Estimating Private Equity Returns from Limited Partner Cash

= PV(Distributions) ●")

- Slides: 30

Estimating Private Equity Returns from Limited Partner Cash Flows Andrew Ang, Bingxu Chen, Will Goetzmann, Ludovic Phalippou Q-Group, Apr 2014

Liquidating Harvard: A Cautionary Example “Liquidating Harvard” Columbia Case available from http: //www 8. gsb. columbia. edu/caseworks/node/236/Liquidating%2 BHarvard

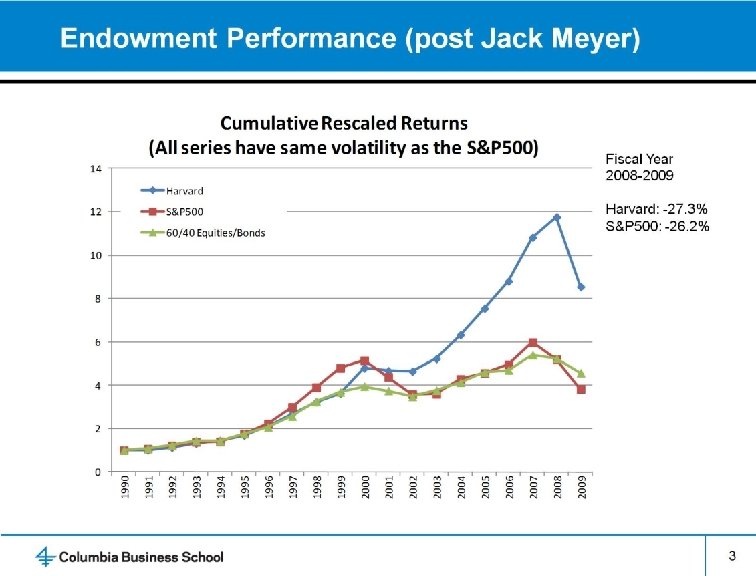

Harvard Endowment ● Harvard was an early adopter of the “endowment” model based on diversification concepts extended to illiquid assets (thanks to Swensen, Leibowitz, and others) 5

“Returns” on Illiquid Assets ● Illiquid asset “returns” are not returns ● Harvard University President Faust, on the 22% loss between July 1 and October 31, 2008: “Yet even the sobering figures is unlikely to capture the full extent of actual losses for this period, because it does not reflect fully updated valuations in certain managed asset classes, mostly notably private equity and real estate. ” ● Returns of illiquid alternatives are biased upwards, and their risk estimates are biased downwards 6

Infrequent Trading ● Infrequent trading biases volatility and beta estimates downwards. 7

Infrequent Trading ● Infrequent trading biases volatility and beta estimates downwards. 8

Infrequent Trading ● Infrequent trading biases volatility and beta estimates downwards. 9

Sample Selection Bias ● Selection biases the average return upwards, systematic risk downwards, and idiosyncratic volatility downwards. Excess Return True Excess Market 10

Sample Selection Bias ● Selection biases the average return upwards, systematic risk downwards, and idiosyncratic volatility downwards. Excess Return True Fitted Excess Market 11

Building a Private Equity Return Index “Estimating Private Equity Returns from Limited Partner Cash Flows” http: //papers. ssrn. com/sol 3/papers. cfm? abstract_id=2356553

Current Approaches Based on ● NAVs ● Deal-level ● IRRs ● Multiples Do not represent returns, and not based on the actual cash flows received by LPs 13

Private Equity Returns ● Based on cashflows to LPs – What you actually “eat” – Data from Prequin and proprietary datasets ● Decompose into market and other factors, and the private equityspecific return (PE “alpha” or “premium”) ● Can be updated in “real time” to create a private equity return index 14

How Does It Work? ● Suppose the private equity total return, g, follows – rmt is the market return – f is the return specific to PE – Risk-free return is zero 15

How Does It Work? ● Consider the cashflows of four funds, living between times t=0 to t=4 16

How Does It Work? ● According to a NPV condition, PV(Investments) = PV(Distributions) ● With four funds, there are four unknowns—can solve using a non -linear root solver 17

How Does It Work? ● If the private equity return, g, were constant then there would be four funds/equations with one unknown resulting in an overidentified system if g is persistent (not iid), then we also require fewer funds/equations ● Similarly, ● Identification is achieved by having funds with different cashflows at different start dates, and different end dates 18

Model ● Total private equity return: ● Private ● NPV equity-specific component is allowed to be persistent: condition for distributions, D, and invested capital, I: 19

20

Comparison with Industry Indexes ● Our cash flow-implied returns are more volatile, with lower autocorrelations than industry indexes 21

22

23

24

Alphas 25

26

27

Pro-Cyclical Investing in Private Equity 28

Private Equity Returns Over the Business Cycle 29

Private Equity Returns ● Reported ● IRRs returns on PE are not returns! and multiples are not returns! ● Develop a time series of private equity values representing the returns to an investor (LP), not a fund, and not a manager (GP) ● Decompose private equity returns into passively replicable returns, and the unique return to private equity (“alpha” or “premium”) 30