Corporate Governance LECTURE 3 BOARDS AND SHAREHOLDERS Boards

Corporate Governance LECTURE 3: BOARDS AND SHAREHOLDERS

Boards Where the major decisions are made, hopefully. Acting as shareholders’ agents Two main types Two tier Unitary

Two Tier Boards Common across Europe Executive Board – which makes operational decisions Supervisory board – which oversees executive board Sets strategic direction All non-executive members Chairman of executive board will attend as non-executive Can include workers representatives and other stakeholders

(managing Director), Chief Finance Officer")

Unitary Boards The Anglo-Saxon model Chairman, Chief Executive Officer (CEO)(managing Director), Chief Finance Officer (CFO)(Finance Director), Other executive positions (such as Marketing Director, Sales Director), Non-Executive Directors. Although, strictly speaking the CEO is the chief executive that reports to the board of directors, and all directors are equal – the executive function is a separate job The Chairman is chairman of the board of directors, not of the company

Does the Board act well? Carey suggested that there can be a successful Board but there also The Rubber Stamp The Dreamers The Talking Shop The Adrenalin Groupies The Number Crunchers The Semi-Detached

Boards spend too much time managing,")

A fish rots from the Head Garratt (1996) Boards spend too much time managing, not enough time directing Garratt suggests this problem is inevitable with executives on the board Problems with lack of clarity over objectives of board Lack of checks and balances

Board functions – originally from ACCA 1. Boards, shareholders and stakeholders share a common understanding of the purpose and scope of corporate governance 2. Boards lead by example 3. Boards appropriately empower executive management and committees 4. Boards ensure their strategy actively considers both risk and reward over time 5. Boards are balanced

Balanced Boards Roles of Chief executive and chairman split Non-Executive directors Diversity

Non-executive directors have four broad responsibilities: to provide advice and")

Non-Executive directors (Tyson report) Non-executive directors have four broad responsibilities: to provide advice and direction to a company’s management in the development and evaluation of its strategy; to monitor the company’s management in strategy implementation and performance; to monitor the company’s legal and ethical performance; and to monitor the veracity and adequacy of the financial and other company information provided to investors and other stakeholders. As part of their monitoring responsibilities over company management, NED directors are responsible for appointing, evaluating and where necessary removing senior management, and for succession planning for top management positions.

“no crooks, no cronies, no cowards” NEDs drawn from limited pool in US with many interlocking Independent directorships Monitoring/advisory role can cause confusion Mixed data on effectiveness (partly due to starting point of research) but US and UK governments committed to expanding role Higgs report proposed NEDs make up 40 per cent of board and work with institutional shareholders Radical for its time and met strong opposition Tyson Report also proposed increasing diversity to engage with different stakeholders

How ethical should boards be? ACCA point 2 Boards lead by example Boards should set the right tone and behave accordingly, paying particular attention to ensuring the continuing ethical health of their organisations. Directors should regard one of their responsibilities as being guardians of the corporate conscience; non-executive directors should have a particular role in this respect. Boards should ensure they have appropriate procedures for monitoring their organisation’s ‘ethical health’. What should govern ethics? Is morality different?

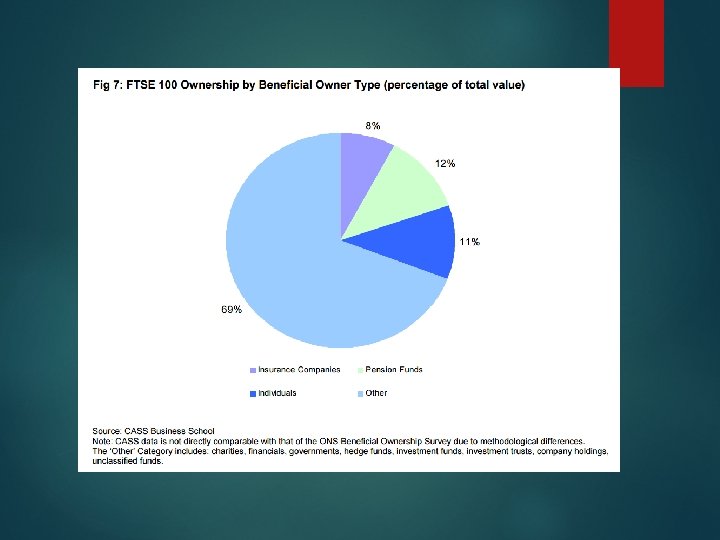

Who are the Shareholders Rest of the world Insurance companies Pension funds Individuals Other 1963 1975 1981 1991 2008 2010 7 5. 6 3. 6 12. 8 35. 7 41. 5 41. 2 10 6. 4 54 22. 6 15. 9 16. 8 37. 5 24. 2 20. 5 26. 7 28. 2 21 20. 8 31. 3 19. 9 15. 2 20 16. 1 14. 8 13. 4 12. 8 10. 2 22. 1 8. 6 5. 1 11. 5 33. 6

Decline")

Shareholders Rise, and then decline of institutional investors (pension funds and insurance companies) Decline of individual share ownership Rise of international ownership Rise of others (charities, financials, governments, hedge funds, investment trusts, company holdings, unclassified funds)

What are the goals of these shareholders? Investment Speculation What is the difference from investment? What level of interest might they have in the company

Institutional investors Not strictly the shareholders Real shareholders are the clients I. e Pension contributors Thus pension fund manager is the agent of the ultimate shareholder This gives an additional agency problem In pension funds, pension fund trustees are entrusted with assets They have a fiduciary duty to maximise returns for owners (contributors) They delegate to the pension fund

So how do they act? It is often said that trustees put fund managers under undue pressure to maximise short-term investment returns, or to maximise dividend income at the expense of retained earnings; and that the fund manager will in turn be reluctant to support board proposals which do not immediately enhance the share price or the dividend rate. Evidence to support this view is limited (particularly in relation to dividends), but we urge trustees to encourage investment managers to take a long view. (Hampel Report)

A new corporate governance problem? Corporate governance in institutional investment is under question Leads to problems between Companies and investors ‘In the last five years, there has been a wide erosion of trust in financial intermediaries and in the financial system as a whole. This erosion is not a result of misplaced public perception, which can be addressed by a public relations campaign; it is based on observation of what has happened. That erosion of trust is the long-term consequence of the systematic and deliberate replacement of a culture based on relationships by one based on trading increasingly characterised by anonymity, and the behaviours which arise from that substitution. In the context of asset management, trust implies stewardship. ’ (THE KAY REVIEW OF UK EQUITY MARKETS AND LONG-TERM DECISION MAKING 2012)

Stewardship The concept of stewardship originates in the responsibilities of a steward as manager of a household or estate, and the historic analogy is apt. The essential characteristics of the steward are understanding and engagement – understanding the needs and expectations of those with whom the steward deals, and engagement with those who meet these needs and discharge the expectations of the principals. Trust and respect are key to the role of the honest steward. The honest steward expects to be rewarded for the discharge of that trust, but on a basis of full disclosure and only on that basis. Analysis and engagement are the characteristics which […] we sought in asset managers, and we would equally look for in company directors and asset holders. The Review believes that stewardship should be key to the equity investment chain. (Kay Report)

Kay’s Remit In June 2011, the Secretary of State for Business, Innovation and Skills asked me to review activity in UK equity markets and its impact on the long-term performance and governance of UK quoted companies. The Review’s principal concern has been to ask how well equity markets are achieving their core purposes: to enhance the performance of UK companies and to enable savers to benefit from the activity of these businesses through returns to direct and indirect ownership of shares in UK companies.

Overall we conclude that short-termism is a problem in UK equity markets, and that the principal causes are the decline of trust and the misalignment of incentives throughout the equity investment chain. These themes of trust and incentives are central to this report. We set out principles that are designed to provide a foundation for a long-term perspective in UK equity markets and describe the directions in which regulatory policy and market practice should move.

Short-termism in business may be characterised both as a tendency to under-investment, whether in physical assets or in intangibles such as product development, employee skills and reputation with customers, and as hyperactive behaviour by executives whose corporate strategy focuses on restructuring, financial re-engineering or mergers and acquisitions at the expense of developing the fundamental operational capabilities of the business. We observe a wide variety of examples of companies that have made bad long-term decisions, and consider that equity markets have evolved in ways that contribute to these errors of managerial judgment. We conclude that the quality – and not the amount – of engagement by shareholders determines whether the influence of equity markets on corporate decisions is beneficial or damaging to the long-term interests of companies. And we conclude that public equity markets currently encourage exit (the sale of shares) over voice (the exchange of views with the company) as a means of engagement, replacing the concerned investor with the anonymous trader. UK equity markets are no longer a significant source of funding for new investment by UK companies. Most publicly traded UK companies generate sufficient cash from their day-to-day operations to fund their own corporate projects. The relatively small number of UK companies which access the new issue market often use it as a means to achieve liquidity for early stage investors, rather to raise funds for new investment. We conclude that the principal role of equity markets in the allocation of capital relates to the oversight of capital allocation within companies rather than the allocation of capital between companies. Promoting good governance and stewardship is therefore a central, rather than an incidental, function of UK equity markets.

Restore relationships of trust and confidence in the investment chain, underpinned by the application of fiduciary standards of care by all those who manage or advise on the investments of others Emphasise the central function of trust relationships in financial intermediation and diminish the current role of trading and transactional cultures Address the disincentives to engagement by asset managers with investee companies that arise from fragmented shareholding Improve the quality of engagement by investors with companies, emphasising and broadening the existing concept of stewardship Increase incentives to such engagement by encouraging asset managers to hold more concentrated portfolios judged on the basis of long-term absolute performance Reduce the pressures for short-term decision making that arise from excessively frequent reporting of financial and investment performance (including quarterly reporting by companies), and from excessive reliance on particular metrics and models for measuring performance, assessing risk and valuing assets

In other words Running against the idea of shareholder value maximisation Putting in place rules to reduce it Reducing reporting to make short-termism less likely Unpicks the idea of anonymous agents and seeking to reinforce the social element into equity markets Not a ‘free’ market as conventionally seen – a substantial shift in philosophy

- Slides: 24