Charitable Remainder Trusts 2 Lesson 47 Case Studies

Charitable Remainder Trusts 2 Lesson 47: Case Studies & Practical Applications

Christ Object Lessons “But money is of no more value than sand, only as it is put to use in providing for the necessities of life, in blessing others, and advancing the cause of Christ. ” (COL 351. 3)

Learning Outcomes 1. Determine which type of CRT is appropriate for fact patterns 2. Know the process of setting up a CRT 3. Know your responsibilities of being a trustee for a CRT

Choosing the Type of CRT 1. Charitable Remainder Unitrust a. Standard b. Net Income c. Net Income with Make-Up d. FLIP 2. Charitable Remainder Annuity Trust

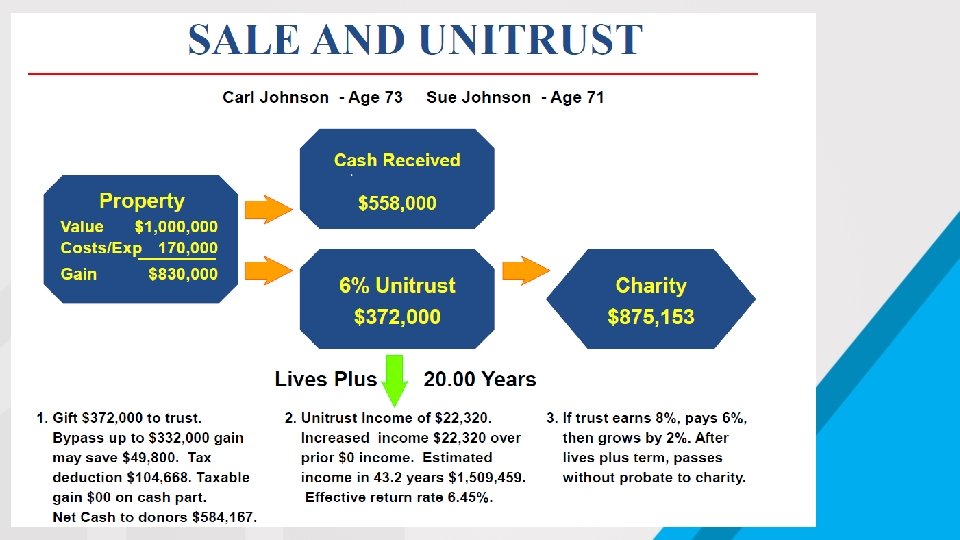

Appreciated Home & Family Income • Carl and Sue Johnson have lived in their home for many years. It has a cost basis of $100, 000 and is valued at approximately $1, 000. They are interested in obtaining cash to move to a retirement condo. • Carl and Sue qualify for the $500, 000 exclusion of capital gain. They could not sell the million-dollar property, however, without payment of some capital gains tax. It would be better in their view if there was a “capital gains tax-free” sale option. • Carl and Sue estimate that it will cost approximately 7% or $70, 000 to sell their home. • They would like any income to continue to benefit their children after they die.

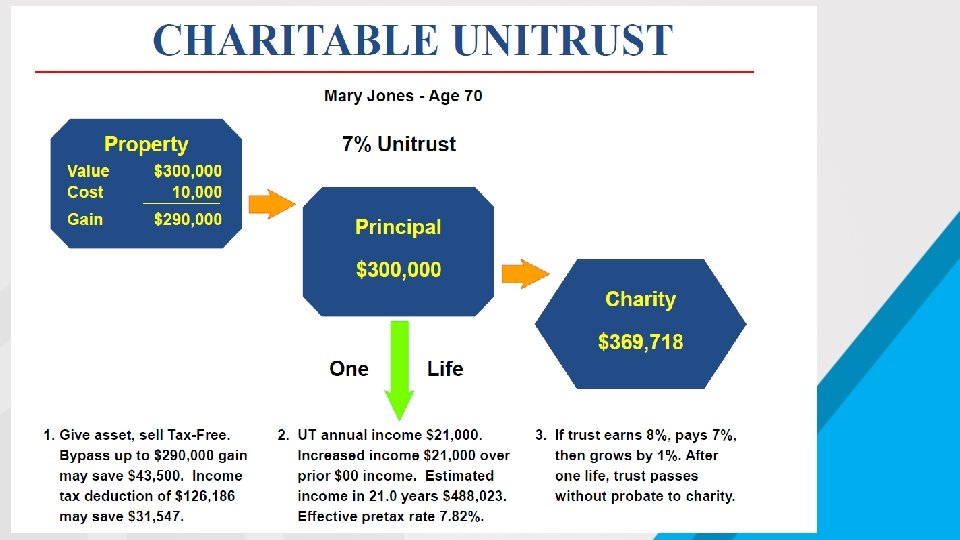

Appreciated Land & Retirement • Mary Jones owns real estate that she inherited twenty years ago from her parents. • Her cost basis is only $10, 000, but the development land has now appreciated dramatically and has a fair market value of $300, 000. • She would like to create a trust and desires to know that the trust will pay her 7% each year.

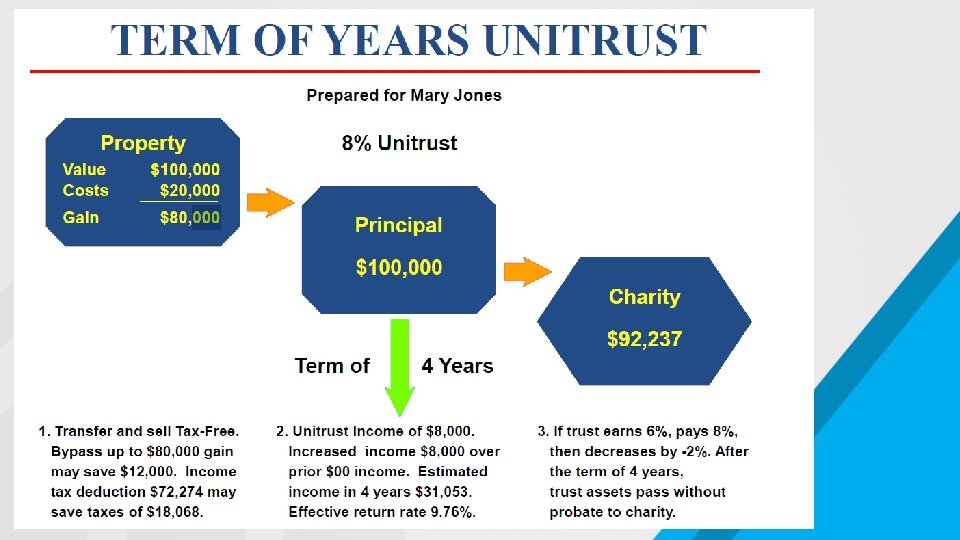

Appreciated Stock & Education for Twins • Assume that Mary Jones desires to assist her twin granddaughters Susie and Emily in their college education. Susie and Emily each have a college savings fund, they worked during the summer and their parents will provide some assistance. However, Grandmother Mary would like to provide an additional amount to assist in their education. • In addition, Mary has supported several charities and she would like both to help the twins receive a college education and to benefit her favorite charity. • Mary owns stock that she purchased for $20, 000. It has increased in value to $100, 000 and has been held for more than one year.

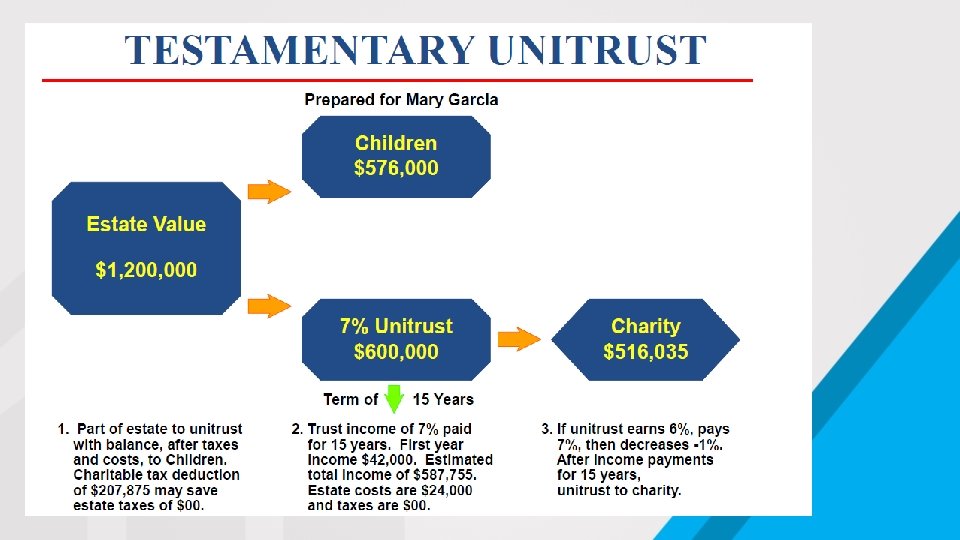

IRA & Income for Children • John and Mary Garcia raised a family of four children. Four years ago, John passed away and transferred all his assets to Mary. She received the house, the CDs, the securities and John’s IRA. • Mary rolled over John’s IRA, added in her IRA and now has $600, 000 in the IRA. She has approximately $600, 000 in other assets. • Mary desires to benefit her four children equally, but faces a challenge common to parents. Two of the children are very good money managers, one is somewhat borderline and one is quite creative. • If she transfers the assets equally to all four, the creative child will use those assets in new wonderful ways in perhaps three weeks. • She thinks that it would be desirable under the circumstances to “diversify” the inheritance.

“Give it Twice” Plan IRA Unitrust Children UCI

Process of Setting Up CRT 1. Choosing a Suitable Asset 2. Valuing the Asset 3. Choosing the type of CRT that meets the donors goals 4. Choosing the Duration 5. Choosing a Trustee 6. Legal Counsel for Charity and Donor 7. Executing & Funding the CRT

Choosing A Suitable Assets Problematic Assets 1. Cash 1. Debt Encumbered Property 2. Cash Equivalents 2. Sole Proprietorships 3. Publicly Traded Securities 3. Professional Practices 4. Close Held Stock in C Corporations 4. Assets with No Ready Market 5. Certain Real Estate

Valuing the Gift 1. Cash and Publicly Listed Securities – Readily Ascertainable Values 2. Non-Cash Assets (Except Publicly Traded Securities) – Require a Qualified Appraiser within 60 Days Prior to Transfer to Trust

Choosing the Type of CRT 1. Charitable Remainder Unitrust a. Standard b. Net Income c. Net Income with Make-Up d. FLIP 2. Charitable Remainder Annuity Trust http: //buckscountyattorney. blogspot. com

2. One Life Measuring")

Choosing the CRT Duration 1. Term of Years (Term Certain) 2. One Life Measuring Term CRT 3. Multiple Lives Measuring Term

Choosing A Trustee 1. Private Trustee: The private trustee has historically been the least frequently used method, but it is growing in popularity. Donor could serve as private trustee. - Donor has more flexibility/control. 2. Corporate Trustees: Major banks, trust companies, and the trust departments of major financial firms. More objective, have expertise, typically charge more. 3. Charity as Trustee: Why would a charity desire to serve as trustee? Can help build relationship, but comes with conflict and risk.

Legal Counsel 1. Denominational Entity: Should be represented by competent legal counsel knowledgeable in this area of the law, especially if the denominational entity is the one drafting the CRT. 2. Donor: Should receive independent legal counsel and tax advice and denominational entity should advise the donor in writing of the need for independent counsel.

Executing and Funding the CRT

Sources • https: //www. estateplanning. com/Understanding-Charitable-Remainder-Trusts/ • Crescendo Gift Law Pro 3. 10. 5 • Crescendo Gift Law Pro 3. 11. 1, 3. 11. 2, 3. 11. 3, 3. 11. 4, 3. 11. 5

IRS Requirements for CRT payouts • The payout rate stated in the trust documents must be: • Minimum 5% • Maximum 50%

Charitable Remainder Annuity Trust • Fixed payout • Payout does not change • Does not provide inflation protection • Provides security of definite payout • Best to use cash or easily marketable assets to fund

Charitable Remainder Uni. Trust • Pays Fixed Percentage of trust assets • Annual payment will fluctuate • Revalued at the beginning of each year to determine the payout • Payouts will increase as the value of the trust grows

- Slides: 25