COST ACCOUNTING Is a process of recording analysing

Verification: The actual stock in hand must be verified periodically to")

From the following information, calculate Economic order quantity. Semi-Annual Consumption 6, 000")

- Slides: 11

COST ACCOUNTING Is a process of recording, analysing and reporting all of a company's costs (both variable and fixed) related to the production of a product. This is so that a company's management can make better financial decisions, introduce efficiencies and budget accurately. COST ACCOUNTING STANDARD 6 - MATERIAL COST Materials constitute one of the important elements of production. The ICWA has issued Cost Accounting Standard (CAS-6) dealing with Material Cost.

Types of Material Raw Materials: Raw material is a basic/main material used in the manufacture of product. For example sugar cane is the raw material for production of sugar. Cotton is the raw material for production of cotton yarn. Process Materials / Additives: Process materials/additives are materials used in the process of manufacture in addition to raw material. It varies from industry to industry. Process material for sugar industry is lime, or sulphur; in paper industry clay/china clay is the additive material. Bought Out Components: Bought out component means a manufactured product, which forms part of the finished product and is fitted to the product without any further processing, fan belt in an automobile. In other words bought components are purchased items used in the assembly of main product. These item are also available in the market for replacement of worn out parts and known as spare parts.

Sub-assemblies: Sub-assembly means an assembly of various components with a distinct identity, and forms part of the finished product, for example engine, or steering in an automobile. Accessories: Accessories may be either a connponent or sub-assembly, which is not essential for the basic functioning of the product, but supplied as an optional item (for example an air conditioner or music system in an automobile. Consumable Stores: Consumable stores are items used in the maintenance of plant and the like.

Objectives and Advantage Material Control basically aims to ensure that adequate goods are in stock to meet all requirements without carrying unnecessarily large stocks. The main objectives of material control are as follows: l. To avoid under stocking i. e. to provide continuous supply of materials so that the production is not held up. 2. To avoid over-stocking to reduce carrying costs and avoid surplus and obsolete stocks. 3. To obtain materials of the required quality at minimum cost from a reliable source. 4. To minimise the total cost (i. e. ordering costs & carrying costs), 5. To avoid wastages and losses during storage and usage. 6. To maintain proper and up-to-date 7. To provide the required information to the management for taking inventory decisions.

Stock Verification (1) Verification: The actual stock in hand must be verified periodically to prevent theft and frauds. Normally, stock is physically verified at the end of the accounting year for the purpose of Balance Sheet. In case of a large concern, there may be a system of continuous verification of stocks. (2) Reconciliation: The physical stocks so verified must be further reconciled with the balances shown in the Stock Ledger and/or the Bin Cards. Thus, the actual Stock must be reconciled with the Book Stock. The actual stock may be more or less than the book stock. The surplus or the shortages should be investigated thoroughly. The differences may be due to clerical errors in writing the Stock Ledger or errors in taking the physical stock or theft or fraud and so on. The causes for differences may be Abnormal or Normal loss.

Stock Level 1. Meaning : Minimum Level indicates the lowest figure of inventory balance, which must be maintained in hand at all times, so that there is no stoppage of production due to nonavailability of inventory. 2. Factors : The main factors considered for the fixation of minimum level of inventory are as follows: (a) Maximum consumption and maximum delivery period in respect of each item to determine its re-order level. (b) Average rate of consumption for each inventory item. (c) Average re-order for each item. This period can be calculated by averaging the maximum and minimum period. 3. Formula : The formula used for its calculation is as follows: Minimum level of inventory = Re-order level — (Average consumption x Average re-order period)

MAXIMUM LEVEL 1. Meaning : Maximum Level indicates the maximum figure of inventory quantity held in stock at any time. 2. Factors : The important factors which should be considered while fixing the maximum level for various inventory items are as follows: (a) The re-order level which itself is the product of maximum consumption of inventory item and its maximum delivery period. (b) Minimum consumption and minimum delivery period for each inventory item should also be known. (c) The economic order quantity. (d) Availability of funds, storage space, nature of items and their price per unit are also important for the fixation of maximum level.

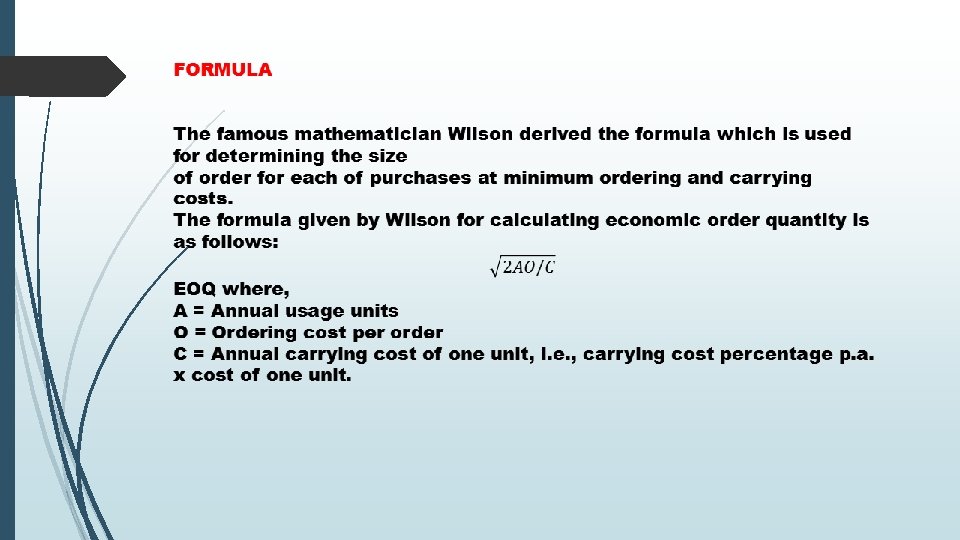

Re-Order Reorder level lies between minimum and the maximum levels in such a way that before the material ordered is received into the stores there is sufficient quantity on hand to cover both normal and abnormal consumptions situation. In short level at which fresh order should be placed for replenishment of stock. Economic order Quantity Economic order quantity, or EOQ, is a calculation designed to find the optimal order quantity(Optimum Level) for businesses to minimize logistics costs, warehousing space, stock outs, and overstock costs. Carrying Cost: Carrying costs are the various costs a business pays for holding inventory in stock. Examples of carrying costs include warehouse storage fees, taxes, insurance, employee costs, and opportunity costs. Ordering Cost: order costs include the costs of preparing a requisition, a purchase order, and a receiving ticket, stocking the items when they arrive, processing the supplier's invoice, and remitting the payment to the supplier.

Q 1) From the following information, calculate Economic order quantity. Semi-Annual Consumption 6, 000 units Purchase price of input unit 25 Ordering cost per order 45 Quarterly carrying cost 3% Q 2) G. Ltd. produces a product which has a monthly demand of 4, 000 units. The product require a component X which is purchased at 20. For Every finished product, one unit of component is required. The ordering cost is 120 per order and the holding cost is 10%p. a. You are required to calculate the Economic order quantity.

Stock Ledger on FIFO and WEIGHTED AVERAGE From the following, Prepare Stock record by FIFO and weighted average Method Date 04 -1 -2014 17 -1 -2014 20 -1 -2014 22 -1 -2014 25 -1 -2014 28 -1 -2014 30 -1 -2014 31 -1 -2014 Transaction Units Rate Purchase Sale 40 60 50 80 80 20 100 90 30 28 35 29 33 34 26 35