Derivatives and Hedging Risk g modebadzeagruni edu ge

Derivatives and Hedging Risk �������� g. modebadze@agruni. edu. ge

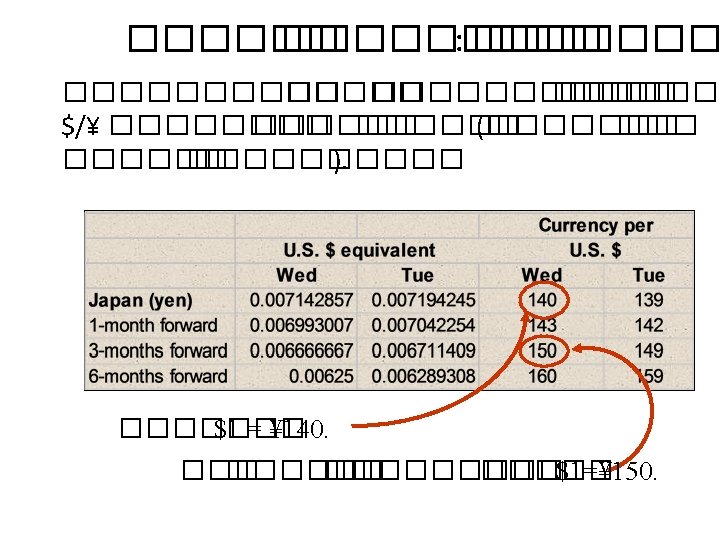

Wall Street Journal Futures Price Quotes Highest price that day Highest and lowest prices over the lifetime of the contract. Opening price Closing price Lowest price that day Expiry month Daily Change Number of open contracts

25. 5 ����������� • • Pricing of Treasury Bonds Pricing of Forward Contracts Futures Contracts Hedging in Interest Rate Futures

Pricing of Treasury Bonds ����� Treasury bond ������� ����� $C-���� T ������������ : – The yield to maturity is R … 0 1 2 3 2 T Value of the T-bond under a flat term structure = PV of face value + PV of coupon payments

Pricing of Treasury Bonds ������ ����� ��������� �������. … 0 1 2 3 2 T = PV of face value + PV of coupon payments

Pricing of Forward Contracts An N-period forward contract on that T-Bond: … 0 N N+1 N+2 N+3 N+2 T Can be valued as the present value of the forward price.

Pricing of Forward Contracts: ���������� 5 ��������� 20 ������ T-bond-�������. coupon rate is 6 percent per annum, and payments are made semiannually on a par value of $1, 000. N 40 = 20 × 2 The Yield to Maturity is 5 percent. I/Y 5 PV – 1, 125. 51 First, set your calculator to 2 payments per year. PMT FV 1, 000 ×. 06 30 = 2 1, 000 Then enter what you know and solve for the value of a 20 -year Treasury bond at the maturity of the forward contract.

Pricing of Forward Contracts: Example First, set your calculator to 1 payment per year. Then, use the cash flow menu: CF 0 0 I CF 1 0 NPV F 1 5 CF 2 – 1, 125. 51 1 5 881. 86

. –")

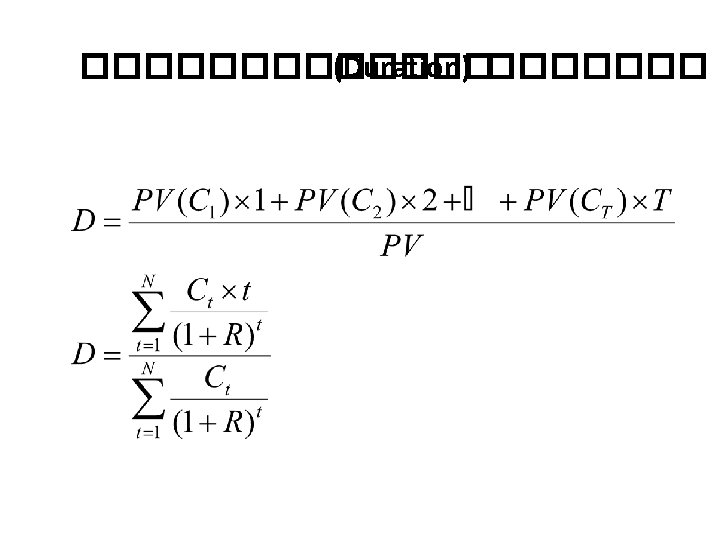

25. 6 ����������� • ������ �������� ����� �������������� (maturity, coupon rate, and YTM). – Measure of the bond’s effective maturity – Measure of the average life of the security – Weighted average maturity of the bond’s cash flows

������� : ������� Duration is expressed in units of time, usually years.

�������������� : – Longer maturity, longer duration – Duration increases at a decreasing rate – Higher coupon, shorter duration – Higher yield, shorter duration • ��������� : duration = maturity

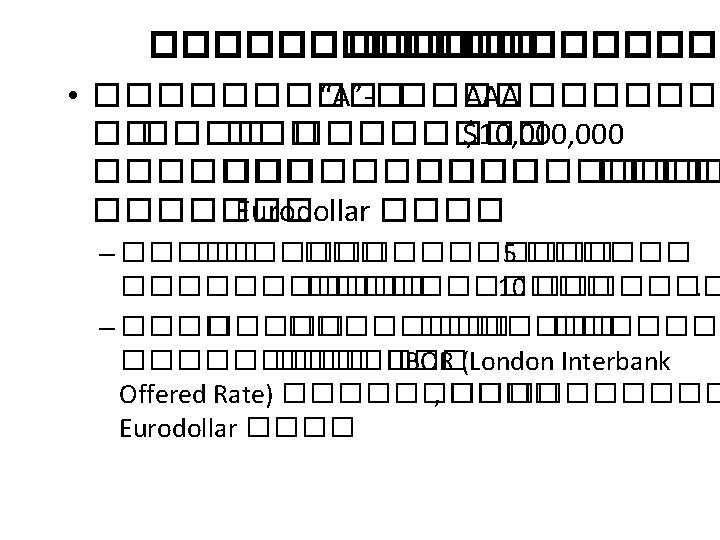

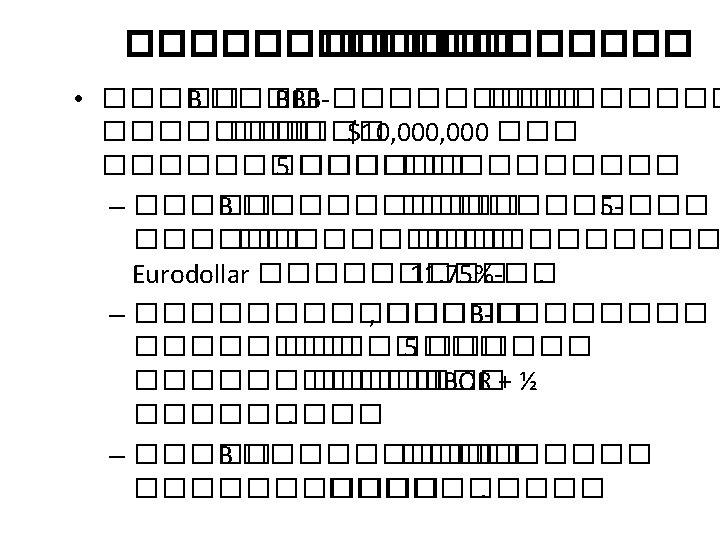

�������� Swap 10 3/8% Bank LIBOR – 1/8% Bank A The swap bank makes this offer to Bank A: You pay LIBOR – 1/8 % per year on $10 million for 5 years, and we will pay you 10 3/8% on $10 million for 5 years

�������� ½% of $10, 000 = $50, 000. That’s quite a cost savings per year for 5 years. 10 3/8% Swap Bank LIBOR – 1/8% Bank 10% A Here’s what’s in it for Bank A: They can borrow externally at 10% fixed and have a net borrowing position of -10 3/8 + 10 + (LIBOR – 1/8) = LIBOR – ½ %, which is ½ % better than they can borrow floating without a swap.

�������� The swap bank makes this offer to company B: You pay us 10½% per year on $10 million for 5 years, and we will pay you LIBOR – ¼ % per year on $10 million for 5 years. Swap Bank 10 ½% LIBOR – ¼% Company B

�������� Here’s what’s in it for B: Swap Bank They can borrow externally at LIBOR + ½ % and have a net ½ % of $10, 000 = $50, 000 that’s quite a cost savings per year for 5 years. 10 ½% LIBOR – ¼% borrowing position of 10½ + (LIBOR + ½ ) - (LIBOR - ¼ ) = 11. 25% which is ½% better than they can borrow floating. Company B LIBOR + ½%

�������� The swap bank makes money too. Swap 10 3/8% Bank 10 ½% LIBOR – 1/8% Bank A ¼% of $10 million = $25, 000 per year for 5 years. LIBOR – ¼% LIBOR – 1/8 – [LIBOR – ¼ ]= 1/8 10 ½ - 10 3/8 = 1/8 Company B

�������� The swap bank makes ¼% Swap 10 3/8% Bank LIBOR – 1/8% 10 ½% LIBOR – ¼% Bank Company A B A saves ½% B saves ½%

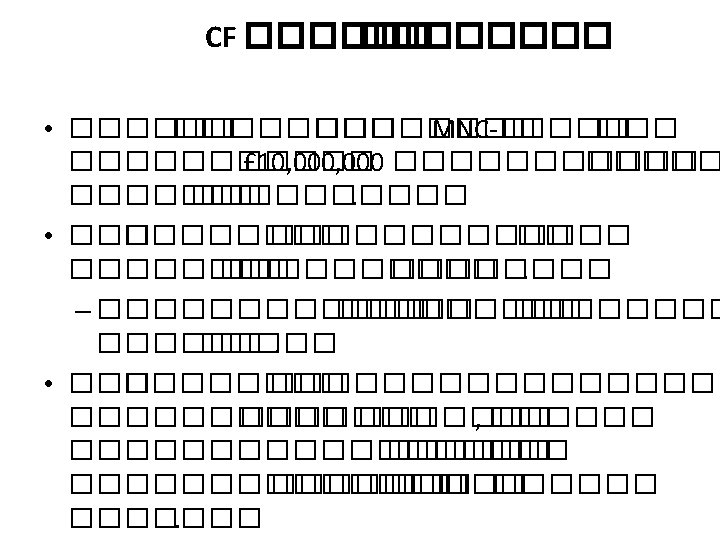

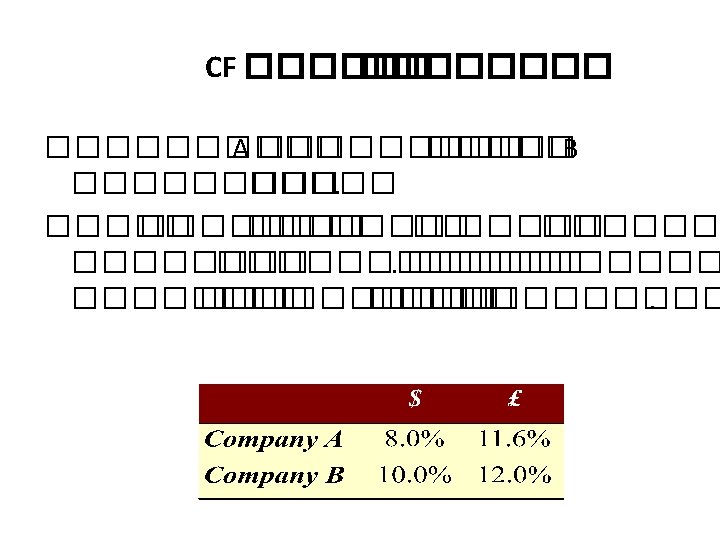

CF �������� Swap Bank $8% £ 11% $8% $9. 4% £ 12% Firm A B £ 12%

CF �������� A’s net position is to borrow at £ 11% Swap Bank $8% £ 11% $8% $9. 4% £ 12% Firm A B A saves £. 6% £ 12%

CF �������� B’s net position is to borrow at $9. 4% Swap Bank $8% £ 11% $8% $9. 4% £ 12% Firm A B £ 12% B saves $. 6%

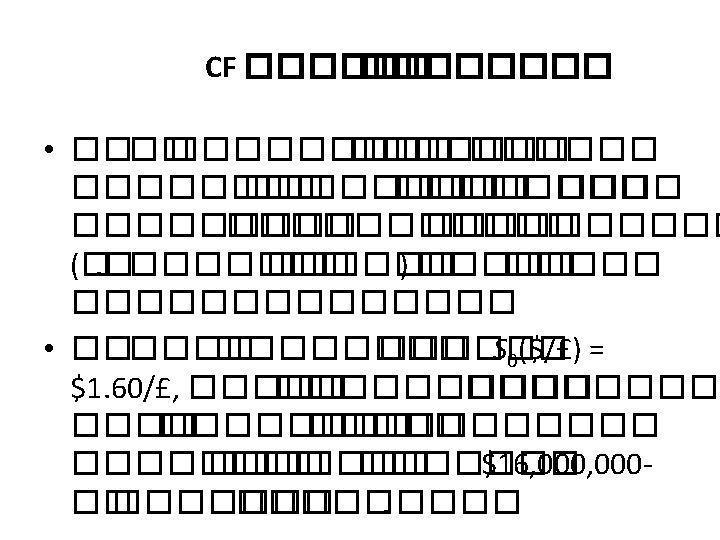

CF �������� The swap bank makes money too: Swap Bank $8% £ 11% $8% Firm A 1. 4% of $16 million financed with 1% of £ 10 million per year for 5 years. $9. 4% £ 12% Firm £ 12% At S 0($/£) = $1. 60/£, that is a gain of $64, 000 per B year for 5 years. The swap bank faces exchange rate risk, but maybe they can lay it off (in another swap).

Variations of Basic Swaps • Currency Swaps – fixed for fixed – fixed for floating – floating for floating – amortizing • Interest Rate Swaps – zero-for floating – floating for floating • Exotics – For a swap to be possible, two humans must like the idea. Beyond that, creativity is the only limit.

Risks of Interest Rate and Currency Swaps • Interest Rate Risk – Interest rates might move against the swap bank after it has only gotten half of a swap on the books, or if it has an unhedged position. • Basis Risk – If the floating rates of the two counterparties are not pegged to the same index • Exchange Rate Risk – In the example of a currency swap given earlier, the swap bank would be worse off if the pound appreciated.

Risks of Interest Rate and Currency Swaps • Credit Risk – This is the major risk faced by a swap dealer—the risk that a counter party will default on its end of the swap. • Mismatch Risk – It is hard to find a counterparty that wants to borrow the right amount of money for the right amount of time. • Sovereign Risk – The risk that a country will impose exchange rate restrictions that will interfere with performance on the swap.

Quick Quiz • Explain the differences between forward and futures contracts. • Explain the process of valuing a futures contract. • Explain why/how corporations would use futures contracts.

- Slides: 46