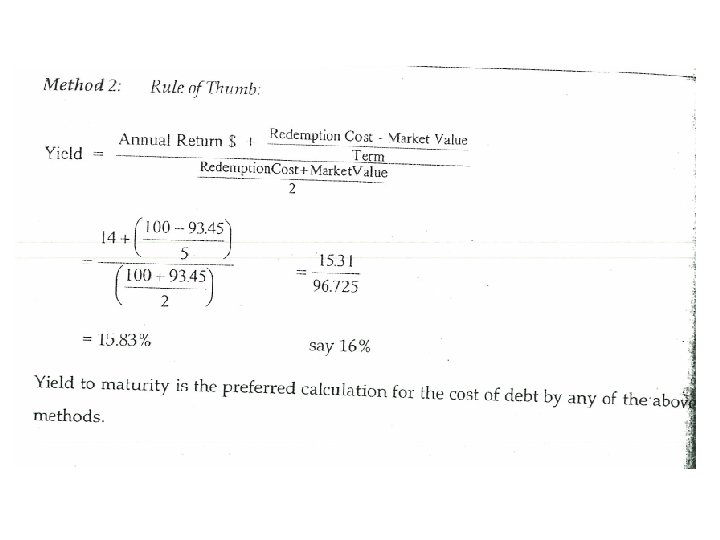

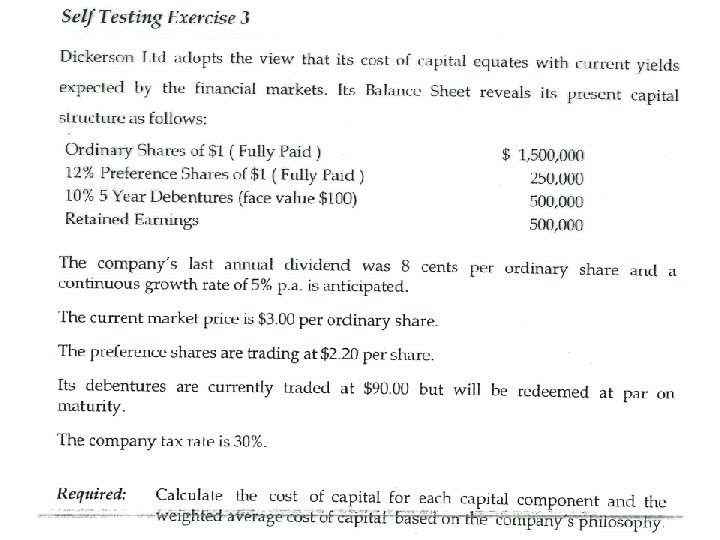

Company could redeem them that is buy them

Company could redeem them – that is buy them back today at $93. 45 or make 5 interest payments of $14 each year plus redeem them at face value of $100 in five years time

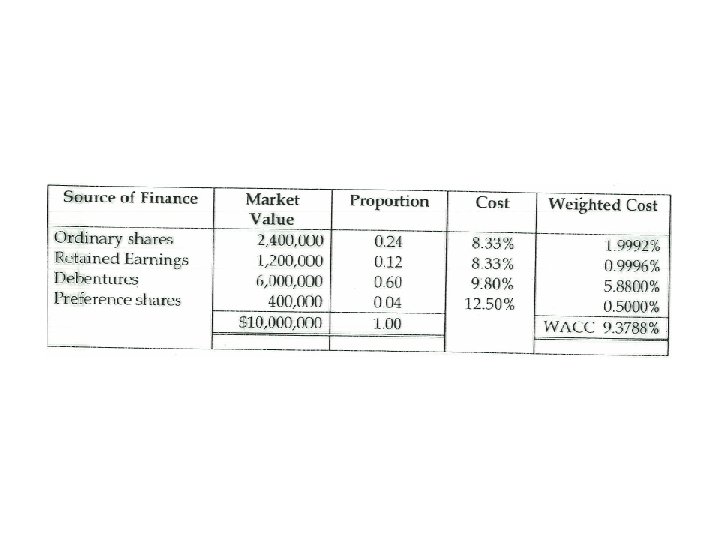

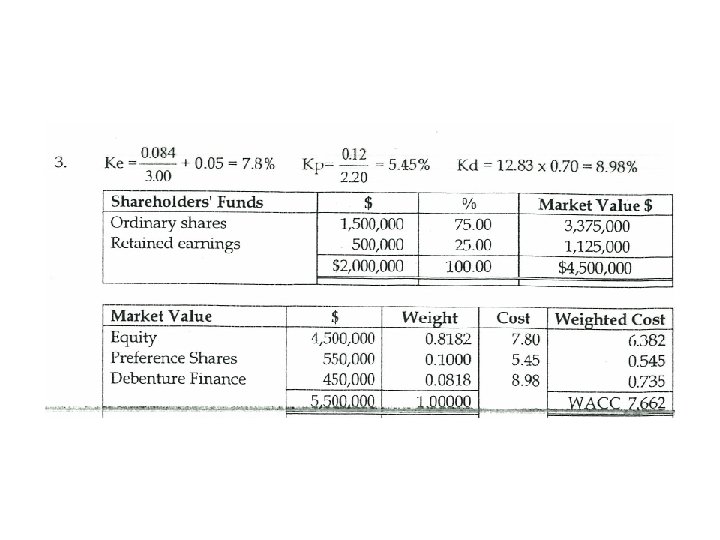

We could have combined Ord Shares and Retained Earnings but if the question asked us to separate them then we should Balance Sheet Values 2000, 000 x Market value of shares 3. 60 = $3, 600, 000

Past Exam Papers…

Testing theory behind using WACC rates for investment criteria Example 1 Assets = Equity Shares only 100, 000 = 100, 000 Shareholders looking for 10% return and shares currently trading at $1 So dividend will be. 10 per share or $10, 000 in total Therfore our assets need to produce a NPAT of $10, 000 Note income before tax = 10, 000 /. 7 = $ 14, 285. 72 Less Tax $ 4, 285. 71 Profit After tax $ 10, 000. 00 My theory is when working out the minimum requirement rate for our investments or capital expenditure we should get the WACC and divide by. 7 , that is we need a return on Assets before tax of 10 /. 7 = 14. 2857%

Example 2 - same as example 1 except we have $50, 000 shareholders and a $50, 000 mortgage at 10% Assets = Equity + Liabilities 100, 000 = 50, 000 + 50, 000 WACC calc is 50% of 10% + 50% of (10% x 0. 7) = 8. 5% So WACC says Assets only have to earn 8. 5% return or $8500, but again I think it should be 8500 /. 7 = Revenue before tax 12143 Assume interest was the only expense we had to cover before tax , therefore we need a profit after tax of $5000 for our shareholders then to have a profit after tax of $5000 we need to earn 5000 /. 7 = 7143 before tax + profit required to cover shareholders dividend after tax - $5000 Proof So Revenue would be $5000 + 7143 = $ 12, 143. 00 Less Expenses - Interest $ 5, 000. 00 Profit before tax $ 7, 143. 00 Less Tax $ 2, 142. 90 Profit After tax $ 5, 000. 00

- Slides: 25