Experiments in Finance and Financial Markets Shyam Sunder

• But")

Copyright Shyam Sunder 15")

Copyright Shyam Sunder 19")

Copyright Shyam Sunder 25")

Copyright Shyam Sunder 26")

Copyright Shyam Sunder")

showed that")

Copyright Shyam Sunder 31")

Copyright Shyam Sunder 45")

Copyright Shyam Sunder")

, their value of information decreases")

Copyright Shyam Sunder 54")

- Slides: 54

Experiments in Finance and Financial Markets Shyam Sunder, Yale University Workshop in Experimental and Behavioral Economics Center for Advanced Studies, Department of Economics Jadavpur University, Kolkata, January 11, 2018 (c) Copyright Shyam Sunder 1

Questions to Address • Why do we need even more data on financial markets? • How could the data from such simple “Mickey Mouse” markets help us learn about far more complex investment environments? • Is experimental finance a branch or variation of behavioral economics/behavioral finance? • What have we learned so far from asset market experiments? • What is next? (c) Copyright Shyam Sunder 2

1. Why Do We Need More Data from Experimental Markets? • Of all branches of economics, financial economics probably has the most detailed and up-to-date observational data available • Consequently, this branch of economics is characterized by one of the strongest empirical traditions • Why, then, spend time and money to conduct experiments with financial markets and gather more data? (c) Copyright Shyam Sunder 3

Transactions v. Expectations • Data from the stock exchanges include bids, asks, transaction prices, volume, etc. • Data from information services on actions and events that may influence markets • Neither does or can report on expectations • Theory of financial markets (and economics of uncertainty) is built on expectations • Need data on expectations to empirically distinguish among competing theories (c) Copyright Shyam Sunder 4

Relating Market Actions to Expectations and Parameters • In experimental markets, the researcher knows the expectations, and the underlying parameters • With this knowledge, we know the price and other predictions of alternative theories • We can therefore conduct powerful tests of theories which were not possible from the field data (because we know little about the parameters and expectations that generate the field data from the stock exchanges). • Examples to follow (c) Copyright Shyam Sunder 5

2. What Can Simple Experiments Tell Us about Complex Markets? • Experimental markets are typically conducted in simple settings • Student subjects of typical laboratory experiments have little experience • Security markets are complex, and populated by experienced professionals • What could we possibly learn from experiments about the “real” markets? (c) Copyright Shyam Sunder 6

Simplicity is Science • All sciences aim at finding simple principles that explain or predict a large part (rarely all) of the phenomenon of interest • Simple models: in math or in laboratory make core as well as convenience assumptions • The power of a theory depends on the robustness of its predictions as the data environments deviate from the assumptions of convenience (c) Copyright Shyam Sunder 7

Simple Experiments Help Discover/Verify Basic Principles • • How do we learn to count? How do we learn to swim? How do we learn the laws of electricity? Noise generated by countless factors in complex environments makes it difficult to detect the fundamental principles • Simple math and laboratory models help us learn better, before we immerse ourselves in the complexity of the real phenomena • If the principle is general, it better be applicable to the simple environments (c) Copyright Shyam Sunder 8

3. Is This Behavioral Economics/Finance? • Experimental economics: emphasis is on design of market and other economic institutions to gather empirical data – Institutions and rules matter (e. g. , microstructure) – People do what they think is best for them, given what they know (they learn, are not dumb) – Design experiments to sort out the claims of competing theories – Engineer test beds for alternative institutions – Focus on equilibrium, efficiency, prices, and allocations – Complements modeling and field empirical research (c) Copyright Shyam Sunder 9

4. What Have We Learned from Experiments? • Within the past two decades, asset market experiments have revealed some important findings by exploiting their advantages • These findings were not, and could not have been, reached from the field data alone • We shall summarize a few key findings in the time available (c) Copyright Shyam Sunder 10

Key Findings • Security markets can aggregate and disseminate information (efficient markets) • But they do not always do so (inefficiency) • Information dissemination, when it occurs, is rarely instantaneous or perfect (learning takes time) • Markets permit costly research to persist in equilibrium (why pay for research? ) • Price, as well as bids, offers, timing, etc. , transmit information (many channels for information flow) (c) Copyright Shyam Sunder 11

More Findings • Well-functioning derivative markets help improve the efficiency of primary markets • Most important: statistical efficiency or inability to make money from past data does not mean informational efficiency (can’t make money if the price is right) (c) Copyright Shyam Sunder 12

Efficient Markets: Information Dissemination • Can markets disseminate information from those who know to those who don’t? • Could not be established from analysis of field data because we don’t know the distribution of information among investors • Plott and Sunder (Journal of Political Economy, 1982) established the basic proposition through a simple experiment (c) Copyright Shyam Sunder 13

Equilibria in a Simple Asset Market State X Prob. =0. 4 State Y Prob. =0. 6 Trader Type I II III PI Eq. Price Asset Holder RE Eq. Price Asset Holder 400 100 300 150 125 175 400 220 Trader Type I Uninformed I Informed 400 175 Trader Type (c) Copyright Shyam Sunder III I Expected Dividend 220 210 155 220 Trader Type I 14

(c) Copyright Shyam Sunder 15

Results • Markets can disseminate information from the informed to the uninformed investors • Dissemination can occur through trading, without exchange of verbal communication • Such markets can achieve high levels of informational efficiency • Securities end up in the hands of those who value them most (c) Copyright Shyam Sunder 16

Efficient Markets: Information Aggregation • Can markets behave as if diverse information in the hands of a few is aggregated so it is in the hands of all? • Suppose there are three possible states of the world: X, Y and Z • Some people know that the state is Not X, and some people know that it is Not Y • Can the market behave as if everyone knows that the state is Z? • Plott and Sunder (Econometrica, 1988) • Choo et al. (Experimental Economics, 2017) (c) Copyright Shyam Sunder 17

Equilibria in an Information Aggregation Experiment Traders X-Asset Y-Asset Z-Asset I II III X Y Z 70 0 0 230 0 0 100 0 0 X Y Z 0 130 0 0 90 0 0 160 0 X Y Z 0 0 300 0 0 60 0 0 200 RE Eq. P 230 0 160 0 300 Holder II - III - - - I - - (c) Copyright Shyam Sunder 18

(c) Copyright Shyam Sunder 19

Aggregation Results • Complete markets can aggregate and disseminate diverse information • Such markets can achieve high information and allocative efficiency • Same happens when investors have homogenous preferences (which makes it easier for traders to infer information from actions of others) (c) Copyright Shyam Sunder 20

Inefficiency • Just because markets can aggregate and disseminate information does not mean that all markets do so under all conditions • Experiments show that market conditions must allow investors the opportunity to learn the information from what they can observe • Even in these simple experimental markets, these conditions are not always satisfied (too many states, too few observations and repetitions to facilitate learning) • For example, a complete market for three Arrow. Debreu securities is efficient, but an incomplete market for a single security is not (c) Copyright Shyam Sunder 21

Learning Takes Time • Even in the best of circumstances, equilibrium outcomes are not achieved instantaneously • Markets tend toward efficiency, but cannot achieve it instantaneously • It takes time for investors to observe, form conjectures, test them, modify their strategies, etc. • With repetition, investors get better at learning, but the environment changes continually, including the behavior of other investors; so the learning process never ends (c) Copyright Shyam Sunder 22

Many Channels for Information Flow • In economic theory, transaction prices are considered the primary vehicle for the transmission of information in markets • Experimental markets show that other observables (bids, asks, volume, timing, etc. ) also transmit information in markets • In deep markets, price can be the result of the information transmission through these other variables • Example: see trading in period 8 on slide number 15 (c) Copyright Shyam Sunder 23

Effect of Derivatives on Primary Markets • Derivative markets help increase the efficiency of primary markets • Forsythe, Palfrey and Plott (Econometrica 1982), the first asset market experiment, showed that futures markets speed up convergence to equilibrium in the primary market • Kluger and Wyatt found that the option markets increase the informational efficiency of the equity market (c) Copyright Shyam Sunder 24

Convergence with Two Spot Markets (c) Copyright Shyam Sunder 25

Convergence with a Spot and a Futures Market (c) Copyright Shyam Sunder 26

Error in Pricing Primary Security with and without Option Market (c) Copyright Shyam Sunder 27

How Can We Tell If a Market is Efficient? • Traditional statistical approach: if you can’t make money from information (past data, public, or all information), the market is efficient • Experiments: statistical efficiency is a necessary but not a sufficient condition for the informational efficiency of markets • Example: Slide 19, second half is efficient by statistical criteria but is not informationally efficient • Even when investors know that the price is not right, they may have no means of profiting from that knowledge (c) Copyright Shyam Sunder 28

5. What Is Next? • The above is a highly selective summary of what we have learned from experimental asset markets • What is coming up next? • The existence and causes of market bubbles is a perennial subject in financial economics • What might we learn about bubbles from experiments? (c) Copyright Shyam Sunder 29

Bubbles in Simple Asset Markets • Smith, Suchanek and Williams (Econometrica 1988) showed that bubbles can arise in simple asset markets with inexperienced subjects, and tend to diminish with experience • Lei, Noussair and Plott (Econometrica 2001) showed that bubbles can arise even when investors cannot engage in speculative trades. They suggest that bubbles can arise from errors in decision making even in absence of a lack of common knowledge of rationality (“bigger fool” beliefs) (c) Copyright Shyam Sunder 30

(c) Copyright Shyam Sunder 31

Valuing Equity without Dividend Anchors • Fundamental economic model of valuation is DCF • When security matures beyond investment horizon, personal DCF includes the sale price at horizon • Sale price depends on other investors’ expectations of DCF beyond my own horizon • Applying DCF involves backward inducting from the maturity of the security through the expectations and valuations of the future “generations” of investors (c) Copyright Shyam Sunder 32

Valuation be Equal to Fundamental Value if • • All investors form rational expectations All investors form higher order expectations Common knowledge of rational expectations Common knowledge of higher order expectations Common knowledge of maturity These are very difficult conditions to meet in a market Bubbles arise, even with rational investors who make no errors, if they cannot backward induct the DCF (c) Copyright Shyam Sunder 33

Exogenous Terminal Payoff Period 15 15 -period security, termination date is common knowledge Single terminal dividend (may vary across traders) A separate set of subjects record their price predictions at the beginning of each period, their mean is announced at the end of each period Hirota and Sunder (2002), Yale Working Paper (c) Copyright Shyam Sunder 34

Figure 4: Stock Prices and Efficiency of Allocations for Session 4 (Exogenous Terminal Payoff Session) (c) Copyright Shyam Sunder 35

Endogenous Terminal Payoff Period 15 -17 Period 30 30 -Period Security with a terminal dividend to be paid at the end of period 30 The security will be terminated earlier than 30 at a time written in the sealed envelope (in fact terminated at 15 -17 periods) Liquidation at average of the prices predicted by the predictors for the period following termination (c) Copyright Shyam Sunder 36

Figure 10: Stock Prices and Efficiency of Allocations for Session 8 (Endogenous Terminal Payoff Session) (c) Copyright Shyam Sunder 37

Understanding Bubbles • DCF valuation makes heroic assumptions about the knowledge necessary to do backward induction • Even if investors are rational and make no mistakes, it is unlikely that they can have the common knowledge necessary for price to be equal to fundamental valuation in a market populated by limited horizon investors • Not surprisingly, pricing of new technology, high growth, and high risk equities are more susceptible to bubbles • In such circumstances, if we do not have common knowledge of higher order beliefs, how can we test valuation theories? (c) Copyright Shyam Sunder 38

Paradox of Efficient Markets: Why Pay for Research? • This has been the conundrum of the efficient market theory: If the markets are efficient, why pay for research. • This finite rate of learning makes it possible to support costly research, even in markets which tend toward efficient outcomes • Enough people would conduct research so the average returns to research equal the average cost. Research users have higher gross profits, but their net profits are the same as the profits of the others • Grossman and Stiglitz (1980) • Sunder (Econometrica, 1993) (c) Copyright Shyam Sunder 39

Is It Just a Theoretical Problem • Conduct an experiment to resove the issue • Two markets: – One market for information – One market for assets whose values are uncertain, but you can buy information about the values • Two treatments – All 12 traders submits their bids for information, and the top four bidders get the information (privately at the fifth highest bid price – Experimenter announces the price of information, and all those who wish to can buy information at that price

Market 1: Supply Q Fixed

Market 2: Price of Information Fixed

Market 3: Q Fixed, P Fixed

Market 4: Price Fixed

(c) Copyright Shyam Sunder 45

Mean Absolute Price Deviations from FR

Cross-sectional SD of Trader Profits

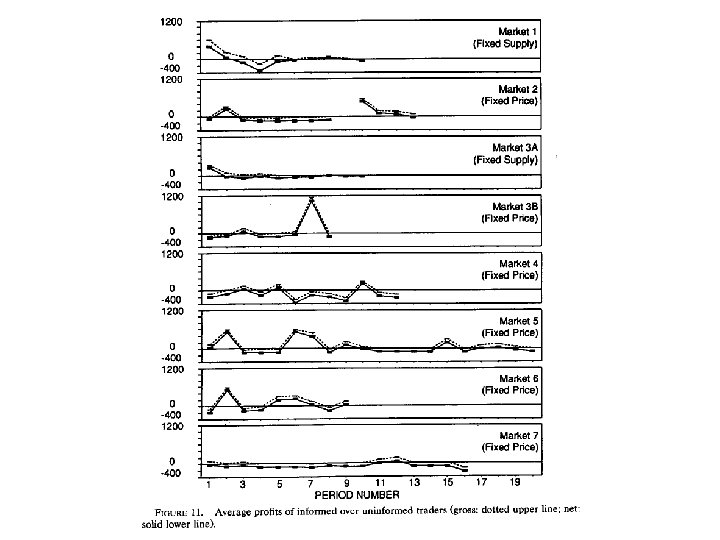

Diff. of Gross and Net Profits of Informed and Uninformed (c) Copyright Shyam Sunder 48

Results • As investors learn (in a fixed environment), their value of information decreases because they can ride free on others’ information • Market price of information falls • If the supply of information can be sustained at the lower price, price drops to a level sustainable by learning frictions: get equilibrium • If the supply of information also falls with its price, we get a noisy equilibrium • Consequences of mandating provision of free research to investors (c) Copyright Shyam Sunder 50

Thank You!

Wrap Up • Only a thumbnail sketch of some experimental results on asset markets • Could not discuss many other important and interesting studies • See Sunder’s survey paper in Kagel and Roth’s Handbook of Experimental Economics (c) Copyright Shyam Sunder 52

Better Understanding • As the experimental camera focused on information processing in asset markets, theoretical line drawing has been filled by details, shadows, color, and warts • This finer grain portrait of asset markets confirms the rough outline of the extant theory • But it is considerably more complex, and is providing guidance and challenges for further theoretical investigations of interplay of information in asset markets (c) Copyright Shyam Sunder 53

Thank You (c) Copyright Shyam Sunder 54