DEPOSITORY INSTITUTIONS What is a DEPOSITORY INSTITUTION A

. • Compte")

: • Commercial banks make up the largest group of")

de MAD Net")

- Slides: 41

DEPOSITORY INSTITUTIONS

What is a DEPOSITORY INSTITUTION ? A depository institution is a financial institution (such as a savings bank, commercial bank, savings and loan association, or credit union) that is legally allowed to accept monetary deposits from consumers (general public) , and pays a fixed or variable rate of interest.

What is a bank? • A bank is a financial organization where people deposit their money to keep it safe. But that’s only part of how a bank works. • A bank is a business like any other business. The business needs to make enough money to pay the people who work there and the cost of things like electricity, office supplies. • In order for a bank to be profitable, it needs to get the maximum of people to put their money in it; thus each bank tries to make THEIR bank look better than all of the others by offering services that some other banks might not have.

Why Banking? How did it start? Why does it work? • Our method of banking originated with the goldsmiths - the predecessors of our present bankers. • The goldsmiths noticed that the people who deposited gold with them for safekeeping only withdrew a small amount at any one time. The goldsmiths realized that they could lend out a lot of the gold left with them by issuing paper receipts to borrowers for gold they did not own. The goldsmiths would make money by charging interest on the loans. • Loans were often secured with a pawn of silver plate or jewelry and the receipts circulated as money. • There were soon several receipts in circulation for one amount of gold, the origins of our system of “Fractional Reserve Banking” where much greater sums of money are lent out than assets held by the banks. • Our economy depends upon banks’ lending money. Bank loans to businesses help create many jobs. • Without a bank mortgage it would take most of our working lives to save the cash to buy a family home. • But banking is all about trust. We trust that the bank will have our money for us when we go to get it.

How banks make money:

The Different Types of Bank Services • • Checks Wire Transfer Bank Payment The Withdrawal La mise a disposition/ The making available Exchange of currency ATM Machine Management Transfer of money abroad (Western Union, Money. Gram, …)

The Different Types of Bank Accounts • Compte courant (Running/current account ). • Compte de depots ou compte cheque (Deposits/Checks account). • Compte a terme (DAT)/ term account. • Compte sur carnet (Book of account). • Convertible dirham account. • Other accounts.

Account Opening • General Conditions • Conditions related to the customer’s identity

Overview of Depository Institutions in Morocco:

Historical Background: • First phase: 1800 -1993 • Second phase: 1993 - 2013

Structure of the Moroccan Banking System:

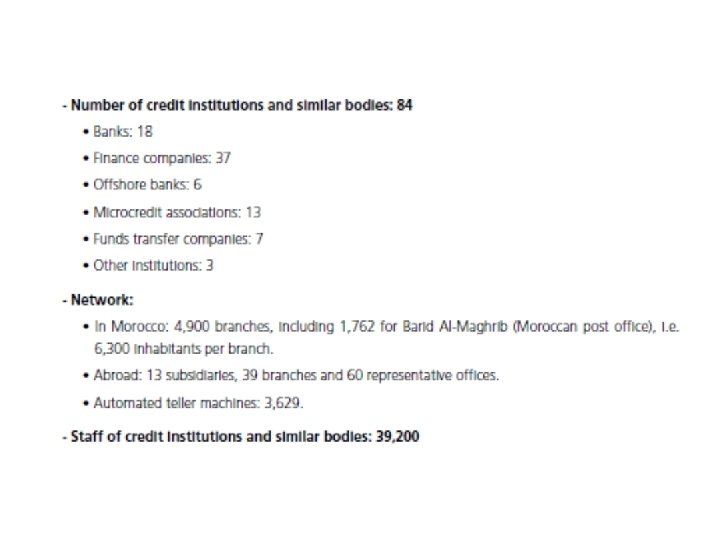

Evolution of Moroccan Credit Institutions and similar bodies’ number:

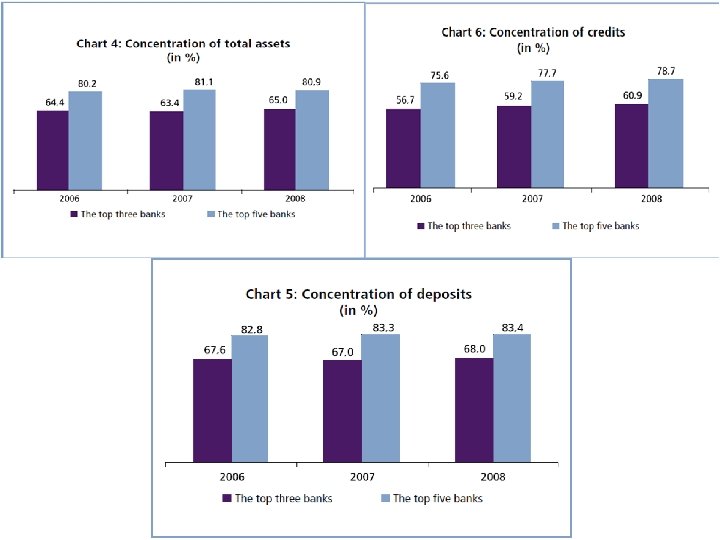

Structure of Moroccan Banks’ Assets and Liabilities:

Bancarization Indicators: • The penetration rate of banking services have drastically improved over the last years to reach 51% in 2012 (expected to reach 54% in 2013). Yet Moroccan banks still suffer from insufficient network. • However, bank density remains unbalanced in favor of urban areas compared to rural areas.

Banking by region:

Moroccan Banks Sectors of Activity

Investment activities: • investment activities are about assisting individuals, corporations, and governments in raising capital by underwriting and/or acting as the client's agent in the issuance of securities. An investment bank may also assist companies involved in mergers and acquisitions, and provide ancillary services such as market making, trading of derivatives, fixed income instruments, foreign exchange commodities, and equity securities. Attijari Wafabank does that through Attijari Invest. Bmce bank does that through BMCE CAPITAL. Banque Populaire does that through UPLINE ALTERNATIVE INVESTMENTS.

Consumer credits: • consumer credits are basically amounts given to consumers and used by them to purchase noninvestment goods or services that are consumed and whose value depreciates quickly. This includes automobiles, recreational vehicles (RVs), and education, boat and trailer loans but excludes debts taken out to purchase real estate or margin on investment account. Attijari Wafabank does that through wafasalaf, and Banque populairedoes that through vivalis.

Mortgages: • which are about giving costumers efficient and effective solutions to acquire real estate. Attijari Wafabank performs this task through Wafa Immobilier, and banque populaire through Maroc leasing.

Asset management: • this task is mainly about managing the portfolio of a client by buying and selling securities. Attijari Wafabank does that through Wafa gestion, banque populaire through UPLINE Capital Management & Al Istitmar Chaâbi, and bmce bank through bmce capital gestion.

Market intermediation: • this activity is mainly dues to the imperfection nature of markets where the complete knowledge about providers and seekers is not available to everyone. Therefore, A financial institution such as a bank, intermediates credit when it obtains money from a depositor and relends it to a borrowing customer. BMCE BANK does that through BMCE CAPITAL BOURSE, and banque populaire does it through UPLINE Securities & ICF Al Wassit

Types of Depository Institutions: • Commercial Banks • Savings Banks • Credit Unions

1. Commercial banks (Definition) : • Commercial banks make up the largest group of depository institutions measured by asset size. They perform functions similar to those of savings institutions and credit unions; that is, they accept deposits (liabilities) and make loans (assets).

2 - Saving Banks “ Savings banks are financial institution that gathers savings and pays interest or dividends to savers. It channels the savings of individuals who wish to consume less than their incomes to borrowers who wish to spend more. ”

3 – Credit Unions

What It Is: • A credit union is a financial institution that is owned and controlled by its members rather than shareholders. The members of the credit union pool their deposits and provide loans and other financial services to each other.

How It Works/Example: • The services offered by a credit union include a wide range of financial services, such as savings accounts, checking accounts, credit cards, certificates of deposit and online financial services. A credit union’s fees, interest rates and levels of service are highly responsive to the needs of its members. Generally, they offer lower interest rates on loans and higher interest rates on savings accounts and certificates of deposit. Credit unions may be formed among any group of members who have a common interest -- usually community groups or employees of a particular organization. The board members of the credit unions are usually volunteers. Credit unions are generally not-forprofit, so often profits are shared by members.

Why It Matters: • Credit unions offer most of the same services as banks, but differ in that individual members are owners and there are generally less assets under management. Because credit unions are usually considerably smaller than banks, they are able to offer more personalized advisory services to their members and they may offer lower cost banking service.

Major Banks in Morocco: • When talking about banks in Morocco we will take the examples of the three major ones: • Attijari Wafabank • Banque Populaire • Bmce Bank

Attijari Wafabank is a Moroccan financial and banking group. It is considered as the first financial and banking group in the Maghreb, and the first at the African level since 2010.

Important Figures: The Attijari Wafabank group has more than 5. 5 millions clients and 14861 collaborators.

Groupe Banque Populaire • • The Moroccan popular bank is the most common name we give to the group of the popular banks. A banking and financial group composed of 11 regional popular banks that are in the form of cooperative companies of the Central Popular bank that is an anonymous company listed in the Casablanca Stock Exchange.

Important Figures: Capitalisation 15, 7 milliards de MAD Profits 10. 2(2012) de MAD Net result 2, 8 milliards de MAD

BMCE BANK • Bmce Bank is a Moroccan Commercial Bank affiliated to the holding Finance. com of Othman benjelloun, it is the third bank of the Kingdom. • It is the third bank in terms of total assets, with market shares about credit and deposits around 13% and 15. 2% respectively. • It is the second transmitter of electronic banking card with a market share of 17. 4%. • It is the second assuror bank with a market share of 30%. • It is the second asset manager with a market share of 14%.

Important Figures:

Postal Saving Banks • Postal savings bank: any of the savings banks formerly operated by local post offices and limited to small accounts

Al Barid Bank • Creation • Strategy • Services

Swot Analysis of Moroccan Banks: • • They all have significant financial resources. The existence of dozens of specialized subsidiaries in all banking sectors. A network covering the totality of the territory and also the main countries hosting Moroccan residents abroad (MRE), plus a wide sales network (5113 branches). Powerful computerized tools. A bank regulation and management based on international standards Modern and diversified product offerings (electronic banking, savings, banking / insurance…) More transparency at the accounting level: under the new banking law, the credit institutions are obliged to establish their accounting statements and any other information allowing the central bank to exercise its control easily according to the standards that it sets. The banking system in Morocco remains protected against external shocks (exchange rate policy, fixed exchange rate regime) Opportunities: • • • Economic aspect: ü Economic development in Morocco several sectors (real estate, tourism, agriculture. . . ) ü Liberalization of banking. ü Liberalization of interest rates. Sociocultural aspect: ü Changing attitudes in Morocco. ü Technological revolution in the use of internet. Geographical aspect: ü Emergence of the concept of customer proximity. • Floating commercial activity due to merger (oligopoly). • Low staff motivation. • A strong position rotation. • Bank Density is unbalanced in favour of urban areas. • Risk of legal system: Our Legal System is still weak. Threats: • • • Economic aspect: ü International Financial Crisis ü Floating at the level of the Casablanca Stock Exchange. ü High intermediation rates compared to resources cost. ü High inflation against low purchasing power and consumption. Legal aspects: ü Absence of a unified legal framework and non-application of prudential rules. Competition: ü There is a tough and unfair competition. ü Uniformity of banking products.

Thank you for your attention