productivity – that is as labor rises, its contribution to production of output shrinks So, absent productivity growth, increasing labor will lower the marginal product of labor

These firms use a production process that exhibits diminishing marginal productivity – that is as labor rises, its contribution to production of output shrinks

These firms are making hiring decisions to maximize profits. Consider what happens to profits if we change labor a little bit… Value marginal product of labor Businesses equate the nominal value of an hour of labor with the nominal wage OR Businesses equate the real value of an hour of labor with the real wage

Profits are maximized when benefits and costs are equated at the margin! Profits are increasing Profits are Decreasing Profits are constant (maximized)

So, these perfectly competitive businesses observe a real wage and make a profit maximizing decision of how much labor to hire. Those decisions are recorded in labor demand. As wages fall, the marginal cost of labor for businesses drops. This allows them to profitably expand their workforces – even in the light of diminishing marginal returns to labor.

Suppose the economy experiences an increase in productivity…. This increase in productivity not only raises total output for every hour of labor worked, but increases the marginal product of every hour worked

As events occur that influence the value of labor at the margin these businesses re-evaluate their hiring decisions and adjust their workforce accordingly. This increase in labor productivity increases labor demanded.

Labor Supply Just as businesses make decisions to maximize profits, we make decisions to maximize our utility Make ourselves as happy as possible Total Utility (Happiness) Real Consumption Leisure time We only have a couple requirements for utility functions • Utility is increasing in consumption (i. e. we like to buy things!) • Utility is decreasing in labor (we don’t like to work) • Utility exhibits diminishing marginal utility (the more we have of anything, the less it is worth to us at the margin)

Let’s suppose the following…you have a job opportunity that pays $12 an hour. You can work as much or as little as you want. Further, assume that the only good to buy is pizza and a pizza costs $10. Finally, assume that you have scholarship that pays you $20 per week (you don’t have to work for the stipend). How many hours would you choose to work? Hours available: 24 hrs. /day - 8 hrs. /day (sleep) 16 hrs. /day*7 days/wk. = 112 hrs. (Real Wage) Nominal Wage = $12/hr. Price (Pizza) = $10 Real Wage = 1. 2 Pizza/Hr. Non-Labor Income = $20/wk. Real Non-Labor Income = 2 Pizza/wk. (Real Wage) Work 112 Hrs. • Labor Income = $1, 344 • Stipend = $20 • Total Income = $1, 364 • Pizzas Bought = 136. 4 Work 30 Hrs. • Labor Income = $360 • Stipend = $20 • Total Income = $380 • Pizzas Bought = 38 No Work • Labor Income = $0 • Stipend = $20 • Total Income = $20 • Pizzas Bought = 2

Real Consumption")

What you choose to do depends on your preferences! Total Utility (Happiness) Real Consumption Leisure time If you work 1 additional hour, what is it cost you? 1 hour of leisure. What's that leisure worth to you? If you work 1 additional hour, what do you gain? 1. 2 pizzas (the real wage). How much are those pizzas worth to you? Value of an hour of leisure Number of pizzas you get per hour of work (real wage) Value of a pizza

, we equate costs and")

Just like with businesses, when we maximize our utility (happiness), we equate costs and benefits at the margin) Benefits of working Cost of working = Let’s rewrite this… Marginal Rate of Substitution Marginal Rate of substitution measures the value of leisure in terms of consumption Pizzas per hour of leisure

We only have a couple requirements for utility functions • Utility is increasing in consumption (i. e. we like to buy things!) • Utility is decreasing in labor (we don’t like to work) • Utility exhibits diminishing marginal utility (the more we have of anything, the less it is worth to us at the margin) Total Utility (Happiness) Real Consumption Leisure time As you work more, leisure falls and the marginal utility of that leisure increases • High marginal utility of leisure • Low Marginal Utility of Consumption • High MRS As you work more, consumption increases and the marginal utility of that consumption falls • Low marginal utility of leisure • High Marginal Utility of Consumption • Low MRS

Of all the affordable choices, the one that equates costs and benefits at the margin is the best choice! (Real Wage) Work 40 Hrs. • Labor Income = $480 • Stipend = $20 • Total Income = $500 • Pizzas Bought = 50 Utility is increasing Utility is decreasing

Suppose that you get a raise…your nominal wage increases to $15 (real wage is now 1. 5) Possibility #1: Labor Supply Increases (Substitution Effect) Work 50 Hrs. (nominal wage = $15) • Labor Income = $750 • Stipend = $20 • Total Income = $770 • Pizzas Bought = 77 Work 40 Hrs. • Labor Income = $480 • Stipend = $20 • Total Income = $500 • Pizzas Bought = 50 The substitution effect generates a labor supply curve that’s upward sloping (normal) (72 hours of leisure) (62 hours of leisure)

Suppose that you get a raise…you nominal wage increases to $15 (real wage is now 1. 5) Possibility #2: Labor Supply decreases (Income Effect) Work 40 Hrs. • Labor Income = $480 • Stipend = $20 • Total Income = $500 • Pizzas Bought = 50 Work 35 Hrs. (nominal wage = $15) • Labor Income = $525 • Stipend = $20 • Total Income = $545 • Pizzas Bought = 54. 5 The income effect generates a labor supply curve that’s downward sloping (weird)

Possibility #1: Labor")

So, which is it? Possibility #2: Labor Supply decreases (Income Effect) Possibility #1: Labor Supply Increases (Substitution Effect) OR We usually assume the substitution effect dominates!

This is")

Suppose that your stipend increases to $200/wk. (Wage rate is still $12) This is a pure income effect (the wage didn’t change, so there is no substitution effect) Work 40 Hrs. • Labor Income = $480 • Stipend = $20 • Total Income = $500 • Pizzas Bought = 50 Work 30 Hrs. (nominal wage = $12) • Labor Income = $360 • Stipend = $200 • Total Income = $560 • Pizzas Bought = 56 Labor supplied declines (labor supply shifts left)

Labor Markets – Equilibrium Real Wage Households choose how much to work Businesses choose how many hours to hire Total Hours Now, we just need to put the pieces together and solve for an equilibrium wage

Labor Markets – Long Run dynamics Over the long term, both productivity and capital increase which increases the marginal product of labor

Labor Markets – Long Run dynamics As our incomes rise, we can afford more leisure time – labor supply drops Long term productivity growth raises the value of labor at the margin – increasing labor demand Over the long term, real wages and employment rise

Labor Markets – Long Run dynamics As employment and productivity both rise, GDP rises

Labor Markets – Business cycle dynamics During economic expansions, labor productivity is above trend…the pushes labor demand up – employment and real wages rise above trend During recessions, labor productivity is below trend…this pushes labor demand down – employment and real wages fall below trend An increase (decrease) in employment raises (decreases) production.

During recessions, productivity declines. Labor demand falls – employment and real wages fall. During recoveries, productivity increases. Labor demand rises – employment and real wages increase. % Deviation From Trend Peak GDP Real Wages Employment 0 Productivity Trough Predicted Correlations Real Wage GDP Recession Recovery + Time Employment + Productivity +

")

Correlations With GDP Real Wage + Actual Predicted Employment + Productivity + (. 12) (. 77) (. 67) + + + The only problem we have is explaining the low correlation between real wages and GDP Some Suggestions • Are we valuing labor contracts correctly? • Have we calculated real wages correctly? • Do wages actually adjust (most labor contracts are fixed for extended periods) • Does minimum wage affect this analysis? • Is our story correct? Empirically In Theory Our story for labor supply says that higher wages increase hours worked At the individual level, labor supply is very inelastic At the macro level, there is labor supply is very elastic

Example: Oil Price Shocks in the 1970’s 45 1979 Iranian Revolution Dollars per Barrel 40 35 We can think about high oil prices as a negative shock to productivity…remember, we measure GDP as value added and (given that the US imports a lot of oil), high energy prices will lower value added 30 25 1973 Arab Oil Embargo 20 15 10 5 0 1946 1951 1956 1961 1966 1971 1976 1981 1986 1991 1996

3 2. 5 % Deviation From Trend 2 1.")

Real Compensation (1972 – 1982) 3 2. 5 % Deviation From Trend 2 1. 5 1 0. 5 0 1972 1975 1978 -0. 5 -1 -1. 5 1979 Iranian Revolution -2 1973 Arab Oil Embargo 1981 The high oil prices lowers the value of labor at the margin…labor demand falls and real wages drop

3 % Deviation From Trend 2 1 The drop in")

Employment (1972 – 1982) 3 % Deviation From Trend 2 1 The drop in labor demand also lowers the new equilibrium level of employment 0 1972 1975 1978 1981 -1 -2 -3 -4 1973 Arab Oil Embargo 1979 Iranian Revolution

5 4 % Deviation From Trend 3 2 1 0")

GDP (1972 – 1982) 5 4 % Deviation From Trend 3 2 1 0 1972 1975 1978 -1 -2 -3 1979 Iranian Revolution -4 -5 -6 1973 Arab Oil Embargo 1981 Lower employment will lower total production (GDP)

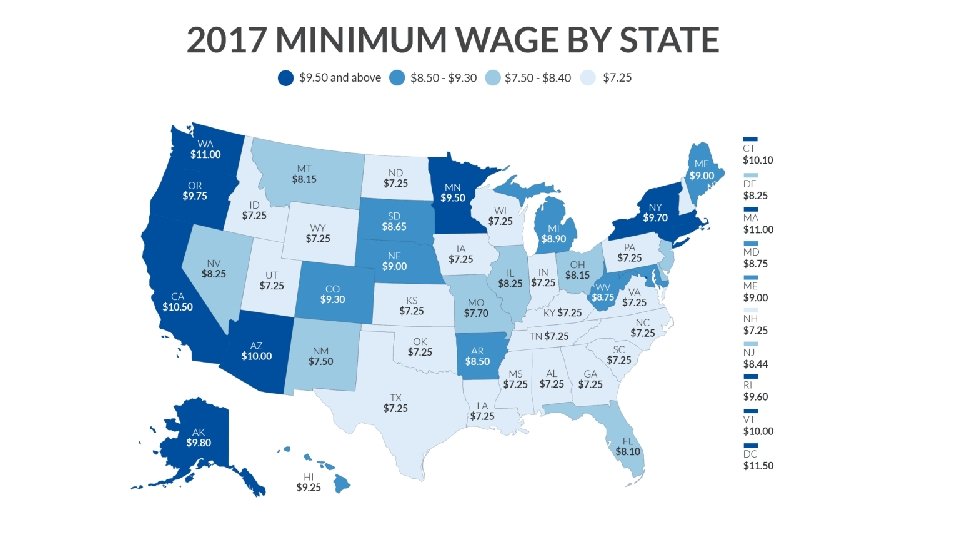

Application of Labor Market Analysis: The Minimum Wage Bernie Sanders has proposed raising the minimum wage from its current level of $7. 25 per hour to $15 per our

The Minimum wage began in 1938. The first minimum wage was $0. 25 per hour (that’s equivalent to about $4. 35 today) 8. 00 $7. 25 (Since 2009) 7. 00 6. 00 5. 00 4. 00 3. 00 2. 00 1. 00 0. 00 1968 1972 1976 1980 1984 1988 1992 1996 2000 2004 2008 2012 2016

However, in real terms, the minimum wage has consistently fallen. 12. 00 10. 00 Re a $s) l Wa g 8. 00 e ( 6. 00 201 6 4. 00 2. 00 0. 00 1968 1972 1976 1980 1984 1988 1992 1996 2000 2004 2008 2012 2016

Minimum wages around the world* * Exchange Rate Method Used

Adjusting for purchasing power changes the story a little….

In 2011, 77 million American workers age 16 and over were paid at hourly rates, representing around 50 percent of all wage and salary workers. • 16 million hourly workers (20% of hourly workers) earn less than the proposed $10. 10 per hour • 1. 3 million (1. 5% of hourly workers) earned exactly the prevailing Federal minimum wage of $7. 25 per hour. • About 1. 7 million (2% of hourly workers) million had wages below the minimum ($2. 13/hr. is the minimum wage for tipped employees). Source: Department of Labor

Most minimum wage workers are part time 20 Percent of minimum wage workers 18 16 14 12 10 8 6 4 2 0 0 to 4 hours 5 to 9 hours 10 to 14 hours 15 to 19 hours 48% 20 to 24 hours 25 to 29 hours 30 to 34 hours 35 to 39 hours 40 hours 41 + hours vary Source: Department of Labor

12 companies with most minimum-wage workers Darden Restaurants Yum Brands Dine. Equity

Highest wage retail companies $11. 27/hr $9. 67/hr $13. 38/hr $10. 20/hr $9. 67/hr $11/hr $9. 24/hr $9. 48/hr $9. 32/hr $9. 38/hr

Costco's CEO and president, Craig Jelinek, has publicly endorsed raising the federal minimum wage to $10. 10 an hour, and he takes that to heart. The company's starting pay is $11. 50 per hour, and the average employee wage is $21 per hour, not including overtime.

Microeconomic Argument for minimum wage increase: minimum wage workers are underpaid…but really, we are all “underpaid” in a competitive market! Labor supply ranks us by the value of our free time The equilibrium wage reflects the productivity/free time of the marginal worker Labor demand ranks us by our productivity For the average worker, they are being paid less than they are worth, but more than their time is worth.

Macroeconomic argument for minimum wage increase: Increasing the minimum wage would put more money into the economy, but does it? • An increase to $10. 10 would amount to a $2. 85 per hour raise for those currently on minimum wage • For a 40 hour week, that would amount to $5700 per year • If we assume that all 16 million people affected got the full $5700, that would be an increase in income of $91. 2 B • $91. 2 B represents around. 5% of the US economy However, can this really be an increase in income? Unless an increase in the minimum wage makes us more productive, NO!

Microeconomic argument for increasing the minimum wage: We are creating a better distribution of income, but are we? Case #1: Rise in minimum wage results in increased unemployment So we have a transfer from one lower income group to another lower income group Case #2: Rise in minimum wage creates no job loss and business can’t pass the higher costs onto consumers Now we have a transfer from business owners to minimum wage workers Case #3: Rise in minimum wage creates no job loss, but businesses can pass the increased cost onto consumers Now we have a transfer from consumers to minimum wage workers

- Slides: 80