Credit Rating Credit Risk Default Risk What is

• What is Credit Risk ? • It is the")

because:")

")

• For example, S&P Global Ratings evaluates the issuer’s")

• In rating an individual debt issue, such as")

")

. • After determining")

bonds")

in the EU")

- Slides: 62

Credit Rating

Credit Risk (Default Risk) • What is Credit Risk ? • It is the possibility of a loss from the failure of a borrower to: (a) repay a loan or (b) meet contractual obligations • It is not possible to assess exactly which borrower will default, however, one can attempt to assess and manage the credit risk; this may lessen the severity of a loss • • • Examples: a government/company does not pay all/some regular coupons on bonds a company does not pay the principal on issued corporate bonds at all or on time business partners do not meet obligations in due time an individual stops/fails to pay bank loans and/or mortgage payments an bank does not return deposits

Credit Risk • Fixed income securities investors are also concerned with: • credit spread risk, i. e. the uncertainty about the credit spread, i. e. the premium that we add on a base rate (e. g. a gov security) that reflects the credit rating or risk rating of the company, etc. • E. g. If the creditworthiness of a company decreases, its credit spread increases (“widens”) and thus the appropriate discount rate increases which means that the price of the debt security decreases (and visa versa) • downgrade risk (related to credit spread risk), i. e. the possibility of a lower credit rating which s an indicator of potential default risk • Changes in the credit spread and downgrade risk directly impact trading prices

Credit Risk • How can investors evaluate the probability of default of an issuer? • Credit Analysis • The evaluation requires resources (time, know how, access to data, etc) and is difficult for investors • Investors can turn to specialised independent international Credit Rating Agencies (CRAs) who help lenders deal with asymmetric information issues (Standard & Poor’s, Moody’s, Fitch, International Bank Credit Rating Agency, Japan Credit Rating Agency, etc. ) • They assign credit ratings to the assessed entities and their debt instruments issues • Standard & Poor’s use letters: ΑΑΑ, Α, ΒΒΒ, Β, CCC, C, C 1, D. Often they use signs (+) or (-) to distinguish between ratings(e. g. ΑΑ+, CCC-), while Moody’s is using Aaa, Aa, Α, Baa, B, ……. …. D, and letters (e. g. Αα 1, Αα 2).

Credit Rating Opinions: Standard & Poor’s

Moody’s

Moody’s

Credit Rating • Credit ratings are opinions about credit risk. They express the CRAs opinion about the ability and willingness of an issuer • Credit rating agencies evaluate the creditworthiness of issuers and estimate the likelihood of default. The rating represents the agency’s evaluation of qualitative and quantitative information for a company or government; • Credit rating agencies use their judgment and experience in determining what public and private information should be considered in giving a rating to a particular company or government. • The credit rating is used by individuals and entities that purchase the bonds issued by companies and governments to determine the likelihood that an issuer will pay its bond obligations.

Credit Rating • Credit ratings are forward looking: CRAs evaluate available current and historical information and assesses the potential impact of foreseeable future events. • Credit ratings are not a guarantee that an investment will pay out or that it will not default. • Credit ratings do not indicate investment merit; they are not buy, sell, or hold recommendations, • Credit ratings are not absolute measures of default probability; future events are not possible to predict with accuracy

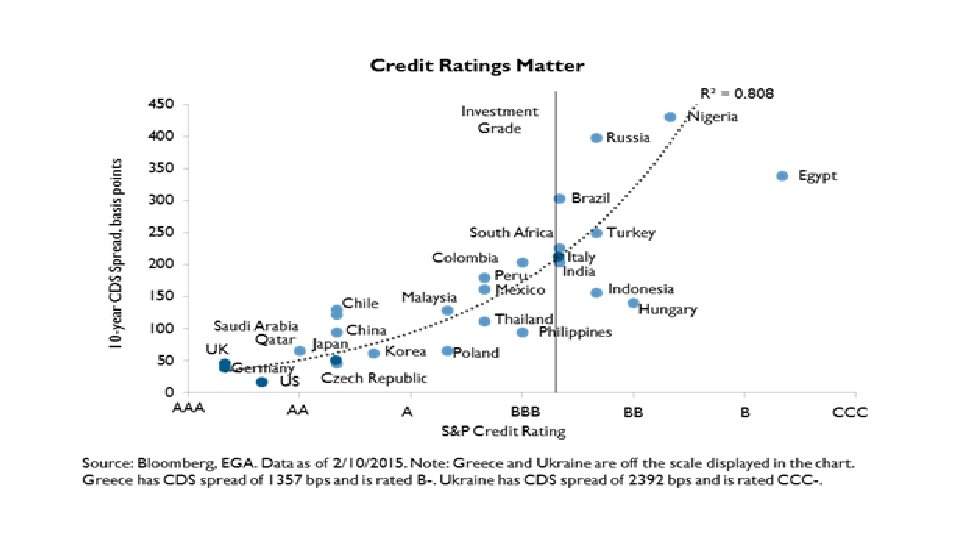

Credit Rating • Credit rating agencies assign ratings to issuers, such as corporations and governments, as well as to specific debt issues, such as bonds, notes, and other debt securities. • An important factor that makes the rating of sovereigns different compared to the rating of firms is the concept of “willingness to pay. ” • To capture this element, CRAs assess a range of qualitative factors such as institutional strength, political stability, fiscal and monetary flexibility, and economic vitality. In addition, a country’s track record of honoring its debt is an important indicator of willingness to pay. • Afonso et al. (2007) , examine the determinants of sovereign debt credit ratings of the big three rating agencies using a panel of 130 and find that GDP per capita, real GDP growth, government debt, government effectiveness, external debt and external reserves, sovereign default indicator, and a dummy for EU membership, are the most important determinants of the sovereign debt ratings.

Credit Rating • Issuers and investors rely heavily on Credit Rating Agencies (CRAs) because: • Issuers are often obliged by regulation to have their issues evaluated and rated in before the enter the market • CRAs have been around for over a century. • Difficult for investors to analyze bond issues • Asymmetric information

Credit Rating • Key-role: central banks often require that assets have a minimum rating to be acceptable as collateral for financial institutions if they want to borrow from the central bank. • For instance, until recently the European Central Bank (ECB) required marketable assets to have at least one BBB- credit rating from one of the four accepted external credit assessment institutions (with the exception of asset-backed securities, for which the credit rating at issuance should be AAA). • Also regulators, have tied bank capital requirements to ratings, effectively outsourcing their due diligence to rating agencies without sufficient consideration of whether credit ratings meant the same thing for structured finance as for other securities. • Source: De Haan and Amtenbrink (2011) Credit rating agencies, DNB Working Paper, No. 278.

Investment-grade and non-investment-grade bonds • The term “investment-grade” historically referred to bonds and other debt securities that bank regulators and market participants viewed as suitable investments for financial institutions. Now the term is broadly used to describe issuers and issues with relatively high levels of creditworthiness and credit quality. • In contrast, the term “non-investment-grade, ” or “speculative-grade, ” generally refers to debt securities where the issuer currently has the ability to repay but faces significant uncertainties, such as adverse business or financial circumstances that could affect credit risk. • In S&P Global Ratings long-term rating scale, issuers and debt issues that receive a rating of ‘BBB-’ or above are generally considered by regulators and market participants to be “investment-grade, ” while those that receive a rating lower than ‘BBB-’ are generally considered to be “speculative-grade. ” • Source: S&P

Investment-grade and Non-investment-grade bonds

Credit Rating: Probability of Default

Credit Rating • Note that CRAs frequently provide different ratings for the same entity. • Alsakka and ap Gwilym (2009) show that rating disagreements across agencies are more frequent for sovereign ratings than for corporate ratings. • In their sample of sovereign ratings, Moody’s and Standard and Poor’s disagree on 50. 6 % of daily rating observations; Moody’s and Fitch have different sovereign ratings in 46. 9 % of the observations; Standard and Poor’s and Fitch have by far the lowest frequency of disagreement (35. 9 %). • Why ? They use different factors and place different weights on these factors, they disagree to a greater extent about more speculative-grade rated issuers, and, finally, some agencies may tend to rate issuers in their “home region” more favorable. • Source: De Haan and Amtenbrink (2011) Credit rating agencies, DNB Working Paper, No. 278.

Long term and short term rating • Credit ratings can be either long-term or short-term. • Short-term ratings are generally assigned to those obligations considered short-term in the relevant market, typically with an original maturity of no more than 365 days. • Medium-term notes are assigned long-term ratings. • Long-Term ratings are based on: • The likelihood of payment (capacity and willingness to meet commitments) • The nature and provisions of the financial obligation, • The protection afforded by, and relative position of, the financial obligation in the event of a bankruptcy, etc • Source: S&P

How CRAs are paid for their services • Agencies typically receive payment for their services either from the issuer that requests the rating or from subscribers who receive the published ratings • Issuer-pay model. Under the issuer-pay model, rating agencies charge issuers a fee for providing a ratings opinion. In conducting their analysis, agencies may obtain information from issuers that might not otherwise be available to the public and factor this information into their ratings opinion. If the rating agency does not rely solely on subscribers for fees, it can publish current ratings broadly to the public free of charge. • Subscription model. Credit rating agencies that use a subscription model charge investors and other market participants a fee for access to the agency’s ratings. Critics point out that, like the issuer-pay model, this model has the potential for conflicts of interest since the entities paying for the rating, in this case investors, may attempt to influence the ratings opinion.

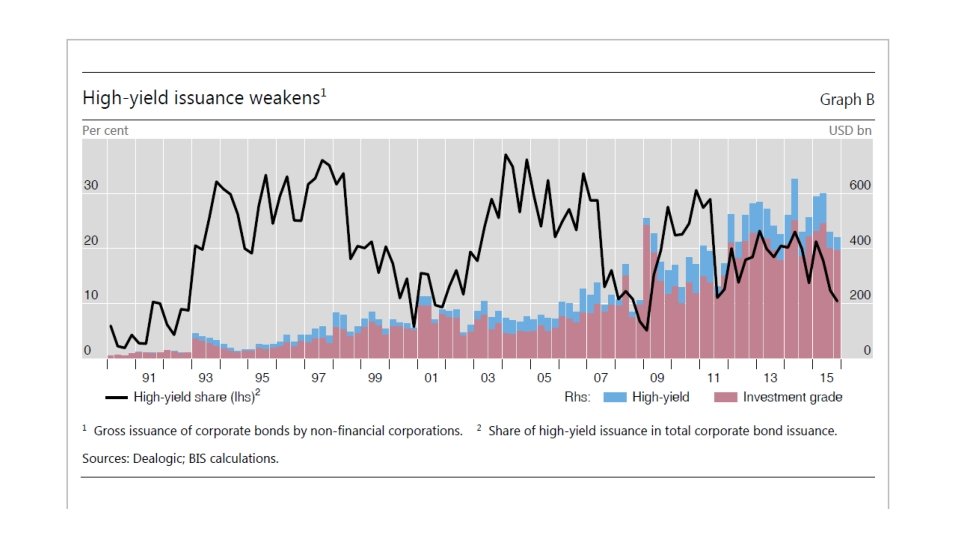

Credit Spreads • The Default premium is usually referred to as “credit spread” since it reflects the spread between the yields to maturity of two differently rated debt securities • Usually we employ a default free security as a “benchmark” (e. g. a gov bond), and the bond we are interested at is identical to benchmark in all aspects expect for credit risk • For example, assume that a the 10 -year corporate bond of company XXX has an AAA rating and a yield of 4. 00% while the 10 -year US gov bond has a yield of 3. 5% • The spread (default premium) for this bond is 0. 5% • Market participants use basis points (1% = 100 basis points, bps) • Thus, the spread in the above corporate bond is 50 bps (basis points)

Credit Spreads

Credit Spreads • During Financial Crises and periods with financial turmoil credit spreads widen while during periods of economic expansions they tend to narrow • The main reasons are (and visa versa): • Increase in uncertainty during financial crises • In a declining economy firms experience declines in sales/revenues/cash flows and may be more difficult for them to meet financial obligations, thus, default risk is higher • “flight to quality”: during financial crises investors turn to safer assets. For example during the EU crises many investors dumped bonds from the EU periphery and massively invested in German bonds

Credit Spreads and the Financial Crisis (2009)

Rating an issuer (Source: S&P) • For example, S&P Global Ratings evaluates the issuer’s ability and willingness to repay its obligations in accordance with the terms of those obligations. • Reviews a broad range of financial and business attributes that may influence the issuer’s prompt repayment. • For a corporate issuer many financial and non-financial factors are analysed, including key performance indicators, economic, regulatory, and geopolitical influences, management and corporate governance attributes, and competitive position. • In rating a sovereign or national government, the analysis may concentrate on fiscal and economic performance, monetary stability and the effectiveness of the government’s institutions. • For high-grade credit ratings, S&P Global Ratings considers the anticipated ups and downs of the business cycle, including industry-specific and broad economic factors.

Rating an issue (Source: S&P) • In rating an individual debt issue, such as a corporate or municipal bond, S&P Global Ratings typically uses, among other things, information from the issuer and other sources to evaluate the credit quality of the issue and the likelihood of default. • In analyzing debt issues, for example, S&P Global Ratings analysts evaluate, among other things: • The terms and conditions of the debt security and, if relevant, its legal structure. • The relative seniority of the issue with regard to the issuer’s other debt issues and priority of repayment in the event of default. • The existence of external support or credit enhancements, such as letters of credit, guarantees, insurance, and collateral. These protections can provide a cushion that limits the potential credit risks associated with a particular issue.

Rating an issue (Source: S&P)

Rating Outlook • Outlooks are used by the agencies in order to provide a possible direction for their longterm evaluation within the following 6 to 24 months; they report on expected economic changing conditions and expected changes on issuers • An Outlook does not necessarily mean a future change of the Rating or a Credit Watch • An Outlook is usually accompanied by the following signs: (+): (-): Stable: Developing: when a rating upgrade is expected when a rating downgrade is expected when no rating changes are expected when it is considered possible that the rating will change but the direction is unknown

Credit Watch • A Credit Watch is announced in order to underline a point relative to the possible future direction of a long/short term Rating • If events or circumstances occur that may affect a credit rating in the near term, usually within 90 days, S&P Global Ratings may place the rating on Credit. Watch. • It focuses on very specific events and short-term trends • A Credit Watch may be positive (suggesting a possible upgrade) or negative (suggesting a possible downgrade) • It may also be accompanied by the term “Developing”

Rating Change • If CRAs has all the information available to warrant a ratings change, it may upgrade or downgrade the rating immediately • without • placing the rating on Credit. Watch or changing its outlook, to reflect these circumstances and its current opinion of relative credit risk.

Ratings Process example: S&P • 1. Contract: The issuer requests a rating and signs an engagement letter. • 2. Pre-Evaluation: Assemble a team of analysts to review pertinent information. • 3. Management Meeting: Analysts meet with management team to review and discuss information. • 4. Analysis: Analysts evaluate information and propose the rating to a rating committee. • 5. Rating Committee: The committee reviews the lead analyst’s rating recommendation then votes • 6. Notification: provide the issuer with a pre-publication rationale for fact-checking and accuracy purposes. • 7. Publication: Publish a press release announcing the public rating and post the rating on our website. • 8. Surveillance of Rated Issuers and Issues: The goal of this surveillance is to keep the rating current

Ratings Process example: S&P

Rating methodologies • CRAs use analysts or mathematical models, or a combination of the two. • Model driven ratings. A small number of credit rating agencies focus almost exclusively on quantitative data, which they incorporate into a mathematical model. For example, an agency using this approach to assess the creditworthiness of a bank or other financial institution might evaluate that entity’s asset quality, funding, and profitability based primarily on data from the institution’s public financial statements and regulatory filings. • Analyst driven ratings. In rating a corporation or municipality, agencies using the analyst driven approach generally assign an analyst, often in conjunction with a team of specialists, to take the lead in evaluating the entity’s creditworthiness. Typically, analysts obtain information from published reports, as well as from interviews and discussions with the issuer’s management. They use that information and apply their analytical judgment to assess the entity’s financial condition, operating performance, policies, and risk management strategies.

Which factors impact sovereign credit risk? • S&P indicates five key areas of evaluation for sovereigns that are important from the perspective of the creditors of sovereigns: • 1. Institutional framework • Qs: how sustainable are public finances, whether the government promotes balanced economic growth, how the government responds to economic and political shocks, how transparent and accountable are data processes, what is the debt repayment culture, what are potential external and domestic security risks • 2. Economic environment • Qs: country’s income level as measured by its GDP per capita, investment future possibilities, economic diversity and volatility, growth prospects as measured by GDP growth, unemployment rate

Which factors impact sovereign credit risk? • Institutional and economic profile: evaluation of the country’s institutional framework and its economic. • It reflects the resilience of a country's economy, the strength and stability of its civil institutions, and the effectiveness of its policymaking. • Flexibility and performance profile: the country’s external assessment along with the evaluation of its fiscal and monetary policy. • It provides information about the sustainability of a government's fiscal balance and debt burden, in light of the country's external position, as well as the government's fiscal and monetary flexibility. • The table in the next slide shows how a specific credit rating is assigned given the combination of the two profiles

Which factors impact sovereign credit risk?

Which factors impact sovereign credit risk? • 3. External assessment • Qs: the status of the currency in international transactions, the country's external liquidity, which provides information on the economy's ability to generate the foreign exchange which is necessary to meet its public and private sector obligations to foreigners, the residents' assets and liabilities (in both foreign and local currency) relative to the rest of the world • Fiscal policy • Qs: fiscal flexibility, long-term fiscal trends and vulnerabilities, debt structure and funding access, potential risks arising from contingent liabilities, the sustainability of a sovereign's deficits and its debt burden. • Monetary policy • Qs: the exchange rate regime, which influences a sovereign's ability to coordinate monetary policy with fiscal and other economic policies to support sustainable economic growth, the credibility of monetary policy as measured by inflation trends over an economic cycle and the effects of market-oriented monetary mechanisms on the real economy, etc

Which factors impact corporate credit risk? • Example of S&P analytical methodology that divides the task into several categories so that all salient issues are considered: • 1. Business risk profile • 2. Financial risk profile • 3. Combination and determination of anchor assessment • 4. Modification to arrive at a stand-alone credit profile • 5. If applicable, factor in group or government influence

Which factors impact corporate credit risk? • 1. Business risk profile • It is defined by the risk/return potential for a company in the markets in which it participates, the country risks within those markets, the industry risk, and the competitive • The business risk profile affects the amount of financial risk that a company can bear • Business risk profile assessments range from "excellent" (highest) to "vulnerable" (lowest).

Which factors impact corporate credit risk? • Industry risk • Two factors for determining a global industry risk assessment: • Cyclicality: Historical research demonstrates that industries vary significantly in their degree of revenue and profitability cyclicality. • Competitive risk and growth environment: the effectiveness of industry barriers to entry; the level and trend of industry profit margins; the risk of secular change and substitution by products, services, and technologies; and the risk in industry growth trends. • Industry risk is scored from 1 (lowest risk) through 6 (highest risk).

Which factors impact corporate credit risk? • The combined assessment for country risk and industry risk is known as the issuer's Corporate Industry and Country Risk Assessment (CICRA). • CICRA is also ranked from 1 (lowest risk) through 6 (highest risk). • The CICRA is combined with a company's competitive position assessment in order to complete the issuer's business risk profile assessment. • Competitive position encompasses the combination of company-specific business features and operating attributes that add to or mitigate its industry risk and country risk: • • Competitive advantage Scale, scope, and diversity Operating efficiency Profitability

Which factors impact corporate credit risk? • The company's strengths and weaknesses with respect to each of the first three of these components shape its competitiveness in the marketplace, the sustainability and volatility of its revenues and profits, and by extension, the strength of its business risk profile. • Ultimately, to demonstrate a strong competitive position, a company should produce superior profitability to that of its peers, while companies with weaker competitive positions would show profitability metrics that underperform peers’. • A stronger-than-industry-average set of competitive position characteristics will strengthen a company's business risk profile (and visa versa) • Based on the above factors, an issuer's competitive position ranges from 1 (excellent) to 6 (vulnerable).

Which factors impact corporate credit risk? • 2. Financial risk profile • The manner in which the company is funded and how its balance sheet is constructed. • It also reflects the relationship of the cash flows the organization can achieve, given its business risk profile • Cash flow/leverage analysis is used to determine a corporate issuer's financial risk profile assessment. • Financial risk profile assessments range from "minimal" (least financial risk) to "highly leveraged" (greatest financial risk).

Which factors impact corporate credit risk? • 3. Anchor • Combination of business risk profile score and its financial risk profile score • The analysis weights business risk profile more heavily in arriving at the overall anchor assessment of an issuer for an investment-grade anchor, while the financial risk profile carries more weight in arriving at the anchor for a speculativegrade anchor. • Standard & Poor's analysts use a matrix (next slide) to combine the business risk profile and financial risk profile assessments.

Which factors impact corporate credit risk?

Which factors impact corporate credit risk? • The key financial measures that are used to assess the credit risk of a corporation or the issued debt instruments are the following: • coverage ratios • leverage ratios • liquidity ratios • profitability ratios • cash-to-debt-flow ratios

An indicative, random, and simplified example • Note that in Sept 2020: S&P GE’s rating was BBB+, while Moody’s GE’s rating was BBB

Which factors impact corporate credit risk? 4. Stand-alone credit profile (SACP). • After determining the anchor, additional rating factors can modify the outcome, and they can raise or lower the anchor by one or more notches--or have no effect in some cases. • These are expressed using specific assessments and descriptors, which in turn, determine the number of notches to apply to the anchor to determine the SACP.

Which factors impact corporate credit risk? • 5. Group or government influence • Assessment of likely extraordinary group or government support (or conversely, negative intervention) factors into the issuer credit rating on an entity that is a member of a group or is a government-related entity. • The criteria define five categories of group status: "core, " "highly strategic, “ "strategically important, " "moderately strategic, " and "nonstrategic. " • Each category indicates a different view of the likelihood that an entity will receive support from the group • The ultimate outcome of group influence analysis can be anything from no change to the SACP up to equalization with the group credit profile.

Ratings Below 'B-' • If S&P views an issuer's capital structure as unsustainable or if its obligations are currently vulnerable to non-payment, and if the obligor is dependent upon favourable business, financial, and economic conditions to meet its commitments on its obligations, then S&P determines the issuer's SACP using "Criteria For Assigning 'CCC+', 'CCC-', And 'CC' Ratings, " published Oct. 1, 2012. • Further, if an issuer is undergoing a debt restructuring we may apply the criteria outlined in "Ratings Implications Of Exchange Offers And Similar Restructurings, Update, " published on May 12, 2009.

Ratings Below 'B-'

Ratings Below 'B-'

Criticism • According to many observers, CRAs underestimated the credit risk associated with structured credit products during the crisis (2007 -2009) (Pagano and Volpin, 2010). • For instance, according to the IMF, more than three quarters of all private residential mortgage backed securities issued in the United States from 2005 to 2007 that were rated AAA by Standard & Poor’s where later rated below BBB-, i. e. , below investment grade. • The IMF (2010) concludes that “While downgrades are expected to some extent, a large number of them—in particular when they involve several notches at the same time or when the downgrading takes place within a short period after issuance or after another downgrade—are evidence of rating failure”.

Criticism • During the 2000 -2002 period Enron and World. Com defaulted despite the investmentgrade evaluation by credit rating agencies • In a Staff Report of the U. S. Senate Committee on Governmental Affairs (2002) it was noted that: • “Not one of the watchdogs was there to prevent or warn of the impending disaster: [. . . ] not the credit rating agencies, who rated Enron’s debt as investment grade up until four days before the company filed for bankruptcy; and not the SEC, which did not begin to seriously investigate Enron’s practices until after the company’s demise became all but inevitable. ” • Same with Lehman (2008): the day before Lehman went bankrupt the major CRAs gave the bank still investment grade ratings. • Source: De Haan and Amtenbrink (2011) Credit rating agencies, DNB Working Paper, No. 278.

Criticism • CRAs were condemned for failing to predict the Asian crisis, and for exacerbating the crisis when they downgraded the countries in the midst of the financial turmoil. • In the context of the EU crisis (2009 -2012), CRAs have been criticised for downgrading European sovereigns thereby exacerbating the fiscal problems of countries like Greece, Ireland, Portugal and Spain. • Some of these adjustments surprised markets, in particular with regard to their scale. Specifically, the four-notch downgrade of Greece by Moody’s in June 2010 caught markets by surprise, with spreads widening significantly following the event. • According to the President of the European Commission, “…. . ratings appear to be too cyclical, too reliant on the general market mood rather than on fundamentals - regardless of whether market mood is too optimistic or too pessimistic”.

Criticism • Same with Leeman and the securitized (toxic as it turned out) bonds that were based on US home loans

Fitch Global Structured Credit Rating Changes

Credit Rating Changes

Credit Rating Agency Supervision • European Security and Markets Authority (ESMA) in the EU • Aim: enhance the integrity, responsibility, good governance and independence of CRAs to ensure quality ratings and high levels of investor protection. • Analyze complaints received by market participants. • Review notifications of material changes to the initial conditions from registration. • Monitor ratings data submitted to ESMA by CRAs • Other objectives: increase competition in the markets for credit ratings by encouraging issuers to use smaller credit rating agencies

Credit Rating Agency Supervision • US: registration under the SEC of Nationally Recognized Statistical Rating Organizations (NRSROs) • Credit Rating Agency Reform Act (2006) gives to SEC the power to regulate CRAs • Dodd-Frank Act (2010) revises CRAs regulation with main targets: • Increase accountability of CRAs • Reduce reliance of regulation on rating (regulation should no longer use/refer to ratings) • Increase information disclosure (similar to Europe) • Individual analyst accountability for the rating independence • ABS rating regulation under scrutiny Global CRAs Regulation • A committee to harmonize the surveillance of internationally active CRAs

Credit Rating Agency Supervision • European regime under Regulation 1060/2009: • Ratings for structured finance instruments must ensure that those credit rating categories attributed to structured finance instruments are clearly differentiated using a symbol, which distinguishes them from rating categories used for any other entities, financial instruments, or financial obligations. • EU registered CRAs are also obliged to disclose to the public the methodologies, models, and key rating assumptions such as mathematical or correlation assumptions used in its credit rating activities as well as their material changes.

Credit Rating Agency Supervision • CRAs must also continually review ratings in order to prevent them from concentrating on the initial rating and neglecting subsequent monitoring against the background of macroeconomic or financial market developments, which can be detrimental to the on-going quality of the ratings. • The Regulation aims at improving the transparency of CRAs, including their past performance. With regard to the latter, CRAs must also disclose ratings on a nonselective basis and in a timely manner. • CRAs must publish an annual transparency report and keep extensive records of their activities. • CRAs are obliged to disclose conflicts of interest in a complete, timely, clear, concise, specific, and prominent manner and record all significant threats to the rating agency’s independence or that of its employees involved in the credit rating process