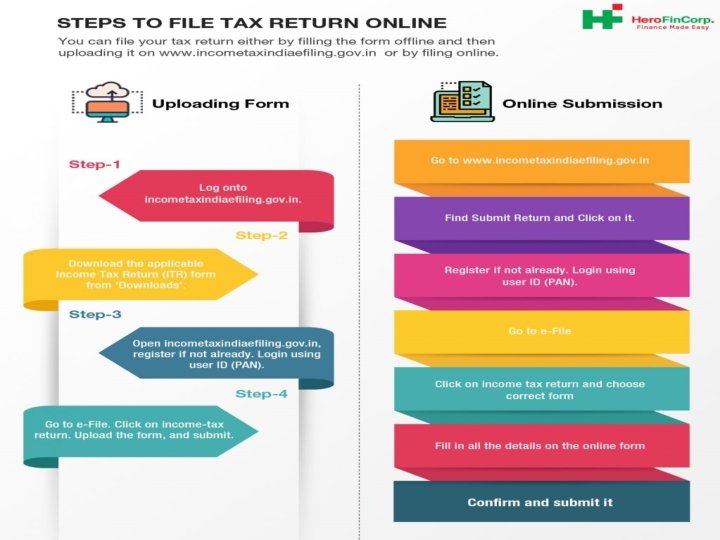

Efiling of Income Tax Returns An overview of

� 44 ADA- 50% (PROFESSION)")

Form 16/16 A 2) Bank Statement 3) House Property")

RELIEF If total income includes any past dues paid in the current")

Relief � Step 1: Calculate tax payable on the")

: � At investment stage , tax")

.")

, local authority - taxable at")

� LESS")

- Slides: 64

E-filing of Income Tax Returns An overview of the Process of efiling of Returns CA. M. K. PILLAI Bsc, FCA mjnmadhu@gmail. com 9400813410 Kottayam 26/06/18

AREAS OF DISCUSSION � ITR FILING PROCESS � HOW TO COMPUTE INCOME AND TAX � INFORMATION TO BE GATHERED � DOCUMENTS TO BE COLLECTED � FUNDFLOW STATEMENT � POST FILING FOLLOW UP

What is e-filing? � Filing of income tax returns is a legal obligation for every person whose total income for the previous year has exceeded the maximum amounts that is not chargeable for the income tax under the provisions of the Income Tax Act, 1961. � Income tax department has introduced a convenient way to file these returns online.

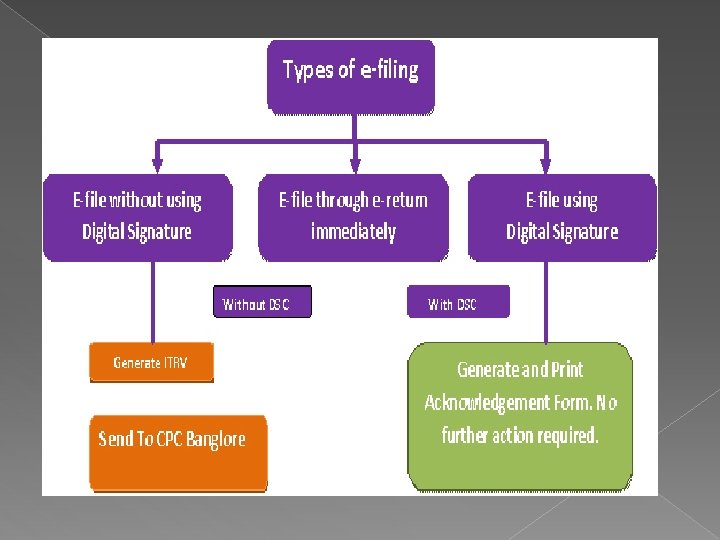

� The process of electronically filing income tax returns through the internet is known as e-filing. � E-filing is possible with or without digital signature.

Benefits of e-filing � Electronically submitting tax returns is much more easier and convenient! � Tax return information is encrypted and transmitted over secure lines to ensure confidentiality. � Electronically filed returns have lesser errors than paper returns. � There is sufficient acknowledgement generated after filing- so there is ample proof!!

Section 44 AB of the Income Tax Act, 1961 � Tax Audit as described under section 44 AB of Income Tax Act 1961 deals in examining the books of accounts of business or profession from Income Tax point of view. It is done by a chartered accountant and a mandatory audit to be carried out. It reviews the incomes, deductions, compliances, procedure related to Income Tax Act.

Objectives of Tax Audit u/s 44 AB � Tax audit makes the income computation for filing the returns more efficient. � The main intention behind tax audit is to assist the tax authorities to determine correct tax liability. � Tax audit also restricts the fraudulent practices. � Tax audit facilitates proper maintenance of books of accounts and revenue / expense. � Tax audits ensure proper administration of tax laws presentation and submission before the prescribed authorities.

Tax Audit Applicability under section 44 AB � If you are a resident in India and you are an Individual / HUF / Partnership firm, then if your annual gross turnover exceeds ` 1 crore it attracts tax audit. � An individual, who is a professional, i. e. engaged in any profession and his income receipts in a year aggregate Rs 50 lakhs and above as per notification 2017 -18.

This is also applicable in case the income on record is more than the amount which is taxfree or not chargeable for taxation i. e. Any individual who qualifies for the presumptive taxation scheme under section 44 AD but later claims that the profits for said business is lower than the profits calculated in accordance with the presumptive taxation scheme. � If the assessee who is qualified under the presumptive taxation scheme but opts out of it after a specified period, he would lose the ability to revert back to the presumptive taxation scheme for a continuous term of 5 assessment years after the decision to opt out is taken. �

� An individual who qualifies to choose the presumptive taxation scheme of selection under section 44 AE but then claims that the profits for such business are lower than the profits calculated in accordance with the presumptive taxation scheme of section 44 AE. � An individual who qualifies to choose the presumptive taxation scheme of selection under section 44 BBB but then claims that the profits for such business are lower than the profits calculated in accordance with the presumptive taxation scheme of section 44 BBB.

Tax audit forms required For persons or individuals carrying on a business or a profession whose accounts are to be audited as per the provisions stated under any kind of law, the following forms are applicable: � Form Number 3 CA – Audit Form � Form Number 3 CD – Statement showing relevant particulars

For persons or individuals whose accounts are not required to be audited as per the provisions stated under any kind of law, with the exception of income tax laws, then the forms mentioned below are applicable: � Form Number 3 CB – Audit Form � Form Number 3 CD – Statement showing relevant particulars

PRESUMPTIVE TAXATION � 44 AD – 8%/6%( ELECTRONIC MODE) � 44 ADA- 50% (PROFESSION) � 44 AE – 7500/ ACTUAL WHICH EVER IS HIGHER (PLYING) � 44 AF – 5%(RETAIL)

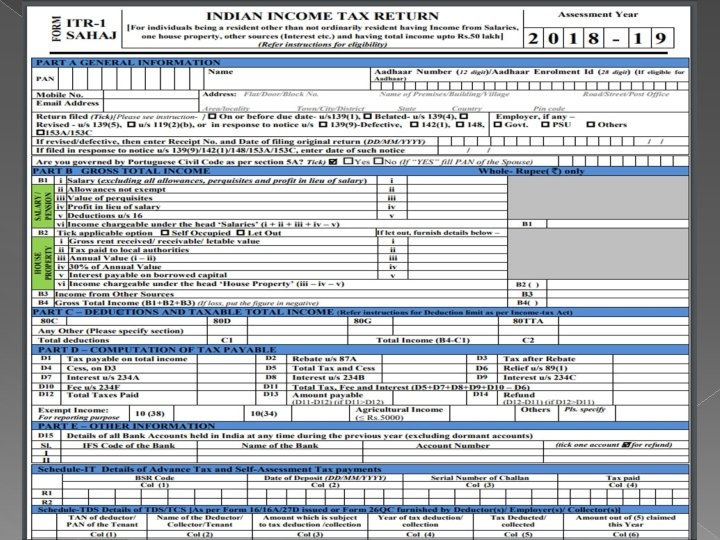

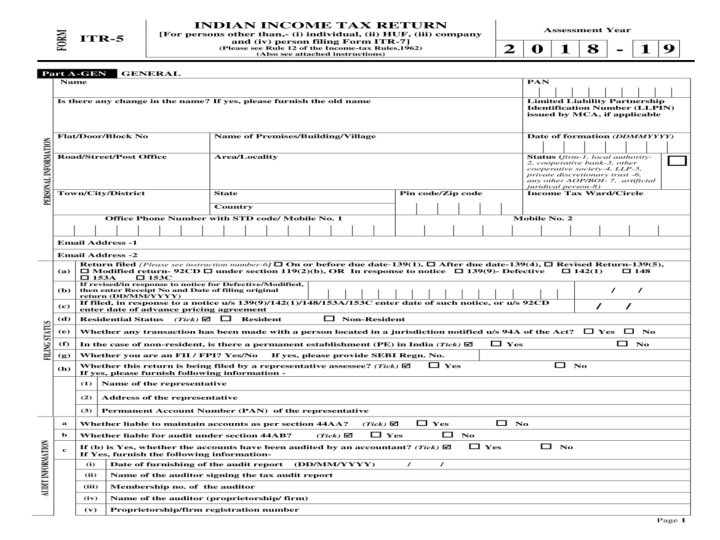

Different types of ITR forms

Sample forms of ITR 1 to 7 and Acknowledgement

INCOME TAX COMPUTATION

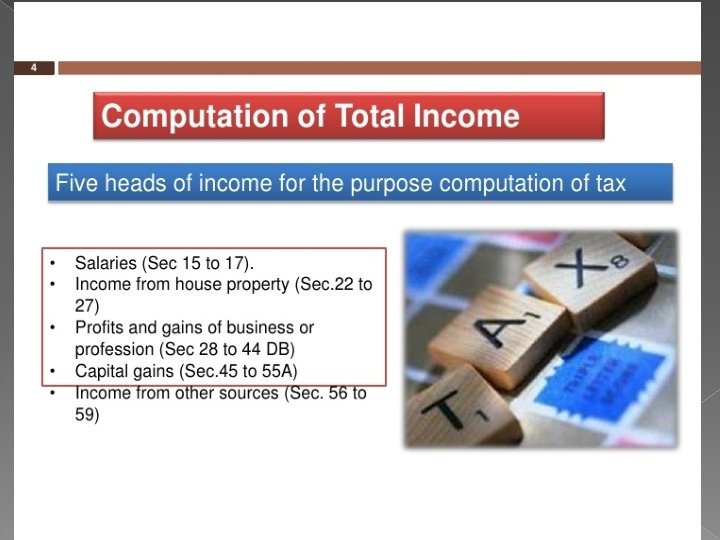

THRUST AREAS � HEADS OF INCOME � CALCULATION OF TAXABLE INCOME � EXEMPTIONS � ALLOWABLE DEDUCTIONS � CALCULATION OF TAX LIABILITY

Documents to be gathered 1) Form 16/16 A 2) Bank Statement 3) House Property Details- (Housing Loan Statement, Rent Received, Municipal tax paid for the Property. . etc ) 4) Medical Insurance, if any 5) Tuition Fee paid, if any 6) LIC paid, if any. 7) Donation, if any - (Please provide Receipt) 8) FD Details etc.

HEADS OF INCOME

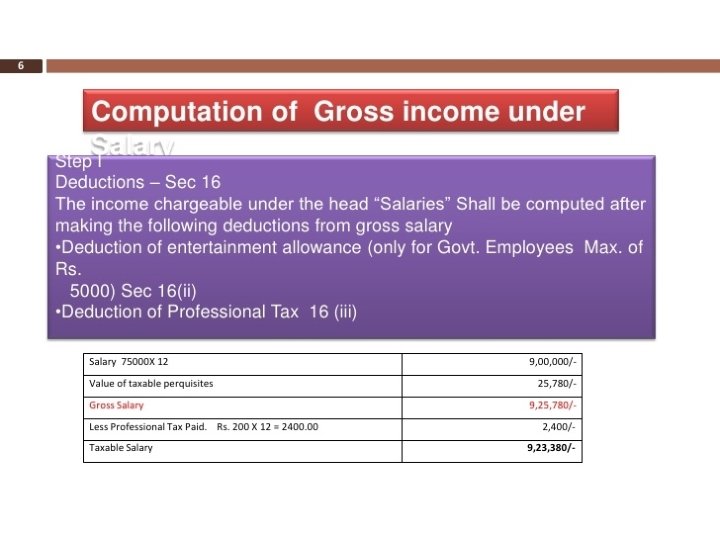

1. WHAT IS SALARY? Salary means fixed weekly or monthly remuneration. � CONTRACTUAL RELATIONSHIP – ER-EEE RELATIONSHIP INEVITABLE �

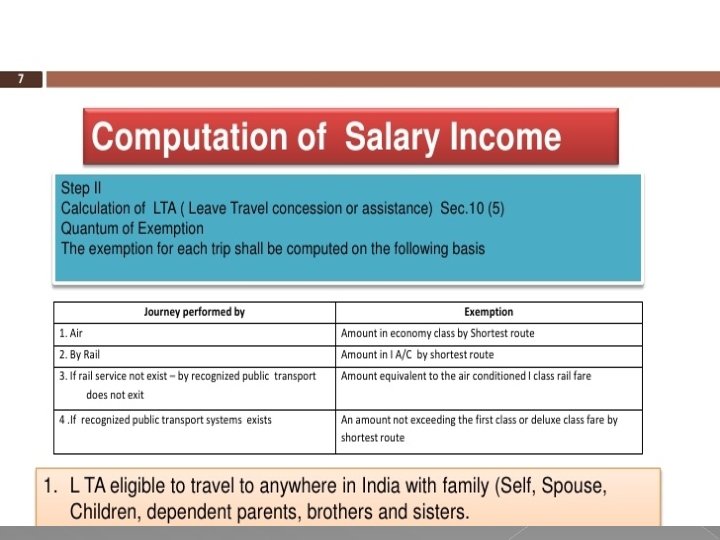

2. INCOME FROM HOUSE PROPERTY annual

• Interest on pre-construction period – Spread over 5 years after construction • Interest on HL- 2 lakh (self occupied)/ no limit for let out property

3. INCOME FROM PROFIT/ GAIN FROM BUSINESS/ PROFESSION

4. CAPITAL GAINS

5. INCOME FROM OTHER SOURCES

COMPUTATION OF TAXABLE INCOME

1

SECTION 89(1) RELIEF If total income includes any past dues paid in the current year, higher amount of tax may incur. To save from any additional burden of tax due to delay in receiving income, the tax laws allow a relief under section 89(1)

Steps in Calculating Sec 89(1) Relief � Step 1: Calculate tax payable on the total income, including additional salary –in the year it is received. � Step 2: Calculate tax payable on the total income, excluding additional salary–in the year it is received. � Step 3: Calculate difference between Step 1 and Step 2.

� Step 4: Calculate tax payable on the total income of the year to which the arrears relate, excluding arrears. � Step 5: Calculate tax payable on the total income of the year to which the arrears relate, including arrears. � Step 6: Calculate difference between Step 4 and Step 5. � Step 7: Excess of amount at Step 3 over Step 6 is the tax relief that shall be allowed.

CALCULATION OF ANNUAL VALUE � Calculate the Municipal & Fair Value of the property � Take the higher amount of Step 1 � Compare Step 2 with Standard Rent, lower will be Expected Rent � Compare Expected Rent with Actual Rent, higher will be GAV � GAV- Municipal Tax=NAV

In case taxpayer has borrowed capital for the purpose of acquiring, constructing , repairing, renewing or reconstructing any property, the amount of interest payable on such loan is allowed as a deduction. Interest on new loan taken to repay the original housing loan is also allowed as deduction.

COMPUTATION OF INCOME UNDER HOUSE PROPERTY TYPE OF HOUSE SELF OCCUPIED LET OUT PROPERTY DEEMED LET OUT Gross annual value Nil XXX Less: Municipal taxes Not applicable XXX Net Annual Value Nil (NAV) XXX Less: standard deduction 30% of NAV Less: interest on Restricted to 2 housing loan lakhs No limit Income from house property XXX Not applicable (XXX)

COMPUTATION OF SHORT TERM CAPITAL GAINS ON SALE OF PROPERTY FULL VALUE OF CONSIDERATION XXX Less: expenditure incurred wholly in connection with such transfer/ sale (XXX) Less: Cost of Acquisition (XXX) Less: Cost of Improvement (XXX) Gross Short Term Capital Gain XXX Less: Exemption (if any) available u/s 54 B/54 D/54 GA (XXX) Net Short Term Capital Gain on Sale of Property XXX TAX RATE – 15%

COMPUTATION OF LONG TERM CAPITAL GAIN FULL VALUE OF CONSIDERATION XXX Less: Expenditure incurred wholly & exclusively in connection with such transfer/sale (XXX) Less: Indexed Cost of Acquisition (XXX) Less: Indexed Cost of Improvement (XXX) Gross Long Term Capital Gain XXX Less: Exemption (if any) available u/s 54/54 B/54 D/54 EC/54 ED/54 F/54 G (XXX) Net Long Term Capital Gain on Sale of Property XXX TAX RATE – 20%

NOTIFIED COST INFLATION INDEX u/s 48 - FY 2018 -19

EXEMPTED CAPITAL GAINS

GROSS TOTAL INCOME = INCOME FROM SALARY + INCOME FROM HOUSE PROPERTY + PROFIT OR GAIN FROM BUSINESS OR PROFESSION + CAPITAL GAIN+ OTHER INCOME

LIMIT : 150000

Section 80 D - Deduction of Rs. 25, 000/30, 000 for medical insurance of self, spouse and dependent children and an additional Rs. 25, 000 for medical insurance of parents above 60 years � � Section 80 G- Donations 100/50% Section 80 CCF- up to Rs. 20, 000 for investment in infrastructure bonds � Section 80 E : Interest on higher education loan for self, spouse, or child. �

� 80 CCD New Pension Scheme (NPS) : � At investment stage , tax deduction is available through 3 sections 80 CCD(1), 80 CCD(1 b), 80 CCD(2). 80 CCD(1) – up to 1. 5 lakhs (this comes under the limit of max limit of 80 c) � � 80 CCD (1 b) – amount contributed in excess of 1. 5 lakhs. Max of 50, 000 � 80 CCD(2) _ Employers contribution to a maximum of 10% of BP+DA.

� Section 80 DDB- Medical treatment expenses for Specified diseases � Maximum deduction: Rs. 1, 000 for Senior citizen & Super Senior citizen � others Rs. 40, 000 or actual expenditure on medical treatment, whichever is less, of the dependant persons

Section 80 TTA-Interest on deposits in Savings Bank Account (up to Rs. 10, 000). � Section 80 GGC-Donation to political party. (Conditions: Registered political party, from the AY 2015 -16, no deduction shall be allowed in respect of any sum contributed by way of cash or kind) � The limit of cash transaction has been reduced from 10, 000 to 2, 000 by the finance act 2017 � Section 80 U- Deduction in respect of a personal disability. Rs. 75, 000/- for ordinary disability and Rs. 1, 25, 000/- for severe disability. ( to be certified by a medical authority as a person with disability) �

INCOME TAX RATES 1. In case of an Individual or HUF or Association of Person or Body of Individual or any other artificial juridical person � 0 - 2, 50, 000 - NIL * � 2, 50, 000 - 5, 000 - 5% � 5, 000 - 10, 000 -20% � ABOVE 10, 000 - 30% � *SENIOR CITIZEN - 3, 000 � *SUPER SENIOR CITIZEN - 5, 000

2. In case of a partnership firm (including LLP), local authority - taxable at 30% 3. In case of a domestic company - taxable at 30%. However, tax rate would be 25% where turnover or gross receipt of the company does not exceed Rs. 50 crore in the previous year 2015 -16. 4. In case of a Co-operative Society Up to Rs. 10, 000 -10% Rs. 10, 000 to Rs. 20, 000 -20% Above Rs. 20, 000 -30%

TAX LIABILITY � A tax liability is the amount of taxation that a business or an individual incurs based on current tax laws. Taxes are imposed by a variety of taxing authorities, including federal, state and local governments.

TAX LIABILITY FORMULA � NORMAL TAX + EDUCATION CESS ( @ 3%) � LESS : REBATE U/S 87 A* TDS */ TCS ADVANCE TAX ( IF ANY )

POINTS TO NOTE: � Rebate u/s 87 A The rebate is available to a resident individual if his total income does not exceed Rs. 3, 50, 000. The amount of rebate shall be 100% of income-tax or Rs. 2, 500, whichever is less.

Common TDS sections � S. 192 – Salary � S. 194 A – Interest other than interest on Securities � S. 194 C – Payment to Contractors � S. 194 I – Rent � S. 194 IA – TDS on sale of immovable property � S. 194 J – Fees for professional or technical service

Format of Computation

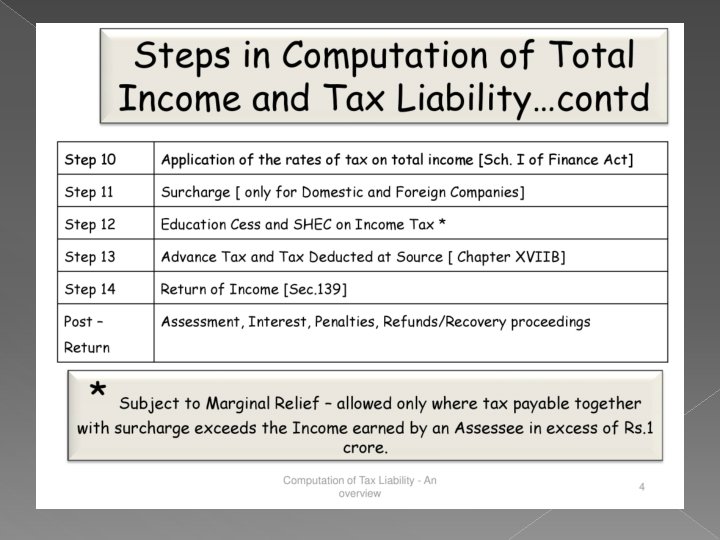

General steps for computing tax liability

Illustration of tax computation of a person having income of 5 lakhs

Fund Flow

THANK YOU!