Dr Muddassir Siddiqui President CEO Shariah Path Consultants

. Most transactions that are undertaken")

• The defendant")

- Slides: 16

Dr. Muddassir Siddiqui President & CEO Shariah Path Consultants Session II: Islamic Banking and Finance in Oman: Present Status and Future Trends Oman Second Islamic Banking & Finance Conference

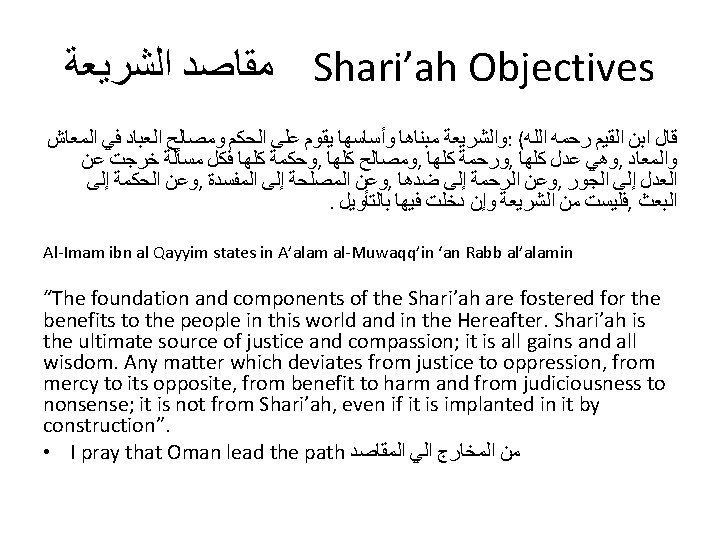

ﺑﺴﻢ ﺍﻟﻠﻪ ﺍﻟﺮﺣﻤﻦ ﺍﻟﺮﺣﻴﻢ The Royal Decree 69/2012 a road map to Islamic banking in Oman Muddassir Siddiqui President Shariah. Path Consultants, LLC, USA Oman Second Banking and Islamic finance conference Muscat, March 17 -18, 2013

Started late but came strong • • Comprehensive GCC Regulations CBO - a serious participant What strikes is the spirit of the law: A yearning to project a credible image by: – Enforcing Strict Shari’ah governance rules to: • avoid conflict of interest • Provide adequacy in the Shari'ah supervision – Restricting the use of certain products (Tawarruq) to: • Avoid Shari’ah compliance risks and credibility deficit • Central Shari’ah Board working with the CBO

Treat the cause -not just the symptoms - Tawarruq • Tawarruq is a symptom – the cause is the use of trade contracts to disguise the financing at LIBOR. • Can not lend at interest. Solution buy and sell at a markup. Use prevalent interest rates (LIBOR) for markup and call interest a “profit” • Remove all commercial risks from the trade contracts to make it acceptable to regulators. OCC rulings. Found Murabaha, Ijarah functionally equivalent to conventional loan (1995) • Use the substance of the engineered contracts for tax - deemed interest. • Pattern: All trade contracts, murabaha, Ijarah muntahia bi al-tamleek, Ijaraha mausufah fi al-zimmah, musharakah mutanaqasah, istisna’a wa istisna’a muwazi, mudarabah investment accounts, wakah istithmar, tawarruq, lead to financing benchmarked to prevalent interest rate. • Reverse engineered conventional contracts • Cause of many conflicts and tensions.

Credibility deficit • Qatar Financial Center Authority Report (2013). Most transactions that are undertaken in Islamic finance seek to achieve the economic outcomes which are similar to the economic outcomes achieved by conventional finance. However, to achieve these economic outcomes the Islamic finance transactions typically require more component steps than do the equivalent conventional finance transactions”. • Tax relief: “Any reference in this act to interest shall apply … to gains or profits received and expenses incurred, in lieu of interest in transactions conducted in accordance with the principles of syariah”. Income Tax Act 1967, Malaysia • The main tool of IF today is organized tawarruq. Yet, it is condemned by the Islamic Fiqh Academy of OIC and Rabita as ﺍﻟﺮﺑﺎ ﻋﻠﻲ ﺍﻟﺘﺤﺎﻳﻞ

disguised loan at interest • Shamil Case – English Court (2004) • The defendant defaulted and alleged “the agreements were unlawful, invalid and unenforceable under the principles of the Sharia in that, despite their form as Morabaha Agreements … (which would be enforceable if they were a true reflection of the underlying transaction) the transactions were in truth disguised loans at interest. As such amounted to unlawful agreements to pay Riba and were thus void and/or unenforceable“. • TID v. Blom – English Court (2009) • ”The defendant defaulted and alleged the wakala agreement was repugnant to the Shari’ah. The court observed “The results of those rather complicated and sophisticated provisions was that any deposit would be at the specified rate of return, let us say for argument's sake 5 per cent. It could not be less than 5 per cent. It could not be more than 5 per cent“. ”One finds, a device to enable what would at least to some eyes appear to be the payment of interest under another guise, that is at least an indirect practice of a non-Sharia compliant activity“

Encourages Forum Shopping • Saudi Board of Grievances - Decision no 21/d/tj/1429 • The outcome can be very different • Purchase and sale of precious metals agreement between and bank and its customer. • “In considering the nature of the relation between the Plaintiff and the Defendant, the Second Circuit found that the Plaintiff considers the agreement with the Defendant to be a "Commercial Agency for Trading, " while the Defendant considers it a "Loan and Credit Facilities" type of relation. However, the Circuit is concerned about the substance, not the title, even if the substance that it finds does not match either of the titles suggested by the parties”. • The Board found it to be a commercial dispute.

Leads to Re-characterization • The Court of First Instance – Dubai • Is the lease to own contract a lease contract or instalment sale and purchase contract. • “The court concludes from the foregoing, the Defendant's application for financing the purchase of the property and not renting it, the issue of the approval to such application, making the lease contract, the undertakings of sale and purchase … and the intention of the parties from that the proper characterization of the contractual relation between them is that it is a sale contract. • The court disregarded the titles and ruled on substance

Sustainability? • Transactional costs • Liabilities exposure to both IFIs and customers • Conflict with other laws; bankruptcy; Consumer protection. • Early payment discount • IFI protection. Contractor abandons, IFI liable • Mismatch between the contract and commercial intention of the IFI and customer • What is the solution

Royal Decree 69/2012 • For the reason listed above CBs are hesitant to allow IF and Banking • When allowed, the CBs only allow the use of modern IF contracts. The permission is not an unrestricted license to engage in full mudarabah and musharakah and other trading activities. • Article 124. Without prejudice to the restrictions set by the Board of Governors, the banks licensed to practice Islamic banking shall in the context of such practice, conduct all transactions … • A) accepting deposits … • b) financing and investing in Mudaraba , Musharaka , Murabaha , ljara , Salam, Istisna or Qard Hassan and other Shariaᾴ formulas. • c) … • What is the long term solution?

The Alternative • The main issues which need to be decided are: – The status of fixed return with capital guarantee under the Shari’ah. Is it always prohibited? – If not, identify the difference between a halal and Haram FRCG – Look into the rules of various forms of Islamic finances – Compare when FRCG is allowed and when it is prohibited – Example: Compare Credit sale with markup (CSM) with mudarabah • Ask why fixed return with capital guarantee in Credit Sale with Markup is halal but forbidden in mudarabah?

Extract the Reason ﺍﻟﻌﻠﺔ ﺍﺳﺘﻨﺒﺎﻁ • Extract THE GOLDEN RULES. • It appears ﺍﻋﻠﻢ ﺍﻟﻠﻪ ﻭ – THE SHARI’AH RULES PROHIBIT A FINANCIER FROM CHARGING A FIXED RETURN WITH CAPITAL GUARANTEE, WHEN THE RECEIVER OF THE FINANCE IS ASKED TO PAY A CONSIDERATION FOR AN SPECULATED BENEFIT WHICH MAY AND MAY NOT OCCUR. – THE SHARI’AH RULES PERMIT A FINANCIER TO CHARGE A FIXED RETURN WITH CAPITAL GUARANTEE WHEN THE USUFRUST ((������� ACCRUING TO THE RECEIVER OF THE FINANCING IS CERTAIN AND MEASUREABLE. • THE CONSIDERATION OF THE USUFRUCT MUST BE MEASURED BY THE VALUE OF THE USUFRUCT AND NOT BY THE TIME VALUE OF MONEY • In trade contracts, the prohibition is based on ��� and not on riba. • Consideration for the usufruct is permitted in Shari’ah (rent) • Consideration for time value of money is not permitted in Shari’ah • How to apply these principles in Islamic banking

How to apply these rules • Have two separate contracts. No need for dressing up. – A loan contract between the IFI with markup for the USUFRUCT and not based on LIBOR – A sale contract between the true owner and IFI customer for the sale, lease etc. of the asset which is the source of the ﻣﻨﻔﻌﺔ – Tie both contracts together. Financing to be an integral part of sale. • Accept that the fixed return with capital guarantee is permissible when the financing confers on the borrower a certain and measureable benefit • Be clear about the principles, transparent in its application and consistent with its implication • Do away with fictitious contracts and fictitious structures

The result Clarity of the Shari’ah principles Clarity in their applications Harmony between form and substance Harmony between rhetoric and actions Less step contracts, Less costs, Less risks to both the IFIs and their customers • Easy to adjudicate and enforce contracts • A dynamic Shari’ah Board at the CBO is must to work together with the CBO • Understand the facts ﺍﻟﻮﺍﻗﻊ and apply the rule which suits it. ﺗﺼﻮﺭﻩ ﻣﻦ ﻓﺮﻉ ﺷﻴﺊ ﻋﻠﻲ ﺍﻟﺤﻜﻢ • • •

Thank you Shaikh Muddassir Siddiqui President/CEO Shariah. Path Consultants, LLC muddassir. siddiqui@shariahpath. com • Shaikh Muddassir Siddiqui is uniquely qualified both as a Shari’ah scholar and as a U. S. trained attorney. In 2010 Thomson Reuters wrote: “Shaikh Muddassir Siddiqui is "one of the industry’s most articulate practitioners, and one whose experience as both a lawyer and Shariah scholar puts him in rare company”. In 2011, Islamic Finance News poll recognized Shaikh Muddassir as one of the Leading Lawyers in Islamic Finance. Shaikh Muddassir is a member of the AAOIFI Shari'ah Standards Committee; the Fiqh Council of North America and a Research Fellow at the International Shari’ah Research Academy for Islamic Finance, in Malaysia. Shaikh Muddassir is a member of New York Bar and Registered Foreign Lawyer with the Solicitors Regulation Authority (SRA), in the U. K. He has extensive experience in advising on transactions involving Shari’ah-compliant financing.