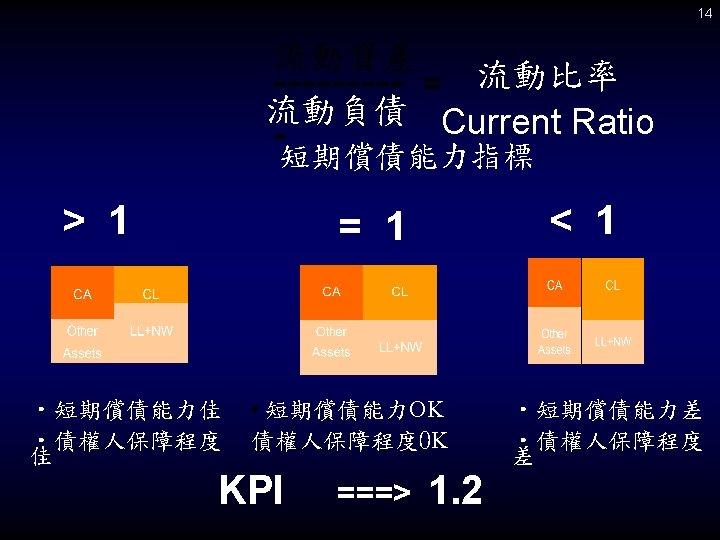

Current ratio 1 Current ratio Current assets Current

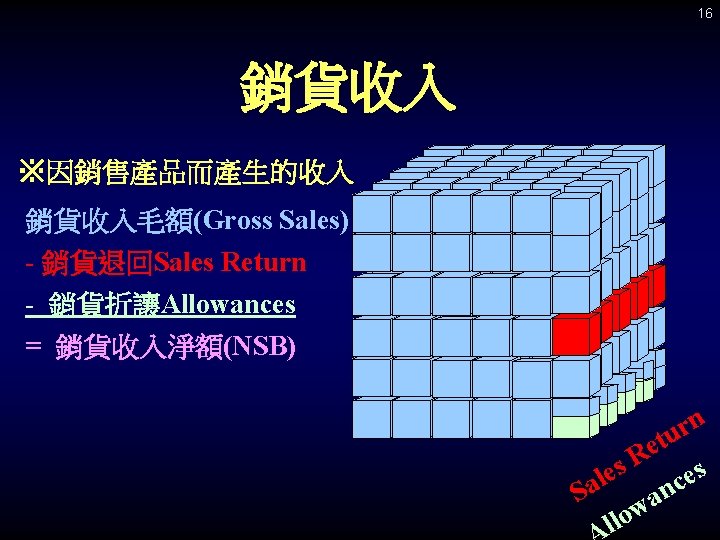

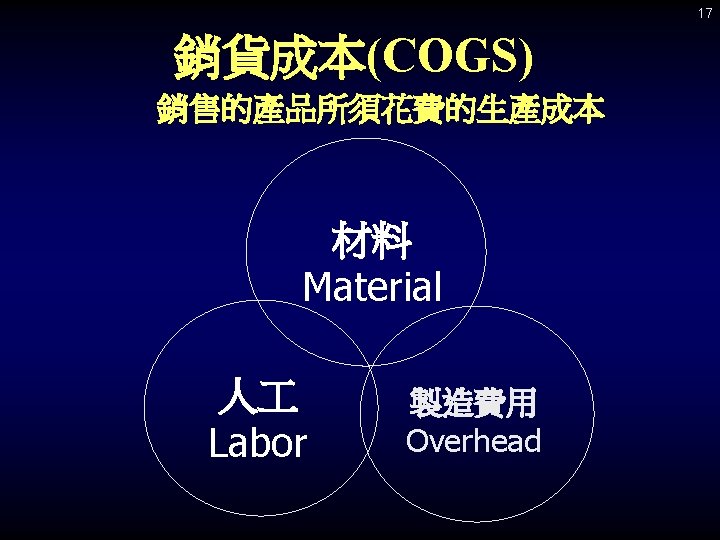

淨銷貨收入NSB(Net Selling Billion) -銷貨成本COGS(Cost of Goods Sold) = 銷貨毛利GPM(Gross")

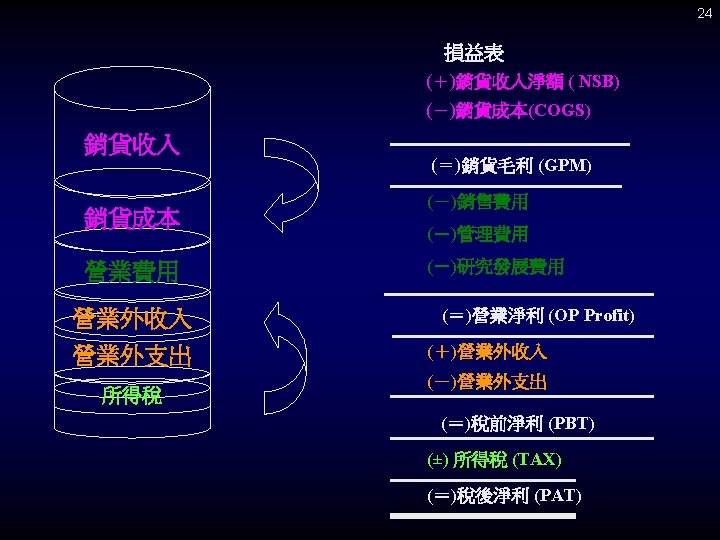

= 銷貨毛利GPM(Gross profit Margin) -營業費用(Operating Expenses) =營業淨利(Operating Profit)")

• NSB/Capital : Capital")

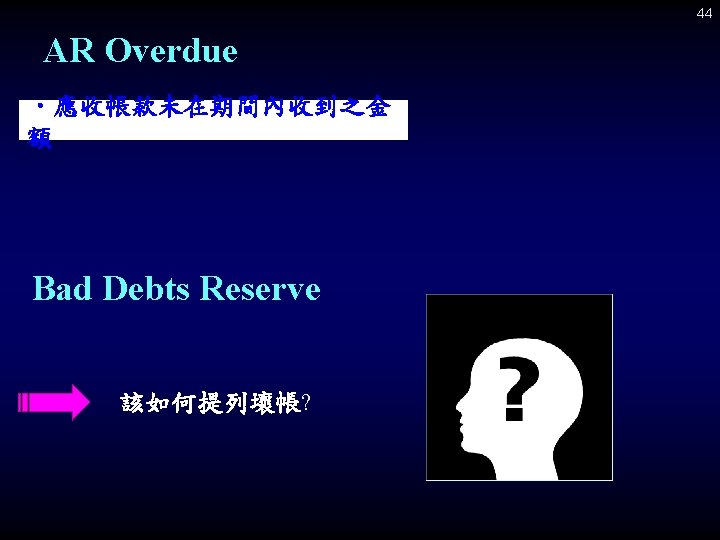

A/R Aging Reserve % Current 0% -- Overdue --")

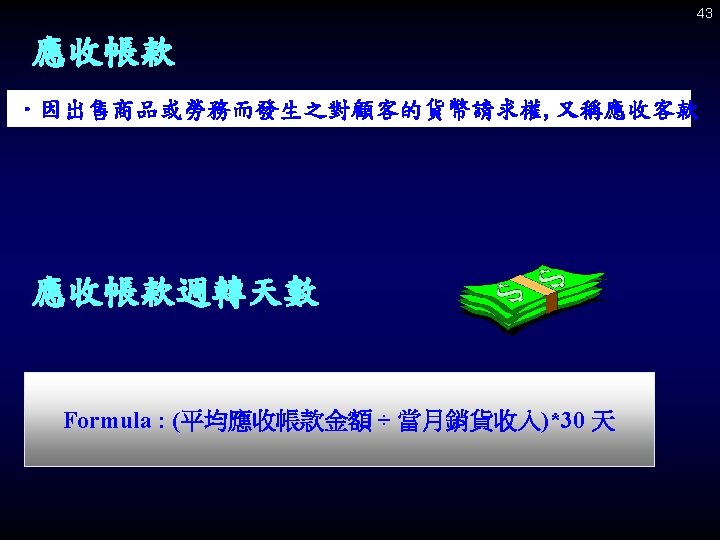

NSB / NUB : Net sales billing , Net")

投入資本報酬率 使用公司多少的資源? 替公司賺取多少的報酬? 賺取的報酬 ROIC= Adjusted operating profit")

- Slides: 63

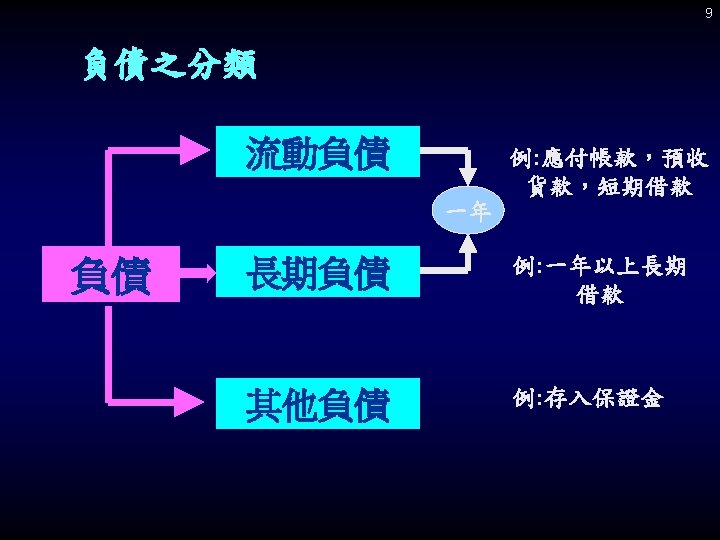

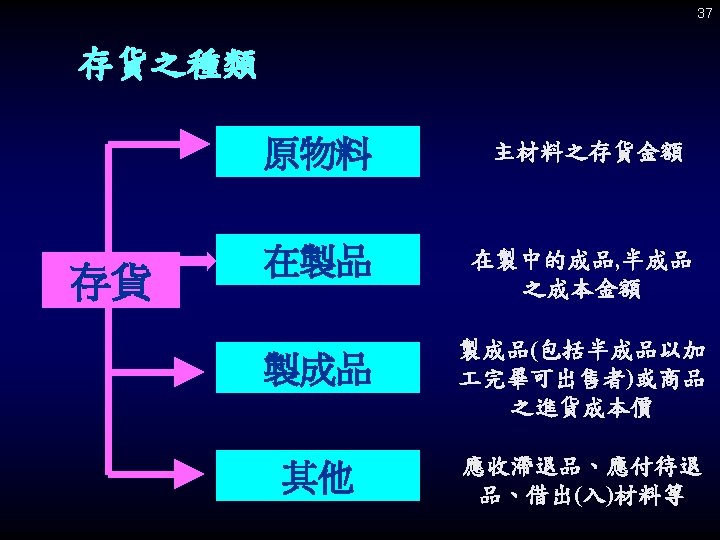

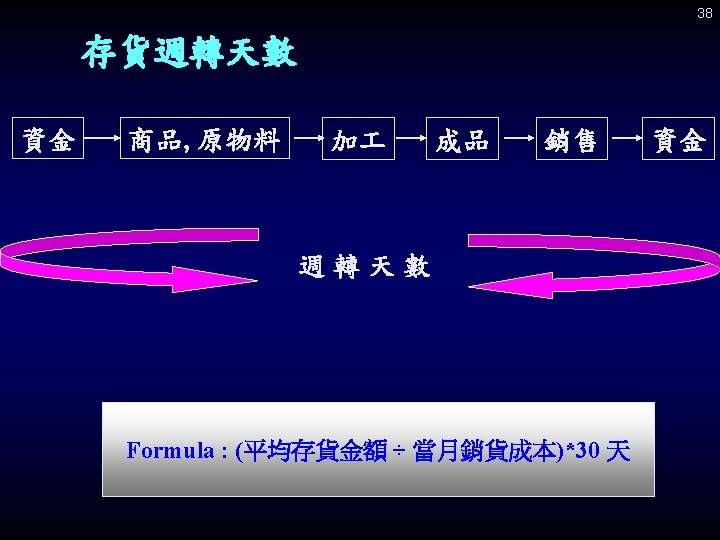

Current ratio 1. Current ratio = Current assets/ Current Liability Normal = 120% Better : 150% 2. Working Capital = A/R + Inventory - A/P If A/R + Inventory > A/P A/R : too long / overdue Inventory : Process , JIT , Idle , Business model ---- Cash out / loan exposure ** Focus on CCC management 13

15 Leverage = Total liability / Equity Normal = 1 Better = 0. 8 If : Total liability > Equity - Working capital out of control - P & L contribution can not support capital expenditure -- ROA - Long term investment is not efficiency -- ROI --- Cash out / loan exposure Focus on : ROA & ROI

21 銷貨毛利GPM (Gross profit margin) 淨銷貨收入NSB(Net Selling Billion) -銷貨成本COGS(Cost of Goods Sold) = 銷貨毛利GPM(Gross profit Margin)

22 營業淨利(Operating Profit) = 銷貨毛利GPM(Gross profit Margin) -營業費用(Operating Expenses) =營業淨利(Operating Profit)

29 Cash Flow 9 8 Finish Goods WIP OVHD Credit Control Material purchase on credit 6 3 2 Accrued Wages 7 Fixed Assets 10 Capex AR Collection 11 5 PIC, RE Equity AP 1 Cash 14 15 dividen d Tax 4 13 Interest 12 Leverag e Liability

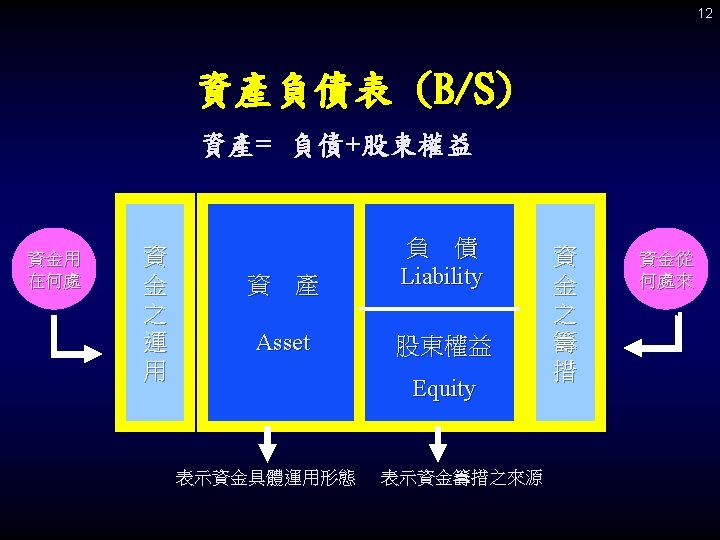

31 財務名詞簡介 Financial Structure Operation Performance Financial KPI Operation Efficiency People Productivity

32 Financial Structure Credit Control Banking 1. Current Ratio ≧ 1 2. Debt Service Ratio ≧ 1. 5 3. Interest Coverage Ratio ≧ 1. 25 4. Leverage Ratio ≦ 1. 33 Formula 1. 2. 3. Current Ratio = 〔流動資產 ÷ 流動負債〕 Debt Service Ratio = 〔(稅前利益+利息費用+折舊及攤提)÷(利息費用+長期負債一年內到期部分) 〕 Interest Coverage Ratio = 〔(稅前利益+利息費用)÷ 利息費用〕

33 Operation Performance NSB Growth • NSB Growth (YOY/ MOM) • NSB/Capital : Capital turnover (YOY: 與去年同期比較) (MOM: 與上個月比較) GPM % • Gross Profit Margin % OP profit % PBT% • OP Profit % • PBT % ROE / ROA • Return on Equity / Return on Total Assets ROI / EPS • Return on Capital / Earnings per Share

34 杜邦圖 1 --ROA HOW TO IMPROVE ROA 投資/匯兌收入Gain on 業外收入 O. I. 淨利 PBT 淨利率 PBT / NSB 銷貨額 資產報酬率 ROA NSB investment / exchange 利息收入 業外支出 O. E. + 營業利潤 O. P. Profit PBT/Total Assets Interest income 投資/匯兌損失Loss on investment / exchange Interest expense 流動資產 Current Assets Total Assets 總資產 Total Assets 銷貨成本 C. O. G. S. 研發 R&D 行銷 MKT 行政 現金 CASH ADM 短期投資Short-term Investment 應收帳款 A/R Fixed Assets 直接材料 M’TL. 直接人 D. L. 製造費用 Overhead 折舊 Depreciation 外包 Subcontract 存貨 INVENTORY 長期投資 Long term Investment 固定資產 銷貨退回 R. M. A. 營業毛利 G. P. M. NSB / 銷貨總額 Total Sales 利息支出 營業費用 O. P. EXP 銷貨額 資產週轉率 銷貨淨額 N. S. B. 土地/建築物 Land / Building 機器/模具 Machine / Tooling 間接人 /物料 I. D. L. / Supplies

35 杜邦圖 2 --ROE HOW TO IMPROVE ROE 投資/匯兌收入Gain on 業外收入 O. I. 銷貨淨額 N. S. B. investment / exchange 利息收入 銷貨總額 Total Sales Interest income 銷貨退回 R. M. A. 投資/匯兌損失Loss on investment / exchange 淨利 PBT 業外支出 O. E. + PBT / Equity Interest expense 直接材料 M’TL. O. P. Profit 直接人 D. L. 營業毛利 G. P. M. 營業利潤 股東權益報酬 率 ROE 銷貨成本 C. O. G. S. 利息支出 研發 R&D 營業費用 O. P. EXP 折舊 行政 ADM 股本 Common Stock Depreciation 現金 CASH 資本公積 Capital reserves 短期投資 流動資產 保留盈餘 Retained earnings 股東權 益 製造費用 Overhead 行銷 MKT 長期投資 總資產 Total Assets 負債 Liability 外包 Subcontract 應收帳款 A/R Current Assets 存貨 本期損益 Net income / loss Equity Short-term Investment 間接人 /物料 INVENTORY I. D. L. / Supplies Long term Investment 固定資產 土地 / 建築物 Land / Building Fixed Assets 機器 / 模具 Machine / Tooling 流動負債 Current Liability 短期借款 Short term loans 長期負債 Long term Liability 應付帳款 A/P

36 Operation Efficiency Inventory AR AP Site Cost Mgmt Loss CCC Days

40 Inventory Reserve Policy Idle Period Reserve % 90 days以上 85% *舊法係以不同Idle期間, 提列不同Reserve % , 四合一後將統一改 為上列之Reserve Policy

AR Reserve Policy -帳齡分析法 (新法) A/R Aging Reserve % Current 0% -- Overdue -- (已超過原先和客戶訂定的收款期限) 1 -30 days 0. 1% 31 -60 days 1% 61 -210 days 50% 211 -240 days 60% Over 241 days 100% * 舊法overdue 180 Days 即提列 100% 新法將於Yr 2003開始實施 45

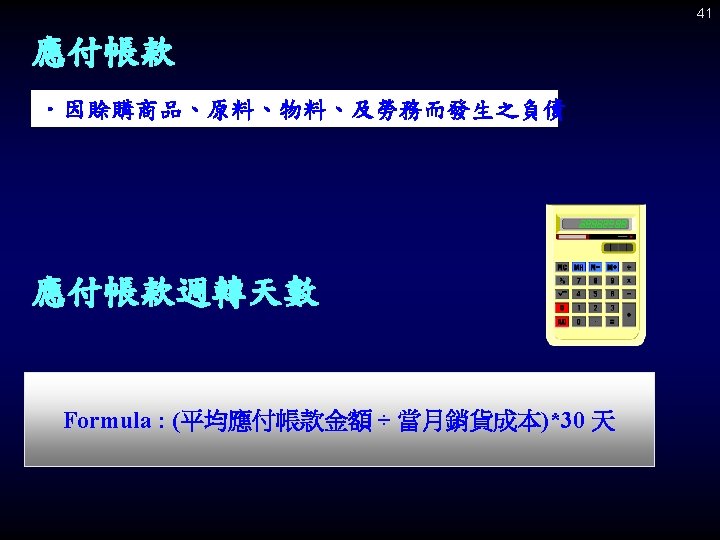

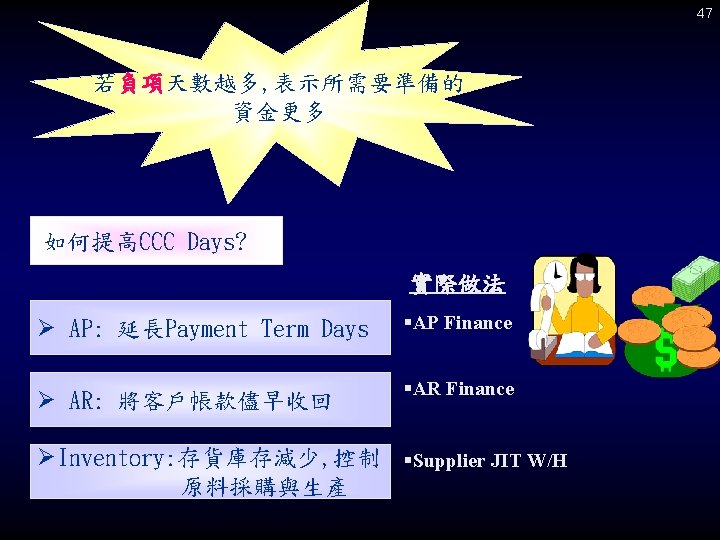

46 CCC Days: A/P Days - Inventory Days - A/R Days Cash Flow: A/P $ - Inventory $ - A/R $ 重點小百科 CCC days:正項 利用別人的錢來做生意 CCC days:負項 公司必須準備資金來做生意

52 Management Loss Ø因管理上的疏失而產生之非正常性的損失 Ø目的: 檢視如何避免管理上所產生之疏失, 以將資訊立即提供 給各BU提出解決之方案 Quality Issue Management Loss Inventory Loss • Sales Return • Rework • Inv Reserve • Inv Scrap • Inv 盤點 Loss Delivery • 交期 Delay 的空運費 Law Suit • 法律訴訟費

55 如何運用管理報表進行 決策與績效評估 ãPayroll Contribution ãHeadcount Analysis ãMaterial Cost Analysis

56 Break Even Point (BEP) NSB / NUB : Net sales billing , Net unit billing Variable cost : material , labor , overhead , expense Fixed cost : people. deprecation , expense NUB * UP = NSB - VC=Margin – FC = Profit NSB – VC - FC = Profit , If Profit = 0 NSB – VC = FC , NSB = FC + VC NUB * UP – NUB * @VC = FC NUB ( UP - @VC ) = FC NUB = FC / ( UP - @VC )

57 Expense Profit Total Cost Total Sales FC Loss VC B. E. P.

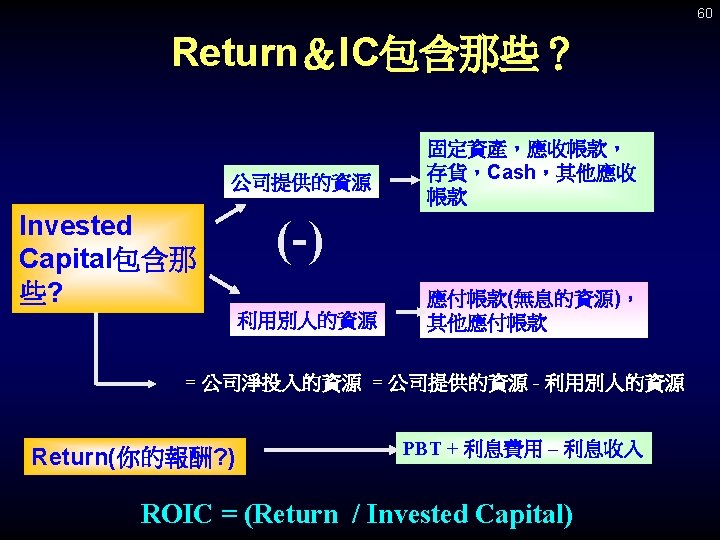

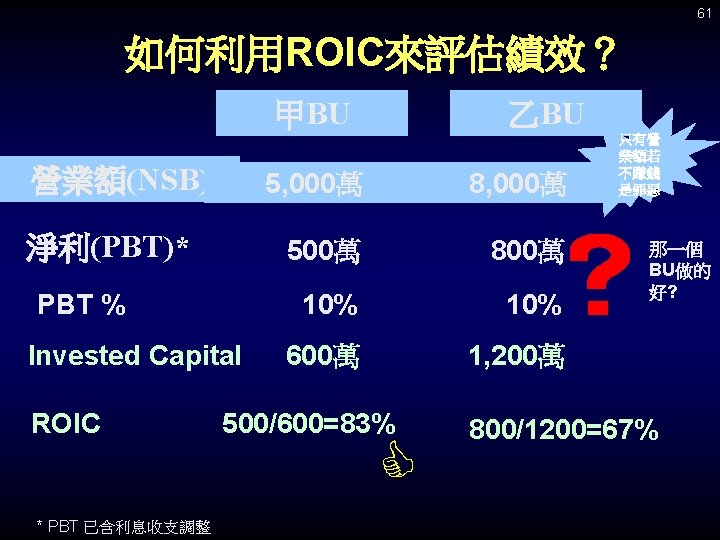

59 ROIC(Return on in Invested Capital) 投入資本報酬率 使用公司多少的資源? 替公司賺取多少的報酬? 賺取的報酬 ROIC= Adjusted operating profit = 使用公司資源 Invested capital

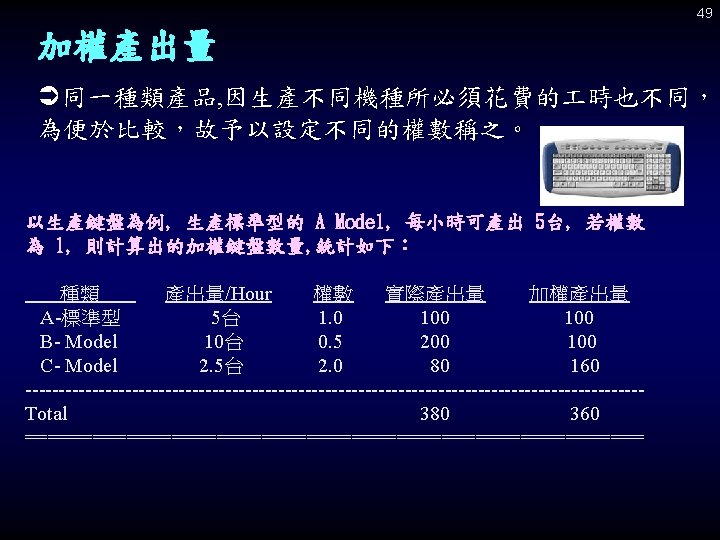

62

63