Dealing with an Credit Crunch Past Lessons New

analyses policy responses to sudden stops episodes of the")

Expansionary Policies can Help § Characterizing expansionary fiscal policy Observed Fiscal Impulse Structural")

Expansionary Policies can Help § Monetary Policy Dilemmas and Taylor Rules. § Conjecture:")

Expansionary Policies can Help Fiscal Policy Monetary Policy (GDP variation and Structural Fiscal")

Initial conditions matter § Stringent preconditions need to be met in order to")

Initial Conditions are not Destiny § Peru’s policy of reserve accumulation and disbursement")

Initial Conditions are not Destiny § Brazil: selective use of international reserves to")

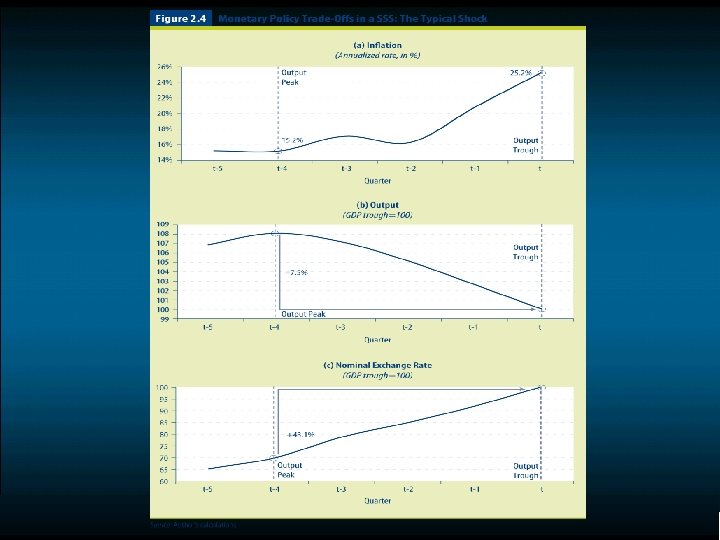

Shock Persistence is Key § Vodka is stronger than Tequila")

External financial packages are essential when initial conditions do not help. § Mexico")

§ Redefine the emphasis of multilateral support. Multilaterals should not")

Refinancing Public Debt Stocks")

Initial Conditions Matter ?")

- Slides: 29

Dealing with an Credit Crunch: Past Lessons, New Challenges Eduardo A. Cavallo Inter-American Development Bank (IDB) Reforming the Bretton Woods Institutions, Copenhagen, 16 -17 September 2009

Outline § Lessons from past financial crisis: the experience of LAC. § Applying the past to the present.

Lessons Learned § IDB (2009) analyses policy responses to sudden stops episodes of the late 1990 s for 8 LAC countries, bringing in also cross-country analysis. 1) Expansionary fiscal and monetary policy that does 2) 3) 4) 5) not affect credibility or solvency can reduce output collapse in the aftermath of a sudden stop. However countries need to be able to afford these policies. Initial conditions matter. Initial conditions are not destiny. The persistence of the shock is key. External financial packages are essential when initial conditions do not help.

1) Expansionary Policies can Help § Characterizing expansionary fiscal policy Observed Fiscal Impulse Structural Fiscal Impulse % PBI Source: Ortiz, Ottonello, Sturzenegger and Talvi (Chapter 2) % PBI

1) Expansionary Policies can Help § Monetary Policy Dilemmas and Taylor Rules. § Conjecture: in Emerging Markets’ prone to financial crises, Central Banks care about: § Inflation § Output Gap § Nominal Exchange Rate (“original sin” & “fear of floating”) § Anatomy of financial crises in Emerging Markets.

1) Expansionary Policies can Help Fiscal Policy Monetary Policy (GDP variation and Structural Fiscal impulse partialling out the effects of monetary policy) (GDP variation and Monetary Policy Regime index partialling out the effects of fiscal policy) Source: Ortiz, Ottonello, Sturzenegger and Talvi (Chapter 2)

2) Initial conditions matter § Stringent preconditions need to be met in order to afford policy flexibility: § Fiscal Policy: fiscal policy rules that guarantee inter- temporal consistency; maintaining low levels of public debt. § Monetary policy: maintaining low levels of financial and debt dollarization; high degree of credibility in the policy framework; trade openness in a context of open capital markets. § Evidence shows that those that were better prepared did better during the crisis.

3) Initial Conditions are not Destiny § Peru’s policy of reserve accumulation and disbursement Domestic Liability Dollarization: Selected LAC Countries Domestic Liability Dollarization Measure Before the Crisis Net Domestic Liability Dollarization Measure Before the Crisis COL CHL COL BRA ECU PER MEX ECU ARG PER MEX URY 0. 0% 10. 0% 20. 0% 30. 0% % of GDP 40. 0% 50. 0% 60. 0% -30. 0% -20. 0% -10. 0% 20. 0% 30. 0% 40. 0% 50. 0% % of GDP

3) Initial Conditions are not Destiny § Brazil: selective use of international reserves to finance trade credit. § Chile: the capacity to switch gears without generating a crisis. § Colombia: fear of floating

4) Shock Persistence is Key § Vodka is stronger than Tequila

5) External financial packages are essential when initial conditions do not help. § Mexico 1994: $51 billion IMF/USA rescue package. § 2. 8 times the total stock of short-term US$ debt by December 2004. § Argentina 2001/2002. § There is reason to believe that with international support, the restructuring process could have been much more orderly.

The Great Crisis of 2008/2009 § ¿What is different this time around? § The epicenter of the crisis: center vs. perifery. § Countries in the LAC region appear to be better prepared. But: will it be enough? § This time around, the initial response of countries in the region has been strongly countercyclical, just like in the developed world. § But unlike the developed world, LAC is not a safe haven for global savings that can provide billions of dollars to pump into a stimulus package. § Precarious market access.

Coordinators Alejandro Izquierdo, IDB Ernesto Talvi, CERES

Outlook for LAC in the context of the crisis § It makes all the difference if the world economy reaches its pre-crisis levels of industrial production in 2010 or in 2013. § This scenario could trigger a liquidity crisis in quite a few countries. If a country does not have sufficient international reserves to cover the debt service, it could generate a stampede by everyone who believes that the reserves are not going to be there when needed.

The Role of Multilaterals § Precarious access to credit markets for many emerging market governments calls for multilaterals to step in and play a key role as a lenders (and borrowers)-of-last resort, akin to the role that credible governments, such as the US government, play domestically. § The question then is not whether multilaterals should play a key role in the current crisis, but which is the most effective way to channel their intervention and at what financial cost.

Policy Principles § Strengthen the role of multilateral institutions. Multilateral support will be vital under precarious access to credit markets. § Move away from short-term financing. Multilaterals should avoid short-term emergency financing and only consider medium to longterm financing in order to partially “complete” markets in terms of maturities.

Policy Principles (cont. ) § Redefine the emphasis of multilateral support. Multilaterals should not only provide medium to long-term financing for fiscal stimulus –when fiscal sustainability is not at stake– but more importantly, they should provide for long-term refinancing of maturing debt obligations. § Ensure that countries work towards sustainable fiscal policy while strengthening social protection. Multilateral support should be complemented with incentive-compatible conditionality, to ensure fiscal sustainability and strengthen social protection.

ILR Dynamics Under Alternative Policies (LAC-7, L-Shaped Scenario, ILR 2) Refinancing Public Debt Stocks vs. Financing Fiscal Deficits 125% Normal International Financial Conditions 120% 115% 110% 105% 100% 95% Full Financing of Flows and Precarization of Stocks 90% 85% Precarization of Flows and Stocks 80% 75% 2008 2009 2010 2011 2012 LAC-7 is the simple average of the seven major Latin American countries, namely Argentina, Brazil, Chile, Colombia, Mexico, Peru and Venezuela. These countries represent 91% of Latin America’s GDP. ILR 2 t = Reservest / (Public Debt Amortizationst+1 + Short Term Private External Debt Amortizations) Source: IDB (2009) Policy-trade-off for Unprecedented Times: Confronting the Global Crisis in LAC. A. Izquierdo and E. Talvi, coordinators.

Concluding Remarks § A strategy by the IMF and multilaterals that only pays attention to financing countercyclical fiscal policies is incomplete and ignoring the impact of expansionary policy on liquidity ratios can be a costly mistake. § It is necessary that lender (and borrower)-of-last -resort functions, similar to those that governments perform in developed economies, be recreated for LAC by multilateral institutions, so that liquidity concerns are kept at bay.

Concluding Remarks § Recent responses: § IMF´s Flexible Credit Line § IDB´s Growth Facility

Thank You

2) Initial Conditions Matter ?

Fiscal Position Under Two Hypotheses on the Global Economy: Are Debt Dynamics Sustainable? Fiscal Balance Public Debt (LAC-7, % of GDP) 2% (LAC-7, % of GDP) 53% 1. 6% 49% 1% 0. 3% 48% L-Shaped Scenario 0% 43% V-Shaped Scenario -1% -2% 38% -2. 6% V-Shaped Scenario -3% -3. 7% 34% 33% L-Shaped Scenario -4% -5. 0% 28% -5% 27% -6% 23% 2006 2007 2008 2009 2010 2011 2012 2013 LAC-7 is the simple average of the seven major Latin American countries, namely Argentina, Brazil, Chile, Colombia, Mexico, Peru and Venezuela. These countries represent 91% of Latin America’s GDP. Source: IDB (2009) Policy-trade-off for Unprecedented Times: Confronting the Global Crisis in LAC. A. Izquierdo and E. Talvi, coordinators.

Latin America: Monetary and Fiscal Policy Response Fiscal Stimulus Announcements in Latin America Monetary Policy (LAC-7*, Interbank interest rate and Nominal Exchange Rate, in % and Sep-15 -08=100) (% of GDP) 126 9. 9% ON - BUDGET OFF – TOTAL BUDGET Revenue-side Expenditure-side 122 9. 7% Interest Rate 9. 5% 114 9. 3% 110 9. 1% 106 8. 9% Exchange Rate Argentina 5. 1 0. 2 1. 1 6. 4 Brazil 0. 3 0. 1 3. 3 3. 6 Chile 1. 0 1. 1 0. 7 2. 8 Mexico 0. 5 1. 0 0. 0 1. 5 Peru 0. 0 1. 4 1. 1 2. 5 Source: Credit Suisse 102 Interest Rate 8. 7% Exchange Rate 118 8. 5% 98 Sep-08 Oct-08 Nov-08 Dec-08 Jan-09 Feb-09 LAC-7 is the simple average of the seven major Latin American countries, namely Argentina, Brazil, Chile, Colombia, Mexico, Peru and Venezuela. These countries represent 91% of Latin America’s GDP. *Excludes Argentina and Venezuela Source: IDB (2009) Policy-trade-off for Unprecedented Times: Confronting the Global Crisis in LAC. A. Izquierdo and E. Talvi, coordinators.

Monetary and Fiscal Policy Response: Russian Crisis vs. Current Crisis Monetary Policy Fiscal Policy (LAC-7, Structural Fiscal Balance, % of GDP) 40% 118 38% 116 36% 114 Interest Rate 34% 112 32% 110 30% 108 28% 106 26% 104 Exchange Rate 24% 0. 0% -0. 5% -1. 0% Exchange Rate -1. 2% -1. 5% -2. 0% -2. 5% 102 -3. 0% Sep-99 Jun-99 Mar-99 Dec-98 Sep-98 Jun-98 Aug-98 Mar-98 Jul-98 -3. 5% Dec-97 98 Sep-97 20% Russian Crisis -3. 2% Jun-97 100 Mar-97 22% Dec-96 Interest Rate (LAC-7*, Interbank Interest Rate and Nominal Exchange Rate, in % and Jul-98=100) LAC-7 is the simple average of the seven major Latin American countries, namely Argentina, Brazil, Chile, Colombia, Mexico, Peru and Venezuela. These countries represent 91% of Latin America’s GDP. *Excludes Argentina and Venezuela Source: IDB (2009) Policy-trade-off for Unprecedented Times: Confronting the Global Crisis in LAC. A. Izquierdo and E. Talvi, coordinators.

The End of the Panglossian Period: International Financial Conditions Corporate Bond Spreads Corporate Bonds: Issuance (Latin CEMBI; 01 -Jan-07 = 100) (LAC-7, billions of USD) 25 Variation in bps 900 800 Jan-07 Jan. 07 May. 08 CEMBI 221 Jun. 08 Mar. 09 Total 06 -Mar-09 516 603 824 87 21. 2 20 700 600 15 500 400 10 300 200 5 2. 5 100 Mar-09 Dec-08 Sep-08 Jun-08 Mar-08 Dec-07 Sep-07 Jun-07 Mar-09 Jan-09 Nov-08 Sep-08 Jul-08 May-08 Mar-08 Jan-08 Nov-07 Sep-07 Jul-07 May-07 0 Mar-07 Jan-07 0 Source: IDB (2009) Policy-trade-off for Unprecedented Times: Confronting the Global Crisis in LAC. A. Izquierdo and E. Talvi, coordinators.

External Factors: International Financial Conditions Sovereign Bonds: Maturity Sovereign Bonds: Issuance (LAC-7, issuances with maturity less than 1 year, % of total issuance) (LAC-7, billions of USD) 100 97. 8 65% 63. 3% 60% 90 55% 80 50% 45% 70 40% 60 56. 6 35% 28. 6% 30% 50 LAC-7 is the simple sum of the seven major Latin American countries, namely Argentina, Brazil, Chile, Colombia, Mexico, Peru and Venezuela. These countries represent 91% of Latin America’s GDP. Source: IDB (2009) Policy-trade-off for Unprecedented Times: Confronting the Global Crisis in LAC. A. Izquierdo and E. Talvi, coordinators. Mar-09 Dec-08 Sep-08 Jun-08 Mar-08 Dec-07 Sep-07 Jun-07 Mar-09 Dec-08 20% Sep-08 Jun-08 Mar-08 Dec-07 Sep-07 Jun-07 Mar-07 40 Mar-07 25%