Compliance update EARLEEN MOULTON VP COMPLIANCE BRIDGEFORCE FINANCIAL

Compliance update EARLEEN MOULTON VP COMPLIANCE, BRIDGEFORCE FINANCIAL GROUP

Agenda • How are your compliance programs coming along? • What’s new in the world of compliance

How do you eat an elephant?

“When eating an elephant take one bite at a time” Creighton Abrams

Start here:

Mandatory Compliance Regime 1. Appointment of Compliance Officer 2. Development, application and maintenance of up-to-date written policies and procedures. 3. Documented risk assessment 4. Ongoing training program for staff 5. Regular review of policies and procedures (at least every 2 years) – “self assessment” CAILBA 2016

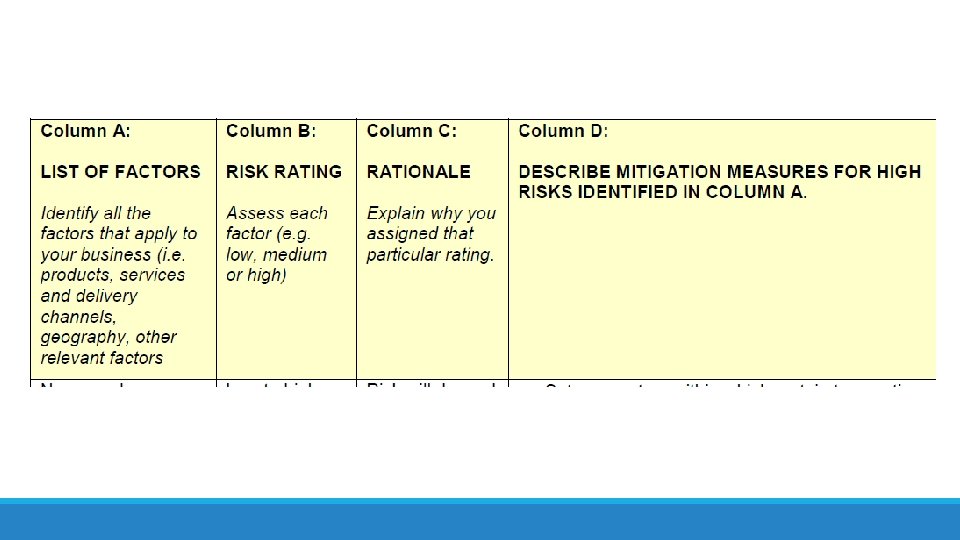

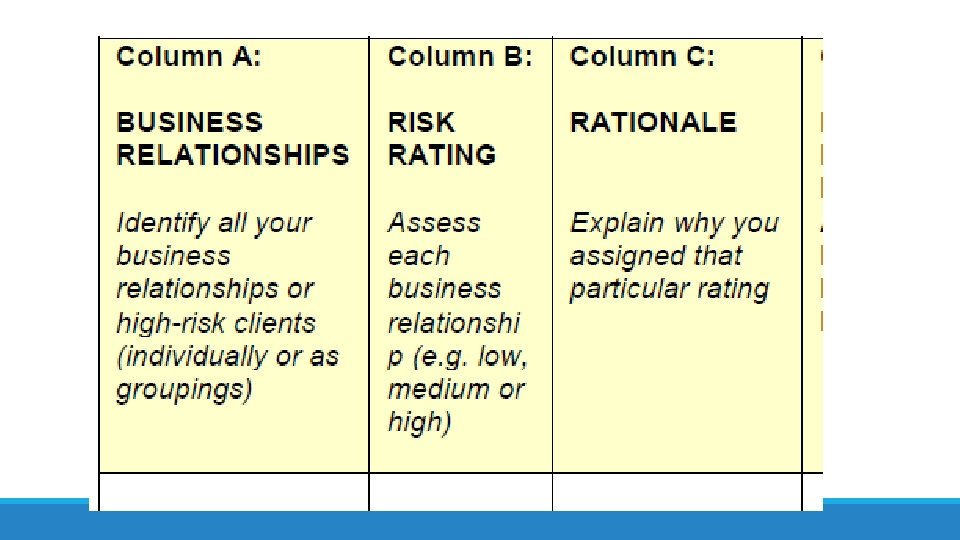

Expectation “FINTRAC expects a well-developed, documented and justifiable RBA process that appropriately identifies, rates, and mitigates the risks to a given entity. ”

Risk-based approach cycle 1. Identification of your inherent risks (business-based risk assessment along with the relationship-based risk assessment) 2. Setting your risk tolerance 3. Creating risk-reduction measures and key controls 4. Evaluating your residual risks 5. Implementing your risk-based approach 6. Reviewing your risk-based approach.

Your obligation The PCMLTF Act and Regulations state that you/your organization has mandatory obligations in situations where high-risk business activities and high-risk business relationships are identified. This step does not allow reporting entities to avoid these obligations.

Expectations For all situation and all clients: • Internal controls to mitigate overall risks (training, servicing clients, keep your compliance program up to date) • Conduct on-going monitoring, keep a record of what and how For high-risk business and client relationships: • Document measures to mitigate risk • Conduct more frequent monitoring of high-risk relationships • Enhance measures to ascertain ID, keep client information up to date

“The best way to get something done is to begin”

Compliance meeting presentations

What’s going on in the world of compliance?

Anti-money laundering & combating terrorist financing • FINTRAC imposes an administrative monetary penalty on Becksley Capital Inc. , in Toronto • Canadian bank fined $1. 1 -million for failing to report suspicious transaction

Why the $28, 500 fine? Becksley Capital Inc. was found to have the following deficiencies: -Inadequate written ongoing compliance training program; -Failure to institute and document the prescribed two year review; and -Failure to take reasonable measures when opening an account to determine if it will be used by or on behalf of a third party.

are the")

Cybersecurity in the news • Pw. C report: Employees (current and past) are the main source of cyber incidents; 34% for financial services firms • Employee training and awareness is a key defense – from top to bottom • Manage cyber security risks • ‘These risks can result in the loss of data and business disruption, making the implementation of cybersecurity measures imperative’.

Proposed regulation of financial planning The Ontario government’s expert panel announced preliminary policy recommendations • financial planning be regulated • financial advice should be subject to a statutory fiduciary duty • Look for report/commentary from Ministry of Finance, Advocis, FPSC • Attend town hall meetings ‘US Department of Labor Finalizes Rule to Address Conflicts of Interest in Retirement Advice, Saving Middle-Class Families Billions of Dollars Every Year’ • Establishes fiduciary role for advisors

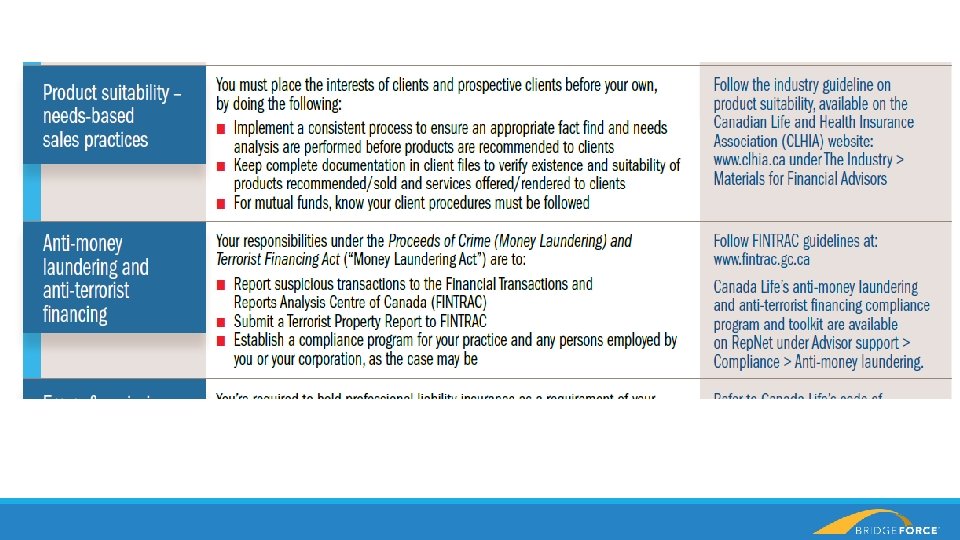

FSCO March newsletter highlights • Non-sponsored life insurance agents must indicate a primary insurance company • Update your email address with FSCO to receive licence renewal notifications • Importance of selecting suitable insurance products that meet the needs of the client, use needs analysis, retain written documentation on file… that clearly demonstrate how the product is suitable for the client

CLHIA paper on insurance distribution Insurance Distribution in Canada: promoting a customer-focused system A. Customers expect knowledgeable and ethical advisors B. Customers purchase suitable products and understand their purchase C. Remuneration models foster FTC outcomes, conflicts minimized & disclosed D. Consumers expect ongoing service & information on policies; have a right to appoint a preferred advisor

Watch for a ‘Compliance News’ email in your in-box for more information

Questions?

- Slides: 24