Classification of Taxes Classification of Taxes Single and

- Slides: 16

Classification of Taxes

Classification of Taxes: Ø Single and Multiple Taxes Ø Proportional, Progressive, Regressive Degressive Taxes Ø Ad Valorem and Specific Taxes Ø Direct Taxes and Indirect Taxes. and

Single and Multiple Taxes �Single Taxes: single tax means that only one tax is levied in the country. The incidence of single tax system is equitably spread across different sections of the society in terms of their ability to pay. �Multiple Tax: multiple taxation system is that system in which several taxes, such as income tax, sales tax etc are levied simultaneously. This system is more flexible,

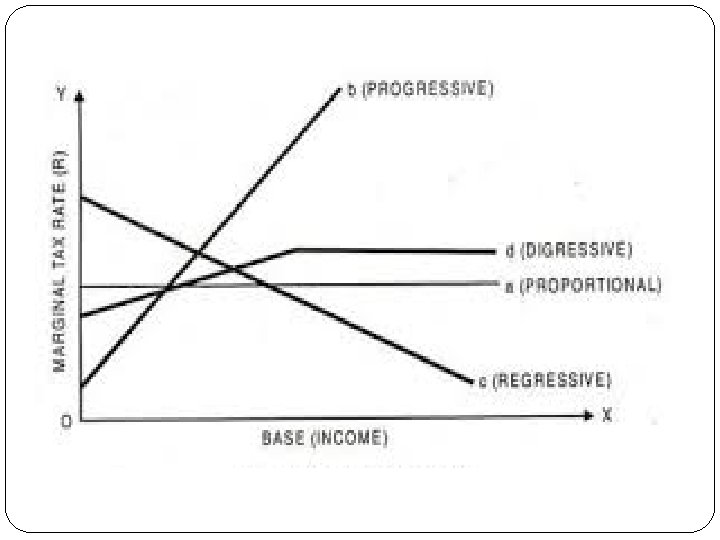

On the basis of degree of progression of tax, it may be classified into: �Proportional tax �Progressive tax �Regressive tax �Degressive tax

Ø Proportional tax A tax is called proportional when the rate of taxation remains constant as the income of the tax payer increases. In this system all incomes are taxed at a single uniform rate, irrespective of whether tax payer’s income is high or low. The tax liability increases in absolute terms, but the proportion of income taxed remains the same.

Ø Progressive tax �When the rate of taxation increases as the tax payer’s income increases, it is called a progressive tax. In this system, the rate of tax goes on increasing with every increase in income.

Ø Regressive taxation A regressive tax is one in which the rate of taxation decreases as the tax payer’s income increases. Lower income is taxed at a higher rate, whereas higher income is taxed at a lower rate. However absolute tax liability may increase.

Ø Degressive taxation A tax is called degressive when the rate of progression in taxation does not increase in the same proportion as the increase in income. In this case, the rate of tax increases up to a certain limit, after that a uniform rate is charged. Thus degressive tax is a combination of progressive and proportional taxation. This type of taxation is often used in case of income tax. This is the case of income tax in India as well.

Taxes can be classified into various types on the basis of form, nature, aim and method of taxation. the most common and traditional classification is to classify into direct and indirect taxes. �Direct Tax �Indirect tax

Ø Direct taxes A direct tax is that tax whose burden is borne by the same person on whom it is levied. The ultimate burden of taxation falls on the person on whom the tax is levied. It is based on the income and property of a person. Thus income tax, corporation tax on company’s profits, property tax, capital gains tax, wealth tax etc are examples of direct taxes. Ø Indirect taxes An indirect tax is that tax which is initially paid by one individual, but the burden of which is passed over to some other individual who ultimately bears it. It is levied on the expenditure of a person. Excise duty, sales tax, custom duties etc are examples of indirect taxes.

Merits of direct taxes Merits of Indirect Taxes Progressive Tax Convenient Economy Less evasion Certainty Variety Elastic Check on harmful consumption Productive Broad base Simple Protection from foreign competition

Demerits of direct taxes Demerits of Indirect Taxes Unpopular Regressive Evasion of Taxes Uncertain Difficulties regarding payment Uneconomical Lack of public spirit Adverse effect on foreign capital Less production Narrow base Discourage savings

Ad valorem and specific tax: �Ad valorem tax or VAT: this type of indirect tax is one of the major source of revenue to the state. VAT is imposed on value added at various stages of production or value adding. Value added= value of output- value of intermediate consumption VAT may be levied in three possible ways: �Central Levy �State Levy �Dual VAT.

Specific Tax: �When a tax is levied on a commodity on the basis of its units, size or weight it is called specific test. The merit of this tax is that it is convenient and simple. but demerit is that its effect is less on the rich and more on the poor people of the country.

THANK YOU!