Classes of External Decisions Investment Decisions Distribution Decisions

Classes of External Decisions Investment Decisions Distribution Decisions

Investment decision = sacrificing current wealth for increased wealth in the future. Wealth = command over good and services.

Features of Investment Decisions 1. Investment alternatives associated with a stream of expected economic consequences example: 2. Expected consequences are uncertain example: 3. Expected consequences differ in timing and magnitude example:

Assumptions Underlying Our Decision Model 1. Expected consequences can be expressed in terms of money flows 2. Expected cash flows are certain 3. No decision constraints

24, 000 (. 25 -. 11) 24, 000 -4, 500")

(. 25 -. 10) 24, 000 (. 25 -. 11) 24, 000 -4, 500 =3, 600 =3, 360 (. 25 -. 12)24, 000 =3, 120 Chevy |___________|_______| 1 2 (. 25 -. 08)24, 000 -6, 900 Fiat =4, 080 3 (. 25 -. 07) 24, 000 =4, 320 (. 25 -. 06) 24, 000 =4, 560 |___________|_______| 1 2 3

Savings. Chevy 10, 080 - Costs = 4, 500 = Fiat 6, 900 12, 960 - = Net Savings 5, 580 6, 060 Savings Per Year 1, 860 2, 020 Decision: Choose ________

= the rate of return")

Time preference rate = f (opportunity rate of return) = the rate of return you require for giving up the use of money for a period of time.

Opportunity Set Passbook savings Money market accounts Tax exempts Junk bonds Stocks

1(1 +. 10) = 1. 10")

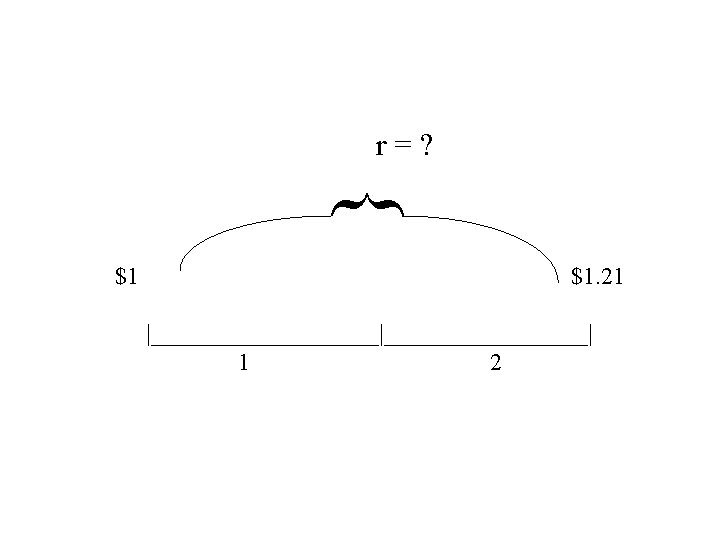

Assume r = 10% $1 + $1(. 10) 1(1 +. 10) = 1. 10 -$1 1

![1(1 +. 10) + [1(1 +. 10)]. 10 = 1(1 +. 10) -$1 1(1](http://slidetodoc.com/presentation_image_h2/7b616db8aa9e90900d7a78fb43d4a67c/image-10.jpg "1(1 +. 10) + [1(1 +. 10)]. 10 = 1(1 +. 10) -$1 1(1")

1(1 +. 10) + [1(1 +. 10)]. 10 = 1(1 +. 10) -$1 1(1 +. 10) = 1(1 +. 10)² = 1. 21 1 2

1 2 1(1 +. 10)² 3 1(1 +. 10)³ =")

-$1 1(1 +. 10) 1 2 1(1 +. 10)² 3 1(1 +. 10)³ = 1. 33

Future Value of a Sum Let FV = future value of a sum r = time preference rate n = number of compounding periods pv = principle sum to be invested at present { FV = PV (1 + r)n interest factor

Problem: What will $1, 000 invested at 8% accumulate to at the end of five years? ? $1, 000 1 2 3 4 5

n = $1, 000 (1 +. 08)5 = $1,")

FV = PV (1 + r)n = $1, 000 (1 +. 08)5 = $1, 000 (1. 47) = $1, 470

Future Value of $1 r´s n´s 1% 2% 3%. . . 8% 1 2 3 4 5. . . 1. 47

= $1, 000 (1. 47) =")

FV = PV (fvf -. 08 - 5) = $1, 000 (1. 47) = $1, 470

n FV/(1 +")

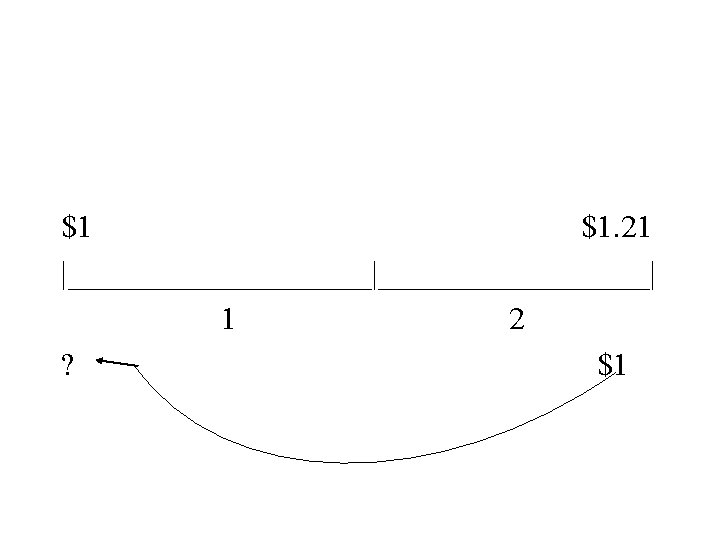

Present Value of a Sum = = = PV (1 + r)n FV/(1 + r)n FV 1/(1 + r)n { FV PV int. factor

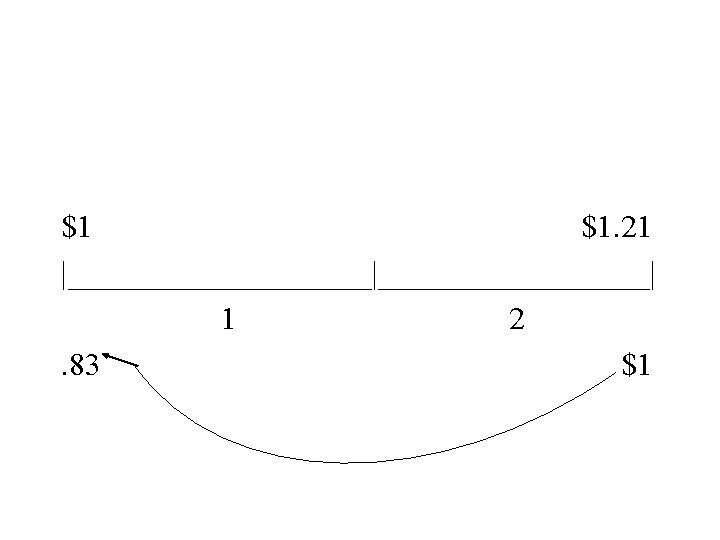

1 X = 1. 21 1 1. 21 X X = = = 1 1/1. 21 $. 83

Problem: What is $1, 000 promised at the end of five years worth today if r = 8%? ________________ ? $1, 000 __________________ 1 2 3 4 5 PV = 1, 000 (pvf -. 08 - 5) = 1, 000 (. 681) = $681

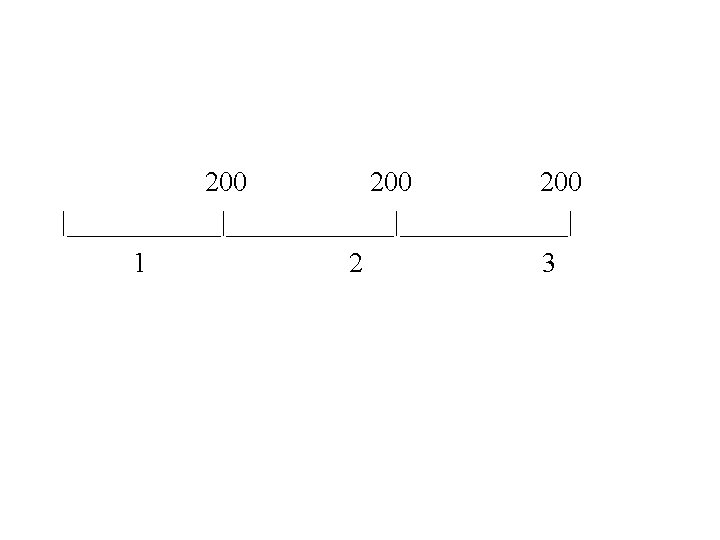

Annuity 100 100 |____________|______| 1 2 3 100 200 100 |____________|______| 1 2 3

200 200 |____________|______| 1 2 3")

Present Value of an Annuity (r = 10%) 200 200 |____________|______| 1 2 3 PV = $200(. 909) + $200(. 826) + $200(. 751) = 182 + 165 + 150 = $497

= 498")

Alternatively, PV = 200 (2. 49) = 498

Net Present Value Model of Investment Choice 1. Felt need: Maximize wealth 2. Problem Identification: a. Objective function: cash flows associated with each alternative b. Decision constraints: none c. Decision rule: choose alternative that maximizes wealth 3. Identify alternatives: predicting (estimating) cash flows associated with each alternative

Net Present Value Model of Investment Choice 4. Evaluate alternatives: a. Calculate PV equivalents of each cash inflow and cash outflow associated with each alternative b. Sum the PV’s of the inflows; sum the PV’s of the outflows c. NPV = sum of PV’s of inflows minus sum of present value of outflows 5. Choose alternative that promises the highest NPV!

-4, 500 3, 600 3, 360 3,")

Auto Replacement Problem Revisited (r = 10%) -4, 500 3, 600 3, 360 3, 120 Chevy |____________|______| 1 2 3 PV’s = -4, 500 + 3, 600 ( ) + 3, 360 ( ) + 3, 120 ( ) = -4, 500 + 3, 272 + 2, 775 + 2, 343 PV’s = -4, 500 + 8, 390 NPV = 3, 890

-4, 500 3, 600 3, 360 3,")

Auto Replacement Problem Revisited (r = 10%) -4, 500 3, 600 3, 360 3, 120 Chevy |____________|______| 1 2 3 PV’s = -4, 500 + 3, 600 (. 909) + 3, 360 (. 826) + 3, 120 (. 751) = -4, 500 + 3, 272 + 2, 775 + 2, 343 PV’s = -4, 500 + 8, 390 NPV = 3, 890

-6, 900 4, 080 4, 320 4, 560 Fiat |____________|______| 1 2 3 PV’s = -6, 900 + 4, 080 (. 909) + 4, 320 (. 826) + 4, 560 (. 751) = -6, 900 + 3, 709 + 3, 568 +3, 425 PV’s = -6, 900 + 10, 702 NPV = 3, 802 Decision: Choose ______

- Slides: 31