Dividend Policy at FPL Group Synopsis n n

generally don’t care")

- Slides: 20

Dividend Policy at FPL Group

Synopsis n n n A Wall Street analyst has just learned that FPL Group (the holding company for Florida Power and Light, the country’s fourth largest electric utility) may decide to freeze its dividend at $2. 48 per share or possibly cut the dividend at the company’s upcoming annual meeting. The decision not to increase the dividend will end a 47 -year streak of annual dividend increases—the longest streak among utilities and the third longest streak among publicly traded U. S. companies. In response to the news, FPL’s stock price is down 6%. The protagonist, Kate Stark, must decide whether to revise her investment recommendation on FPL in light of this new information.

Background behind FPL’s decision in dividend? n n n In 1992, federal regulators introduced wholesale wheeling and, by mid-1994, state regulators in 23 states are considering retail wheeling proposals. When the California regulators released their retail wheeling proposal, the three largest utilities in the state lost a combined $1. 8 billion in market value. S&P Electric Utilities Index has declined more than 20% since September 1993. While much of this can be attributed to the increase in interest rates, some portion of the decline is due to the effects of deregulation.

If you are FPL CEO, what will you do? n Take a vote! q q q n Increase dividend Remain the same! ($2. 48) Cut dividend What are your reasons behind your votes?

Why FPL want to increase dividend? n n n Meet market expectation. Signal good earnings perspective. Free cash flow hypothesis.

Why FPL want to decrease dividend? n n n To signal worsening industry prospect. (not much so for FPL) Increased competition leads to increased volatility in earnings, makes a high payout ratio unlikely to maintain. Other concerns than signaling. Taxes, transaction cost, or agency conflicts.

FPL’s competitive advantages n n n FPL’s service territory, eastern and southern Florida, country’s fastest growing markets: FPL expects annual growth of 2. 7% (the U. S. average of 1. 8%). FPL’s customer mix is also a competitive advantage since industrial sales represent only 4% of total sales compared to an average of 21% for the others. According to the retail wheeling proposals, having a low percentage of industrial customers limits FPL’s risk to the threat of competition. S&P ranked FPL’s competitive position among the top 10% of investor-owned utilities.

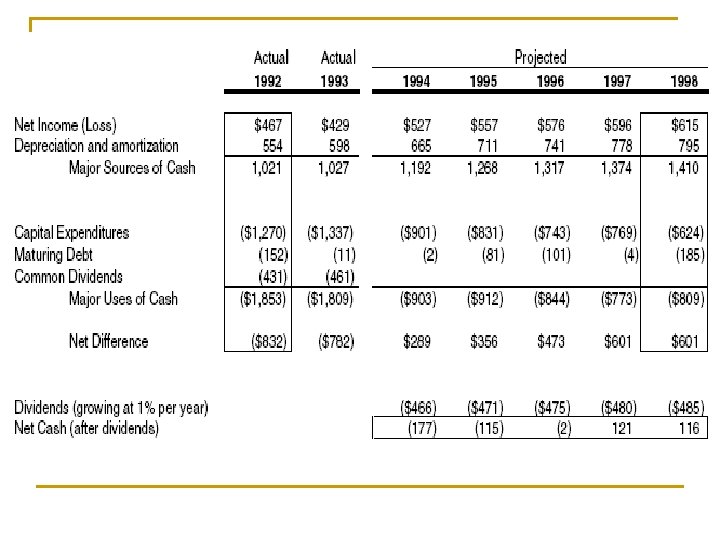

FPL’s financial strength n n n FPL’s cash flow is improving due to increasing net income and declining capital expenditures. FPL will have $601 million in cash before common dividends in 1998 compared to negative $832 million in cash flow after dividends in 1992. By slowing dividend growth to 1% per year, FPL can fund its dividend internally by 1996 and reduce its payout ratio to below 80% by 1998. This strong future cash flow makes it unlikely that FPL will cut its dividend. Indeed, according to the analyst, FPL views earnings growth as a possible solution to the high payout ratio problem.

FPL’s competitive disadvantages? n n FPL is a high cost utility in a commodity business. FPL’s generating and transmission costs are significantly higher than most of its competitors. Because the competitors currently have excess generating capacity (see the load factor and capacity margins) and sufficient transmission capacity for the next several years, they pose a serious threat to FPL’s future profitability.

Does signaling play a role in FPL’s dividend policy? n n What FPL tries to signal? Better? Or worse? Improved competitive edge and financial strength increase dividend. Worsening industry profitability cut dividend. The major problem with cutting the dividend is the likelihood of severe market reaction. Both Consolidated Edison and Sierra Pacific experienced significant share price declines in the wake of dividend cuts.

Taxes and dividends for FPL n n Non-tax paying institutions (30%) generally don’t care whichever capital gains or dividends. For individuals (52%), between 1986 and 1993, they were taxed at same rates. More recently, tax codes favor capital gains: the tax rate on long-term capital gains peaks at 28% while the rate on dividend income can go as high as 39% for high income individuals. Corporations, which own approximately 5% of shares, can exclude a substantial portion of dividend income from taxes. If they own less than 20% of a company’s stock, they can exclude 70% of dividend income; if they own from 20% to 80% of the stock, they can exclude 80%; and if they own more than 80%, they can exclude 100%. The fact that FPL has a relatively high dividend yield would seem to indicate that the tax disadvantage of dividends does not concern its investors.

Transactions Costs n n One can see that operating cash flows were approximately equal to investing cash flows; long term debt issuance was approximately equal to debt retirement; and stock issuance was approximately equal to the payment of common dividends. To pay the dividends, FPL issued 55 million shares of common stock worth $1. 9 billion. The investment banking fees for the issuances, estimated at 3% of the total amount issued, would equal $60 million. As a general rule, a firm should not issue equity to pay dividends because it results in a deadweight loss for investors.

Agency costs n n n Managers own only 0. 1% of stock. Firm is to ratify a new executive compensation plan, which will emphasize net income and reduce the extent to which bonuses are paid in stock. agency conflict If Broadhead were to pursue new ways to increase net income, he might well reduce the dividend. FPL could simply invest the $150 million of savings from cutting the dividend at 5% to yield $7. 5 million per year. This extra income would increase net income by 1%—significant in an industry that is growing at only 2% per year.

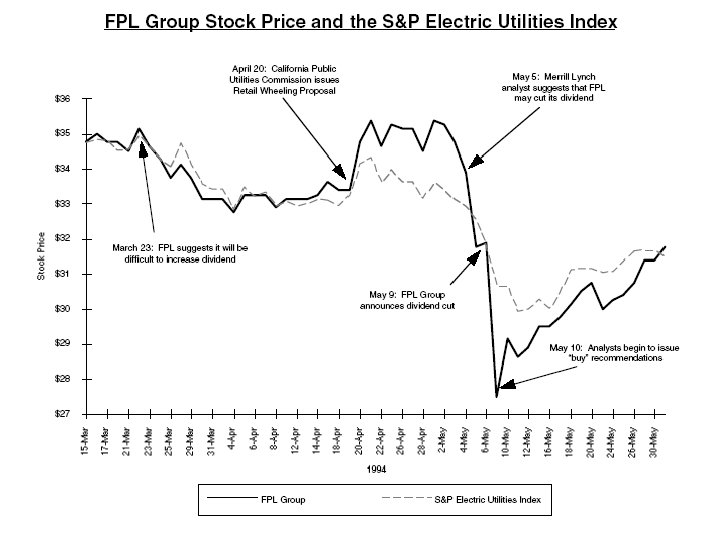

What Will Broadhead Do? n May 9: FPL announces new financial strategy q q q n n 32% reduction in quarterly dividend Dividend payout targeted at 60 -65% Repurchase 10 million shares over 3 years Reduce debt levels Move annual dividend announcement to February Broadhead’s explanation for the cut that the firm needs more financial flexibility to deal with future competition. For electric utilities industry which generate large amounts of free cash flow, financial slack may not be such a good thing. Stock price falls $4. 375 to $27. 50 [down 13. 7%], Stock price is down 22. 3% since April 29

Does a cut in dividend meet with capital market’s expectation? n n n FPL’s competitive position and future cash flow seems to indicate that FPL may increase its dividend or, at a minimum, hold the dividend where it is. FPL’s shareholders clientele seems to be satisfied with current payout dollar and ratio. Investors view the dividend cut as a bad signal regarding future profitability because profitable firms rarely cut their dividends.

What should Stark recommend to her clients regarding FPL’s stock— buy, sell, or hold

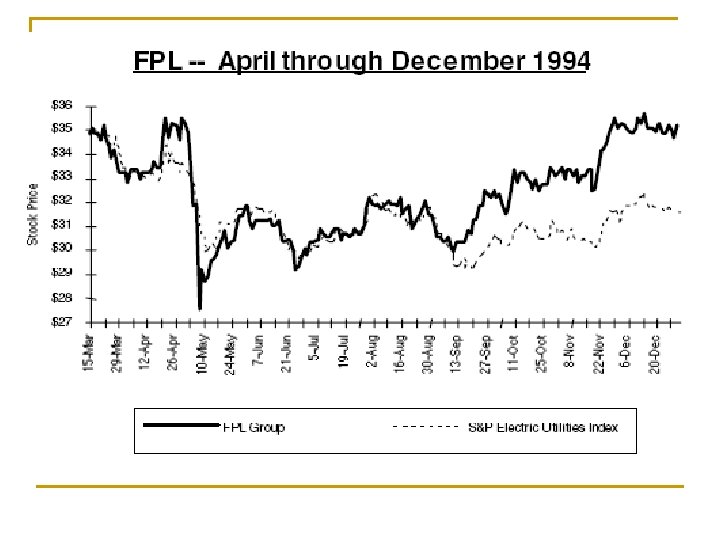

The aftermath n n FPL cut dividend, and it’s stock price dropped 14% in one day The recovery of the stock price begins immediately after the initial decline as analysts began to issue “buy” recommendations. FPL buy back shares after the cut in dividend. The buyback in turns reduce shares, and increase EPS, which is good for shareholders. Investors had lost $0. 80 per share in dividends. The FPL’s buyback program has posted EPS growth of 5. 6% over the year ($2. 91 in 1994 versus $2. 75 in 1993).