Chapter ACCT 201 2 Accounting Information System ACCT

ACCT 201 On December")

ACCT 201 Taylor personally")

ACCT 201 To illustrate")

30, 000 (2) 2, 500 (5) 4, 200 (3) 26, 000 (9)")

Item PR Debit Credit 30, 000 Debit")

- Slides: 55

Chapter ACCT 201 2 Accounting Information System ACCT 201 UAA – ACCT 201 Principles of Financial Accounting Dr. Fred Barbee

Chapter 2 - Day 1 - Agenda Topic Generally Accepted Accounting Principles Transactions, Documents, and the Accounting Equation Transaction Analysis and the Accounting Equation LO Read HW C 1, C 2 38 -41 QS 1, E 1 C 3, C 4, 41 -46 C 5 A 1 46 -52 QS 2, QS 3 E 3

derstanding tastic ancial

ACCT 201 Learning Accounting ACCT 201 If you want to learn accounting, you learn it one concept at a time, one principle at a time. ACCT 201

Chapter ACCT 201 2 Accounting Information System ACCT 201 Text Section: Generally Accepted Accounting Principles (p. 38)

ACCT 201 C 1 Learning Objective ACCT 201 Explain the financial reporting environment ACCT 201 Conceptual

The Accounting System: A Conceptual Overview Operating Environment Entity B Entity C Business Entity A System Inputs: Measurable Transactions and Events Entity D Process and Summarize System Outputs: Financial Statements and Reports Entity E

Financial Reporting Environment FASB GAAP Financial Statements Preparers Audit Report Auditors ASB GAAS Decision makers

Independent Auditor Management 1 A A 3 P Income Statement Balance Sheet G Auditors Management Prepares S G A Statement of Cash Flows A Lends Credibility 4 Dr. Fred Barbee Basic Mistrust Users AC-300 Fall Session 1996 2 10

International Accounting Principles Despite our growing global economy, countries continue to maintain their unique set of acceptable accounting practices.

ACCT 201 C 2 Learning Objective ACCT 201 Identify, explain, and apply accounting principles. ACCT 201 Conceptual

A business continues operation instead of being closed or sold. A business is accounted for separately from its owner(s). Financial Statement information is supported by independent, unbiased evidence.

Express transactions and events in monetary units. Financial statements are based on actual costs incurred in business transactions.

Chapter ACCT 201 2 Accounting Information System ACCT 201 Text Section: Transactions, Documents, and Accounts (p. 41)

ACCT 201 C 3 Learning Objective ACCT 201 Identify, explain, and apply accounting principles. ACCT 201 Conceptual

The Accounting Process Transaction or event Source documents Analysis Reporting Trial balance Recording & posting Exh. 2. 2

Transactions and Events Exchanges of economic consideration between two parties. External Transactions occur between the organization and an outside party. Internal Transactions occur within the organization.

Accounting Information System Boundary Ongoing events in world Recording Data Bank Information Classifying

ACCT 201 C 4 Learning Objective ACCT 201 Describe source documents and their purpose. ACCT 201 Conceptual

Source Documents Other Invoices Check Stubs Bank Statement Journal

ACCT 201 C 5 Learning Objective ACCT 201 Describe an account and its uses in recording transactions. Conceptual

ACCT 201 Account ACCT 201 A storage unit used to classify and summarize money measurements of business activity of a similar nature. ACCT 201

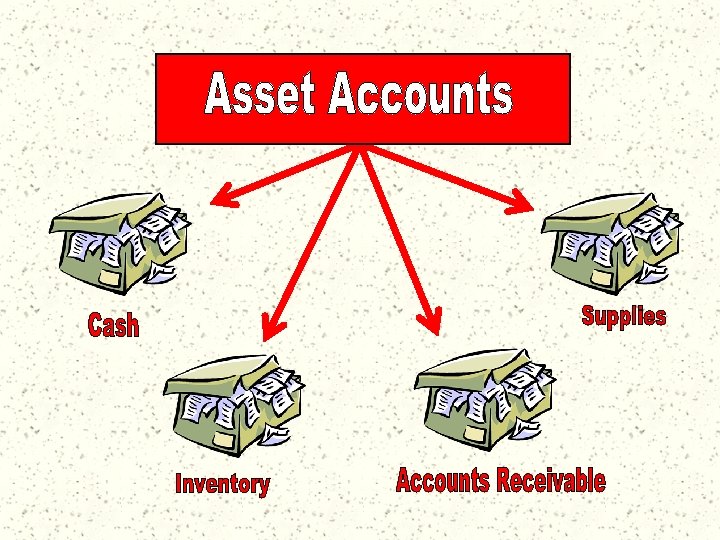

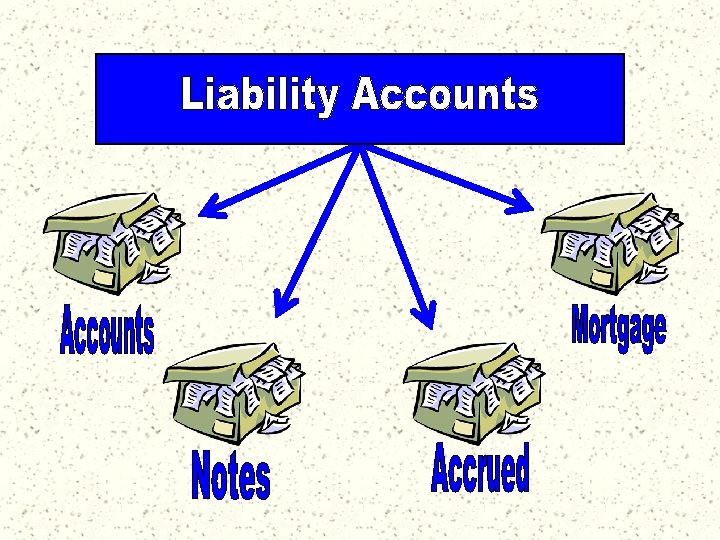

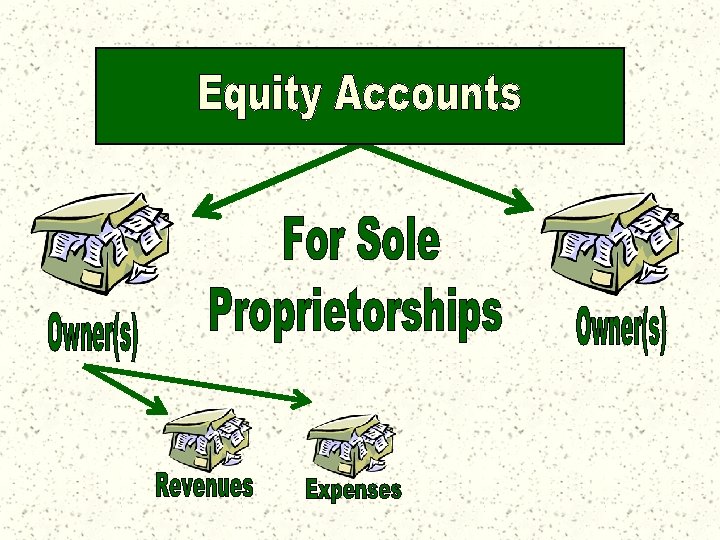

ACCT 201 The Account ACCT 201 Detailed record of increases and decreases in specific assets, liabilities, equities, revenues, or expenses. ============ Separate accounts are maintained for each item of importance.

The General Ledger Accts Rec. Inventory Cash General Notes Pay. Mortgage Accts Pay. Ledger Revenue Expenses Retained Earnings

ACCT 201

Account Title Left Side Right Side

ACCT 201 The Formal Account ACCT 201 The Balance Column Ledger

Account No. ### Account Title Date Item Post Ref Balance Debit Credit

Chapter ACCT 201 2 Accounting Information System ACCT 201 Text Section: Transactional Analysis and the Accounting Equation (p. 46)

ACCT 201 A 1 Learning Objective ACCT 201 Analyze business transactions using the accounting equation. Analytical

Assets = Liabilities + Owners’ Equity Capital Stock The Accounting Equation A = L + OE December 20 Retained Earnings Revenue = -Expenses Net Income

ACCT 201 Analyzing Transactions ACCT 201 1. Analyze the transaction and its source. 2. Identify the impact of the transaction on account balances. ACCT 201 3. Identify the financial statements that are impacted by the transaction.

ACCT 201 Transaction Analysis – Part 1 (Text p. 47) ACCT 201 On December 1, Chuck Taylor forms an athletic shoe consulting business. He sets it up as a corporation. Taylor owns and manages the business. The marketing plan for the business is to focus primarily on consulting with sports clubs, amateur athletes and others who place orders for athletic shoes with manufacturers.

ACCT 201 Transaction Analysis – Part 1 (Text p. 47) ACCT 201 Taylor personally invests $30, 000 cash in the new company in exchange for common stock, and deposits the cash in a bank account opened under the name of Fast. Forward, Inc. ACCT 201

ACCT 201 Transaction Analysis – Part II (Text p. 50) ACCT 201 To illustrate how revenue recognition works, let’s return to Fast. Forward’s transactions. ACCT 201

ACCT 201 1 Chuck Taylor invests $30, 000 in the company in exchange for common stock. ACCT 201

ACCT 201 2 Fast. Forward purchases $2, 500 of supplies for cash. ACCT 201

ACCT 201 3 Fast. Forward spends $26, 000 to acquire equipment for testing athletic shoes. ACCT 201

ACCT 201 4 Fast. Forward purchased $7, 100 of supplies on credit. ACCT 201

ACCT 201 5 Fast. Forward provides consulting services to an athletic club and collects $4, 200 in cash. ACCT 201

ACCT 201 6 Fast. Forward pays $1, 000 rent to the landlord of the building where its store is located. ACCT 201

ACCT 201 7 Fast. Forward pays the biweekly $700 salary of the company’s only employee. ACCT 201

ACCT 201 Revenue Recognition Principle ACCT 201 1. Revenue is recognized when earned. 2. Assets received from selling products and services need not be in cash. ACCT 201 3. Revenue recognized is measured by the cash received plus the cash equivalent (market) value of any other assets received.

8 Fast. Forward provides consulting services of $1, 600 and rents its test facilities for $300.

9 The client in transaction 8 pays $1, 900 to Fast. Forward 10 days after it is billed for consulting services.

10 Fast. Forward pays $900 to Cal. Tech Supply as partial payment for its earlier $7, 100 purchase of supplies.

11 Fast. Forward declares and pays a $600 cash dividend to its owner.

Cash (1) 30, 000 (2) 2, 500 (5) 4, 200 (3) 26, 000 (9) 1, 900 (6) 1, 000 (7) 700 Increases 36, 100 (10) 900 Decreases -31, 700 (11) 600 Balance 4, 400 Decreases 31, 700

Account No. 101 Cash Balance Date (1) Item PR Debit Credit 30, 000 Debit 30, 000 (2) 2, 500 27, 500 (3) 26, 000 1, 500 (5) 4, 200 5, 700 (6) 1, 000 4, 700 (7) 700 4, 000 (9) 1, 900 5, 900 (10) 900 5, 000 (11) 600 4, 400 Credit

“One must learn by doing the thing; though you think you know it, you have no certainty until you try it. ” Publilius Syrus, Moral Sayings