Deploying New Markets and Historic Tax Credits for

is a federal income tax")

? A census tract in which:")

makes")

is a federal income tax")

$10 million X: HTC Tax Credit Rate")

$X Loan Proceeds NMTC Fund Equity")

- Slides: 24

Deploying New Markets and Historic Tax Credits for Capital Projects Fall 2020 CPE Forum

Matt Blumenfeld, Principal ~ matthew@financialdevelopmentagency. com Sarah Tanner, Principal ~ sarah@financialdevelopmentagency. com 49 South Pleasant Street • Suite 201 • Amherst, MA 01002 413. 253. 0239 www. financialdevelopmentagency. com

Tax Credits can mean the difference between success and failure for Capital Projects Overview: Both for profit and non-profit entities may take advantage of tax credit programs to make capital projects a reality. New Markets Tax Credits (NMTCs), and Federal Historic Tax Credits (FHTCs) are federal programs, while states often have additional Historic Tax Credit programs available. Capital Stack Complexity: Tax credits make for more complex transactions than traditional project financing. Both federal programs require expertise and a complex legal structure. Massachusetts HTC program is relatively straightforward. Balancing Act: Deal monitoring, restrictions and oversight costs must be balanced against the financial benefits.

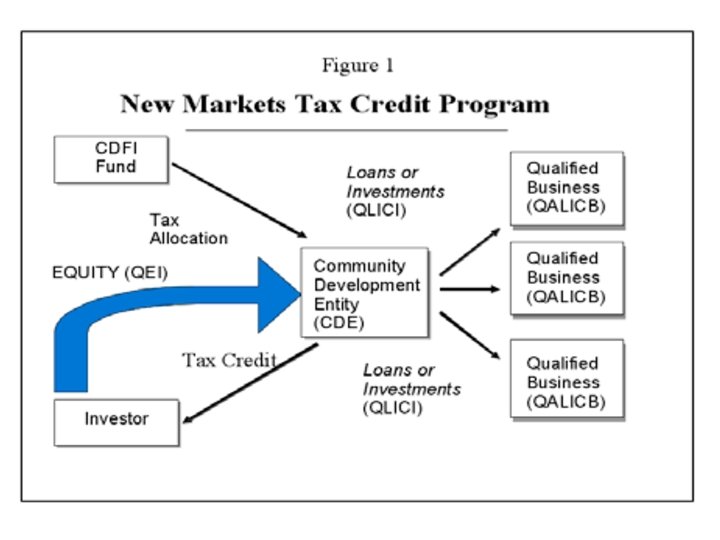

NMTC Program Overview: The New Markets Tax Credit (NMTC) is a federal income tax credit for commercial and mixed-use projects and businesses located in qualified (lowincome) census tracts. NMTC Amount: The NMTC amount equals 39 percent of a qualified equity investment (QEI) in a “community development entity” (CDE). NMTC Accrual: The NMTC amount accrues over seven years (5 points over first three years and 6 points for final four years). Combination: NMTCs can be combined with other tax incentives (such as taxexempt bonds and historic tax credits), other than LIHTCs.

NMTC Program Overview NMTC Allocation: A CDE is a privately-owned entity certified as targeted at lowincome communities or persons. An NMTC allocation is the total qualified equity investment (QEI) dollar amount that a CDE can issue (as opposed to the total credit amount that the QEI will generate). A CDE with an NMTC allocation functions, in essence, as a special purpose bank. NMTC Allocation Awards: The CDFI Fund (within the Department of the Treasury) certifies CDE status and makes annual QEI allocations to competing CDEs. NMTC Conditions: A CDE must use QEI proceeds to make qualified equity investments in or loans (QLICI) to a qualified active low-income community business (QALICB). QEI proceeds must remain fully deployed (via the QLICIs) for seven years. This seven-year full deployment requirement precludes any return of capital or principal repayment (including as a result of a foreclosure) on any QLICI.

NMTC Program Overview QALICB: In general, a QALICB is any business or project located in a qualified census tract, except for any unimproved real estate, residential real estate, collectible business, financial property business or “sin”- type business. Numerical tests (based revenue source, asset location, and employees) determine a QALICB’s “location. ” Recapture: In general, NMTC recapture occurs if the CDE goes out of compliance (i. e. , off mission) or the CDE receives principal during the initial seven-year credit period and fails to re-deploy in a timely manner. A QALICB bankruptcy does not affect NMTC availability. NMTC Pricing: NMTCs are “sold” for 70 - 80 cents per NMTC dollar. NMTC investors get their entire return from the purchase discount, generating “free” equity for the QALICB.

What Qualifies as a Low Income Census Tract (LIC)? A census tract in which: • the poverty rate is at least 20%; or • the median family income does not exceed 80% of the greater of statewide median family income or the metropolitan area median family income; or • additional areas including certain high migration rural areas, projects that serve targeted populations, and certain zones designated as Empowerment Zones by the Federal Government.

NMTC Pricing Example Project Cost $10 million X: NMTC Tax Credit Rate 39 percent NMTC Amount $3. 9 million X: NMTC Price 70 cents per NMTC Dollar NMTC Equity (Pre-Fees) $2. 73 million Note: The above example is based on a leveraged NMTC structure.

What are the investor’s incentives? • NMTC Investor can claim a tax credit against federal income tax (not AMT) • Credit can be claimed for a seven year period starting on the date the initial “Qualified Equity Investment” (QEI) is made with the Community Development Entity (CDE), and continuing on each subsequent anniversary • The total tax credit is 39% of the QEI – 5% of the QEI is paid in Years 1 -3 – 6% of the QEI is paid in Years 4 -7 • Unused NMTCs can be carried back 1 year and forward 20 years.

What are the developer’s incentives? • Projects that pose too much credit risk may become feasible through the inclusion of NMTC investor equity in the capital stack • Developers typically pay interest-only loan payments during the 7 -year compliance period with a balloon payment at the maturity • Key funds to capital stack - making debt service less expensive – a significant project subsidy • At times a non-profit may claim a significant developer fee

What are the lender’s incentives? • Credit under the Community Reinvestment Act (“CRA”) makes the deals particularly attractive to banks as a NMTC investor and/or leverage lender • Required loan amount is reduced by NMTC investor’s equity contribution • In addition to a pledge of membership or other capital interest, collateral can include personal guarantees and pledges of various state and local grants as well as campaign pledges.

Basic Leveraged NMTC Structure Leveraged Credit Structure: A tax credit investor can use borrowed money to fund QEI purchase. The IRS has issued a favorable ruling allowing leveraged NMTC structures. NMTC Investor Equity ($Y) $X Loan Proceeds NMTC Fund Equity (X+Y) Put/Call on Fund Equity CDE Fees Lender Pledge –CDE Sub Equity* CDE Sub X+Y Disbursement Account A Loan ($X) B Loan ($Y) Developer Entity (QALICB) *7 -Year Forbearnace

Lease Structure – Set Up Pledge Leasehold + Fund Notes* Lender Construction Contract Developer Operator Loan X+Y+Z NMTC Investor Fund Equity X+Y+Z CDE Parent CDE Sub Fees X+Y+Z Disbursement Account A Loan ($X) B Loan ($Y) C Loan ($Z) Developer Affiliate (QALICB) Construction Payment (X+Y+Z) Equity ($Z) Building Lease and Ground Sublease Put/Call on Fund Equity NMTC Investor $X Bond Proceeds Fund Loans A($X)/B($Y) Developer $Y Operator Monies Bond Proceeds ($X) *7 -Year Forbearnace Construction Trades

Lease Structure – Cash Flow Lender P&I Operating Cash Flow Developer QEI Distribution NMTC Investor Fund CDE Parent Fees CDE Sub End Loan Interest Developer Affiliate (QALICB) Building Rent Fund Loan Interest

Federal HTC Program Overview: The Historic Tax Credit (HTC) is a federal income tax credit for qualified rehabilitation expenditures (QREs) made to historic buildings. HTC Amount: The HTC amount equals the following percentage of QREs: (A) 20% in the case of a “certified historic structure” (e. g. , National Register) or (B) 10% in the case of a building dating from 1935 or earlier. Qualified Rehabilitation: Rehabilitation must (A) be certified the Secretary of the Interior in the case of a certified historic structure or (B) meet certain structural retention requirements in the case of a non-certified pre-1936 historic structure. HTC Accrual: The full HTC amount accrues in the year in which the rehabilitated building is placed in service. Recapture: In general, HTC recapture occurs if the building is transferred within five years of completion (including foreclosure).

Fed HTC Pricing Example Project Cost (QREs) $10 million X: HTC Tax Credit Rate 20 percent HTC Amount $2. 0 million X: HTC Price 70 cents per HTC Dollar HTC Equity (Pre-Fees) $1. 4 million

Massachusetts HTC Program Overview: The Massachusetts Historic Rehabilitation Tax Credit program is available competitively for income-producing buildings that are determined as a “qualified historic structure” by the Massachusetts Historical Commission, (MHC) and which are substantially rehabilitated and determined a certified rehabilitation. HTC Amount: Under the MHRTC program, up to 20 percent of the total qualified rehabilitation expenditures is returned to the owner in the form of a dollar-per-dollar credit on state income taxes. Rehabilitation expenditures need to meet or exceed 25% of the adjusted basis of the property. Qualified Rehabilitation: Rehabilitation must approved and certified by MHC. HTC Accrual: The full HTC amount accrues in the year in which the rehabilitated building is placed in service. Recapture: The credit may be subject to recapture if the taxpayer disposes of its interest in the structure within 5 years of being placed in service.

State HTC Pricing Example Project Cost $10 million X: HTC Tax Credit Rate 20 percent HTC Amount $2. 0 million X: HTC Price 88 cents per NMTC Dollar HTC Equity $1. 76 million

Basic Federal HTC Structure 5 Year Put/Call on HTC Investor LLC Interest HTC Investor HTC Equity Developer Owner Entity LLC Interest – 3% Preferred Return and HTC Pass-Through

Combined HTC/NMTC Structure NMTC Investor NMTC Equity ($Y) $X Loan Proceeds NMTC Fund Equity (X+Y) Put/Call on Fund Equity CDE Fees Lender Pledge –CDE Sub Equity* CDE Sub X+Y Disbursement Account A Loan ($X) B Loan ($Y) $Z HTC Equity Developer Entity (QALICB) *7 -Year Forebearance HTC Investor HTC Pass-Through

Why you go through the pain Project Cost $10 million NMTC Equity $2. 73 million Fed HTC Equity Amount $1. 40 million MA HTC Equity $1. 76 million Total Equity Contribution $5. 89 million Permanent Loan $4. 11 million

Give Your Project Adequate Time January – April: Produce plans and other prerequisites for shovel-ready project. Assemble team of professionals (tax council, financing, OPM, etc. ) Shop project to prospective leverage lenders. April – September: Shop project (with “soft” leverage lender commitments) to CDEs for inclusion in NMTC applications for Fall round. Applications for State and Federal HTCs October - December: Negotiate and close on NMTC financing, including leveraged loan. Approval of Federal HTCs and first tranche MAHTCs (reapply) January - April: Close transaction and start construction. Post Construction/COO – Complete Part 3 HTC application, sell MAHTCs.

Potentially Useful Resources/Contacts CFDI Fund Mapping Tool: https: //www. cdfifund. gov/Pages/mapping-system. aspx Epsilon Historic Tax Credit Consulting: https: //www. epsilonassociates. com/historic -resources Tax Credit Legal Council: https: //www. kleinhornig. com/professional/d_kolodner/ Mass. Development: https: //www. massdevelopment. com/ HTC Investor Services: https: //dorfmancapital. com/