ECONOMIC GROWTH Every country worries about economic growth

ECONOMIC GROWTH

• Every country worries about economic growth. • WHY? • Because economic growth can dramatically improve standard of living (the level of wealth, comfort, material goods…)

Some indicators of standard of living • Household income. • General health of a population. • Life expectancy of the members of a population. • Availability and quality of housing. • Level of crime. • Access to health care. • Access to education. Economic growth will bring a positive change in these indicators.

• When you travel around the world, you see tremendous variation in the standard of living across countries and this is due to the fact that economic growth differs from country to country. • In 2008, a photograph of a typical family in three different countries were taken together with all their material possessions.

United Kingdom • The United Kingdom is an advanced economy. In 2008, its GDP • person was $36, 130. A negligible share of the population • lives in extreme poverty, defined here as less than $2 a day.

Mexico • Mexico is a middleincome country. • In 2008, its GDP person was $14, 270. • About 5 percent of the population lives on less than $2 a day.

Mali • Mali is a poor country. In 2008, its GDP person was only • $1, 090. Extreme poverty is the norm: More than threequarters • of the population lives on less than $2 per day.

• The standard of living is different for each of these countries because economic growth is varies across countries.

• Even within a country, there are large changes in the standard of living over time. • The typical or average Ghanaian enjoys much greater economic prosperity than did his or her parents, grandparents, and greatgrandparents.

• Can the world’s poor be lifted from their poverty? • Answer: YES!! • Dramatic improvements in a nation’s standard of living are possible with economic growth. • South Korea is a standout example, but it is not the only case of rapid and sustained economic growth. Other nations of East Asia, like Thailand Indonesia, have seen very rapid growth as well. • China has grown enormously since market-oriented economic reforms were enacted around 1980.

• So this lecture seeks to explain these diverse experiences. • Why some countries are rich and others are poor? • Why some countries grow faster than others? • Why does the economy grow faster in some periods than in others? • In other words, what are the determinants of economic growth? • This will help poor countries know which policies to adopt in order to grow rapidly.

• But before we examine the determinants of economic growth, how do we define economic growth? • There are several definitions of economic growth.

Definition of economic growth • Economic growth relates to long-term changes in real GDP • The business cycle is a long term cycle.

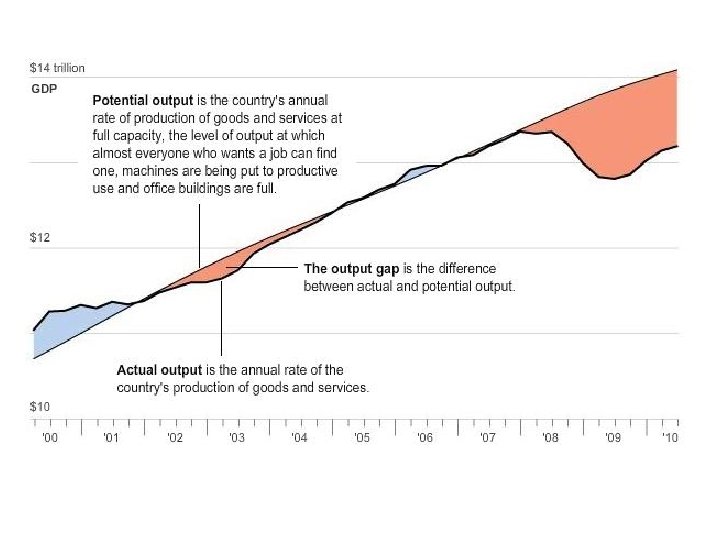

Definition of economic growth • Can be defined as expansion of the country's potential GDP or national output. • So what is potential GDP? • Actual GDP (Y ) refers to what the economy does produce, whilst Potential GDP (Yp) refers to what the economy could produce if all the resources in the economy are fully utilized. • So at potential GDP, we are on the PPF curve where all resources are being utilised.

• An increase in resources will increase potential GDP. In other words, it will shift the PPF curve outwards and hence an increase in economic growth. • Some factors that can increase potential GDP over time includes technical progress, accumulation of physical and human capital, etc. • This increase or expansion in potential GDP over time can termed as economic growth.

OUTPUT GAP • The difference between what the economy could have produced and what actually is produced is referred to as the Output (GDP) Gap. • Output gap = Yp - Y • If output gap is positive ie Yp > Y we have recessionary gap • If output gap is negative ie Yp < Y we have inflationary gap • If output gap is zero ie Yp = Y we have full employment. This occurs in the long run.

• As highlighted above, in the short run the actual GDP can be higher than its potential level, which implies an accumulation of inflationary pressures. • A positive output gap (when GDP is above the potential level) reveals the existence of inflationary pressures. • Conversely, a negative output gap shows deflationary pressures (downward pressures on prices).

Zero output gap • In the long run, the accumulated pressures are released, prices become flexible, and output gap always tends to zero, bringing GDP to its potential level (GDP trend).

Another definition of Economic growth • It is sustained expansion in the production of goods and services in an economy over time

Definition of Economic growth • Economic growth can also be seen as expansion of a country's production possibilities frontier.

Benefits or Importance of Economic growth. • Economic growth is very important for expanding living standards. • Sometimes people measuring economic growth with increases in the per capita GDP. • Per capita income/GDP is the total GDP divided by the total population • It is commonly used as a measure of the standard of living of a country • It is usually used to compare standard of living across countries.

Benefits or Importance of Economic growth. • Rapid economic growth allows countries to give more of everything to their citizens • better food and bigger homes • more resources for health care • universal education for children • better pensions for retirees • NOTE: A country’s standard of living depends on its ability to produce more goods and services.

Determinants of Economic growth • There are many different successful strategies to sustained economic growth • Britain became world economic leader in the 19 th century by pioneering the Industrial Revolution • Japan became world economic superpower by initially imitating foreign technologies. It then developed high level of expertise in manufacturing and electronics

• Although there are different individual paths to sustained economic growth, there are common fundamental factors the underlie all sustained economic expansions.

• RECALL: Economic growth can be defined as the sustained expansion in the aggregate production of goods and services in an economy over time. • So to proceed, we need to know the level of aggregate production in the economy. In other words, the level of GDP (Q).

• Economists sometimes use a production function to measure the level of aggregate production in the economy. • The production function describes the relationship between the quantity of inputs used in production and the quantity of output from production.

is produced using the following technological relationship: Q")

• Aggregate production/ GDP (Q) is produced using the following technological relationship: Q = AF(K, L, R, H) • where A is the level of technology in the economy • K is productive services of physical capital • L is labour units • R is raw material inputs/Natural resources • H is human capital • If GDP is produced with these inputs, growth rate of GDP will come from growth rate of these inputs

. •")

• The quantity of human resources refer to the labour supply (L). • Population growth is the only source of growth in aggregate labor supply that can be sustained over long periods. • An increase in labour supply can increase production, however many economists place less importance on the quantity of labour. • Many economists place more importance on labour productivity rather than just the quantity of labour supply. • Population growth brings economic growth, but it does not always bring growth in real GDP person unless labor becomes more productive.

Labour Productivity • Productivity is the quantity of goods and services produced from each unit of labor input. • Let’s divide the production function by L. • We have Q/L = AF(K/L, R/L, H/L) • Q/L is output per worker which is a measure of productivity. As workers become more productive, GDP or aggregate production increase which leads to economic growth.

• When labor productivity grows, real GDP person grows, real GDP grows and economic growth increases. • So the growth in labor productivity is the basis of economic growth and rising living standards. • So the determinants of productivity also becomes the determinants of Economic growth and it includes the folowing:

Physical Capital or physical capital per Worker • Capital includes • tangible capital goods like roads, power plants • equipment and machines like trucks and computers • intangible goods like computer software • Workers are more productive if they have tools with which to work. The stock of equipment and structures used to produce goods and services is called physical capital, or just capital.

• For example, when woodworkers make furniture, they use saws, lathes, and drill presses. More tools allow the woodworkers to produce their output more quickly and more accurately: • A worker with only basic hand tools can make less furniture each week than a worker with sophisticated and specialized woodworking equipment.

Human Capital or human capital per Worker • Human capital is the economist’s term for the knowledge and skills that workers acquire through education, training, and experience. • Education, training, and experience are less tangible than lathes, bulldozers, and buildings, but human capital is like physical capital in many ways. Like physical capital, human capital raises a nation’s ability to produce more goods and services.

• Indeed, students can be viewed as “workers” who have the important job of producing the human capital that will be used in future production.

Natural Resources or natural resources per Worker • Natural resources are inputs into production that are provided by nature, such as land, rivers, and mineral deposits. • Natural resources take two forms: renewable and non renewable. A forest is an example of a renewable resource. When one tree is cut down, a seedling can be planted in its place to be harvested in the future. Oil is an example of a non renewable resource. Because oil is produced by nature over many millions of years, there is only a limited supply. Once the supply of oil is depleted, it is impossible to create more.

• Differences in natural resources are responsible for some of the differences in economic growth around the world. The historical success of the United States was driven in part by the large supply of land well suited for agriculture. • Today, some countries in the Middle East, such as Kuwait and Saudi Arabia, are rich simply because they happen to be on top of some of the largest pools of oil in the world.

• Although natural resources can be important, they are not necessary for an economy to be highly productive in producing goods and services. • Japan, for instance, is one of the richest countries in the world, despite having few natural resources. International trade makes Japan’s success possible. Japan imports many of the natural resources it needs, such as oil, and exports its manufactured goods to economies rich in natural resources.

• Moreover, as the example of many African countries show, possession of abundant resources is neither necessary nor sufficient for economic success

Technology – a combination of innovation and invention • Technological change denotes changes in the processes of production or introduction of new products and services. • Technological Knowledge deals with understanding the best ways to produce goods and services.

• A hundred years ago, most Americans worked on farms because farm technology required a high input of labor to feed the entire population. • Today, thanks to advances in farming technology, a small fraction of the population can produce enough food to feed the entire country. This technological change made labor available to produce other goods and services.

• Technological change promotes growth by enhancing productivity.

Some costs of economic growth • When we use per capita income as the yardstick we ignore the effect of growth on income distribution • Not everyone benefits from growth equally because growth is normally distributed through increased wages and higher profits; • The poorest who are unemployed therefore do not share in the growth.

• When growth is driven mainly by technological change it leads to loss of jobs, and thus not everyone shares in the growth. • Thus we should note that in even in periods of high growth, the distribution may be unequal

• Some will face extreme poverty and hardships and so there will be need for redistribution policies to avert the hardships • Empirically the relationship between economic growth and income distribution is not clear • Redistribution policies are pro-poor policies to make growth share-growth. Here the increment in real GDP is redistributed through gov't. intervention.

• Inflation risk: If demand races ahead of aggregate supply the scene is set for rising prices – many of the faster-growing countries have seen a trend rise in inflation. • If AD increases faster than AS then economic growth will be unsustainable. Economic growth tends to cause inflation when the growth rate is above the long run trend rate of growth.

Environmental concerns: • Fast growth can create negative externalities e. g. noise pollution and lower air quality arising from air pollution and road congestion • The depletion of the resource base • Examples include the destruction of rain forests through deforestation, the over-exploitation of fish stocks and loss of natural habitat and biodiversity from the construction of new roads, hotels, malls and industrial estates.

• Has technology improved student’s productivity? What do you think?

- Slides: 48