Employee Benefits Why benefits n Types of benefits

Employee Benefits Why benefits? n Types of benefits n ¨ Legally required benefits ¨ Security and retirement benefits ¨ Health coverage ¨ Time off work ¨ Employee services

Why Benefits? Legal requirements n Employee attraction and retention n Non-taxable compensation to employee n Employer can often purchase at more favorable rate n Employee morale, well-being n

Legally Required Benefits Workers’ compensation n Social security n Unemployment compensation n Family/medical leave n Continuation of health coverage n

Workers’ Compensation: Definition and Purpose n n n Covers injury or disease arising from course of employment Employer normally relieved of other liability for injuries / diseases Goals of workers’ compensation ¨ ¨ ¨ Prompt and reasonable compensation to victims of work accidents Eliminate delays, costs, and waste in personal injury cases Reduce the number of accident cases Provide prompt and adequate medical treatment Rehabilitate injured workers

What is covered:")

Workers’ Compensation: Coverage n n Paid by employer (insured or self-funded) What is covered: ¨ ¨ ¨ n n Total disability, temporary or permanent (up to 400 weeks, or until age 65 for permanent disability) Partial disability (elaborate schedule of body parts and $) Survivor’s benefits Medical expenses (employer selects; includes psychologists in Tennessee) Rehabilitation Payment tied to earnings (to 66 2/3% of pay, up to a cap of $784 (temporary) or $713 (permanent) per week, in Tennessee) Permanent disability payments integrated with Social Security

Workers’ Compensation: Cost Issues n Rising costs In 2000, 1. 03% of payroll (down from 1. 68% in 1992 and 1. 29% in 1999) ¨ Can run up to 25% in hazardous industries ¨ n Why? Rising medical costs ¨ Worker abuse ¨ Inclusion of stress-related illnesses ¨ n What can be done? Medical cost control (managed care, utilization review, bill audit, fee schedules) ¨ Monitor worker status ¨

Social Security: Overview n Benefits for: ¨ Retirement ¨ Disability ¨ Survivors (lump sum and monthly payments) Based on contributions from employers and employees n Majority of U. S. workers covered n

: n ¨ Old age/survivors’/disability")

Social Security: Coverage Payment tied to contributions n Amounts (2008): n ¨ Old age/survivors’/disability - 6. 2%, up to $102, 000 ¨ Health - 1. 45%, no earnings cap n Should social security be moved to the private sector?

Employer contributions, often with")

Unemployment Compensation n Administered by states (coverage varies by state) Employer contributions, often with experience ratings Who is covered? ¨ ¨ ¨ n n People able to work and actively seeking work Cannot have refused employment Not on strike Not voluntarily quit Not terminated for gross misconduct Previously employed in a covered job Payments for 26 weeks In theory, 50% of wages up to a cap ($275/week)

n Unpaid leave up to 12 weeks per")

Family And Medical Leave Act (FMLA) n Unpaid leave up to 12 weeks per year Seriously ill family member ¨ Own illness ¨ Birth of a child ¨ Adoption of a child ¨ n n Companies with 50 or more employees, after 1 year employment Return to same or equivalent job Top 10% paid employees not eligible State laws or company policies may be more generous

Employee pays")

COBRA n n n Provides for continuation of health coverage (if offered) Employee pays 102% of total cost Coverage period: ¨ 18 months for terminated employees ¨ 36 months for spouse / ineligible dependent

Security and Retirement Benefits Security benefits n Social Security n Life insurance n Long-term disability coverage n Long-term care benefits Retirement benefits n Social Security n Defined benefit plans n Defined contribution plans n 401(k) plans n ESOPs n IRA / SEP / Keogh plans

ERISA Provisions n n n Passed in 1974 in response to abuses of pension plans Does not require that a plan be offered ERISA covers: Who is eligible? ¨ Vesting (entitlement to employer contributions) ¨ Plan funding required ¨ n Also established Pension Benefit Guarantee Corporation Employers required to pay premiums to PBGC to cover company bankruptcies ¨ If necessary, PBGC will assume payments ¨

Eligibility and Vesting n Eligibility ¨ Age 21 ¨ One year’s service (1, 000 hours) ¨ May be eligible even if “contractor” (Microsoft case) n Vesting (right to employer’s contributions) ¨ Can be a 6 year or a 3 year schedule

Security Benefits Group term policies n Offered by 58% of employers n Commonly 1 x to 2 x annual salary n Employer paid (94% of employers) n Option to purchase additional coverage (group rates) AD & D Policies n Typically employee paid Short-Term Disability n Short-term disability may covered through sick leave policies n 39% of employers offer other coverage Long-term disability coverage n 31% access n LTD normally picks up after 6 months disability n 50% to 67% of previous salary and integrated with Social Security to provide up to 80% of previous salary n Often employee paid (so benefits are non-taxable)

Long-Term Care Benefits: Why n n n Becoming more popular as life span and medical costs increase In 2000…. 12. 4% of population over age 65; 1. 5% over age 85 Projected for 2050…. 20. 7%; 5% over age 8 Two-thirds of elderly have assets to pay for one year or less of nursing home care Estimated 7% to 12% of workforce is providing elder care; 33% of employees have lost work time and 27% of caregivers have left the workforce

Long-Term Care Benefits: Coverage n n Currently, offered by 12% of firms Employee paid Rates depend on age ($700/year for 40 year old) What is covered? In-home assistance ¨ Supervised living ¨ Skilled care ¨ n n May cover elderly dependents Lots of doubt, though, about quality of plans (http: //www. consumerreports. org/cro/money/insurance/longterm-care-insurance-1103/overview/)

Retirement Benefits: The Pension n Coverage Overall, 55% of employees are covered under one or more employer-sponsored plans ¨ Full-time = 64%, part-time= 27% ¨ n Average cost to employers ¨ n $1. 07 per hour worked Types of plans ¨ ¨ ¨ Defined benefit Defined contribution 401(k) plans ESOPs IRA / SEP / Keogh plans

Retirement Benefits: Defined Benefit Plans n n Once popular, now offered by fewer employers (currently only 22% of plans) Typically entirely funded by employer Social Security is a defined benefit plan Employer guarantees to: ¨ n “Provide a specific level of retirement pension that is expressed as either a fixed dollar or percentage-of-earnings amount that may vary (increase) with years of seniority” Pro and con Employer must fund future obligations (ERISA) ¨ Employer is assuming all risk ¨ Less attractive to employees, who no longer stay with one employer for entire career ¨

Retirement Benefits: Defined Contribution Plans n n More popular now (close to 80% of plans) Employer makes specific contributions; employee contributions may or may not be required or allowed ¨ n About 65% of plans do require employee contribution Pro and con More portable for mobile employees ¨ Employee assumes some risk; if employee contributions required, lower-paid employees may not participate ¨ Employees will need assistance counseling about investment options at retirement (although employer can’t actually give advice without incurring legal liability) ¨

plans Employee contributions required to participate ¨ May")

Retirement Benefits: Other Plans n 401(k) plans Employee contributions required to participate ¨ May be matched or partially matched by employer ¨ Contributions and earnings not taxed until withdrawal ¨ May or may not have investment choices ¨ n ESOP (Employee Stock Ownership Plan) Employer gains tax advantage from contributing stock to a trust for employees ¨ Employees may be reluctant to have retirement depend on employer’s stock ¨ Best results if combined with meaningful participation programs ¨

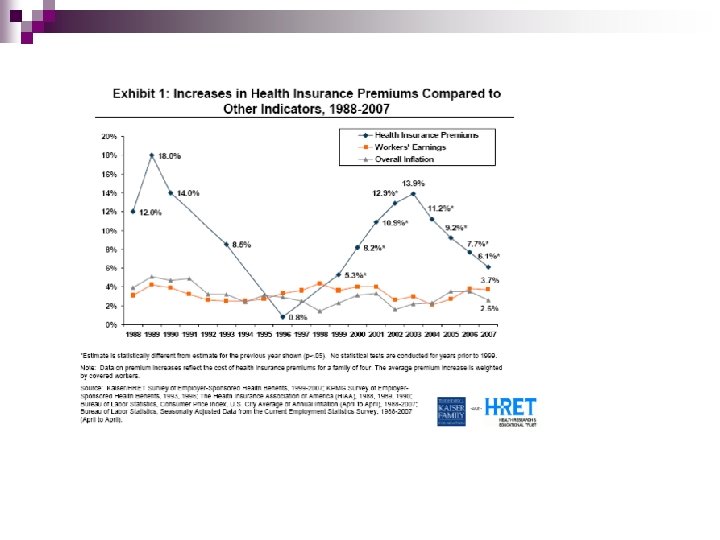

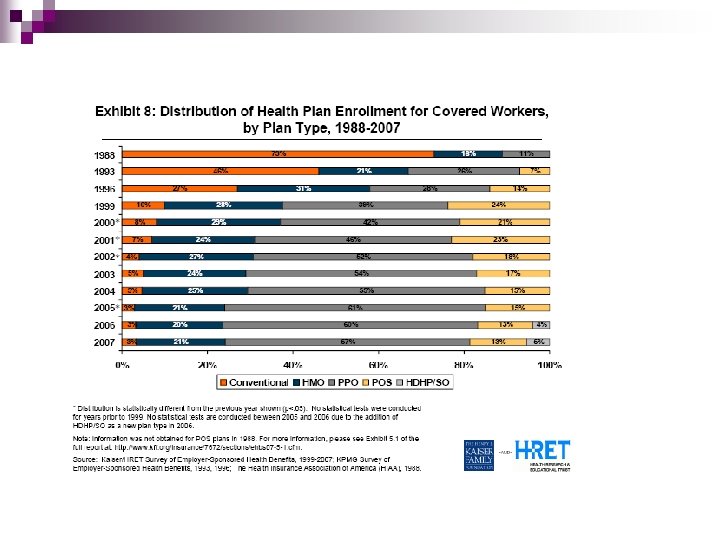

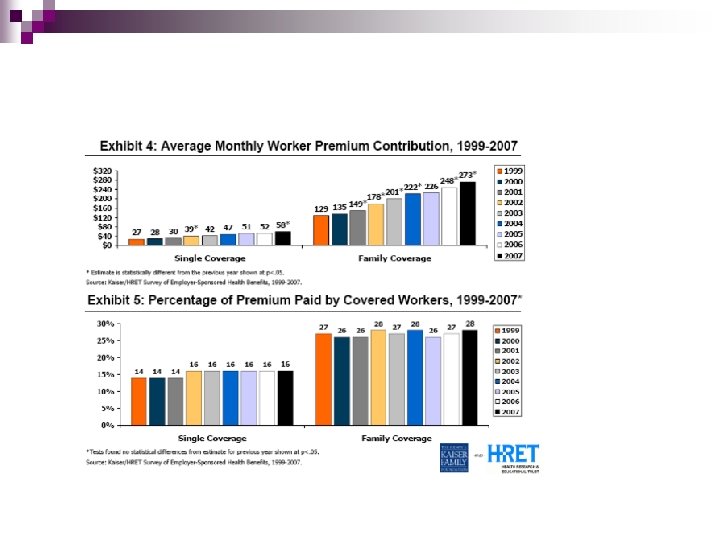

Health Coverage n n Overview only…. what we learn today won’t apply tomorrow The basic issue: cost containment Basic medical coverage Other coverage ¨ Mental health ¨ Vision ¨ Dental n Wellness programs

¨")

Who Has It? n According to BLS: 85% of full-time employees (64% participate) ¨ 24% of part-time employees (12% participate) ¨ n n But…. . ¨ Mini-meds ($2, 000 or less annual caps) ¨ High deductible plans (looking at $10, 000 annual cost) According to a Harvard Medical School study, health care costs contribute to about half of bankruptcy findings – even though the majority of the individuals had insurance at some point.

Trends in Insurance Coverage Source: Center for Studying Health System Change (http: //ctsonline. s-3. com/hhsurvey. asp)

Who Doesn’t Have Health Coverage Source: http: //www. kff. org/uninsured/upload/1420_09. pdf

Cost Containment Issues n n Estimated 6% to 7% annual increase in costs This, even with managed care, so. . ¨ Increased employee cost sharing (higher premiums, deductibles, copays) ¨ Employee wellness (keep them healthy) ¨ Other ideas n n Self-insurance Flexible spending accounts Bargaining with providers Mail-order prescriptions (for maintenance drugs)

Other Coverage n Mental health ¨ n Can be very costly, but, must be covered as other conditions Vision One big issue: laser surgery (an estimated 1 to 1½ million done per year) ¨ Can employers cover? Not in standard plans, but can add to high-end plans, set up flexible spending accounts, negotiate provider discounts ¨ n n Dental Contraceptives ¨ December 2000 EEOC decision held that under Pregnancy Discrimination Act, health plans must cover prescribed contraceptives as other prescription drugs

Employee Wellness Programs n n Idea is to reduce health care costs. . for the most part, successful over the long-term What’s included ¨ ¨ ¨ n Health screenings (blood pressure, cholesterol, mammograms) Education and advice (exercise, nutrition, etc. ) Exercise facilities Healthy cafeteria food Smoking cessation, weight loss Pre-natal education More and more popular; some form of program offered by 93% of U. S. employers (Hewitt Associates survey, 2002)

Time Off Work Vacations n Holidays n PTO plans n Other time off n

Vacations available to 77% of employees Source: Bureau of Labor Statistics 1997 survey

Holiday Policies n n n 77% of employees receive paid holidays; Average of 8 paid holidays per year Exact holidays vary by industry, part of country ¨ Financial / government ¨ The case of Mardi Gras

PTO Plans n PTO ¨ Paid Time Off ¨ A bank of days, accrued during the year, than can be used as the employee wishes ¨ Replaces vacation, holidays, short-term illness n Most often found in health care, but used by 18% of U. S. employers in 2000 (Hewitt Associates survey)

Other Time Off n Jury duty ¨ Must legally give time off ¨ Some employers make this paid time Military n Voting n Funeral / bereavement n

Employee Services n Traditionally, included ¨ Discounts n on products or services Today, anything goes ¨ Child care (on-site, assistance) ¨ Other employee services

- Slides: 37