Dividend Decision And Stock RepurchaseDividend and Split Dividend

2. Decide whether or not a dividend will be paid. • Firm")

How much in dividends should be paid if the company has Rs 1.")

How much in dividends should be paid if the company has Rs 2")

How much in dividends should be paid if the company has Rs 3")

1. Each quarter’s dividend can be fixed fraction of that quarter’s")

• Another method used to pay out a firm’s earnings")

Assuming no signaling effect, at what share price should the company offer to")

In total, how much will the company be distributing through share repurchase ?")

What is the total amount used from retained earnings to repurchase the stocks")

If the company were to pay out funds through cash dividends instead, what")

What will happen to this account and to the number of shares outstanding")

20 % Stock Dividend • Number of shares outstanding before stock dividend= Rs")

Additional paid-in capital Retained")

a 2 for 1 stock split ? • Par value after split =")

a 1 for 2 reverse stock split ? • Par value after split")

In the absence of an informational or signaling effect, at what share price")

What would have happened if there were signaling effect ? • If there")

Additional paid-in capital Retained earnings Total shareholders’ equity")

- Slides: 56

Dividend Decision And Stock Repurchase/Dividend and Split

Dividend Policy • Determines the distribution of firm’s earnings between retention and dividend payment (Cash). • Other Options: – Stock Dividend – Stock Split – Stock Repurchase

Company’s Earnings Retained for further investment Distributed to Shareholders Cash Dividend Stock Repurchase Stock Split Retained Earnings

Factors Affecting Dividend Decisions • • Legal Rules Liquidity Positions Rate of Asset Expansion Profit Rate Stability of Earnings Control Need to Repay Debt Restrictive Covenants

Cash Dividends and Dividend Payment • • Dividend: A payment made out of a firm’s earnings to its owners, in the form of either cash or stock. If a payment is made from other sources than current or accumulated retained earnings, the term distribution is used. Distribution from earnings is dividend while distribution from capital as a liquidating dividend. Basic types of cash dividends: a) Regular Cash Dividends – paid regularly as a part of policy. b) Extra Dividends- extra part may or may not be repeated in future. c) Special Dividends- truly unusual or one-time event d) Liquidating Dividends- some or all of business has been luqidated

Standard Method of Cash Dividend Payment 1. Declaration Date: The Bo. D declares dividend 2. Ex-Dividend Date: The holder of the share certificate is entitled to dividend before this date. On or after this date, even if you buy the share, then the previous owner will get the dividend. Its two business days before the date of record. 3. Record Date: The declared dividends are distributable to those people who are shareholders of record as of this specific date. 4. Payment date: The dividends are paid to shareholders.

More on Ex-Dividend Date • Before, ex-dividend date, the stock is said to trade “with dividend” and afterwards the stock trades “ex dividend” • The ex-dividend date convention removes any ambiguity about who is entitled to the dividend. • The stock price will be affected when the stock goes “ex”. Illustration: • A share is selling for $ 10 • Bo. D declares $ 1 dividend per share, and record date is Tuesday, June 12 (Sunday being off-day in market) • Ex-Date – Friday (June 8) • You buy stock on last hour of Thursday (June 7). You’ll get $ 1 dividend. • You buy stock as the market opens on Friday (June 8). You wont get $ 1 dividend. • What happens to the value of stock overnight ?

Price Behavior around Ex-Date • Stock is worth about $ 1 less on Friday morning, so its price will drop by that amount. • In general, we expect that the value of the share of stock will go down by about the dividend amount when the stock goes ex dividend. (Remember – ABOUT)

Establishing Dividend Policy • How do firms actually determine the level of dividends they will pay at a particular time ? 1. Residual Dividend Approach 2. Dividend Stability 3. A Compromise Dividend Policy

Residual Dividend Approach • A policy under which a firm pays dividends only after meeting its investment needs while maintaining a desired debt-equity ratio. • Firm generally doesn’t wish to sell new equity to pay out dividend (expensive). (Firm wishes to minimize the need to sell new equity) • Then it will have to rely on internally generated equity to finance new positive NPV projects. • With a residual dividend policy, the firm’s objective is to meet its investment needs and maintain its desired debt-equity ratio before paying dividends.

Illustration: • Imagine that a firm has $ 1, 000 in earnings and debt equity ratio of 1: 2. Steps in implementing residual dividend policy: 1. Determine the amount of funds that can be generated without selling new equity. – If the firm reinvests the entire $ 1, 000 and pays no dividend, then equity will increase by $ 1, 000. – But debt equity ratio should be maintained. – So firm has to borrow additional amount of $ 500 – Total amount of funds that can be generated without selling new equity is thus $ 1, 000 + $ 500 = $ 1, 500

Illustration (contd…) 2. Decide whether or not a dividend will be paid. • Firm must generate this $ 900 ($ 1, 000 is already there, but the firm has to maintain the current capital structure) Firm will borrow 1/3 x $ 900 = $ 300 Rest $ 600 will be taken from available equity of $ 1, 000 Residual fund available for dividend payment = $ 1, 000 - $ 600 = $ 400 • • • – To do that, compare the total amount that can be generated without selling new equity ( $ 1, 500) to the planned capital spending. – If funds needed exceed funds available, then, no dividends will be paid. – In such case, dividends can only be paid by cutting out on some capital spending or by selling new equity. – If funds needed are less than funds generated, then a dividend will be paid, and the amount of dividend will be residual. – Suppose the firm has $ 900 in planned capital spending. – What will be residual fund available for dividend payment ?

Sum up of the illustration • • Firm has after-tax earnings of $ 1, 000. Dividends paid are $ 400 Retained Earnings are $ 600 The firm’s debt equity ratio of 1: 2 is unchanged. The relationship between investment and dividend payout for various levels of investments :

The relationship S. No Aftertax Earnings New Investment Additional Debt Retained Earnings Additional Stock Dividend 1 $ 1, 000 $ 3, 000 ? ? 2 1, 000 2, 000 ? ? 3 1, 000 1, 500 ? ? 4 1, 000 ? ? 5 1, 000 500 ? ? 6 1, 000 0 ? ?

The relationship S. No Aftertax Earnings New Investment Additional Debt Retained Earnings Additional Stock Dividend 1 $ 1, 000 $ 3, 000 $ 1, 000 $0 2 1, 000 2, 000 667 1, 000 333 0 3 1, 000 1, 500 1, 000 0 0 4 1, 000 333 667 0 333 5 1, 000 500 167 333 0 667 6 1, 000 0 0 1, 000

The Relationship A firm with many investment opportunities will pay small amounts of dividends and a firm with few investment opportunities will pay relatively larger amounts of dividends. Younger, fast-growing firms commonly employ a low payout ratio, whereas older, slower-growing firms in more mature industries use a higher payout ratio.

Formula under Residual Dividend Policy Dividend = Net Income – [Capital Budget x Target equity ratio] Where, target equity ratio is the proportion of equity in the capital structure. If the answer comes in negative, it means that the firm has to raise that much amount from new equity sale (external equity financing)

Example • Malkor Instruments Company treats dividends as a residual decision. It expects to generate Rs 2 million in net earnings after taxes in the coming year. The company has an all-equity capital structure and its cost of equity capital is 15%. The Company treats this cost as the opportunity cost of retained earnings. Because of floatation costs and under-pricing, the cost of common stock financing is higher. It is 16%.

(a) How much in dividends should be paid if the company has Rs 1. 5 million in projects whose expected return exceeds 15%? • Dividend = Net Income – [Capital Budget x Target equity ratio] = Rs 2, 000, 00 – [1, 500, 000 x 1] = Rs 500, 000 Company can pay Rs 500, 000 in dividends

(b) How much in dividends should be paid if the company has Rs 2 million in projects whose expected return exceeds 15%? • Dividend = Net Income – [Capital Budget x Target equity ratio] = Rs 2, 000, 00 – [2, 000 x 1] = Rs 0 Company can pay no dividend.

(c) How much in dividends should be paid if the company has Rs 3 million in projects whose expected return exceeds 16%? What else should be done • Dividend = Net Income – [Capital Budget x Target equity ratio] = Rs 2, 000, 00 – [3, 000 x 1] = - Rs 1, 000 Company can pay no dividend. Company should raise Rs 1000, 000 fund from external equity to finance the project

Dividend Stability • Strict residual dividend policy might lead to a very unstable dividend policy. • If investment opportunities in one period are quite high, dividends will be low or zero. • Conversely, dividends might be high in the next period of investment opportunities are considered less promising. • Consider a firm with seasonal sales pattern. • Its annual earnings are forecasted to be equal year to year. • But quarterly earnings vary greatly throughout the year. • 1 st quarter- low, raises in 2 nd and 3 rd, and then 4 th highest • The firm can choose between at least two types of dividend policies.

Dividend Stability (contd…) 1. Each quarter’s dividend can be fixed fraction of that quarter’s earnings. • Here, dividends will vary throughout the year. • This is cyclical dividend policy, where dividends are constant proportion of earnings at each pay date. 2. Each quarter’s dividend can be a fixed fraction of yearly earnings. • Here, all dividend payments will be equal. • This is stable dividend policy, where dividends are a constant proportion of earnings over an earnings cycle. Stable policy seems to be in the best interest of the firm and its stockholders, and stable policy would be more common.

A Compromise Dividend Policy 1. 2. 3. 4. 5. • • This policy is based on five main goals: (in the order of importance) Avoid cutting back on positive NPV projects to pay a dividend Avoid dividend cuts Avoid the need to sell equity Maintain a target debt-equity ratio Maintain a target dividend payout ratio. Debt-Equity ratio is viewed as long-range goal, it is allowed to vary in short run if necessary to avoid a dividend cut or the need to sell the new equity. One can minimize the problems of dividend instability by creating two types of dividends : regular and extra.

Share Repurchase • When the firm has funds in excess of present and foreseeable future investment needs. • It may distribute these funds either by cash dividends or by the repurchase of the sock.

Stock Dividends • Company distributes shares as dividends to the shareholders • Either from past retained earnings or from net profit earned in the respective year. • A company distributes stock dividend to raise capital, to save tax to the stockholders etc.

Stock Split • Company brakes shares through splitting the par value of the share. • A split takes place in two ways: 1. Straight split • Company increases he number of shares outstanding through reducing the par value 2. Reverse split • • Company reduces the number of shares outstanding through merging the par value. This takes place to increase the value of stock.

Stock Dividend Par Value per Share Market Price per Share Number of Shares Common Stock Additional Paid-in Capital Retained Earnings EPS DPS (If not constant dividend policy) Straight Stock Split Reverse Stock Split Stock Repurchase

Stock Repurchase (Share Buybacks) • Another method used to pay out a firm’s earnings to its owners, which provides more preferable tax treatment than dividends. Illustration: • Imagine all-equity firm with excess cash of $ 300, 000. • The firm pays no dividends, and its net income for the year just ended is $ 49, 000. • The market value balance sheet at the end of the year is: Market Value Balance Sheet (before paying out excess cash) Excess cash $ 300, 000 Debt $0 Other assets 700, 000 Equity 1, 000, 000 Total $ 1, 000

Contd…. • There are 100, 000 shares outstanding • Price per share = $ 10 • EPS = $ 49, 000/100, 000 = $ 0. 49 • P/E Ratio = $ 10 / 0. 49 = 20. 4 • The firm is considering two options: Option 1: $ 300, 000/100, 000 = $3 per share extra dividend Market Value Balance Sheet (After paying out excess cash) Excess Cash $0 Debt $0 Other assets 700, 000 Equity 700, 000 Total $ 700, 000

Contd…. • There are still 100, 000 shares outstanding. Hence each share is worth = $ 700, 000/100, 000 = $ 7 • Value per share has fallen, but what happened to shareholder’s wealth. • A shareholder having 100 shares will have $700 + $ 300 = $ 1000 in his wealth and that is same as before (100 x $10 = $ 1000) • In this case, the stock price simply fell by $ 3 when the stock went ex dividend. • EPS is still the same = $ 0. 49 • P/E ratio falls to $ 7/ 0. 49 = 14. 3

Contd… Option 2: Company is thinking of using the money to repurchase $ 300, 000 / 10 = 30, 000 shares. Market Value Balance Sheet (After Share Repurchase) Excess Cash $0 Debt $0 Other assets 700, 000 Equity 700, 000 Total $ 700, 000 • The worth of the company hasn’t changed ($700, 000) • Each share still worth $ 10 • EPS goes up to $ 49, 000/70, 000 = $ 0. 70 • P/E ratio is same as that of option 1 = $ 10/0. 70 = 14. 3 If there are no imperfections, a cash dividend a share repurchase are essentially the same thing.

Equilibrium Repurchase Price

Example • Company A has enjoyed considerable recent success because they placed a huge order of their product. The business is not expected to be repeated, and Company has Rs 6 million in excess funds. The company wishes to distribute these funds via the repurchase of stock. Presently it has 2, 400, 000 shares outstanding, and the market price per share is Rs 25. It wishes to repurchase 10 percent of its stocks, or, 240, 000 shares.

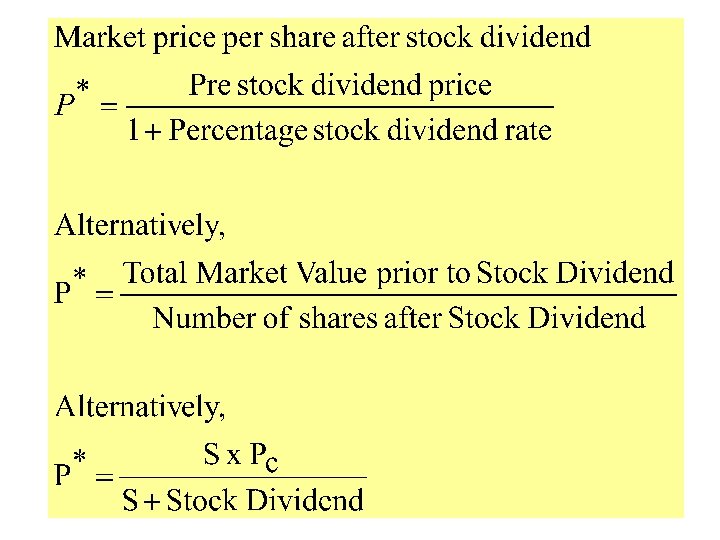

(a) Assuming no signaling effect, at what share price should the company offer to repurchase?

(b) In total, how much will the company be distributing through share repurchase ? Amount distributed through share repurchase = P* x n = Rs 27. 78 x 240, 000 = Rs 6, 667, 200

(c) What is the total amount used from retained earnings to repurchase the stocks ? Rs 6, 667, 200

(d) If the company were to pay out funds through cash dividends instead, what would be the market price per share after distribution ? • Cash dividend per share = P* - PC = Rs 27. 78 – Rs 25 = Rs 2. 78 • Price per share after cash dividend = PC - DPS = Rs 25 – Rs 2. 78 = Rs 22. 22

Real world considerations in repurchase • In the real world, there exists transaction costs and tax. • Generally a repurchase has a significant tax advantage over a cash dividend. • A dividend is fully taxed as ordinary income, and a shareholder has no choice about whether or not to receive the dividend. • In a repurchase, a shareholder pays taxes only if: – The shareholder actually chooses to sell – The shareholder has a capital gain on the sale (only on profit) • But there has to be some business-related reason for repurchasing. • “ The stock is a good investment”, “investing in the stock is a good use of money” , “the stock is undervalued”

Stock Dividends and Stock Splits • Stock Dividend: Dividend paid out in shares of stock. • The effect of a stock dividend is to increase the number of shares that each owner holds. (thus diluting the value of each shares outstanding) • A stock dividend is commonly expressed as a percentage. • Stock Split: Essentially the same thing as stock dividend, but in this case, there’s no change in the owner’s equity. • It is expressed as a ratio instead of percentage. • When a split is declared, each share is split-up to create additional shares. • For eg. In a 3 for 1 stock split, each old share is split into three new shares.

Illustration Stock Dividend • Co. A has 10, 000 shares outstanding, each selling for $ 66 • Stock dividend announced = 10 % • Total no of shares outstanding after the dividend = 11, 000 Equity position of Co. A before stock dividend: Common Stock ( $1 par, 10, 000 shares ) $ 10, 000 Capital in excess of par value (Add. Paid in capital) 200, 000 Retained earnings 290, 000 Total owner’s equity 500, 000 • After stock dividend, common stock a/c increases by $ 1, 000 • But market price of each stock is more by $ 65. • Excess of $ 65 x 1000 = $ 65, 000 is added to Capital in excess of par value.

Illustration • Total owner’s equity is unaffected by the stock dividend because, no cash has come in or gone out. • Equity position of Co A after stock dividend Common Stock ( $1 par, 11, 000 shares ) $ 11, 000 Capital in excess of par value (Additional paid in capital) 265, 000 Retained earnings 224, 000 Total owner’s equity 500, 000

Example • The Kleidon King Company has the following shareholder’s equity account: Common Stock ( Rs 8 par value) Additional paid-in capital Retained Earnings Shareholder’s equity Rs 2, 000 Rs 1, 600, 000 Rs 8, 400, 000 Rs 12, 000 The current market price of the stock is Rs 60 per share.

(a) What will happen to this account and to the number of shares outstanding with (i) 20% stock dividend ? (ii) a 2 for 1 stock split ? (iii) a 1 for 2 reverse stock split ?

(i) 20 % Stock Dividend • Number of shares outstanding before stock dividend= Rs 2000, 000/8 = 250, 000 • Stock dividend = 20% of 250, 000 = 50, 000 shares • Rs 8 x 50000 = Rs 400, 000 added in common stock. • Rs 52 premium x 50000 = Rs 2, 600, 000 added in additional paid in capital • Rs (8+ 52) x 50, 000 = Rs 3, 000 deducted from retained earnings • No of shares outstanding after stock dividend = Rs 3, 000

After stock dividend Common Stock ( Rs 8 par value) Additional paid-in capital Retained Earnings Shareholder’s equity Rs 2, 400, 000 Rs 4, 200, 000 Rs 5, 400, 000 Rs 12, 000 Number of shares outstanding = 3, 000

(ii) a 2 for 1 stock split ? • Par value after split = 8 x ½ = Rs 4 • Number of shares after split = 250, 000 x 2/1 = 500, 000 shares Common Stock ( Rs 4 par value) Additional paid-in capital Retained Earnings Shareholder’s equity Rs 2, 000 Rs 1, 600, 000 Rs 8, 400, 000 Rs 12, 000

(iii) a 1 for 2 reverse stock split ? • Par value after split = 8 x 2/1 = Rs 16 • Number of shares after split = 250, 000 x 1/2 = 125, 000 shares Common Stock ( Rs 16 par value) Rs 2, 000 Additional paid-in capital Rs 1, 600, 000 Retained Earnings Rs 8, 400, 000 Shareholder’s equity Rs 12, 000

(b) In the absence of an informational or signaling effect, at what share price should be common stock sell after the 20% stock dividend ?

(b) What would have happened if there were signaling effect ? • If there were a signaling or informational effect, the stock price per share might be somewhat higher than Rs 50

Exercise Common stock ($8 par value) Additional paid-in capital Retained earnings Total shareholders’ equity $2, 000 1, 600, 000 8, 400, 000 12, 000 • The current market price of the stock is $ 60 per share. • What will happen to this account and to the number of shares outstanding with – A 10 percent stock dividend – A 2 -for-1 stock split – A 1 -for-2 reverse stock split • In the absence of an informational or signaling effect, at what share price should the common stock sell after the 10 percent stock dividend? What might happen to stock price if there were signaling effect?

• Present number of shares outstanding = 2, 000 / 8 = 250, 000 Stock dividend Common stock 275, 000 @ 8 = 2, 200, 000 Additional paid in capital 2, 900, 000 Retained earnings 6, 900, 000 Total shareholders’ equity 12 million

• Present number of shares outstanding = 2, 000 / 8 = 250, 000 Stock dividend Stock split Common stock 275, 000 @ 8 = 500, 000 @ 4 = 2, 200, 000 2, 000 Additional paid in capital 2, 900, 000 1, 600, 000 Retained earnings 6, 900, 000 8, 400, 000 Total shareholders’ equity 12 million

• Present number of shares outstanding = 2, 000 / 8 = 250, 000 Stock dividend Stock split Reverse split Common stock 275, 000 @ 8 = 500, 000 @ 4 = 2, 200, 000 2, 000 125, 000 @ 16 = 2, 000 Additional paid in capital 2, 900, 000 1, 600, 000 Retained earnings 6, 900, 000 8, 400, 000 Total shareholders’ equity 12 million

• Present number of shares outstanding = 2, 000 / 8 = 250, 000 Stock dividend Stock split Reverse split Common stock 275, 000 @ 8 = 500, 000 @ 4 = 2, 200, 000 2, 000 125, 000 @ 16 = 2, 000 Additional paid in capital 2, 900, 000 1, 600, 000 Retained earnings 6, 900, 000 8, 400, 000 Total shareholders’ equity 12 million The total market value of the firm before the stock dividend is $60 x 250, 000 = $ 15 million. With no change in the total value of the firm the market price of share after stock dividend should be = $ 15 million / 275, 000 = 54. 55 per share. However, if there is signaling effect, the total value of the firm might rise and share price be somewhat higher than 54. 55 per share.