Deposit Insurance in Hong Kong Deposit Protection Scheme

l United States government corporation Start in 1933")

Maximum")

l l The objectives of the deposit insurance systems protect depositors and")

l Funding is provided in some ways such as through government appropriations,")

- Slides: 36

Deposit Insurance in Hong Kong

Deposit Protection Scheme in HK l Commencement on 25 th of Sept 2006 l Governing by Deposit Protection Scheme Ordinance (Cap. 581) l Compensation limit is set at maximum HK $100, 000

Deposit Protection Scheme in HK l Both Hong Kong dollar and foreign currency deposits are protected l The fund will be built up through the collection of contributions from Scheme members l Differential contributions will be assessed based on the supervisory ratings of individual Scheme members

The duties & responsibilities of DPS Board l l l Collect premiums Manage the DIS Fund Assess claims Make compensation payments Make rules relating to the procedures for making claims and payouts

The Deposit Insurance in the world l l Total 44 Countries Albania, Quebec, Morocco, Sudan, Bulgaria, Canada, Taiwan, Romania, Russia, Bosnia and Herzegovina, India, Tanzania, Trinidad and Tobago, Japan, Bahamas, Czech Republic, Vietnam, Zimbabwe, Kenya, USA, Nicaragua, Venezuela, Colombia, Peru, France, Brazil, Hong Kong, Indonesia, Lebanon, El Salvador, Mexico, Jamaica, Jordan, Kazakhstan, Korea, Malaysia, Hungary, Nigeria, Philippine, Turkey, Argentina, Singapore, Sweden, Ukraine

Deposit Insurance – USA

Background Federal Deposit Insurance Corporation (FDIC) l United States government corporation Start in 1933 ( Great Depression ) l bank runs (4004 banks) l depositor lose of confidence l Arthur Vandenberg, Henry Steagall restore confidence

FDIC l Independent agency l Protect depositor against loss l Provides deposit insurance taken by banks l Meet high standards (financial strength, stability)

Insurance l Insured tradition types of bank account e. g. checking, saving, trust, CDs etc… legal limit of $100, 000 per depositor per insured bank l Uninsured investment products e. g. mutual funds, stocks, bonds

Deposit Insurance –Taiwan

Deposit Insurance –Taiwan The policy goals: 1. Safeguarding the benefits of depositors in financial institutions 2. Promoting savings 3. Maintaining an orderly credit system 4. Enhancing the sound development of financial operations

Taiwan Deposit Insurance System Launched September-1985 Administered by Central Deposit Insurance Corporation (CDIC) Maximum Coverage NT$1 million limited to deposit principal per depositor per insured institution Premiums Premium Rates Paid by member institutions Risk-based rate system and three rates instituted: 0. 05%, 0. 055% and 0. 06%

Participating Institutions Domestic banks • including trust and investment companies and postal savings bank Credit cooperatives Foreign bank branches in Taiwan • Foreign bank branches whose deposits are protected in their home countries may not participate

Insured Deposits Checking accounts Passbook deposits Time deposits Savings deposits, including postal savings deposits 支票存款 活期存款 定期存款 儲蓄存款、郵政儲金

Uninsured Deposits Foreign currency and foreign exchange deposits 外幣、外匯存款 Negotiable certificates of deposit 可轉讓定期存單 Structured deposits Deposits from government agencies 各級政府機關存款 Deposits from the Central Bank 中央銀行存款 Deposits exceeding the per-institution maximum insurance coverage established for each depositor 每一存款人在同一金融機構 超過最高保額部分的存款

Deposit Insurance –Japan

Deposit Insurance Corporation of Japan l Established in 1971 l The limited coverage of ¥ 1 million l April 2002 l The limited coverage of ¥ 10 million

Insurance Pay-out method 1. 2. 3. 4. 5. 6. 7. 8. Occurrence of insurable contingency. Notification of contingency Submission of data on depositors Calculation of the insurance (Max: ¥ 10 million per depositor ) Decision on payment of the insurance and details of public announcement Public Announcements Insurance Payment Notification Claim for the insurance payment

Financial Assistance l When a financial institution fails, DICJ may extend financial assistance l Facilitate the transaction

Financial Assistance Method of financial assistance: l Purchases assets l Partial Business Transfer l Monetary grant l Subscribing of Preferred Shares

Summary In Hong Kong, Japan, Taiwan & USA

Summary (1) l l The objectives of the deposit insurance systems protect depositors and contribute to financial system stability Legally separate organizations, rely on a board of directors The membership is compulsory and is extended to institutions subject to effective supervision and regulation Covering savings deposit products and excluded coverage of non-deposit products

Summary (2) l Funding is provided in some ways such as through government appropriations, premiums assessed against member banks… l To reimburse depositors as quickly as possible. Reimbursement depends on the bank deposit records

Conclusion

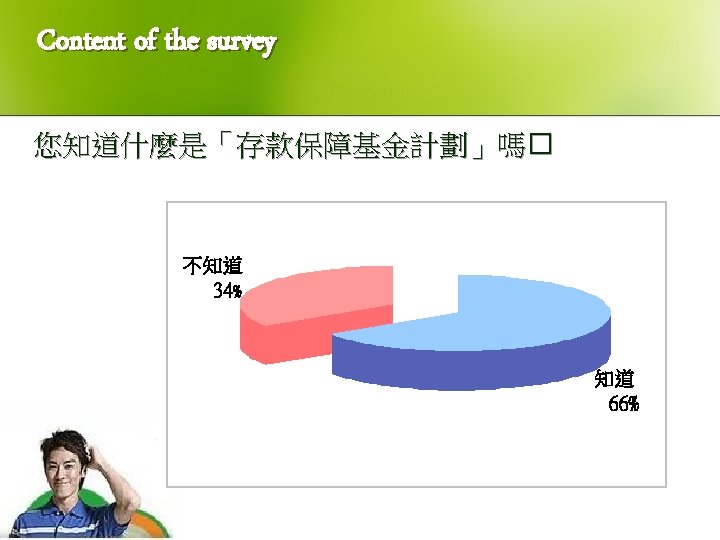

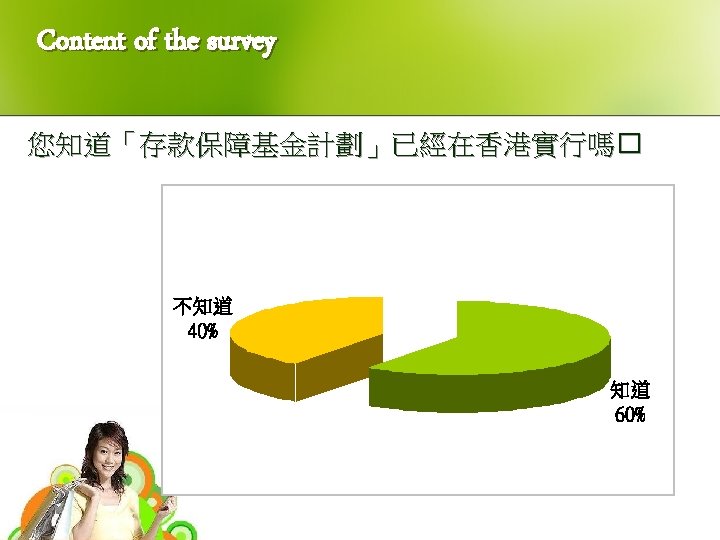

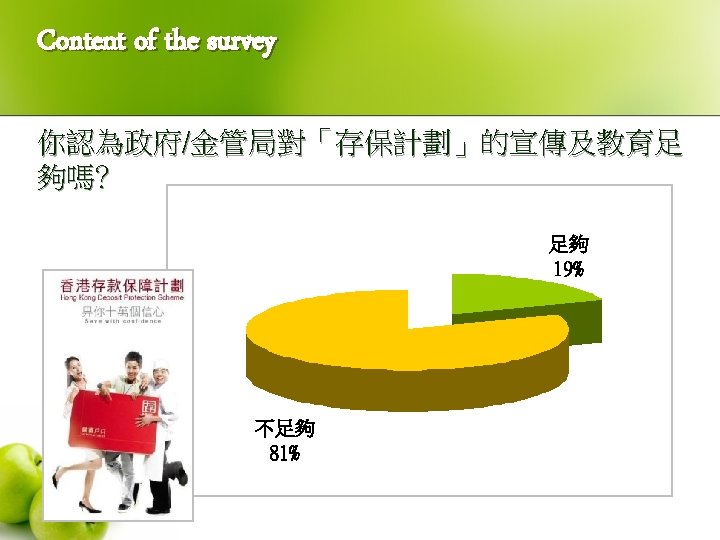

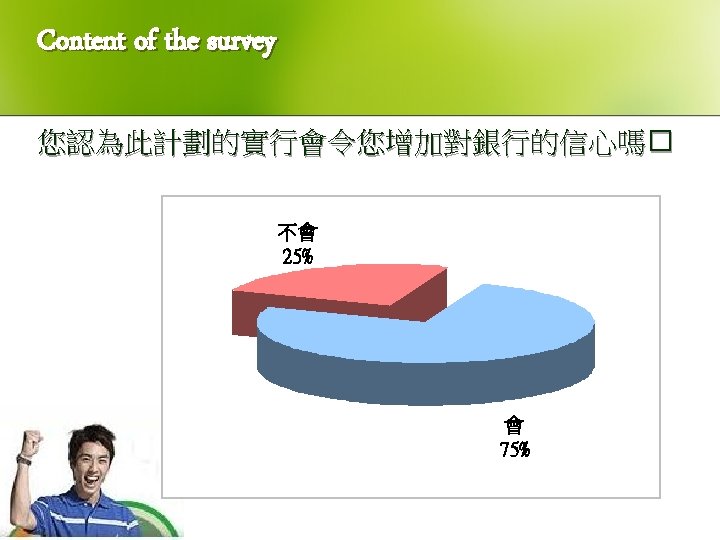

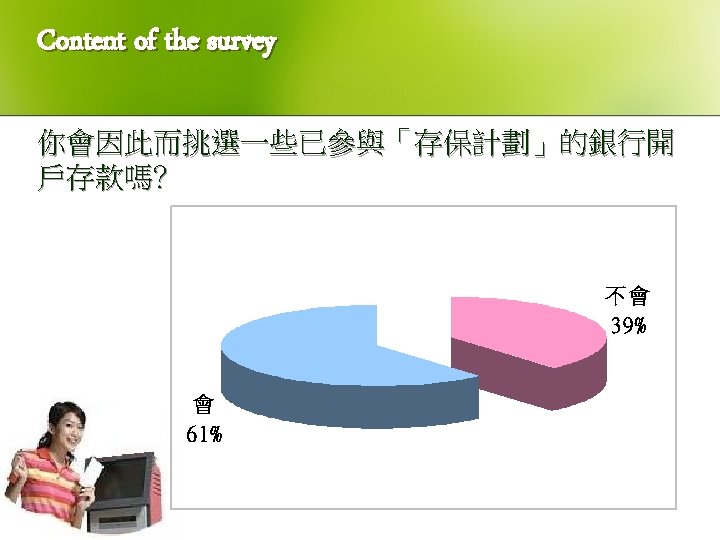

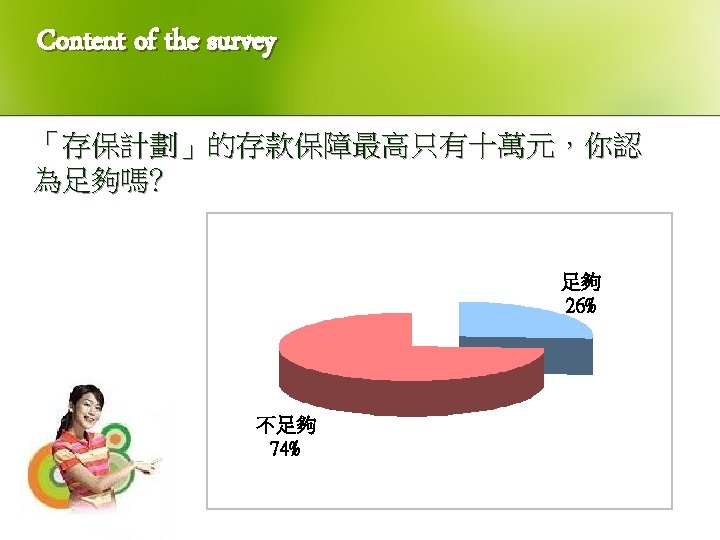

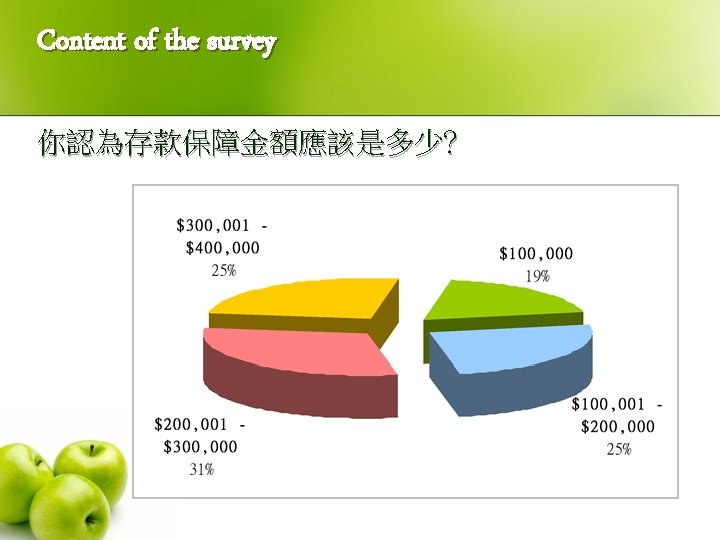

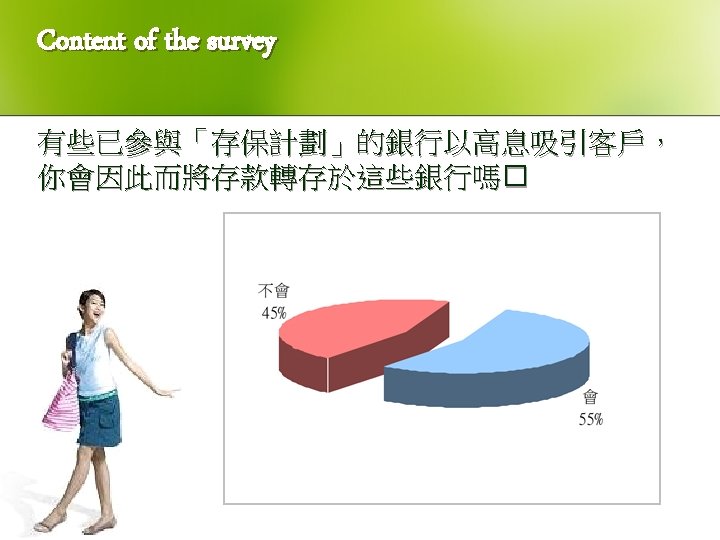

Survey Date : 29 th November, 06 - 10 th December, 06 Interviewers : 122 people Website : http: //www. my 3 q. com/view. Summary. phtml? questid=13511

The conclusion of the Survey

-The End-