Crisis US money market 18 marzo 2015 Crisis

- Slides: 29

Crisis US money market 18 marzo 2015

Crisis liquidity

Response to the crisis

Mbs • Main problem: MBS collateral in repo • The dealers in MBS were damaged by the lack of liquidity so they had to be replaced by the public sector.

Shadow banks

Repo financing • Shadow banks used repo as means of financing because it was cheap.

taxonomy • Money market rates

Short term Rates spread • Befor the crisi erupted the spread between these rates were a few basis • A basis point = 0. 01

BASIS POINT • Smallest measure of quoting the yield on a bond, note, or other debt instrument. One basis point is equal to one hundredth of one percent (0. 01%): one percent of a yield equals 100 basis points. For example, an interest rate of 5 percent is 50 basis point higher than the interest rate of 4. 5 percent. Similarly, a spread of 50 basis points (between the bid price and offer price of a bond) means the investor must pay 0. 5 percent more to buy it than he or she could realize from selling it. Read more: http: //www. businessdictionary. com/definition/basispoint. html#ixzz 2 w. VQGCcpu

repo • REPO SONO LA MAGGIORE FONTE DI FIN. • PER I DEALERS NEI TITOLI CHE FANNO IL MERCATO. • Se un dealer acquista un titolo si finanzia per mezzo di un repo in cui offre come garanzia il titolo acquistato. La controparte e’ un altro dealer o un’impresa non finanziaria.

Federal funds market • The fed. funds is an inter-bank market where banks that borrow fed funds receive deposits at the Fed and pay an interest. The Federal funds rate is determined by the supply of and demand for funds. The fed however tries to keep it within a certain range and in order to make it converge to the desired target it lends against collateral.

• Le banche non hanno accesso ai fed funds devono invece pagare il libor. • Fed funds and libor prestiti non sono assicurati ma le banche osservano con attenzione i bilanci delle controparti. • Questi tassi sono allineati dall’arbitragggio. Gli operatori che possono farlo prendono a prestito al tasso piu’ economico e danno a prestito al tasso piu’ elevato.

• Questa struttura e’ antecedente la nascita dello shadow banking ma lo shadow banking l’ha utilizzata cosicche’ durante la crisi essa ne’ stata influenzata. • Il crollo delle relazioni di arbitraggio tra i tassi durante la crisi e’ la prova EVIDENTE dei problemi di liquidita’ ad essa collegati.

overnight money market rates

Vertical lines • Vertical lines show when Bear Stearns and Lehman failed.

First period • In the first period from july 2007 to march 2008 the spread between the libor rate and the federal funds rate increased while the spread between treasury repos and federal funds rate decreased. In this period the fed intervened every day in the market to stabilize the federal funds rate at its target rate which was 2% (falling from 5%).

Fed funds rate and target

Second period • In the second period overnight rates go back to the pre-crisis standards. • The reason for this behaviour is not that problems in markets have vanished but rather the fed intervention exchanging Treasuries with MBS and facilities TAF. Fed acts as public lender of last resort.

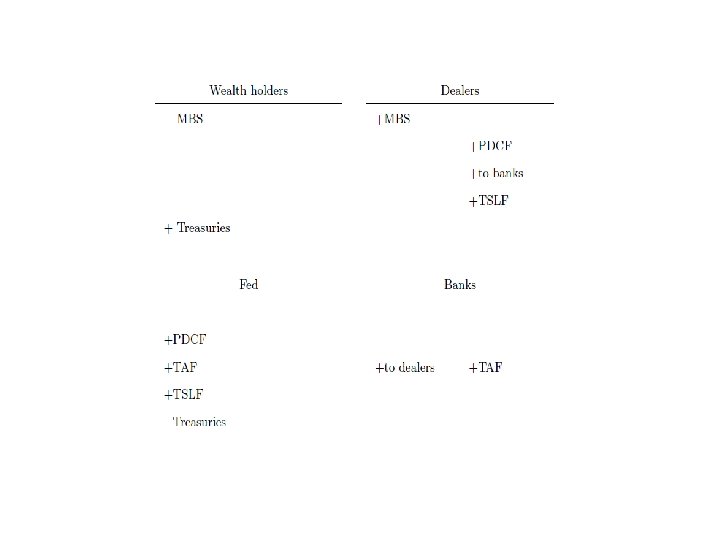

Figure explanation • As wealth holders attempt to get rid of their MBS the dealers must buy them. The Fed supports them with various facilities. PDCF provides funds to dealers while TAF provides fund to banks. The Fed finances these loans by selling treasuries.

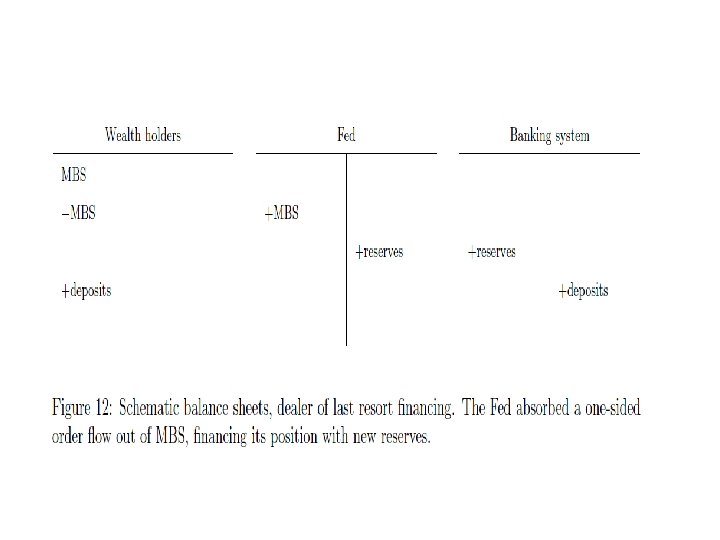

third period • After Lehman’s collapse the spread between repo rates and fed funds rates and that between Libor rates and federal funds rate have increased. In this period the Fed intervened as dealer di last resort.

Expansion fed’s balance • This intervention made the balance sheets of the fed double within some weeks. Rates fell from 2% to 0%. The most important thing however is the expansion of the Fed’s balance sheet.

fed assets

fed liabilities

Comment graph • The Fed used open market operations as policy tool until the end of 2007. From the spring of 2008 onwards it started using special facilities and this has changed the composition of its balance sheet.

Third period • After Lehman’s colapse the fed’s balance sheet has dramatically expanded. On the assets side we can see the various new facilities introduced by the Fed. These facilities were just temporary. When they expired in 2010 the Fed used the sums reimbursed to buy directly in the market MBS. On the liabilities’ side we can see that reserves have increased.