Expectations Consumption and Investment CHAPTER 16 Prepared by

Expectations, Consumption, and Investment CHAPTER 16 Prepared by: Fernando Quijano and Yvonn Quijano Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall • Macroeconomics, 5/e • Olivier Blanchard

Chapter 16: Expectations, Consumption, and Investment 16 -1 소비 프리드먼과 모디리아니에 의하여 1950년대에 항상소득 소비이론(permanent income theory of consumption)과 평생주기 소비이론(life cycle theory of consumption)이 개발. Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall • Macroeconomics, 5/e • Olivier Blanchard 2 of 27

16 -1 Consumption 매우 계획적인 소비자 Chapter 16: Expectations, Consumption, and Investment 자신의 총 부에 근거하여 얼마를 소비할 지를 결정하는 계획 적인 소비자의 경우, 총 부(total wealth)는: 1. 금융자산 부와 부동산 부(financial wealth and housing wealth)의 합인 비 인적 부(nonhuman wealth). 2. 그리고 인적 부(human wealth). 인적 부와 비 인적 부(nonhuman wealth)의 합이 총 부(total wealth). Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall • Macroeconomics, 5/e • Olivier Blanchard 3 of 27

Chapter 16: Expectations, Consumption, and Investment Up Close and Personal: Learning from Panel Data Sets Panel data sets are data sets that show the value of one or more variables for many individuals or many firms over time. Among the many questions for which the Panel Study of Income Dynamics (PSID) has been used are: § How much does (food) consumption respond to transitory movements in income—for example, to the loss of income from becoming unemployed? § How much risk sharing is there within families? For example, when a family member becomes sick or unemployed, how much help does he or she get from other family members? § How much do people care about staying geographically close to their families? Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall • Macroeconomics, 5/e • Olivier Blanchard 4 of 27

")

16 -1 Consumption Chapter 16: Expectations, Consumption, and Investment 예 노동소득의 현재가치를 세후(세율 25%) 기대되는 실질 소득을 실질이자율로 할인하여 구하면(19세부터 노동 하여 60세에 은퇴하고 소득은 년 3%로 증가한다고 상 정). 생애동안 기대되는 세후 실질 소득의 현재가치는 약 2 백만달러. Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall • Macroeconomics, 5/e • Olivier Blanchard 5 of 27

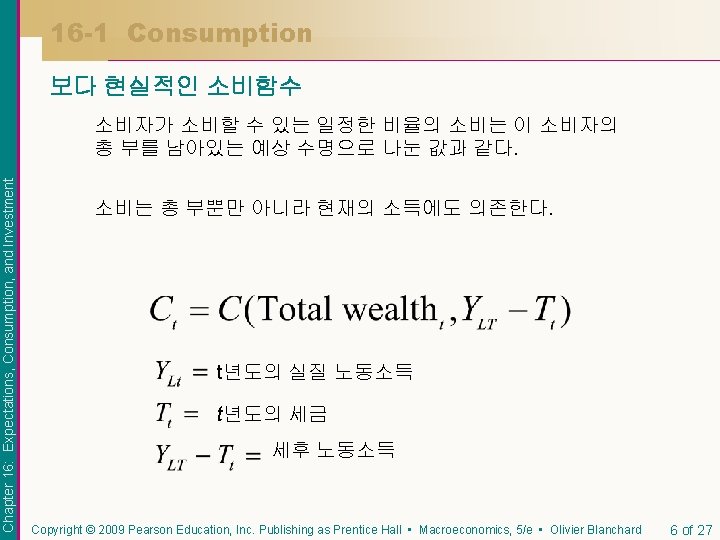

16 -1 Consumption Toward a More Realistic Description Chapter 16: Expectations, Consumption, and Investment 즉, 소비는 총 부의 증가함수이고, 또한 세후 노동소 득의 증가함수이다. 총 부는 금융자산 및 부동산 과 같은 비인적 부와 세후 노동소득의 현재가치 인 인적 부의 합이다. Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall • Macroeconomics, 5/e • Olivier Blanchard 7 of 27

Chapter 16: Expectations, Consumption, and Investment Do People Save Enough for Retirement? Table 1 Mean Wealth of People, Age 65 -69, in 1991 (in thousands of 1991 dollars) Social Security Pension $100 Employer-provided pension 62 Personal retirement assets 11 Other financial assets 42 Home equity 65 Other equity 34 Total $314 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall • Macroeconomics, 5/e • Olivier Blanchard 9 of 27

16 -1 Consumption Chapter 16: Expectations, Consumption, and Investment Putting Things Together: Current Income, Expectations, and Consumption 소비가 기대에 의존한다는 사실은 소비와 소득간의 관계에 있 어서 2 가지 중요한 시사점을 준다: 1. 소비는 경상소득의 변동과 1: 1 보다 작게 반응한다. 2. 경상소득이 변하지 않아도 소비는 변동한다. 소비자의 신뢰변화로 소비는 경상소득 불변상황에서도 변화 할 수 있다. Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall • Macroeconomics, 5/e • Olivier Blanchard 10 of 27

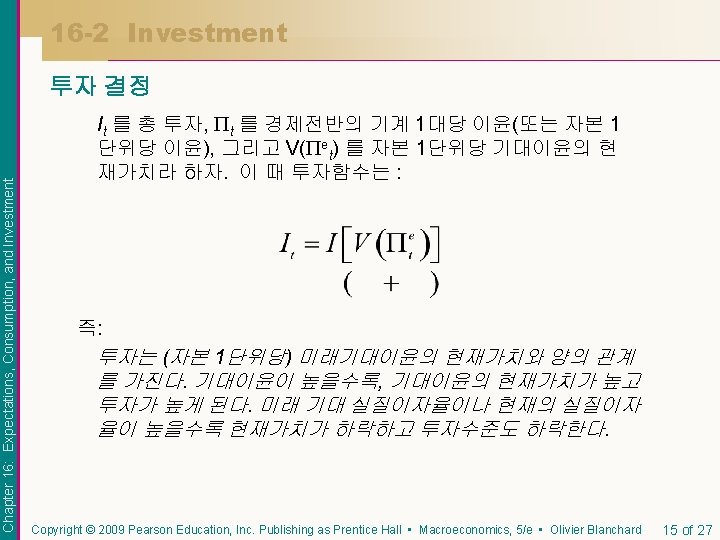

16 -2 투자 Chapter 16: Expectations, Consumption, and Investment 투자는 경상 매출, 경상 이자율, 그라고 미래의 기 대에 의존한다. 지금 기계 1대를 구입할 지의 여부는 기계 구입에 대한 기대이윤의 현재가치가 기계 구입에 따른 비용보다 큰 가에 의존한다. Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall • Macroeconomics, 5/e • Olivier Blanchard 11 of 27

은")

16 -2 Investment 투자와 기대이윤 Chapter 16: Expectations, Consumption, and Investment 감가상각률(depreciation rate, )은 기계가 1년 뒤에 얼마 나 유용한 지를 측정한다. 에 대한 합리적인 추정값은 기계는 년 4 - 15%, 빌딩이나 공장은 2 - 4%이다. Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall • Macroeconomics, 5/e • Olivier Blanchard 12 of 27

:")

16 -2 Investment 기대 이윤의 현재가치 Chapter 16: Expectations, Consumption, and Investment V( et): t+1년도 이후에 기대되는 이윤의 (t 년도의) 현재 가치: In year t+2, In year t, Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall • Macroeconomics, 5/e • Olivier Blanchard 13 of 27

16 -2 Investment The Present Value of Expected Profits Chapter 16: Expectations, Consumption, and Investment Figure 16 - 1 기대 이윤의 현재가치 계산 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall • Macroeconomics, 5/e • Olivier Blanchard 14 of 27

16 -2 Investment 특별한 경우 Chapter 16: Expectations, Consumption, and Investment 기업이 예상하는 미래이윤과 이자율이 현재수준과 동일하 다고 상정하자. and 이러한 기대(미래 기대값 = 현재값)를 정태적 기대(static expectations)라 한다. 상기 가정하에서 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall • Macroeconomics, 5/e • Olivier Blanchard 16 of 27

는 자본 1단위의 구입가격과 자본 1단위의 가 Chapter 16: Expectations,")

I투자와 주식시장 토빈의 q(Tobin’s q)는 자본 1단위의 구입가격과 자본 1단위의 가 Chapter 16: Expectations, Consumption, and Investment 치의 비율이다. Figure 1 Tobin’s q versus the Ratio of Investment to Capital: Annual Rates of Change, 1960 to 1999 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall • Macroeconomics, 5/e • Olivier Blanchard 17 of 27

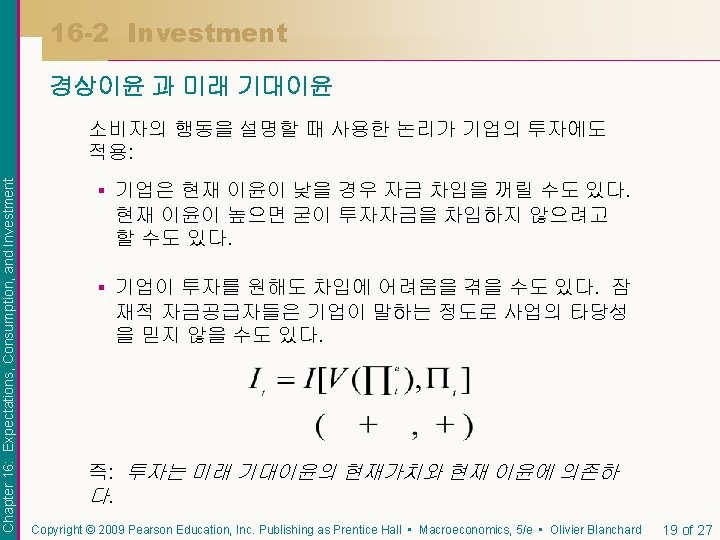

16 -2 Investment 특별한 경우 Chapter 16: Expectations, Consumption, and Investment 다음 2 식 수는 으로부터 투자함 실질이자율과 감가상각률의 합을 사용자 비용 또는 자본의 임대비용(user cost or the rental cost of capital)이라 한다. 따라서: 임대비용 = Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall • Macroeconomics, 5/e • Olivier Blanchard 18 of 27

16 -2 Investment Current versus Expected Profit Figure 16 - 2 Chapter 16: Expectations, Consumption, and Investment 1960년 이후 미국에서 나 타난 투자와 이윤의 변화분 간의 관계 Investment and profit move very much together. Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall • Macroeconomics, 5/e • Olivier Blanchard 20 of 27

은 미래 기대이윤의 현재가")

Chapter 16: Expectations, Consumption, and Investment Profitability versus Cash Flow 수익성(Profitability)은 미래 기대이윤의 현재가 치를. 현금흐름 (Cash flow)은 경상이윤, 즉 기업이 받 게 되는 순 현금흐름을 이야기 한다. 수익성과 유동성 모두 투자경정에 중요하며 이 들은 같은 방향으로 움직인다. . Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall • Macroeconomics, 5/e • Olivier Blanchard 21 of 27

16 -2 Investment 이윤과 매출액 Chapter 16: Expectations, Consumption, and Investment Figure 16 - 3 1960년이후 미국의 자본 1 단위당 이윤변화와 자본/산 출물 변화. Profit per unit of capital and the ratio of output to capital move largely together. (+) Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall • Macroeconomics, 5/e • Olivier Blanchard 22 of 27

16 -3 The Volatility of Consumption and Investment Chapter 16: Expectations, Consumption, and Investment 그러나 소비 결정과 투자결정에는 중대한 차이가 있다. § 소비자가 항구적 소득 변동으로 인지하면 소비도 거의 비슷한 비율로 항구적으로 번동. § 기업이 항구적 매출증가로 인지하여 이것이 이윤 의 현재가치에 영향을 미치고 투자를 증가시킨다. Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall • Macroeconomics, 5/e • Olivier Blanchard 24 of 27

16 -3 소비와 투자의 변동성 Chapter 16: Expectations, Consumption, and Investment Figure 16 - 4 1960년이후 소비변화율과 투자변화율의 변동폭이 소비변화율의 변동폭보 다 훨씬 크다. Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall • Macroeconomics, 5/e • Olivier Blanchard 25 of 27

16 -3 The Volatility of Consumption and Investment Chapter 16: Expectations, Consumption, and Investment 상기 그림은 3 가지 시사점을 준다: § 소비와 투자는 동행성을 지닌다. § 투자가 소비보다 변동성이 훨씬 크다. § 그러나 투자 수준이 소비수준보다 훨씬 작기 때문에 년간 투자 변동규모가 년간 소비의 규모가 거의 비슷 하다. Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall • Macroeconomics, 5/e • Olivier Blanchard 26 of 27

Chapter 16: Expectations, Consumption, and Investment Key Terms § permanent income theory of consumption § life cycle theory of consumption § financial wealth § housing wealth § human wealth § nonhuman wealth § total wealth § panel data sets § Tobin’s q § static expectations § user cost of capital, or rental cost of capital § profitability § cash flow Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall • Macroeconomics, 5/e • Olivier Blanchard 27 of 27

- Slides: 27