DIP Business Plan E Lim Sei Kee c

Lim Sei Kee @ c. K")

DIP - Business Plan (E) Lim Sei Kee @ c. K

Plan to make your Business Plan Allocate the time you need to do certain parts of the Business Plan - Use calendar / Planner / Diary / Journal - Create a deadline for specific tasks If you are doing in a group, allocate specific tasks for a specified person

Writing tips � Clear � Concise � Organized � Well laid out � Natural � Positive � Well interpreted facts � Do not jump to conclusions � Show sources � Proofread � Make it perfect

Presentation Tips � 15 – 20 slides � 15 – 20 minutes � Keep it simple � Make it to the point � Tell a story � Dress professionally � Practice ◦ In front of mirror ◦ In front of someone

� Existing problem/pain/situation � Solution (Product/service)")

Tell a story � Introduction (breaking the ice) � Existing problem/pain/situation � Solution (Product/service) you are providing � Market research and strategy � Who are involved � How you can succeed

Quick tips � Its not just an idea, but a work in progress � You have the numbers to back you up � You have qualified people involved � Be passionate in your presentation

![Introduction Financial planning means to prepare the financial plan. [@ capital plan] A financial](http://slidetodoc.com/presentation_image_h2/414546408249a19dd177c45ccf8d8ba4/image-8.jpg "Introduction Financial planning means to prepare the financial plan. [@ capital plan] A financial")

Introduction Financial planning means to prepare the financial plan. [@ capital plan] A financial plan is an estimate of the total capital requirements of the business. Financial plan gives a total picture of the future financial activities of the business.

Financial Plan � Taking a commercial business as the most common organizational structure, the key objectives of producing a financial plan would be to: � • Create wealth for the business � • Generate cash, and � • Provide an adequate return on investment

FINANCIAL PLAN IS NOT ACCOUNTING � Accounting looks back in time, starting today and taking an historical view. � Business planning or forecasting is a forwardlooking view, starting today and going forward into the future.

The working capital cycle � Cash sales to customers � Purchasing � Receipts � Purchasing from customers who were allowed to buy on credit (trade debtors) � Investment by shareholders Inflows finished goods for re-sale raw materials needed for the manufacturing of the final product � Paying salaries and wages and other operating expenses Outflows

Cash flow can be described as a cycle: business uses cash to acquire (assets such as stocks) � The resources are put to work and goods and services produced. These are then sold to customers � The customers pay in cash, but others ask for time to pay. Eventually they pay and these funds are used to settle any liabilities of the business. � Some � And so the cycle repeats

� The cash needed to make the cycle above work effectively is known as working capital. �Working capital is the cash needed to pay for the day to day operations of the business.

3 important financial statements � Financial statements: � A. the income statement, � B. the cash flow projection, and � C. the balance sheet � PLUS, a brief explanation/analysis of these three statements.

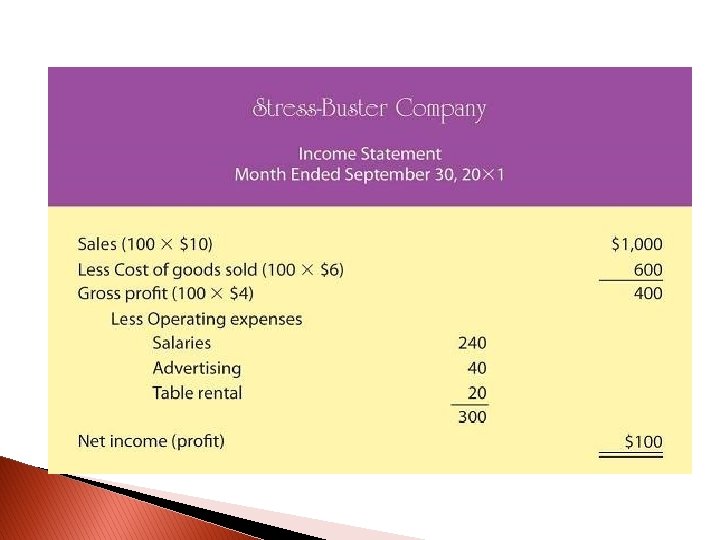

Income Statement � The Income Statement shows your Revenues, Expenses, and Profit �")

(A) Income Statement � The Income Statement shows your Revenues, Expenses, and Profit � Revenue - Expenses = Profit/Loss.

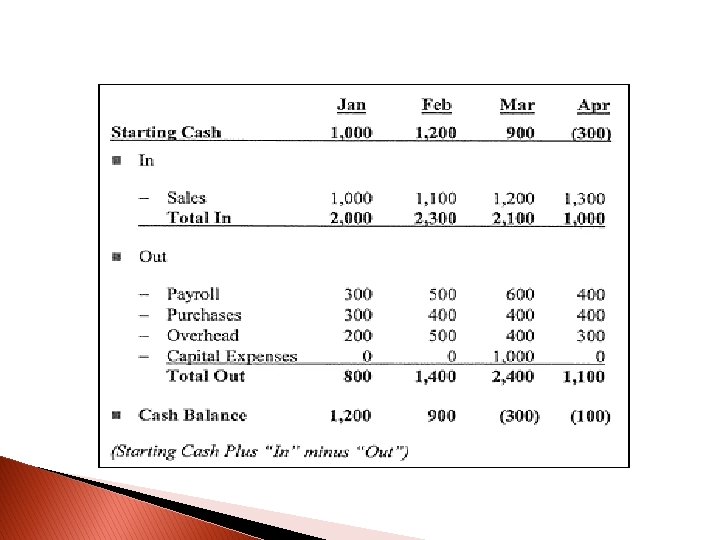

Cash flow projection � Opening balance -How much cash business has at start")

(B) Cash flow projection � Opening balance -How much cash business has at start of time period � Cash inflows - How much cash is coming into business from product sales, sales of assets, loans from bank, and other sources of finance � Cash outflows - How much cash is going out of business, such as expenses, wages, raw materials, buying new machinery, and dividends � Closing balance - How much money is left at end of month

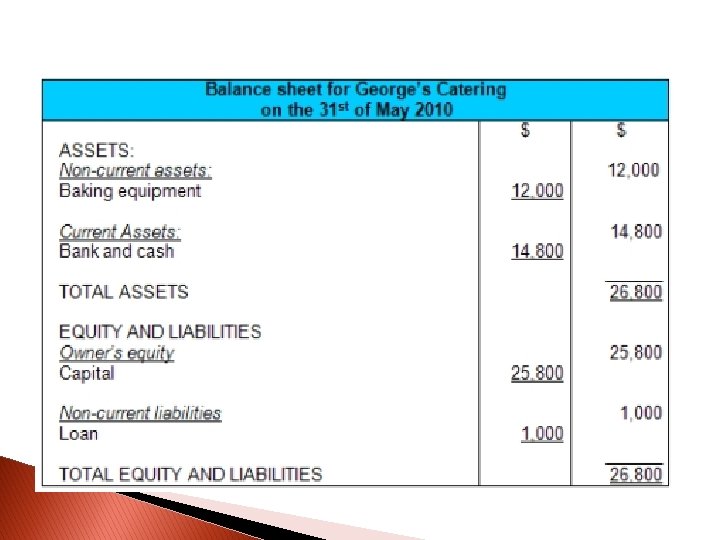

Balance Sheet � The Balance Sheet is the last of the financial statements")

(C) Balance Sheet � The Balance Sheet is the last of the financial statements that you need to include in the Financial Plan section of the business plan. � It summarizes all the financial data about your business, breaking that data into 3 categories; assets, liabilities, and equity.

�Assets are tangible objects of financial value that are owned by the company. �A liability is a debt owed to a creditor of the company. �Equity is the net difference when the total liabilities are subtracted from the total assets.

Your financial plan: � Start with a sales forecast. � Create an expenses budget. � Develop the three financial statements.

- Slides: 23