Credit Cards Credit Credit when good or service

- extended as a line of credit")

• Is rate F")

- Slides: 53

Credit Cards

Credit • Credit- when good or service is received in exchange for a promise to pay a definite sum of money at a future date • Lender- Person or Organization that provides the loan. Bank, Credit • Borrower- Person who get the money on as a loan • Creditworthiness- ability and willingness to pay money back • Principal- The amount of money you borrow ($1, 000) • Interest- The price a lender charges you to borrow money (20%)

Closed-Ended Credit • Closed Ended Credit- Borrower must repay in specified number of payments. 5 years for a car, 30 years for house • Agreement between borrower and lender with terms that end after principal is repaid • Installment credit (closed ended)- # of payments (5 years 60 months) + Interest (APR or rate) • Examples of closed ended credit- College Loans, Auto, Home • Can extra pay off principal to cut years off by paying extra payments

Principal Installment Interest over 10 years Total amount to pay back with interest

Open Ended Credit • Revolving Credit (Open Ended)- extended as a line of credit in advance so borrower doesn’t have to apply for credit each time it is desired • Can be repaid in one month or over many • Borrower chooses how much to repay each month • Minimum payment- lender requests a small fee per month • Unpaid balance is revolved into next month

How do I obtain a credit card? • Credit application- complete application • What do they look at? Earnings, Savings, Job, Credit Worthiness • Pre-approved- you passed initial check but doesn’t mean anything • Credit Investigation- lenders compare your information and study your credit history • Denial- You can be denied based on your credit history after investigation

Sample $1, 500 purchase on revolving Credit Total Interest Total Amount paid Payment Length Full Payment $1500 1 month $0 $1, 500 Partial $135 1 year $125 $1, 625 Minimum $30 11 years $1, 413 $2, 913

SAFETY TIPS • Sign your credit card or write Please see ID • People that work register will ask for a photo ID to prove it is you • Never give out credit number unless purchasing something • Report lost or stolen immediately • Check online accounts weekly for any suspicious activity such as unknown purchases

APR- Inerest Rate • Interest Rate- Is charge to borrow the money known as (APR) Annual Percentage Rate • Very High for Credit Cards 20% and going up, some all the way up to 30% • 24% means 2% per month for each purchase that you don’t pay off- for annual % of 24.

APR - Interest Rates • APR - only matters if you do not pay off your balance • I. E. - Charge 2, 000 and pay it off before due date- no APR is ever assessed, no charges to you • I. E. - Charge 2, 000 and pay off $50. The $1950 will be charged at your APR. 24% APR will put 2% on at end of month due to 24% Annual Percentage/12 months=2% every month or 24% for the year.

Understanding Credit Cards 1. Knowing Your Limit 2. Don’t get in over your head. 3. A credit card is a loan Anything not paid back in full is assessed an interest charge. 4. There’s a pre-determined credit limit and money spent can be paid back in full or in installments.

Advantages 1. Convenient 2. Emergencies useful 3 Required for reservations 4. Big purchases can be spread out 5. Positive credit rating 6. Bonuses and Rewards 7. Immediate purchasing power 8. No need for cash 9. Bills can be consolidated 10. Zero liability on fraud

Disadvantages 1. It’s a loan 2. Interest makes more purchases more expensive 3. Identity theft threats 4. Interest rate may go up 5. May include additional fees 6. Can be easy to overspend 7. Can promote impulse buying

The Debit Card Looks just like a credit card but not a loan, you pay no interest it is money you already have Backed only by the checking account behind it. Widely accepted, can be a good budgeting tool. Does not help credit score.

Debit Card Security • • • Need to know PIN to access the money. ATM use Create a PIN that a smart thief couldn’t figure out. Avoid the obvious like birth dates, names, etc. Always keep receipts Always check online checking account for suspicious activity or unknown transactions

Debit Card ATM Use • Make sure to know what bank you have money in • Banks Charge you to use their ATM if not their bank • Makes putting in and taking out money easy

Bad Credit can cost you • FICO or credit score rates you and determines the following: • Credit Card Issuers & Lenders check to… • • Auto Insurers • • Determine Premium- bad credit higher premium Employers • • Determine APR per month- higher bad credit or don’t offer you credit Are you a worthy hire? Some jobs don’t allow to hire bad credit employees Landlords • Are you a reliable tenant? Would you rent to someone with bad credit?

The Three Cs of Credit • Character: The way you handle money and have repaid debt in the past. • Capacity: Your ability to pay the debt after considering other monthly expenses. • Capital: The value of your assets or what you own.

Credit Cards – The Perceived Great Equalizer • Credit lets you buy more than you can afford. • Current World Problem • Most people cannot differentiate between wants and needs.

Credit Advice 1. Pay off balance at the end of each month to avoid late fees. • Avoids Late Fees • Avoids Paying Interest - Easiest way to make money is to save money. Don’t waste 2. Maintain a good credit score • Late payments have the biggest negative impact.

Credit Advice cont… • Limit the number of cards you have and apply for • Know your budget • Know yourself and buying habits • Choose a card with a low interest rate- 0% has a catch

Credit Advice cont… 1. Pay more than the minimum - If you have a credit card balance: • Make a plan to pay as much as you can every month • Start with the credit card with the highest interest rate • Pay off the credit cards as quickly as you can

Payday Loans, Cash Advance & Check Cashing • Stay Away! • What is it? • Cash Loan • Extremely High Interest • Short-term (14 – 45 days)

How Do They Work? • You postdate a check • They give you a loan • Loan last for 2 weeks • They charge you a fee for borrowing the money— equivalent APR can be over 300%.

Long-term Effects of Credit • Graduate with: • Student loans • Credit card debt • Affect credit score • Harder to get: • Car loan or insurance • Apartment lease • Mortgage loan • Job

Managing Money in College • Don't spend more money than you have • Divide spending into: • • Needs - Food • Wants - $1, 800 for a spring break trip to Florida Don't pay for the wants unless you can cover the needs

Advice • • Get one credit card • Be an Authorized user on parents’ card • Ask parent to cosign card • Secured Card Pay off the balance every month • • Be aware of intro APRs vs. annual APRs. Don’t take cash advances

Co-signer • Legally responsible to pay consumer debt if borrower defaults • Co-signer: An individual with assets who agrees to repay a loan or consumer debt if the borrower defaults. • Your credit score and report will reflect the co-signers actions to your: • Benefit • Detriment

How to Use Credit Cards to Help You • Pay credit card balance every month • pay credit card bills on time • Apply for credit only when needed • Keep track of all charges- keep receipts • Check monthly credit card statements

How credit could hurt you? • Making late payments- could trigger higher rates and hurt credit score • Paying only the minimum- costs you money in interest in the long run • Don’t Exceed the cards limit- triggers a penalty fee • Don’t Charge items that cannot be paid off in foreseeable future • Don’t Own too many credit cards

Your credit history describes how you use money • If you have a credit card or a loan from a bank, you have a credit history. Companies collect information about your loans and credit cards. Do you pay your bills on time? How many loans do you have? How many credit cards do you have? • Companies also collect information about how you pay your bills. They put this information in one place: your credit report.

Credit / FICO Score • FICO- Fair Isaac Company • Range between 300 & 850 • U. S. Median: 723 in 2014 • < 620 = sub prime • > 760 = best rates

• A credit score is a number. It is based on your credit history. • A high credit score means you have good credit. A low credit score means you have bad credit. Different companies have different scores. Low scores are around 300. High scores are around 700 -850.

The Cost of Borrowing Your Credit score: Your interest rate: Your monthly payment: 760 - 850 6. 13% $1, 313 700 - 759 6. 35% $1, 344 680 - 699 6. 53% $1, 369 660 - 679 6. 74% $1, 400 640 - 659 7. 17% $1, 462 620 - 639 7. 72% $1, 543 © 2006 Consumer Jungle

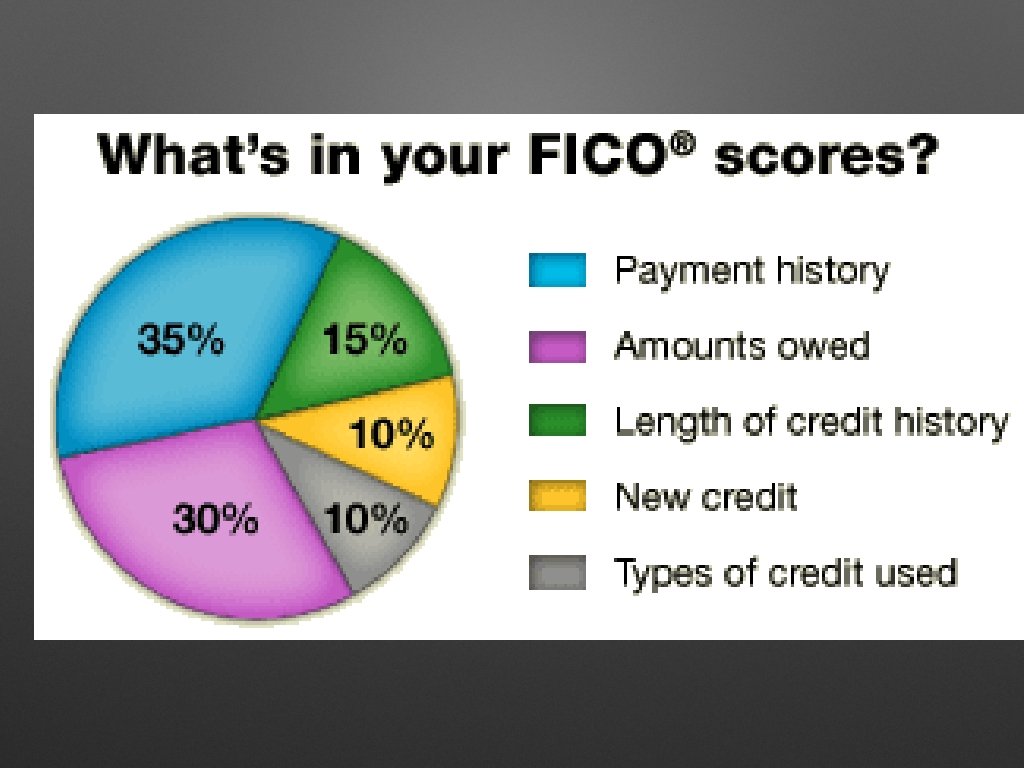

35% Payment History • Late payments have the greatest negative impact on your credit score. • You prove if you are good or bad! • Recency & frequency are important to creditors too.

30% Outstanding Balances • FICO- Looks at Total balance vs. total available credit • Are you overextended? Can you go further into debt? • Do you have too much credit to give more?

15% Length of Credit History • FICO measures: Number of years you’ve used credit. • It is important that you start using credit early and using it wisely. • The longer you’ve had credit the better • How long since you’ve used certain accounts.

10% New Credit • FICO Tracks: Number of new accounts you open • If you opened multiple new accounts at one time makes it look like you plan on going into debt • Even Multiple credit requests reduce your score.

10% Types of Credit • FICO wants a Mix of: • Open/Revolving Credit • • Credit cards & Installment Credits • Car loan • Home loan © 2006 Consumer Jungle

How to Improve Your Score • Pay all bills on time. • Pay any delinquent bills. • Lower your total credit card debt. • Don’t close unused credit cards. • Don’t open up new credit cards to increase available credit.

Do I have Credit? ? ? • If you do not have: • a credit card • not gotten a loan from a bank or credit union • Without a credit history, it can be harder to get a job, an apartment, or even a credit card. • You need credit to get credit.

Shopping for card… • Know the Annual Percentage Rate (APR) • Is rate F (Fixed) rate- 15% always • Is rate V (variable) rate 12 -20% • Know the Introductory rate • Length of introductory- use 0% but pay off before the interest kicks in. • What will the rate be after introductory rate

Shopping… • Know Grace Period- Interest-free time between transaction time and bill due date. Statement ends the 30 th, bill due by 21 st of next month. • Usually 20 – 30 days • No grace period if: • Carry a balance • No stated grace period

Shopping • Know Credit Limit- The maximum amount you can charge on a credit account. • • Customer gets denied if you go over limit if you try to purchase something. Recommended limit • 20% of net income

Shopping cont… • Choose a rewards card - a card that gives you rewards you and works for you. • I. E. 1. 5 miles for $1 charged. 100 miles per ticket purchase.

Rewards cont. . . • Pick a rewards card that benefits you • Mileage, cash back, gas, etc. . . • Pay off card at end of month and you get the rewards without costing anything. You can make money off the credit card. • Personal use- Know when and how much you spend

Shopping cont… • Little or no annual fee for young students- Try to have no or small annual fee or you are paying for it. You can use the card for your benefit!!! • Paying for the privilege of using a credit card • Weigh cost of annual fee to value of reward • Mileage • Cash Back • Gas etc. . .

Shopping cont… • Know the Late-Payment Fee- Charge imposed for not paying on time • Know your payment due date & time • Know how you can Pay - U. S. mail, phone, online, automatic bill pay, etc.

Shopping cont… • Know Balance Transfer • • The process of moving an unpaid credit card debt from one issuer to another Shift balances from one card easy? Cost?

Online Banking • All cards Allow you to manage your account online or on phones • Let’s you see monthly statement • Pay online • Tracks rewards

The True Cost of Paying the Minimum Payment Schedule: It will take you 8 years and 1 month to be rid of your debt. In that time, you will pay $470. 32 in interest. Month Minimum Payment Interest Paid Principal Paid Remaining Balance 1 $14. 25 $8. 55 $5. 70 $564. 30 2 $14. 11 $8. 46 $5. 64 $558. 66 3 $13. 97 $8. 38 $5. 59 $553. 07 4 $13. 83 $8. 30 $5. 53 $547. 54 5 $13. 69 $8. 21 $5. 48 $542. 06 6 $13. 55 $8. 13 $5. 42 $536. 64

THE END