CSMFO 2013 ANNUAL CONFERENCE WHAT TO DO WHEN

:")

- Slides: 29

CSMFO 2013 ANNUAL CONFERENCE WHAT TO DO WHEN THE IRS COMES CALLING David Walton Tax Partner Jones Hall, A Professional Law Corporation San Francisco

• WHAT ARE THE ISSUES THAT POSE POTENTIAL RISKS FOR IRS AUDITS ON TAX-EXEMPT BONDS? • IRS Tax Exempt Audit Program • The IRS has an active tax-exempt bond audit group in its Tax Exempt and Governmental Entities division (TEGE).

• The IRS conducts both random and targeted audits. • The IRS may randomly select bonds to sample general compliance with tax rules. • The IRS may select bonds for audit based on specific attributes of the transaction. For example, the types of projects financed or the types of investments in refunding escrows (e. g. , yield burning audits). • How likely is it that the IRS will audit my bonds? While the IRS has a significantly larger group of tax-exempt bond auditors than it did just a few years ago, still only a small percentage of bonds are audited.

• Compliance Check Audits • The IRS may do a random check of general compliance with tax rules. • Lately, the IRS has been doing these checks through questionnaires. • The questionnaire will usually contain check the box questions with space for explanations if necessary.

• Compliance checks or surveys are not technically audits and cannot end in a determination from the IRS that the bonds are not tax-exempt. • Based on information gleaned from a compliance check, the IRS may open a formal examination or audit which can result in an adverse determination. • Care should be taken in responding to compliance checks. All questions should be answered but should be limited to the specific question asked and should not embellish or expand.

• Common Issues on Audit • Random audit, IRS is not necessarily looking for anything in particular. • Common areas the IRS focuses on: • Investments in advance refunding escrows (open market securities vs. SLGS) • Unspent proceeds. Bond proceeds should be spent within 3 years of issue. • Use of proceeds. Nongovernmental uses, management contracts, leases, preferential uses, nonpublic, etc.

• Compliance with reimbursement and allocation and accounting rules. • Rebate compliance. Computations of rebate and computation of bond yield. • Issue price of bonds. IRS has been talking about this for awhile. Will look at EMMA to compare secondary market trading to initial offering prices. BABS and direct pay credit bond issues. • Actual cash flow deficits on TRANs (recent compliance questionnaire).

• Exempt private activity bond issues – Public Hearings, Volume Cap, 95% Expenditure Test, Use of Facility, etc. • IRS announced a QSCB questionnaire in 2012. Will be an online form. • IRS has mentioned possible audits of under $15 million small issuers. Goal is educational to raise awareness of post-issuance compliance.

• Bond. Buyer Articles on April 4, 2012 and February 7, 2013 IRS “Red-Flag Transactions”: • IRS has created a compliance research team to identify red -flags indicating questionable municipal bond transactions. • Specific focus on bid-rigging and price fixing. • Goal is to provide a product to issuers to allow identification of red flags during the life of the bond issue. • The IRS has sent out a 14 -page semiannual newsletter to advise issuers about the IRS’ agenda and provide information on key issues. Issuer input requested.

• HOW CAN FINANCE PROFESSIONALS MINIMIZE THESE RISKS? • Post Issuance Compliance • Monitor and record all expenditures of bond proceeds. • Monitor uses of bond-financed property including agreements for the use of the property (e. g. , management contracts, reserved uses, naming rights, etc).

• Monitor investments and assure compliance with rebate. Do rebate yourself or hire a rebate consultant. Yield restrict bond proceeds if required. • Assure that the trustee is maintaining good records and that you have access to those records. • Call bond counsel and ask questions if in doubt regarding the use of bond proceeds. The best questions start with “we are considering using the bond proceeds for” as opposed to “we used the bond proceeds for”.

• Time Limits On Allocating Bond Proceeds • Due to limits on allocating bond proceeds, issuers should review (internal audit) expenditures of bond proceeds 5 years after date of issue, reallocate uses if necessary.

• Regulatory limit on allocations and reallocations (Treas. Reg. § 1. 148 -6): • (3) Absence of allocation and accounting methods. If an issuer fails to maintain books and records sufficient to establish the accounting method for an issue and the allocation of the proceeds of that issue, the rules of this section are applied using the specific tracing method. • (iii) Timing. An issuer must account for the allocation of proceeds to expenditures not later than 18 months after the later of the date the expenditure is paid or the date the project, if any, that is financed by the issue is placed in service. This allocation must be made in any event by the date 60 days after the fifth anniversary of the issue date or the date 60 days after the retirement of the issue, if earlier.

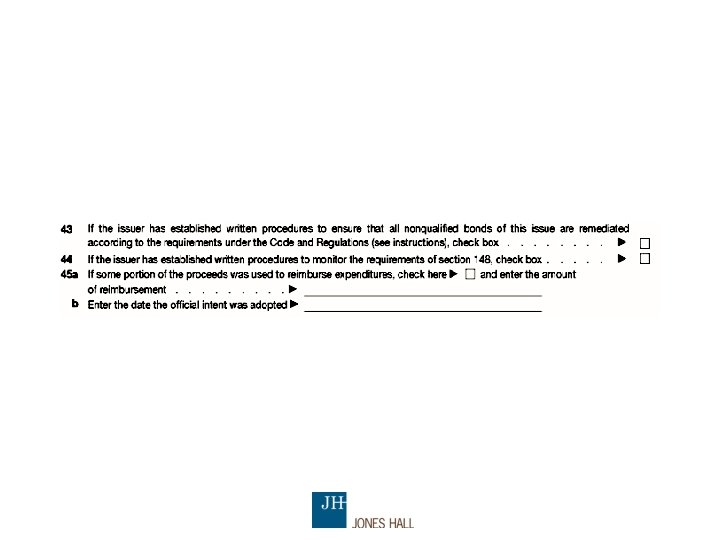

• Written Procedures for Post Issuance Compliance • IRS is asking if you have written procedures to ensure post -issuance compliance. • Forms 8038 now have a box to check if you have written procedures. Not required under statute but unclear if this will be an issue on audit. Here are the new questions on the form:

• Written procedures statement from IRS website: • Issuers should adopt written procedures, applicable to all bond issues, which go beyond reliance on tax certificates included in bond documents provided at closing. Sole reliance on the closing bond documents may result in procedures insufficiently detailed or not incorporated into an issuer’s operations. Written procedures should contain certain key characteristics, including making provision for:

• Due diligence review at regular intervals; • Identifying the official or employee responsible for review; • Training of the responsible official/employee; • Retention of adequate records to substantiate compliance (e. g. , records relating to expenditure of proceeds); • Procedures reasonably noncompliance; and expected to timely identify

• Procedures ensuring that the issuer will take steps to timely correct noncompliance. • The goal of establishing and following written procedures is to identify and resolve noncompliance, on a timely basis, to preserve the preferential status of tax-advantaged bonds. Generally, an issuer that has established and followed comprehensive written procedures to promote post-issuance compliance is less likely, than an issuer that does not have such procedures, to violate the federal tax requirements related to its bonds. http: //www. irs. gov/taxexemptbond/article/0, , id=243503, 00. ht ml

• Recordkeeping Requirements • Keep records with respect to the bonds for the entire term the bonds are outstanding plus 3 years thereafter. • If the bonds are refunded, keep records for the bonds and refunded bonds until the refunded bonds are redeemed plus 3 years thereafter. • Records in electronic format are permitted (scan docs). • The IRS has published a detailed statement regarding record retention with respect to tax-exempt bonds on their website. http: //www. irs. gov/taxexemptbond/article/0, , id=134435, 00. html

• Records the IRS May Request on Audit • Issuer draw requests and matching trustee records showing the expenditure. • Invoices and other material backing up draw requests including general ledger information. • Investment records showing interest earnings and investments. • For refundings, notices of redemption and trustee records showing payment of the refunded bonds. • For TRANs, general fund cash flow and backup.

What should I do if the IRS Audits my bonds? There at least 3 possible responses to a notice of an IRS audit of your tax-exempt bonds: • Ignore the IRS audit letter. Theorize that the IRS is a large bureaucracy and they will most likely not follow up if you fail to respond. • Panic and despair that all is lost. • Provide the information the IRS requests in an organized and carefully prepared manner showing compliance with all of the tax rules.

• An IRS audit is generally commenced with a letter being sent to the issuer announcing the audit. The letter identifies the issue being audited and the name and contact information of the auditor conducting the audit. This first letter will generally contain an “information document request” (IDR) that requests that certain base legal documents, such as an indenture and tax certificates, be provided to the auditor. The IDR will generally provide a relatively short deadline (usually 3 - 4 weeks) to provide the information.

• The letter will usually state that the IRS has no reason to believe that there is a problem with the bonds. • The time for responding to the letter and providing any documents or information requested can be extended, but you should request this extension from the auditor before the deadline has run.

• Care should be taken in responding to the auditor. While you should not withhold documents or information requested, documents and information should be presented in a format that minimizes the possibility that the auditor will think there is a problem. • While an issuer can handle an audit by themselves, it may be a good idea to get a professional involved. Note that the auditor will not talk to your attorney, rebate calculation agent, accountant or other representative who is not an employee of the issuer, without a signed power of attorney executed by the issuer.

• Usually, after the first letter and the issuer’s response, the auditor will send a second IDR asking for more information and/or more documents. It is not uncommon for multiple IDRs to be issued during the course of audit. Respond carefully to each IDR providing the specific information requested but not embellishing taking care not to present information in a manner that can be misinterpreted. • The auditor may request an onsite visit. Generally the auditor will want to match a sample of invoices, canceled checks and ledger entries to verify expenditures of bond proceeds. Be prepared to have these materials available. Also, the auditor will usually want to do an onsite inspection of the bond financed facilities. Care should be taken on who accompanies the auditor on these inspections to insure that statements that can be misunderstood are not made to the auditor.

• If all of your records are in order and the onsite inspection does not raise any issues regarding inappropriate uses of the bondfinanced facilities, the auditor should terminate the audit. The letter we hope to receive from the auditor at the end of the audit is a “no change” letter stating that they IRS is closing the audit with no changes.

Unspent RDA Proceeds and Successor Agencies • Unspent TAB bond proceeds are still bond proceeds and should not be used for nongovernmental or non-capital purposes (i. e, no working capital). • A State prohibition on expenditure of TAB bond proceeds has unclear Federal tax ramifications. May be deemed an abusive tax device. Delays due to waiting for a Finding of Completion from the State Department of Finance, (a “Golden Ticket”) may cause less problems. Golden Tickets do not apply to post 2011 bonds (AB 1484 § 34191. 4). • Unspent TAB bond proceeds in the project fund should be yield restricted once the State determines that the proceeds cannot be spent on the project (unclear if the delay is due to waiting for a Golden Ticket, possible yield restriction after the end of the 3 -year temporary period).

• It is unclear whether the IRS will approve of the use of unspent TAB proceeds to pay current and future debt service on bonds (applies to post 2011 non-Golden Ticket bonds). • One alternative is to invest these moneys in a yield restricted escrow and call the bonds on the first call date (hedge bond issues). • Since the TAB proceeds have not been spent, there is technically no “change in use” (since there is no use) so it is doubtful that the change in use remedial action provisions for governmental bonds will apply. • It may be helpful if a successor agency or the State asks the IRS to publish guidance or issue a private letter ruling addressing this issue.

David Walton Tax Partner Jones Hall A Professional Law Corporation 650 California Street, 18 th Floor San Francisco, CA 94108 415 -391 -5780 dwalton@joneshall. com