Definitions of Listed Entity Public Interest Entity Mike

Definitions of Listed Entity & Public Interest Entity Mike Ashley Task Force Chair, IESBA Member IESBA Meeting November-December 2020 Virtual

Objectives of Session To consider TF views and proposals, with a view to approving proposed text for exposure Report-Back Overarching Objective List of PIE Categories Local Body Capacity to Refine Code Firms & Transparency Disclosure Other Matters Walk-through of 2 nd Read Page 2 | Proprietary and Copyrighted Information

Journey So Far… Sept 2019 Joint IESBA -IAASB Session Dec 2019 Mar 2020 Jun/Jul 2020 Sept 2020 IESBA & IAASB IESBA Project Approval Strawman Draft Preliminary Draft 1 st Read Nov 2020 IAASB Revised 1 st Read Dec 2020 IESBA 2 nd Read

Information Gathering Since September 2020 Joint CAG Session IAASB Meeting SMPAG Meeting Questionnaire to Additional PAOs Fo. F Questionnaire Page 4 | Proprietary and Copyrighted Information

Report-Back – Joint CAG and SMPAG Meetings Joint IESBA-IAASB CAG – Oct 2020 • Support for shared overarching objective • Some comments about the factors in determining level of public interest, new firm requirement to determine additional entities as PIEs and transparency disclosure • No new issues raised • All key comments addressed by the TF in the issues paper SMP Advisory Group – Nov 2020 • Supportive of the direction of travel • No new issues raised Page 5 | Proprietary and Copyrighted Information

Coordination with IAASB Strong coordination with IAASB at staff, TF and Board level • • 2 IAASB correspondent members 2 IAASB PIE sessions to date Use ED to gather info for IAASB Joint NSS and joint CAG sessions Page 6 | Proprietary and Copyrighted Information

Report-Back - IAASB November 2020 PIE Session Overarching Objective • Continued to support shared overarching objective for additional requirements of certain entities in both standards • Queries if “financial condition” in 400. 8 is too broad “Listed Entity” in IAASB Standards • Continued to support case by case approach which is consistent with a shared overarching objective • Need to consider any IESBA replacement for “listed entity” Transparency • Recognized importance of transparency • Preferred further analysis as part of its AR PIR Page 7 | Proprietary and Copyrighted Information

Overarching Objective for Additional Requirements Overarching Objective Both IAASB and IESBA are supportive of a common overarching objective for additional requirements (Proposed 400. 8 and 400. 9) Page 8 | Proprietary and Copyrighted Information

Overarching Objective for Additional Requirements Overarching Objective for additional requirements (Proposed 400. 8 and 400. 9) Significant public interest in the financial condition of certain entities Public confidence in those financial statements are important Confidence in their audits will enhance public confidence in those financial statements Additional requirements will enhance confidence in their audits which in turn will enhance confidence in those financial statements Page 9 | Proprietary and Copyrighted Information

Paragraphs 400. 8 and 400. 9 “Financial condition” in lead-in too broad, suggest terms such as “financial position”, “financial performance” TF responses - No change • Board considered “financial statement” too narrow and maybe perceived as focusing on investors only; more about financial well-being of an entity • Other terms do not sufficiently capture the Board’s view • 400. 8 sets up context for 400. 9 and R 400. 14 • Not felt appropriate to include ‘business activities’ in addition to ‘financial condition’ as potentially too broad given the focus on the role of the auditor Bullet #2 – is it necessary in light of bullets #1 and #6 TF responses - No change • Prudential regulation not restricted to financial markets Bullet #4 – “easily replaceable” unclear TF responses - Sought to clarify the language

Paragraphs 400. 8 and 400. 9 If there should be reference to independence requirements in 400. 9 TF responses • No change • Should be sufficiently clear from context, including extant 400. 1 and R 400. 11 • Facilitate use of the same wording by the IAASB in due course

Overarching Objective Do IESBA members: • Continue to support the use of the term “financial condition” in proposed 400. 8 • Agree with the TF’s view and proposed revisions to 400. 8 and 400. 9 Page 12 | Proprietary and Copyrighted Information

Definition of Public Interest Entity Broad Approach Recap A longer and more broadly defined list which local regulators and authorities can modify by tightening definitions, setting size criteria and adding new types of PIEs or exempting particular entities Role of Code Role of Local Bodies Role of Firms List of common PIE categories Refine the list as appropriate Determine to add to the list Page 13 | Proprietary and Copyrighted Information

Role of Code Role of Local Bodies")

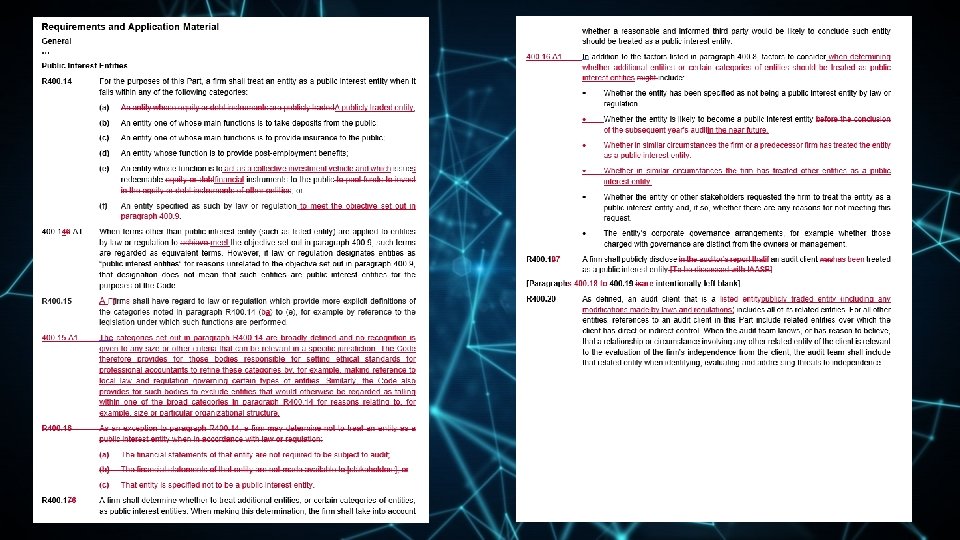

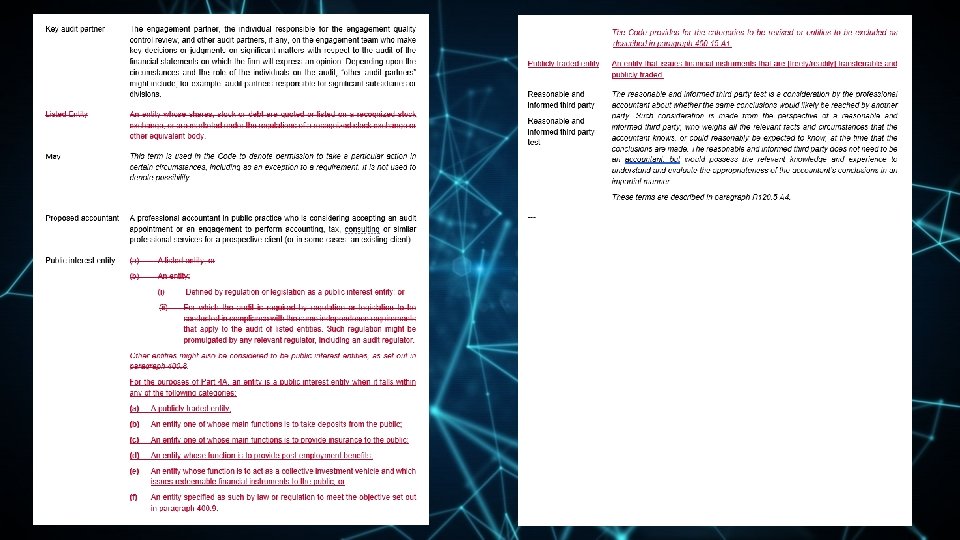

Expanded List of PIE Categories Category (a) Role of Code Role of Local Bodies Role of Firms • A new term - “publicly traded entity” • Uses the broader term “financial instruments” • Intention is to exclude entities where effective interests in their financial instruments are traded without their knowledge • [freely/readily] transferrable without limitation • “Publicly traded” still requires access to a public market trading mechanism, but broader than “listed • Replaces “listed entity” Category (e) • More succinctly describes investment funds available to the public Category (f) • Ties the definition of the entity to the overarching objective Publicly traded entity: “An entity that issues financial instruments that are [freely/readily] transferrable and publicly traded” Replacing Listed entity: “An entity whose shares, stock or debt are quoted or listed on a recognized stock exchange, or are marketed under the regulations of a recognized stock exchange or other equivalent body. ”

Expanded List of PIE Categories Do IESBA members agree with: • The introduction of the new term “publicly traded entity”, in paragraph R 400. 14, replacing “listed entity” in paragraph R 400. 20, and consequential deletion of the term “listed entity”? • The remaining proposed revisions to the list of PIE categories in paragraph R 400. 14? Page 15 | Proprietary and Copyrighted Information

Role of")

Definition of PIE Other Related Changes 400. 16 A 1 (First Read) Role of Code Role of Local Bodies • Moved to 400. 14 A 1 as it aligns better with R 400. 14 400. 15 A 1 • A new paragraph that aims to clarify the high-level nature of the Code’s categories and the role of the local bodies R 400. 16 (First Read) • Deleted as no longer warranted Role of Firms Page 16 | Proprietary and Copyrighted Information

Definition of PIE Other Related Changes Do IESBA members agree with: • The new paragraph 400. 15 A 1 • Deletion of R 400. 16 (First Read) Page 17 | Proprietary and Copyrighted Information

Expected Role of Local Bodies Role of Code Role of Local Bodies Current Approach • Proposed definition needs to be refined as appropriate at local level because of its high-level nature • If not, the new definition might inadvertently scope in the wrong entities or not scope in others where appropriate Recap Concern Role of Firms • Some local bodies do not have capacity to refine the highlevel definition or simply adopt it as is Page 18 | Proprietary and Copyrighted Information

Expected Role of Local Bodies PAO Questionnaire Role of Code • • Role of Local Bodies • • • Role of Firms In collaboration with IFAC’s Quality & Development team Questionnaire circulated to about 50 PAOs in July-October v Mostly smaller and less developed jurisdictions including francophone African jurisdictions 25+ responses received as of mid-November Strong indication from responses that refinement of the PIE definition can be achieved at these jurisdictions TF will continue to socialize the proposals with local bodies across jurisdictions as part of its outreach activities in 2021 Page 19 | Proprietary and Copyrighted Information

Expected Role of Local Bodies Mitigation Strategy Role of Code List of factors in 400. 8 • For consideration by local bodies Longer transition period Role of Local Bodies • At least 18 months • Board discussion on NAS/Fees/ PIE effective date to come Outreach activities Role of Firms • Include non-authoritative guidance material • Better understanding of Board approach & rationale • Commences Q 1 Page 20 | Proprietary and Copyrighted Information

Expected Role of Local Bodies Any Comment? Page 21 | Proprietary and Copyrighted Information

Role of Firms Role of Code Role of Local Bodies Role of Firms 2 New Requirements • Determination if additional entities should be PIEs • Transparency disclosure Page 22 | Proprietary and Copyrighted Information

Role of Firms Role of Code Role of Local Bodies Role of Firms Firm Determination (R 400. 16, 400. 16 A 1) • Firm to determine if additional entities should be treated as PIEs v Elevated AM in Extant to requirement v General support from stakeholders to date • Revisions from 1 st Read v Moved the additional list of factors to a new paragraph as AM v Revised bullet #2 to make timing less specific v Added 2 new factors (bullets #3 and #4) relating to treatments of entities in similar circumstances Page 23 | Proprietary and Copyrighted Information

Role of Firms Do IESBA members agree with: • Revisions to R 400. 16 and 400. 16 A 1 Page 24 | Proprietary and Copyrighted Information

Role of Firms Transparency Disclosure Role of Code Role of Local Bodies Role of Firms Transparency Disclosure • • • First Read (R 400. 18) proposed new requirements for firms to publicly disclose in auditor’s report if an audit client was treated as PIE At its July 2020 meeting, mixed feedback from IAASB about such disclosure in auditor’s report At its November 2020 meeting, IAASB considered 3 options Page 25 | Proprietary and Copyrighted Information

Role of Firms Transparency Disclosure Role of Code Role of Local Bodies Role of Firms Option 1 Option 2 Option 3 No change to auditor’s report Consider as part of AR PIR Explore ISA 700. 28 (c) revision • Majority of IAASB members support Option 2 v Further review under the PIR allows IAASB to properly consider Option 3 v IAASB recognized that transparency is an essential component of the Task Force’s proposals v IAASB agreed that IESBA should seek views from stakeholders about the options • PIOB Observer reinforced PIOB’s view that it is in the public interest to enhance transparency Page 26 | Proprietary and Copyrighted Information

Role of Firms Transparency Disclosure Role of Code In light of IAASB responses, TF: • Proposes to revise the requirement to a more general requirement without stating how the disclosure should be made Role of Local Bodies Role of Firms • Intends to seek feedback from stakeholders as to the preferred method of disclosure, including potentially on examples from the IAASB Page 27 | Proprietary and Copyrighted Information

Role of Firms Transparency Disclosure Do IESBA members agree with: • The proposed revisions to R 400. 17 • Recommendation to seek further input from stakeholders about how such disclosure could be made Page 28 | Proprietary and Copyrighted Information

Other Matters Related Entity Part 4 B of the Code Page 29 | Proprietary and Copyrighted Information

Other Matters Related Entity Whether the definition of audit client that is a listed entity in paragraph R 400. 20 should be extended to all PIE audit clients Sept-Oct 2020 meeting Fo. F Questionnaire Oct 2020 • • • Related Entity IESBA discussed if any philosophical barriers to extend the definition as well as other reasons such as corporate structures and flow of information within certain groups IESBA agreed complexity of the issue and agreed further research is necessary but likely outside the scope of the PIE project Received 5 responses, consistent with IESBA discussions. Key comments: v Difficult to obtain information for some corporate structures vs listed entity v Can be costly and labor-intensive work, for firms and client, without much benefit from an independence perspective v If definition of audit client is changed, IESBA should consider some level of best effort as well as the need for longer transition period v No objection to replacing listed entity with new subparagraph (a) in R 400. 14 v Supportive of a new IESBA project to review group corporate structures Page 30 | Proprietary and Copyrighted Information

Other Matters Related Entity Whether the definition of audit client that is a listed entity in paragraph R 400. 20 should be extended to all PIE audit clients TF Recommendations • The definition of audit client in R 400. 20 be reviewed as a separate IESBA workstream, considering: v If any philosophical reason not to extend and other reasons v Impact on independence standards v If the definition of “related entity” should be revised Related Entity v Relevant requirements in major jurisdictions • “Listed entity” in R 400. 20 be replaced with “publicly traded entity” Page 31 | Proprietary and Copyrighted Information

Other Matters Part 4 B of the Code • Project scope includes: v Implications for Part 4 B of the Code will be taken into account and addressed • TF view - Revisions to Part 4 B not necessary: Part 4 B v Greater public interest in some assurance engagement has at least as much to do with the nature of the engagement as to the nature of the entity v Not all assurance engagements for a PIE would be of significant public interest v Some assurance engagements for a non-PIE might be of significant public interest v “Public interest assurance engagements” is outside this project’s scope Page 32 | Proprietary and Copyrighted Information

Other Matters Do IESBA members agree with: • TF’s recommendation for a new workstream on related entity • The proposed revisions to R 400. 20 • TF view’s that no adjustments to Part 4 B are required as a result of this project Page 33 | Proprietary and Copyrighted Information

Use of Listed Entity and PIE in ISAs • IAASB preferred a case-by-case approach in determining whether PIE or a subset of PIE v Maybe compelling reasons to retain “listed entity” without being inconsistent with a common overarching objective v Allow for consideration of any unintended consequences v Listed entities are referred to throughout ISAs and ISQMs • IAASB agreed to use IESBA ED process to get initial input from IAASB stakeholders v Make sure there is the right messages and communication from IAASB Page 34 | Proprietary and Copyrighted Information

Use of Listed Entity in ISAs and ISQM 1 Any Comment? Page 35 | Proprietary and Copyrighted Information

")

Walk Through nd 2 Read (Mark-up from 1 st Read)

Part 4 A

Consequential & Conforming Amendments

Next Steps 12/4 Review turnaround version Approve proposed text for exposure 12/8 Effective date options discussion Page 41 | Proprietary and Copyrighted Information

The Ethics Board www. ethicsboard. org 42

- Slides: 42