Econ 433 Money and Banking Week 6 Lectures

Econ 433 Money and Banking Week 6 Lectures By Dr. E. Osei-Assibey Department of Economics University of Ghana 21 st September, 2011:

The Demand for Money • the Quantity Theory of Money and its Variants Money; • Fisher’s Quantity Theory of Money; The Cash Transaction Approach; • The Cambridge Equations: • Keynesian Theory of Money and Prices • Friedman’s Restatement of the Quantity Theory Vrs Keynes’

:")

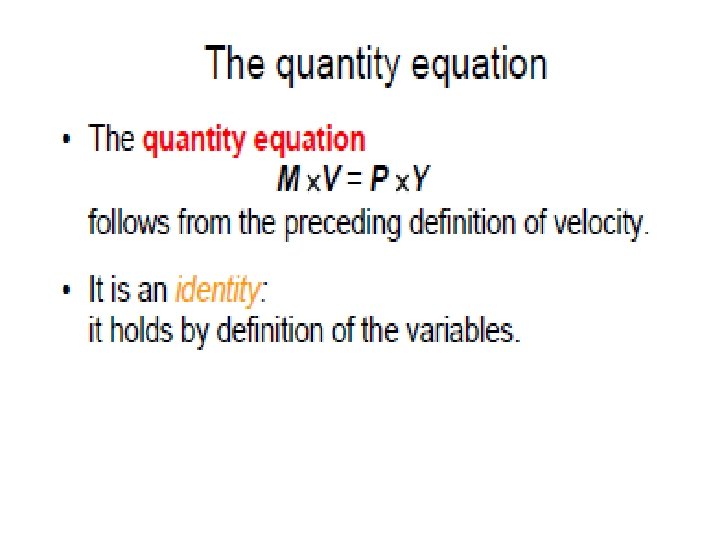

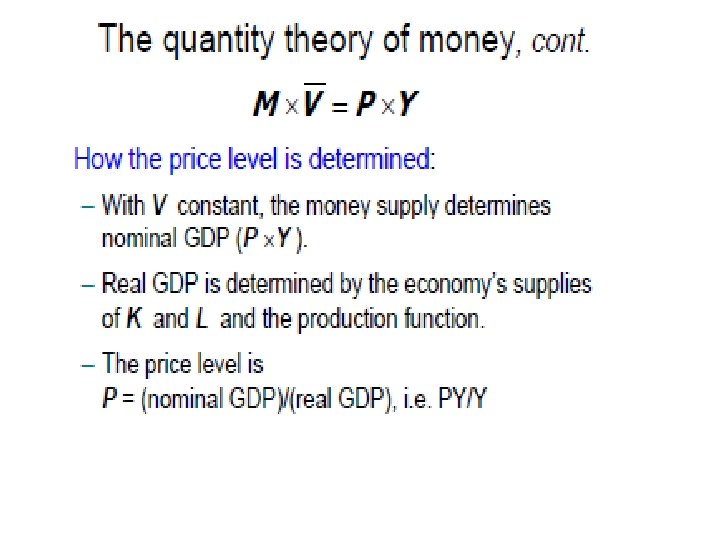

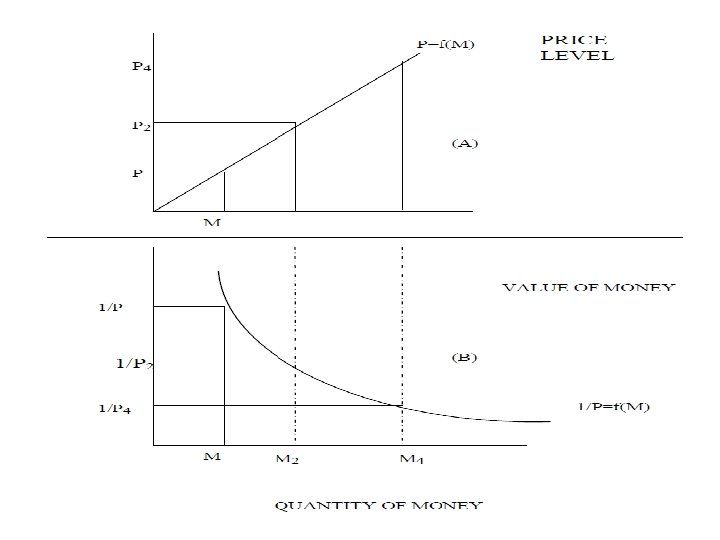

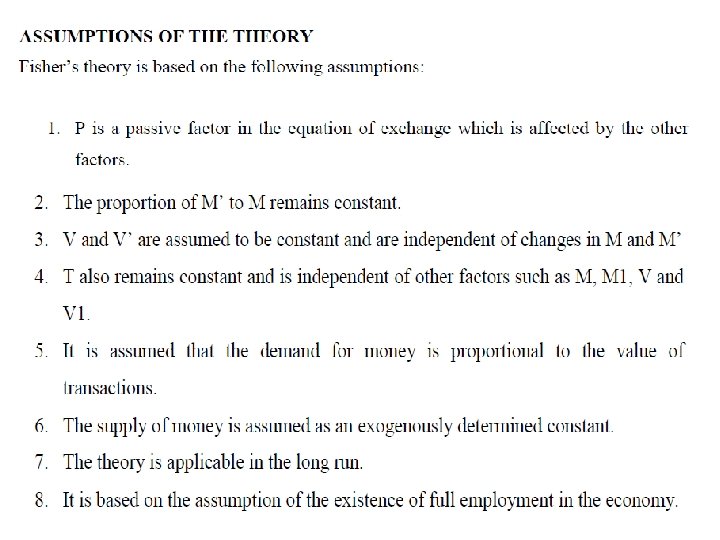

The Fisher’s Quantity Theory of Money (QTM • The Value of money (V) : • V= 1/P (P = prices) • The Cash Transaction Approach Definition of QTM: Ø It states that the quantity of money is the main determinant the price level or the value of money Irvin Fisher: “Other things remaining unchanged, as the quantity of money in circulation increases, the price level also increases in direct proportion and the value of money decreases and vice versa” Any Change in in the qty of money produces an exactly proportionate change in the price level

= supply of money (MV+M’V’) In")

The equation equates the demand for money (PT) = supply of money (MV+M’V’) In order to find the effect of the quantity of money on price level

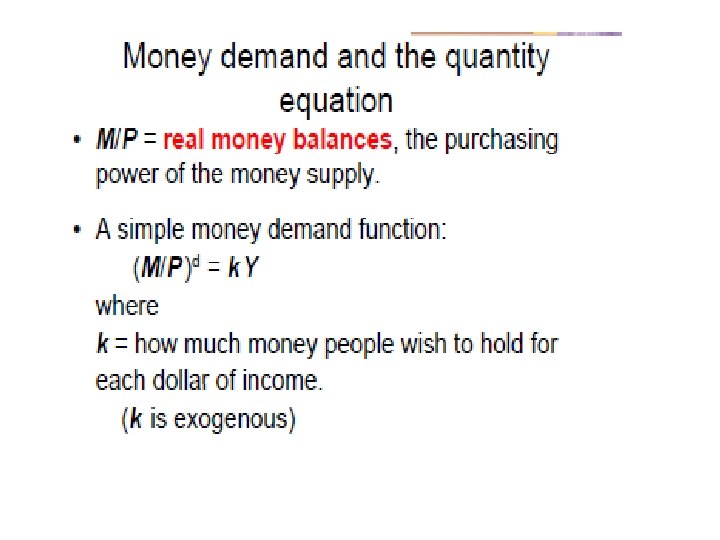

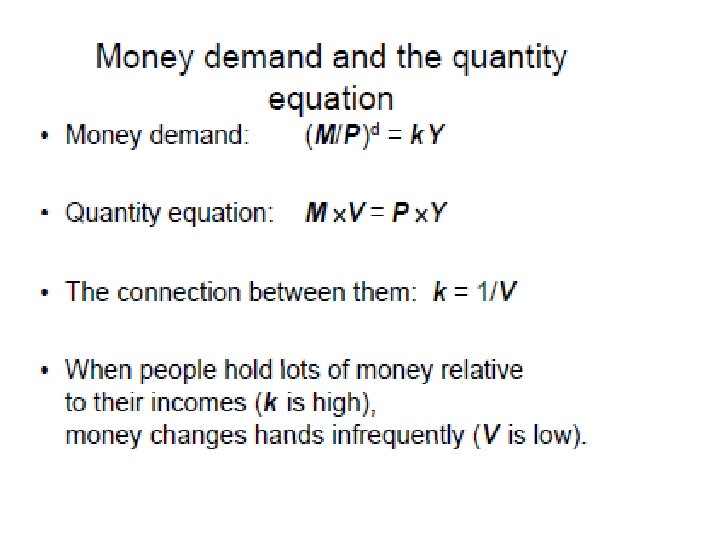

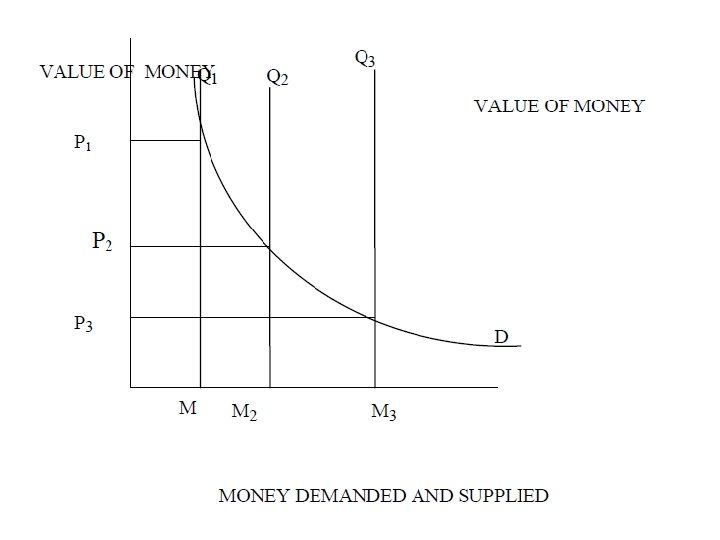

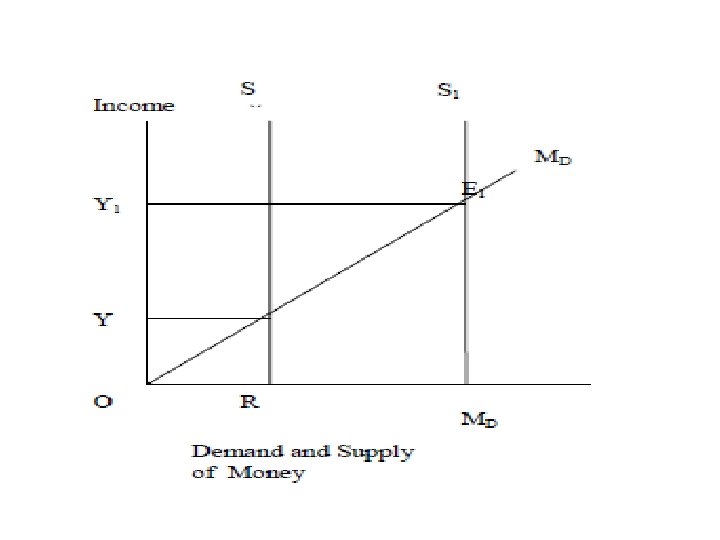

THE CAMBRIDGE EQUATIONS: THE CASH BALANCES APPROACH • Theory by Cambridge Economists: Marshal, Robertson, Pigou, and Keynes Theory: Ø The concept of supply of money is exogenously determined at a point in time by the banking system § The concept of velocity is altogether discarded in the cash balance approach because it obscures the motives and decisions behind it § The concept of demand for money plays a major role in determining the value of money § It considers demand for money not as a medium of exchange but as a store of value The value of money is determined by the demand for cash balances: When the Md increases, expenditure on goods and services reduces in order to increase their cash balance

M = exogenously determined supply of money, k = the fraction of the real money income (PY) which people wish to hold in cash and demand deposits P= the price level, and Y = the aggregate real income. Thus the price level or the value of money (the reciprocal of price level):

Criticisms • Truisms, like the transactions equation, the cash balances equations are truisms. Ø Take any Cambridge equation: Marshall’s p=M/ky or Pigou’s P=KR/M or Robertson’s P=M/KT or Keynes’s p=n/k, it establishes a proportionate relation between quantity of money and price level • K and Y not constant.

Question? ? ? ? • Discuss the Cambridge Cash Balance Approach to the Quantity theory of money. How far is it superior to the Cash Transactions Approach?

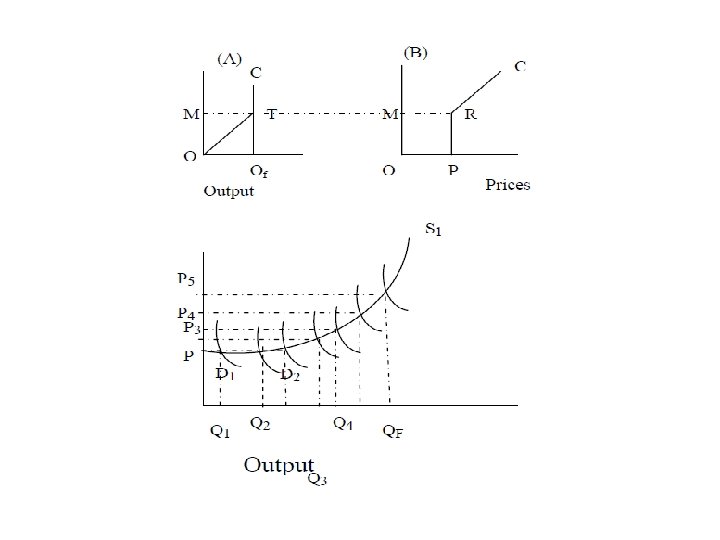

KEYNES’S REFORMULATED QUANTITY THEORY OF MONEY Modification: He Integrates Monetary theory with value theory and linked theory of interest into monetary theory Assumptions: • All factors of production are in perfectly elastic supply so long as there is any unemployment. • All unemployed factors are homogeneous • There are constant returns to scale so that prices do not rise or fall as output increases. • Effective demand quantity of money change in the same proportion so long as there any unemployed resources.

between")

Keynes QTM • Main points Ø The channel of influence (or the causation) between changes in qty of money and prices is an indirect one through inflation: Ø Transmission Mechanism (Unemployment) Ms r I AD Q Emp ( P = 0) Full Employment P (by the same % as the change in Ms ) ( Q = 0) Ms

FRIEDMAN’S RESTATEMENT OF THE QUANTITY THEORY OF MONEY • Friedman asserts that the QTM is in the first instance a theory of demand for money: • Real cash balances (M/P) is regarded as a commodity which is demanded because it yields services or returns to the person who holds it. • Demand for money (M/P) is a function of the following: Ø Total Wealth. The total wealth is the analogue of the budget constraint. It is the total that must be divided among various forms of assets. Ø The Division of Wealth between human and non-human forms. The major source of wealth is the productive capacity of human beings which is human wealth. Ø The Expected Rates of Return on money and other Assets. These rates of return are the counterparts of the prices of a commodity and its substitutes and complements in theory of consumer demand. Ø Other Variables other than income may affect the utility attached to the services of money which deter liquidity proper.

Composition of Wealth • W = All sources of income or consumables • Money is taken in the broadest sense to include currency, demand deposits and time deposits which yield interest on deposits. • Bonds are defined as claim to a time stream of payments that are fixed in normal units • equities are defined as a claim to a time stream of payments that are fixed in real units • physical goods or non-human goods are inventories of producer and consumer durable • Human capital is the productive capacity of human beings.

Friedman Eq • The present discounted value of these expected income flows from these five forms of wealth constitutes the current value of wealth which can be expressed as: • • W is the current value of total wealth. Y is the total flow of expected income from the five forms of wealth, and r is the interest rate.

Friedman QTM • demand function for money for an individual wealth holder with slightly different notations from his original study of 1956 as: • • M/P=f(y, w; Rm, Rb, Re, gp, u) M = the total stock of money demanded; P = the price level; y = the real income; w = the fraction of wealth in non-human form; Rm is the expected nominal rate of return on money; Rb is the expected rate of return on bonds, including expected changes in their prices. • Re = Expected rate of return on equities, including expected changes in their prices; • gp = (I/P) (dp/dt) is the expected rate of change of prices of goods and hence the expected nominal rate of return on physical assets; and • u stands for variables other than income that may affect the utility attached to the services of money. • •

The transaction demand 2)")

Liquidity Preference • Keynes suggested three motives holding money: 1) The transaction demand 2) Precautionary demand 3) The speculative demand

The transaction demand (MT • MT arises from the medium of exchange • It is divided into income and business motives. • The income motive is meant to bring the interval between the receipt of income and its disbursement. • The business motive is meant to bridge the interval between the time of incurring business cost and that is the receipt of the sale of proceeds • MT is direct proportion and positive function of the level of income

MT • LT = k. Y Transactions dd

• Transactions balances are held because")

MT and Interest Rates Keynes: Interest inelastic (r=0) • Transactions balances are held because income. Alternative View: W. Baumol (1952) J. Tobin (1956) MT and income is non-linear and not proportional • Interest rate is an important determinant § MT = f (y, r) § A portion MT can be invested in interest-bearing assets § Consider the cost and the inconvenience of purchase and sale of bonds to the interest expected to be earned

")

MT and interest rates LT = f(y, r)

Interest rate cont • So long as interest rate is below certain level, MT will be inelastic, but if it’s move above this level, it becomes sensitive to interest rate

• Mp is keeping cash against unforeseen contingencies and")

Precautionary Demand for Money (Mp) • Mp is keeping cash against unforeseen contingencies and unexpected needs • Keynes: Mp = f(y) • Post Keynesian: Mp = L(y, r)

• Money held speculative purposes is a liquid store")

Speculative Demand for Money (Ms) • Money held speculative purposes is a liquid store of value which can be invested at an opportune time in interest-bearing bonds or securities. • Bond prices and interest rate are invested related. B = V: the value (price)of bond, R is the fixed rate on bonds and r = r is the market interest Ø It’s the changes in V or r that determines Ms Ms = S(v, r)

. • If, r")

• Keynes has a normal or critical interest rate (rc). • If, r > rc , an investor holds all his liquid assets in bonds • If, r < rc an investor holds all his assets in cash • If, r = rc ? ? ?

Ms cont. When r > rc = LM, when r < rc = OW Ms = LMSW

Liquidity Trap When the market interest rate is so low that the yields on bonds will also be low making a change in quantity supply of money or monetary policy ineffective

Baumol’s Inventory Theoretic Approach • Baumol shows that MT is neither linear nor proportional. • Changes income lead to a less than proportionate MT • The theory is based on holding an optimum inventory of money for transaction purposes. • A firm would always try to keep minimum transaction balances in order to earn maximum interest from its assets • The higher the interest rate on bonds, the lesser transaction demand

Minimization of cost of transaction

Cost of Inputs Tariffs �� Duty drawbacks �� Trade facilitation �� Rules of origin �� Custom valuation • . INFRASTRUCTU RE SERVICES COSTS Regulatory systems �� Efficiency of services providers �� Market access to foreign services suppliers �� Competition policy BUSINESS ENVIRONMENT FDI openness �� Export / investment links �� Tariffs on capital goods �� Protection of property rights �� Good governance �� Labour market �� SPS/TBT compliance Conformity assessment �� Mutual recognition / equivalence agreements EXPORT COSTS Efficiency of port services �� Trade facilitation Market access - Agricultu re - Manufac tured goods - Services �� Export subsidies / domestic support in agricultu re �� Nontariff measure

- Slides: 41