CHRISTMAS TREE CONFERENCE SUMMER CONVENTION AND TRADE SHOW

are the only federally")

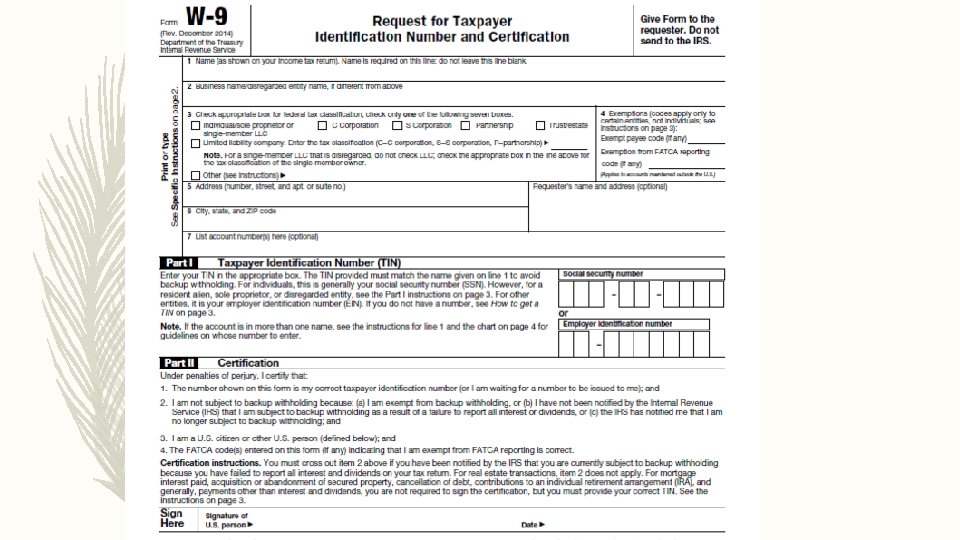

from whomever you pay B - Preparing")

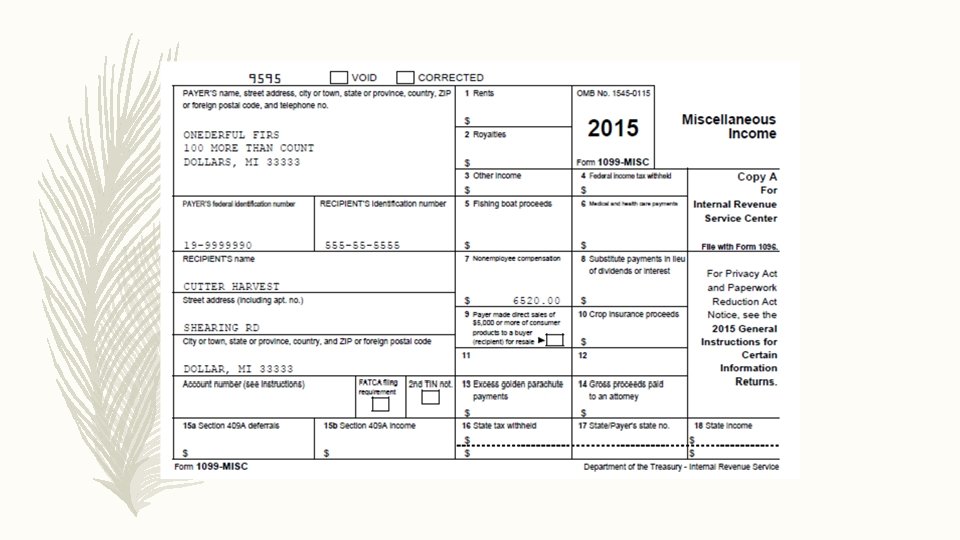

If, as part of your trade or business, you made")

(Box")

. You can")

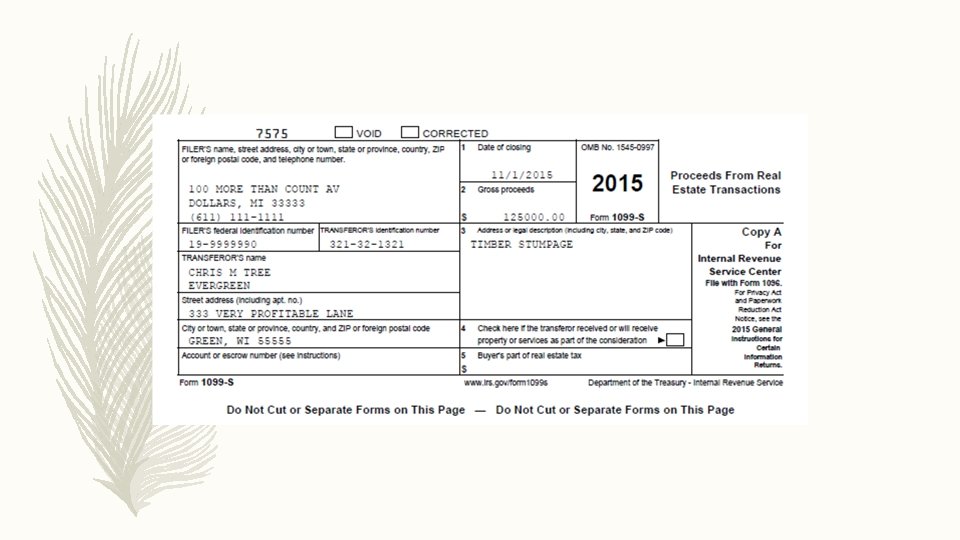

Transaction (Election to Treat Cutting as a Sale) – Timber owners who")

, gains or losses from the sale of standing timber shall,")

- Slides: 47

CHRISTMAS TREE CONFERENCE SUMMER CONVENTION AND TRADE SHOW FRIDAY, AUGUST 25 TH 2016 DODGE COUNTY FAIRGROUNDS, BEAVER DAM, WI WISCONSIN CHRISTMAS TREE PRODUCERS ASSOCIATION, INC.

D. Eckerman Tax Services Darlene G. Eckerman Enrolled Agent

Table of Contents 1. What is an Enrolled Agent? EA – Authorized by the IRS 2. W-9 s, 1096, W-2 s 3. Farm Business Tax Info Keeping; Sec 179, Office in the Home 4. Safe Harbor Election, 8903, WI MA-A, FC-A 5. Christmas Tree Business (CALL YOUR WI LEGISLATURE) 6. IRS Sec 631 7. Recap – You Should!

Enrolled Agents: are America’s Tax Experts. – Enrolled Agents, (EAs) are the only federally licensed tax practitioners who specialize in taxation. – They are empowered by the U. S. Department of the Treasury to represent taxpayers before the Internal Revenue Service. – Enrolled agent status is the highest credential awarded by the IRS. – Darlene is a member of the NAEA; National Association of Enrolled Agents, and a member of NATP; National Association of Tax Professionals.

D. Eckerman Tax Services N 681 S Rollwood Rd Antigo, WI 54409 Phone: 715 -623 -2520 Fax: 715 -623 -3646 Email: eckermantax@gmail. com Website: www. eckermantax. com

Dilemmas A - Getting 1099 information (W-9) from whomever you pay B - Preparing the 1099’s for the client and for your payees C - How should you answer the question(s) on top of 1040 Schedules C, E, F? D - Rule: No W-9 = No Check and/or No Cash and Get a Receipt if Cash!

Noncompliance A penalty for the information return applies for failure to: – File by the required due date – Include all of the information required to be shown or any incorrect information, i. e. wrong social security number, incorrect name or number and name do not match. – File on paper if you were required to file electronically – Report a correct TIN or any failure to report a TIN – File paper forms that are machine readable And You Cannot Show Reasonable Cause**

Penalties Fines: – $30 to $100 per return, 2016 law to $1, 000 – Up to 1. 5 M per year – Up to 500, 000 for small businesses

MOST COMMON TYPES OF FORM 1099’S

1099 – MISC (Miscellaneous) If, as part of your trade or business, you made any of the following types of payments…

ØServices performed by independent contractors or others * (not employees of your business) (Box 7) i. e. tax professionals, accountants, etc. * ØPrizes and awards and certain other payments (see instructions for Form 1099 -Misc Box 3. Other Income for more information) i. e. Spiff, Amway, party plans ØRent (Box 1) i. e. Land* ØRoyalties (Box 2) ØBackup withholding or federal income tax withheld (Box 4) ØCrewmembers of your fishing boat (Box 5) ØTo physicians, physicians’ corporations or other supplier of health and medical services (Box 6) ØFor a purchase of fish from anyone engaged in the trade or business of catching fish (Box 7) ØSubstitute dividends or tax exempt interest payments and you are a broker (Box 8) ØCrop insurance proceeds (Box 10) ØGross proceeds of $600 or more paid to an attorney (generally Box 7 but see instructions as box 14 may apply) * ØYour made direct sales of at least $5, 000 of consumer products to a buyer for resale anywhere other than a permanent retail establishment. i. e. Mary Kay, party plans, etc. Does not apply to S Corporations or C Corporations, only Individuals, including LLC’s

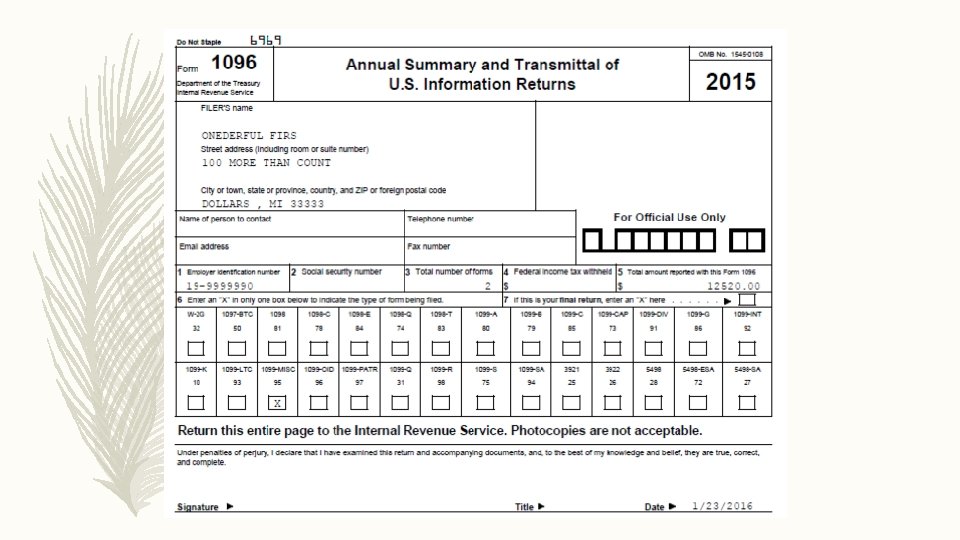

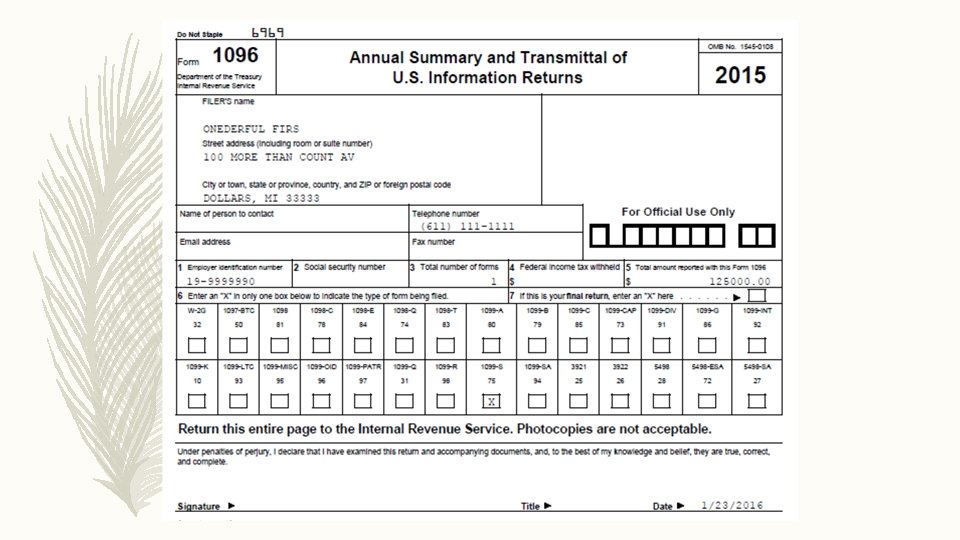

Due Dates Ø 1099, 1098 Form…. . . February 1 st 2017 Ø 1099 -B, 1099 -S, and 1099 Misc (if there amounts in box 8 and 14)…………………. February 29 th 2017 Paper filing, need red copies and due February 29 th 2017 ( an address can be found in part D and the 1096 summary) Electronically filing the 1099 forms, need to be complete and due March 31 st 2017

*VIP* W-2’s Social Security Copies must be filed by: January 31 st, 2017

FARM TAX INFORMATION KEEPING INCOME Sales - 1099's, Products sold, Other Sales, Products for Resale Also include the cost of purchase for resale animals, etc. Other Income - Ag payments, Farmland Credits, Patronage Dividends, Farm Interest Income, Fuel Tax Credit, Custom Hire, Scrap

EXPENSES Auto & Truck Expenses – Total Mileage - Odometer readings Jan 1, and December 31. – Date started odometer reading, business miles – Vehicle year/make – Gas, repairs, insurance, oil – Separate mileage logs for each vehicle used* – Car washes, loan interest, lease payment* * A per cent of business versus total miles driven per year. The per cent may vary year to year depending on business use Farms may use 75% without records, otherwise they need beginning and ending odometer readings Chemicals - Self explanatory Custom Hire - Hay Baling, Combining, etc. Feed - Includes hay, grain, minerals Fertilizers & Lime - Self explanatory Freight & Trucking - For hauling, shipping Gasoline, Fuel & Oil - For tractors and machinery, not cars or pick-ups, also need gallons used of OFF FARM gasoline

Insurance - Liability, Building - not auto, see above Interest - Credit card related to business, Farm Business Loan, Equipment Labor Hired Your own children under age 18. Case by case. Talk to me. Hired help on payroll. No FUTA or SUTA paid on farm labor usually. Rent Please differentiate between lease payment for equipment, payments for purchased capital items, and land rent. Repairs & Maintenance Office equipment and computer repair Garbage fees Machinery and Building Repair and Maintenance Seeds & plants - Self explanatory Storage & Warehousing - Self explanatory Supplies Items for use in farm business, milking, crops, packaging, etc. Office expenses, paper supplies Travel - Motel, airlines, taxi, rental car

Meals & Entertainment 1. Record in diary, journal or log Receipt not needed for meals under $75 for business reasons Record date, where, who with, amount paid and what discussed. Can be with spouse, significant other, others Do not count meals by yourself if not overnight 2. Per Diem Count number of days away for overnight stays. Include the day you left, days away and day returned using 1/4, 1/2, 3/4 or full day. $51 person/per day. If meals for that day are greater than $51, use option number 1. 3. Entertainment Movies, events for business. These should be journal entries also. Record total amount spent for entertainment. Utilities - If separate building - electricity, heat Vet, Breeding &Medicine - Include hoof trimming, as well as medicines and vet bills Other Seminars/Education - meetings, seminars, conventions Processing Advertising Personal Use – shows as a negative Legal/Prof Fees - Tax preparation, Attorney, Entity Fee ** ** Do not include fees associated with the purchase of land, buildings or equipment. Those fees are added into the cost or the basis of the item(s). Medical Expense - Section 105 plan. See me. Medical out of pocket and Mileage

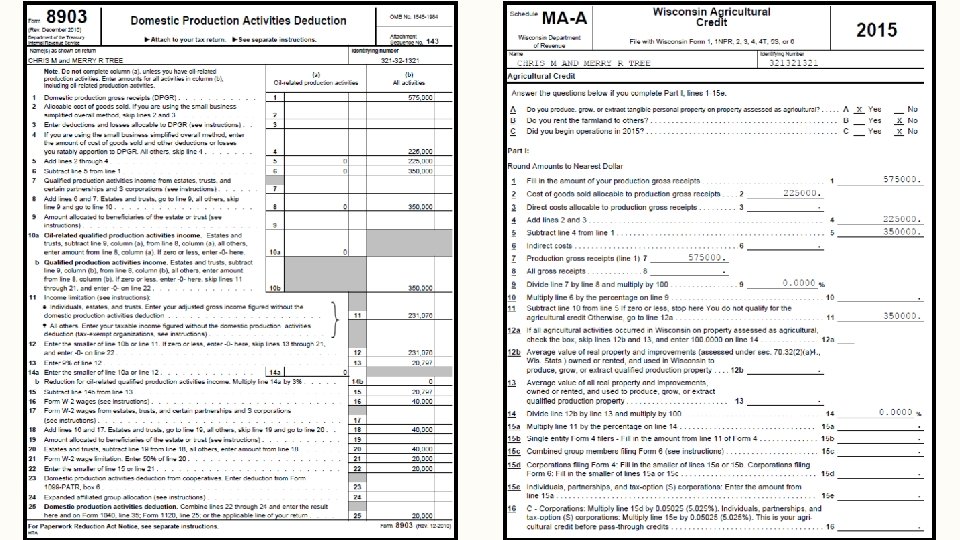

Office in your home Area used exclusively for business Does not have to be a separate room, but separate area Square feet of “office” Square feet of living space of home Utilities - water/sewer, electricity, heat Homeowners insurance Property taxes Mortgage interest, Rent Repairs to office or house Value of house, value of land Large home improvements Capital Items Converted or purchased Computer, printer, answering machine, copier, desk, chair, table File Cabinet, cupboards. Buildings Machinery Items greater than ~$250 - $500 and a useful life greater than one year. *Election available since 2014 for Improvements and Repairs. AMEND!

New Law 2014 Safe Harbor Election

Hmm… Sounds about right? !? !

Christmas Tree Cultivation If you are in the business of planting and cultivation Christmas trees to sell when they are more than 6 years old: – Capitalize expenses incurred for planting and stump culture and add them to the basis of the standing trees – Recover these expenses as part of your adjusted basis when you sell the standing trees or as depletion allowances when you cut the trees

Deductible Business Expenses – Costs incurred for shearing and basal pruning of trees – Silvicultural practices – weeding or cleaning, and noncommercial thinning Capitalize Cost of land improvements: road grading, ditching, and fire breaks (that have a useful life beyond the tax year) If improvements do not have a determinable useful life, add their cost to the basis of the land Cost is recovered when you sell or otherwise dispose of it Cost of equipment and other depreciable assets: culverts and fences, to the extent you do not use them in planting If improvements have a determinable useful life, recover their cost through depreciation

Timber Depletion: Takes place when you cut standing timber (Including Christmas Trees). You can figure you depletion deduction when the quantity of cut timber is first accurately measured in the process of exploitation.

Figuring Depletion There are two ways of figuring depletion: – Cost depletion – Percentage depletion For mineral property, you generally must use the method that gives you the larger deduction. For standing timber, you must use cost depletion. Cost Depletion To figure cost depletion you must first determine the following: – The property's basis for depletion – The total recoverable units of mineral in the property's natural deposit – The number of units of mineral sold during the tax year You must estimate or determine recoverable units (tons, barrels, board feet, thousands of cubic feet, or other measure) using the current industry method and the most accurate and reliable information you can obtain. Basis for depletion and total recoverable units are explained in chapter 9 of Publication 535.

Figuring The Timber Depletion Deduction – To figure your cost depletion allowance, multiply the number of units of standing timber cut by your depletion unit. When To Claim Timber Depletion – Claim your depletion allowance as a deduction in the year of sale or other disposition of the products cut from the timber, unless you elect to treat the cutting of timber as a sale or exchange as explained in chapter 8. – Include allowable depletion for timber products not sold during the tax year the timber is cut, as a cost item in the closing inventory of timber products for the year. – The inventory is your basis for determining gain or loss in the tax year you sell the timber products.

WI SCH WD - LONG TERM CAPITAL GAINS CHRISTMAS TREE GROWERS EXCLUDED! – Complete lines 21 -25 only if you have long-term gain from sale of farm assets. – Sixty percent of net long-term gain from the sale or other disposition of farm assets may be excluded. “Farm assets” means livestock, farm equipment, farm real property, and farm depreciable property. The exclusion applies to capital gain as computed under the Internal Revenue Code, not including amounts treated as ordinary income for federal purposes because of recapture of depreciation or any other reason. – “Farming” means the cultivation of land or the raising or harvesting of any agricultural or horticultural commodity including the raising, shearing, feeding, caring for, training, and management of animals. Trees (other than trees bearing fruit or nuts) shall not be treated as an agricultural or horticultural commodity. The 60 percent exclusion applies only to assets used in farming. The sale of woodland that cannot be used in farming would not qualify for the 60 percent. CALL YOUR WISCONSIN LEGISLATURES!!

IRS Section 631 Special Timber Rules are contained in Sec. 631, which applies generally to gain or loss from timber, coal, or domestic iron ore.

Section 631(a) Transaction (Election to Treat Cutting as a Sale) – Timber owners who cut timber for use in their own trade or business can, under certain conditions, obtain partial capital gains treatment by “electing to treat the cutting as a sale” under the provisions of Section 631(a) of the Internal Revenue Code. – The gain from timber cut under a section 631(a) election, that has been held for more than one year, and was cut as part of a trade or business is reported in two parts.

Specifically, under Sec. 631(b), gains or losses from the sale of standing timber shall, solely for purposes of determining character of income, be considered gains and/or losses from the sale of business use property as defined in Sec. 1231 (i. e. , capital gain property used in a trade or business), as long as the taxpayer held the standing timber for more than one year. Basically, sales of standing timber with a short-term holding period (one year or less) are considered ordinary trade or business or royalty income, or short-term capital gain, but gains on timber sales with a long-term holding period are allowed favored capital gains rates, while losses are deemed ordinary. So do not sell unless one year and one day! For the best tax treatment.

You Should… Ø Get Educated Ø Find a Knowledgeable Tax Professional Ø Audit Proof Yourself- (Keep good records, W-9 s, Receipts, Mileage log) Ø Make as Many of your Expenses, Business- (Are they Ordinary and Necessary? ) Ø Maximize the Use of Tax Laws: * % Business Use * Office in the Home * 8903 Sec 631 * LT Capital Gains * Schedule F-Farm * Accelerated Deprecation-Sec 179* Safe Harbor * WI-MA-A * WI FP-A * Ø Check your Tax Returns for the Above Ø Protect Your Future Income – Hold that Asset? Retirement Plans? LTC vs Trust? Ø Find JOY in What You are Doing Each Day!!

D. Eckerman Tax Services LLC N 681 S Rollwood Rd Antigo, WI 54409 Phone: 715 -623 -2520 Fax: 715 -623 -3646 Email: eckermantax@gmail. com Website: www. eckermantax. com

Thank You. A Great Growing & Selling Season To All!