Corporate Finance MLI 28 C 060 International Finance

• Douglas North: ”Institutions are the humanly devised constraints that structure")

- Inquisitorial")

• Manner of legal reasoning - Civil-Law")

• Judges - Role in trials. *")

")

do we raise finance? •")

- First offering of stock to the general")

- Slides: 37

Corporate Finance MLI 28 C 060 International Finance: Institutions and legal systems Lecture 9 Thursday 20 October 2016

How institutions and legal system shape financing and economic activity

What are institutions? • Institutions are the humanly devised constraints that structure political, economic and social interaction. They consist of both informal constraints (sanctions, taboos, customs, traditions, codes of conduct), and formal rules (constitutions, laws, property rights) • D. C. North, The Journal of Economic Perspectives, 1991.

Institutions defined (again) • Douglas North: ”Institutions are the humanly devised constraints that structure human interaction. They are made up of formal constraints 1, informal constraints 2 and their enforcement characteristics. Together they define the incentive structure of societies and specificially economies”. – 1) rules, laws, constitutions – 2) norms, behavior, conventions • … or simply ’the rules of the game’

• What are institutions? “Institutions are the rules of the game in a society; are the humanly devised constraints that shape human interaction” (North 1990, p. 3); Economic, political and social Interactions • Informal institutions - informal constraints: sanctions, taboos, customs, tradition and code of conduct; • Formal institutions - formal rules: constitutions, laws, property rights;

Hierarchy based classification Level Example 1 Institutions related to the social structure of the society Mainly informal institutions such as traditions, social norms, and customs 2 Institutions related to rules of the game Mainly formal rules defining property rights and the judiciary system 3 Institutions related to the play of the game Rules defining the governance structure of a country and contractual relationships such as business contracts 4 Institutions related to allocation mechanisms Rules related to resource allocation such as capital flow controls, trade flow regimes and social security systems

Why civil society is key – Institutional and normative set-up of international finance Figure: Ideal influence patterns

Why civil society is key – Institutional and normative set-up of international finance Figure: Actual influence patterns

Why civil society is key – Institutional and normative set-up of international finance • Why legitimacy is important: – The legitimacy of the governance system in place becomes a positive and negative reinforcer that magnifies the effects of efficacy and effectiveness on performance and vice versa.

Differences in Legal system Civil Code vs. Common Law

• Features of Civil Code law (as opposed to common law) - Inquisitorial (vs. accusatorial) - Code-based (vs. case law) - History: Roman Law - Branches: public / private – criminal / civil - Career judges - Written proceedings (vs. oral proceedings)

Comparison of Civil-Law and Common-Law Systems (III) • Manner of legal reasoning - Civil-Law → Deductive - Common-Law → Inductive • Structure of Courts - Civil-Law → Integrated Court system - Common-Law → Specialty Court system • Trial process - Civil-Law → Extended process - Common-Law → Single-event trial

Comparison of Civil-Law and Common-Law Systems (IV) • Judges - Role in trials. * Civil-Law → elevated role * Common-Law → «referee» - Judicial attitudes. *Civil-Law → mere appliers of the law * Common-Law → search creatively for an answer - Selection and training. * Civil-Law → a part of the civil service * Common-Law → selected from a political process

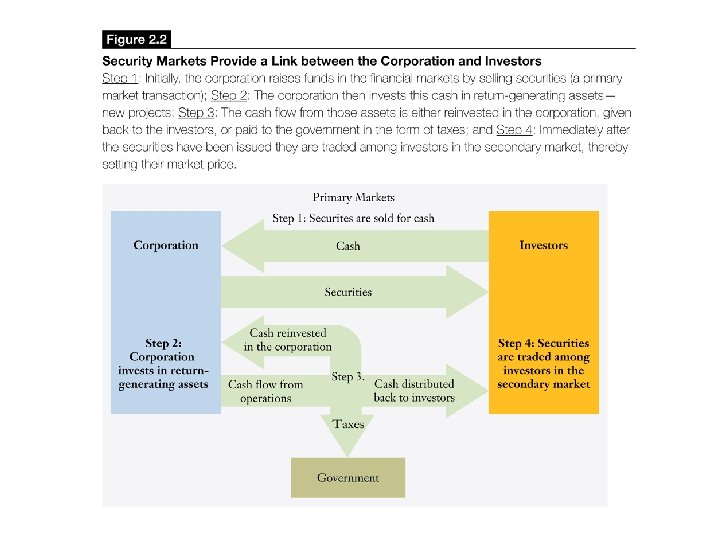

Primary and Secondary financial markets and IPO underpricing

Types of Securities: Debt securities • Debt Securities: Firms borrow money by selling debt securities in the debt market. – If the debt has a maturity of less than one year, it is typically called notes, and is traded in the money market. – If the debt has a maturity of more than one year, it is called bond and is traded in the capital market. • Most bonds pay a fixed interest rate on the face or par value of bond. • Example: A bond with a face value of $1, 000 and semi-annual coupon rate of 9% will pay an interest of $45 every 6 months or $90 per year, which is 9% of $1, 000. When the bond matures, the owner of the bond will receive $1, 000.

Figure: Bond certificate with coupons

Types of Securities: Equity securities • Equity securities represent ownership of the corporation. • Common stock is a security that represents equity ownership in a corporation, provides voting rights, and entitles the holder to a share of the company’s success in the form of dividends and any capital appreciation in the value of the security. – Common stockholders are residual owners of the firm. They earn a return only after all other security holder claims (debt and preferred equity) have been satisfied in full. – Dividend on common stock are neither fixed nor guaranteed. Thus, a company can choose to reinvest all of the profits in a new project and pay no dividends. • Preferred stock is an equity security. However, preferred stockholders have preference with regard to: – Dividends: They are paid before the common stockholders. – Claim on assets: They are paid before common stockholders if the firm goes bankrupt and sells or liquidates its assets.

Figure: Share Certificate ( “Ordinary” CERTIFICATES)

Preferred stock • Preferred stock is also referred to as a hybrid security as it has features of both common stock and bonds. • Preferred stock is similar to common stocks in that: – It has no fixed maturity date, – The nonpayment of dividends does not result in bankruptcy of the firm, and – The dividends are not deductible for tax purposes. • Preferred stock is similar to corporate bonds in that: – The dividends are typically a fixed amount, and – There are no voting rights.

So……. there are 2 questions: • 1: where (location) do we raise finance? • 2: what type of finance do we use?

• Firms almost always exhaust internal sources of capital first before considering external sources – why? • Answer: Internal sources draw on ”Internal Capital Market” within firm and it’s network (network in case of business groups or family firms)

• Entrepreneurial firms – lifecycle: – Internal sources exhausted by entrepreneur (friends, family and business groups in case of network economies) – Then Business Angels (BA) early stage investors – Then Venture Capital (VC) – The ultimate goal/aim is for firm to achieve a stock market IPO (Intitial Public Offering)

• Normally after internal sources bank finance/lending is preferable to external capital markets – why? • One answer is ”informational” i. e. – For a firm to issue bonds to external investors there are huge costs in terms of auditing, accounting transparency, issuing prospectuses etc – This is in order to provide investors with confidence through firm incurring ”bonding costs” as in bonding with investors – Alternative is bank lending – with relationship with bank mitigating informational costs

• Bank lending is also a useful indicator to investors – i. e. if banks continue to supply credit to firm then given their close relationship – this is a good sign of credit-worthiness of firm – The presence of banking relationships thus impacts positively on value of firm’s equity and debt (bonds)

• Now………. Where do firm’s raise finance: • This has everything to do with costs of debt and costs of equity – This is the subject of tommorow’s (Friday’s) lecture

The importance of stock markets as a source of capital

Stock Markets • A stock market is a public market in which the stocks of companies is traded. • Stock markets are classified as either organized security exchanges or over-the-counter (OTC) market. • Organized security exchanges are tangible entities; that is, they physically occupy space and financial instruments are traded on their premises. For example, the New York Stock Exchange (NYSE) is located at 11 Wall Street in Manhattan, NY. The total value of stocks listed on the NYSE fell from $18 trillion in 2007 to just over $10 trillion at the beginning of 2009. • The over-the-counter markets include all security market except the organized exchanges. NASDAQ (National Association of Securities Dealers Automated Quotations) is an over-thecounter market and describes itself as a “screen-based, floorless market”. In 2009, nearly 3, 900 companies were listed on NASDAQ, including Starbucks, Google, Intel.

Initial Offering Initial Public Offering (IPO) - First offering of stock to the general public. Underwriter - Firm that buys an issue of securities from a company and resells it to the public. Spread - Difference between public offer price and price paid by underwriter. Prospectus - Formal summary that provides information on an issue of securities. Underpricing - Issuing securities at an offering price set below the true value of the security.

Example of IPO listing process – Manila, Philippines

Motives For An IPO Percent of CFOs who strongly agree with the reason for an IPO To create public shares for use in future acquisitions 59. 4 To establish a market price/value for our firm 51. 2 To enhance the reputation of our company 49. 1 To broaden the base of ownership 45. 9 To allow one or more principals to diversify personal holdings 44. 1 To minimize our cost of capital 42. 5 To allow venture capitalists to cash out 32. 2 To attract analysts' attention 29. 8 Our company has run out of private equity 27. 6 Debt is becoming too expensive 14. 3 0 10 20 30 40 50 60 70

Average Initial IPO Returns

Initial Offering Average Expenses on 1767 IPOs from 1990 -1994

General Cash Offers Seasoned Offering - Sale of securities by a firm that is already publicly traded. General Cash Offer - Sale of securities open to all investors by an already public company. Shelf Registration - A procedure that allows firms to file one registration statement for several issues of the same security. Private Placement - Sale of securities to a limited number of investors without a public offering.

Total Direct Costs of Raising Capital