Decisions Under Risk and Uncertainty Risk vs Uncertainty

of a probability distribution is: Where Xi")

for more risk averse")

- Slides: 45

Decisions Under Risk and Uncertainty

Risk vs. Uncertainty • Risk – Must make a decision for which the outcome is not known with certainty – Can list all possible outcomes & assign probabilities to the outcomes • Uncertainty – Cannot list all possible outcomes – Cannot assign probabilities to the outcomes

Measuring Risk Probability Distributions • Probability – Chance that an event will occur • Probability Distribution – List of all possible events and the probability that each will occur – probability distribution is essential in evaluating and comparing investment projects • Expected Value or Expected Profit

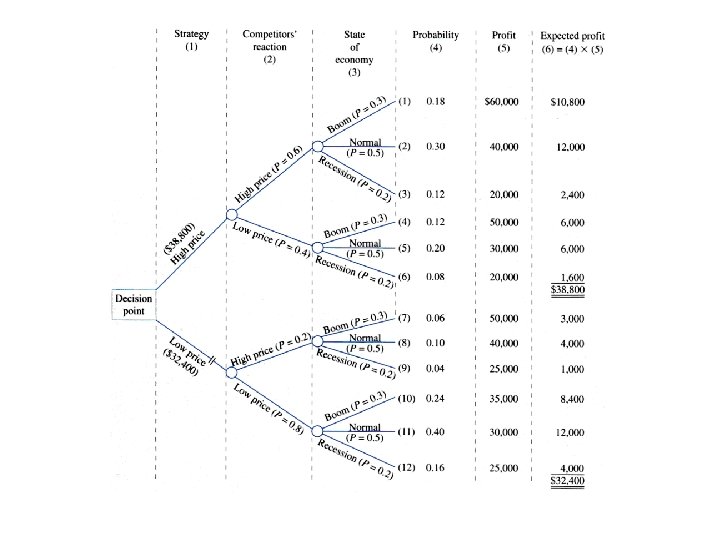

Probability Distribution for Sales

Expected Value • Expected value (or mean) of a probability distribution is: Where Xi is the ith outcome of a decision, pi is the probability of the ith outcome, and n is the total number of possible outcomes

Measuring Risk Probability Distributions Calculation of Expected Profit Expected profit of an investment is the weighted average of all possible profit levels that can result from the investment under the various state of the economy, with the probability of those outcomes or profits used as weights.

Expected Value • Does not give actual value of the random outcome – Indicates “average” value of the outcomes if the risky decision were to be repeated a large number of times

Variance • Variance is a measure of absolute risk – Measures dispersion of the outcomes about the mean or expected outcome • The higher the variance, the greater the risk associated with a probability distribution

Measuring Risk Probability Distributions Calculation of the Standard Deviation Project A

Measuring Risk Probability Distributions Calculation of the Standard Deviation Project B

Identical Means but Different Variances

Standard Deviation • Standard deviation is the square root of the variance • The higher the standard deviation, the greater the risk

Probability Distributions with Different Variances

Coefficient of Variation • When expected values of outcomes differ substantially, managers should measure riskiness of a decision relative to its expected value using the coefficient of variation – A measure of relative risk

Decisions Under Risk • No single decision rule guarantees profits will actually be maximized • Decision rules do not eliminate risk – Provide a method to systematically include risk in the decision making process

Which Rule is Best? • For a repeated decision, with identical probabilities each time – Expected value rule is most reliable to maximizing (expected) profit – Average return of a given risky course of action repeated many times approaches the expected value of that action

Expected Utility Theory • Actual decisions made depend on the willingness to accept risk • Expected utility theory allows for different attitudes toward risk-taking in decision making – Managers are assumed to derive utility from earning profits

Expected Utility Theory • Managers make risky decisions in a way that maximizes expected utility of the profit outcomes • Utility function measures utility associated with a particular level of profit • Index to measure level of utility received for a given amount of earned profit

Manager’s Attitude Toward Risk • Determined by the manager’s marginal utility of profit: • Marginal utility (slope of utility curve) determines attitude toward risk

Manager’s Attitude Toward Risk • Risk averse – If faced with two risky decisions with equal expected profits, the less risky decision is chosen • Risk loving – Expected profits are equal & the more risky decision is chosen • Risk neutral – Indifferent between risky decisions that have equal expected profit

Manager’s Attitude Toward Risk • Can relate to marginal utility of profit • Diminishing MUprofit – Risk averse • Increasing MUprofit – Risk loving • Constant MUprofit – Risk neutral

Manager’s Attitude Toward Risk

Manager’s Attitude Toward Risk

Manager’s Attitude Toward Risk

Adjusting Value for Risk • Value of the Firm = Net Present Value r is appropriate discount rate We will extend this model to deal with an investment project subject to risk. Two commonly used methods. 1 Risk-Adjusted Discount Rate 2 Certainty Equivalent Approach

Risk-Adjusted Discount Rate This reflects the managers /investors trade off between risk and return. Risk measured by the SD of profits/returns The risk return trade off function of indifference curve ( R) shows that the manager is indifferent among a 10 % rate of return on a riskless asset with SD = 0 ( point A) 20% rate of return with SD =1 (Point C) 32% with SD 1. 5 (point D) Difference between the expected rate of return on risky project and riskless project is called risk premium on risky investment Risk –return trade off function ( R) shows that risk premium of 4% is required to compensate for the level of risk given by SD = 0. 5 Similarly 10% premium required for an investment with SD =1. 0

Adjusting Value for Risk

The risk return trade off curve would be steeper (R’) for more risk averse manager and less steep (R’’) for a less risk averse manager. More risk –averse manager facing R’ would require a premium of 22%(c’) for project with SD=1, while a less risk –averse manager with R’’ would require a risk premium of only 4% for the same investment

R= net cash flow or return C= initial cost of investment Project is undertaken if its NPV greater than or equal to zero, or larger than that for an alternative project

There is a project with expected net cash flow /return 45, 000 for the next five years and initial cost 100, 000. Risk adjusted discount rate is 20% Then , we have If firm perceived this as much risky project and used 32% as k its NPV would be

Adjusting Value for Risk Certainty Equivalent Approach Certainty Equivalent Coefficient This modifies the numerator of the valuation model Here R is risky net cash flow r is risk free discount rate α is certainty equivalent coefficient The investor must specify the certain sum that yields to him same utility or satisfaction of the expected risky sum from the investment. The value of α ranges from 0 to 1. 0 means too risky project 1 means risk free project

If the manager regarded the sum of 36000 with certainty as equivalent to the expected (risky) net cash flow of 45000 per year for the next five years therefore α = 36000/45000= 0. 8 Take 10% as risk free discount rate Then NPV would be If firm perceived this as much more risky and applied 0. 62 as certainty equivalent coefficient the NPV would be 5, 763. 32. These answers are closed to those under previous method

Manager’s Utility Function for Profit

Expected Utility of Profits • According to expected utility theory, decisions are made to maximize the manager’s expected utility of profits • Such decisions reflect risk-taking attitude – Generally differ from those reached by decision rules that do not consider risk – For a risk-neutral manager, decisions are identical under maximization of expected utility or maximization of expected profit

Decisions Under Uncertainty • With uncertainty, decision science provides little guidance – Four basic decision rules are provided to aid managers in analysis of uncertain situations

Summary of Decision Rules Under Conditions of Uncertainty Maximax rule Identify best outcome for each possible decision & choose decision with maximum payoff. Maximin rule Identify worst outcome for each decision & choose decision with maximum worst payoff. Minimax regret rule Determine worst potential regret associated with each decision, where potential regret with any decision & state of nature is the improvement in payoff the manager could have received had the decision been the best one when the state of nature actually occurred. Manager chooses decision with minimum worst potential regret. Equal probability rule Assume each state of nature is equally likely to occur & compute average payoff for each. Choose decision with highest average payoff.

• Decision Trees – Sequence of possible managerial decisions and their expected outcomes – Conditional probabilities

Uncertainty • Maximin Criterion – Determine worst possible outcome for each strategy – Select the strategy that yields the best of the worst outcomes

Uncertainty: Maximin The payoff matrix below shows the payoffs from two states of nature and two strategies.

Uncertainty: Maximin The payoff matrix below shows the payoffs from two states of nature and two strategies. For the strategy “Invest” the worst outcome is a loss of 10, 000. For the strategy “Do Not Invest” the worst outcome is 0. The maximin strategy is the best of the two worst outcomes - Do Not Invest.

Uncertainty: Minimax Regret The payoff matrix below shows the payoffs from two states of nature and two strategies.

Uncertainty: Minimax Regret The regret matrix represents the difference between the given strategy and the payoff of the best strategy under the same state of nature.

Uncertainty: Minimax Regret For each strategy, the maximum regret is identified. The minimax regret strategy is the one that results in the minimum value of the maximum regret.

Uncertainty: Informal Methods • • Gather Additional Information Request the Opinion of an Authority Control the Business Environment Diversification