CHAPTER 9 RECEVABLES AND PAYABLES Principles of Accounting

CHAPTER 9 RECEVABLES AND PAYABLES Principles of Accounting with Key Words in Korean Soon Suk Yoon • Hyo Jin Kim Power. Point Presentation by: Soon Suk Yoon, Professor, Chonnam National University Hyo Jin Kim, Assistant Professor, Jeonju University 2012

1 Types of receivables

includes all money claims against other entities, including people, business")

The term receivables (수취채권) includes all money claims against other entities, including people, business firms, and other organizations.

, resulting from the sales of goods or services, are normally expected")

Accounts receivable (외상매출금), resulting from the sales of goods or services, are normally expected to be collected within a relatively short period, such as 30 or 60 days.

are amounts that customers owe for which")

Notes receivable (받 을 어 음 ) are amounts that customers owe for which a formal, written instrument of credit has been issued.

Other receivables includes non-trade receivables such as interest receivable, loans receivable, income taxes refundable and so forth.

2 Recognizing and valuing accounts receivable

Regardless of how careful a company is in granting credit, some credit sales will be uncollectible. The operating expense account is called bad debt expense, uncollectible accounts expense (대손상 각비), or doubtful accounts expense.

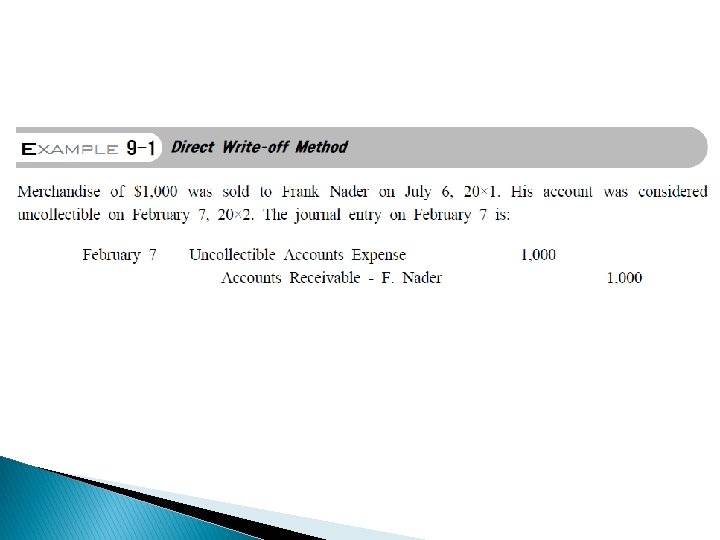

records bad debt expense")

The direct write-off method (직 접 차 감 법 ) records bad debt expense only when an account is judged to be worthless. The direct write-off method has two deficiencies. First, it fails to match the uncollectible expense against the revenue in the year of sale. Second, accounts receivable is shown at gross amount, resulting in overstatement of assets.

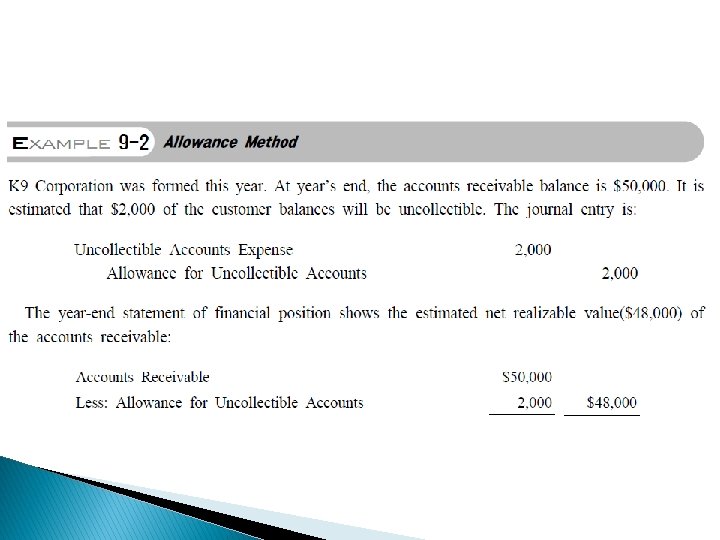

records bad debt expense by estimating uncollectible accounts at the")

The allowance method (충당금설정법) records bad debt expense by estimating uncollectible accounts at the end of the accounting period. Receivables are valued at Net Realizable Value ( 순 실 현 가 능 가 치 ). Uncollectible Accounts Expense (대 손 상 각 비 ) is matched with the revenue in the year of sale. The Allowance for Uncollectible Accounts (대손 충당금) is a contra asset account (자산차감계정 ).

3 Methods of Computing Provision for Uncollectible Accounts

Estimating Uncollectibles Alternative ways can be used to estimate the amount debited to Uncollectible Accounts Expense. 1. Percent of sales method. 2. Percent of accounts receivable method 3. Aging method

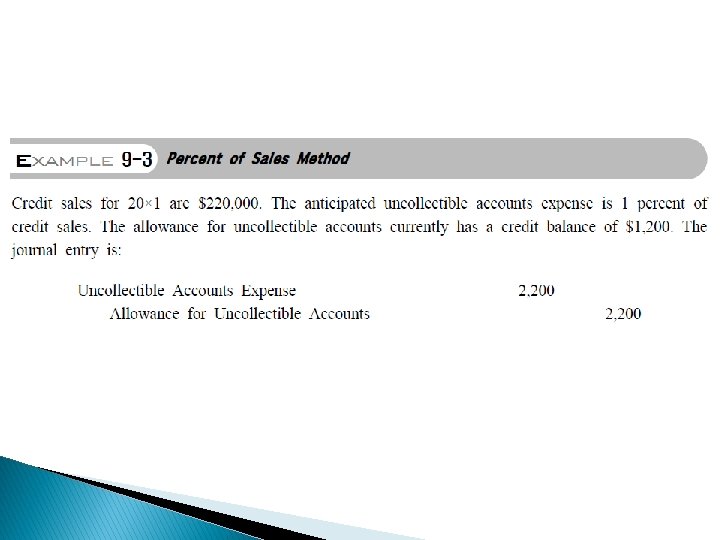

This is an income statement approach to estimating")

Percent of Sales Method (매출액비례법 ) This is an income statement approach to estimating uncollectible accounts expense. The expense is computed by multiplying the current year’s net credit sales (순외상 매출액) by a flat uncollectible rate (단일대손율). The method emphasizes the matching (대 응 ) between Uncollectible Accounts Expense and Credit Sales. Therefore, the current balance in the Allowance for Uncollectible Accounts does not affect Uncollectible Accounts Expense.

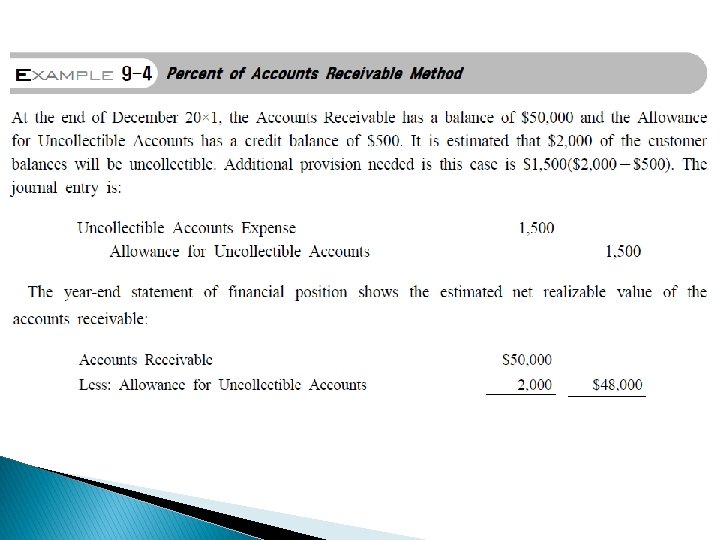

This is the statement of financial position approach to")

Percent of Receivable Method (채권잔액비례법) This is the statement of financial position approach to estimating allowance for uncollectible accounts. The allowance is computed by multiplying the receivable balance (채권잔액) at the end of a period by a flat uncollectible rate (단일대손율). The method emphasizes the measurement of receivable at Net Realizable Value. Therefore, the balance in the Allowance for Uncollectible Accounts is taken into account to record the adjusting entry for Uncollectible Accounts Expense.

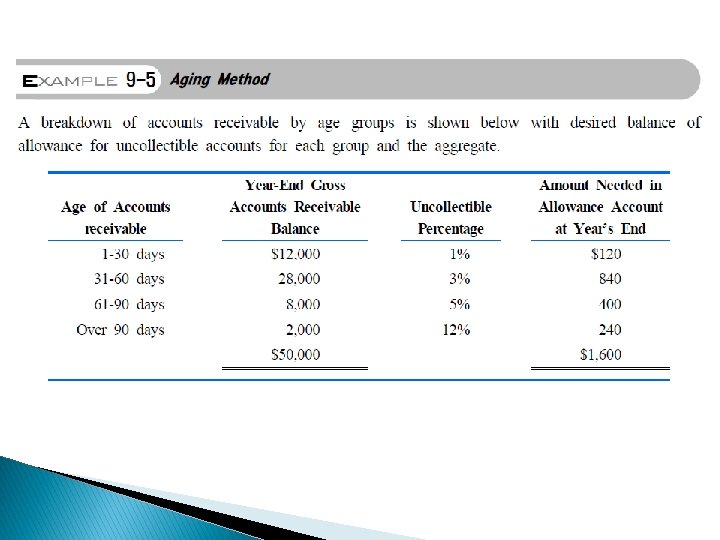

The longer an account receivable is overdue, the more likely it")

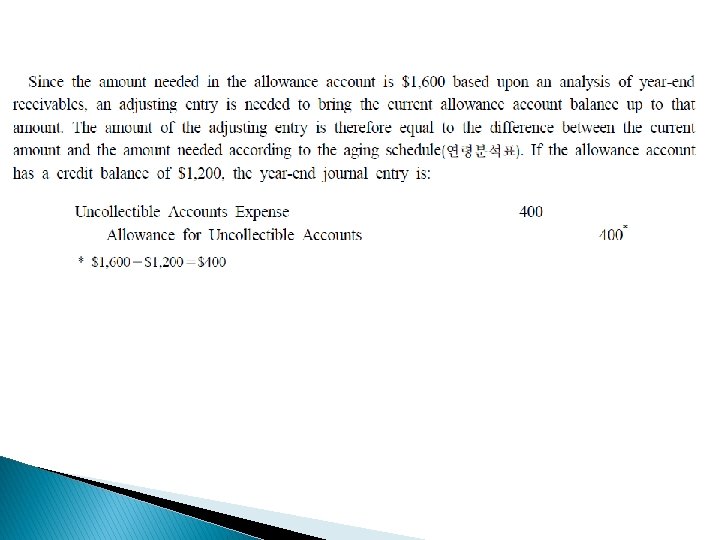

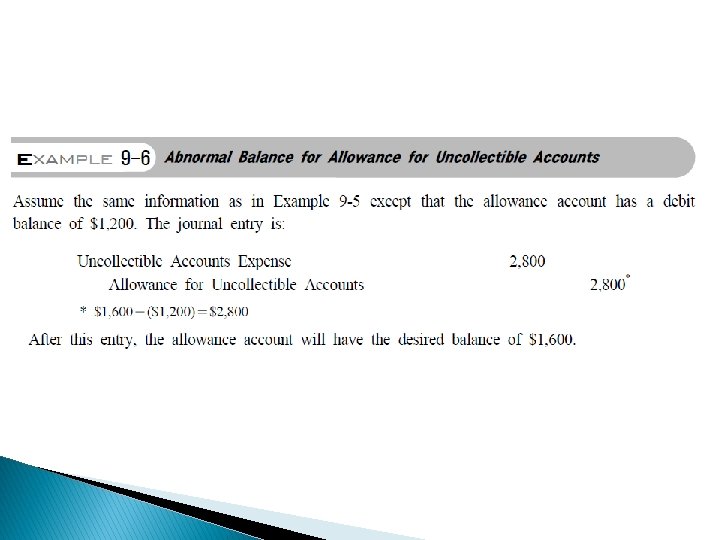

Aging Method (연령분석법) The longer an account receivable is overdue, the more likely it is that it fails to be collected. Basing the estimate of uncollectible accounts on how long specific amounts have been outstanding is called aging method. The aging method is also a balance sheet approach since it breaks down the gross receivables into different age groups and applies different uncollectible rates across the age groups.

4 WRITING OFF CUSTOMERS’ACCOUNTS

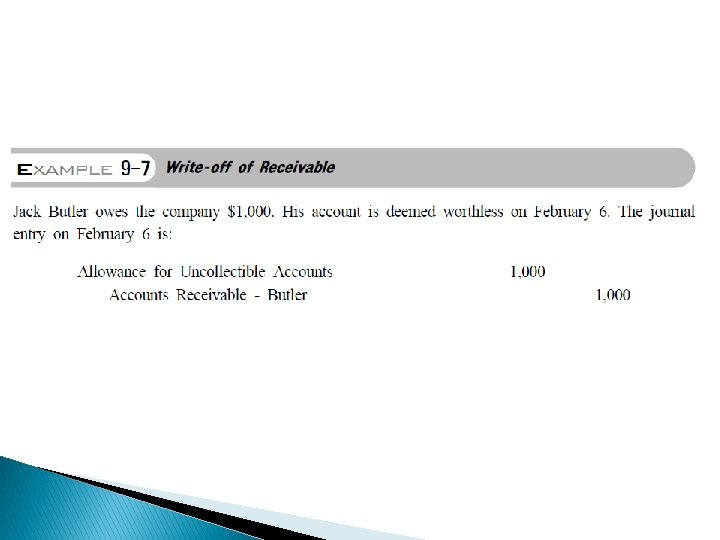

Write-off of a Specific Account When it is obvious that a customer is no longer able to pay the amount due, the specific account should be written off. The journal entry is: Allowance for Uncollectible Accounts* xxx Accounts Receivable xxx * Be careful not to debit Uncollectible Accounts Expense.

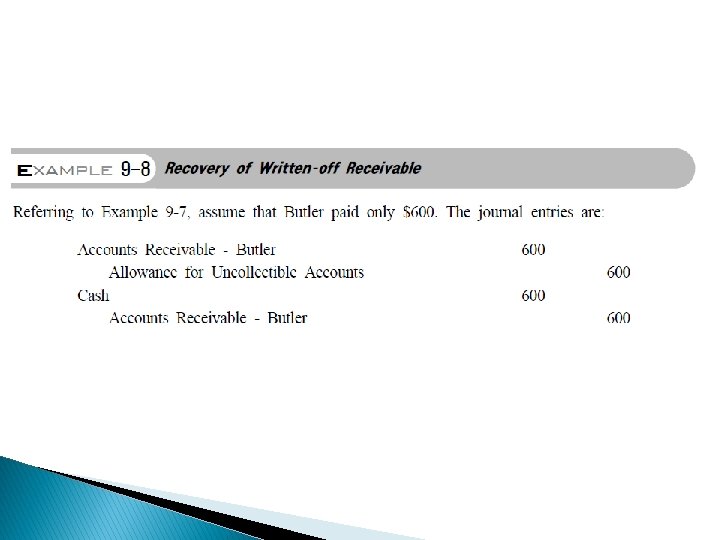

5 RECOVERY OF WRITTEN-OFF RECEIVABLES

Recovery of Written-off Receivables A full or partial recovery of a previously written-off accounts should be recorded in two steps. First, reverse the write-off journal entry. Second, record the collection of accounts receivable. 1) Accounts Receivable xxx Allowance for Uncollectible Accounts xxx 2) Cash xxx Accounts Receivable xxx

6 PROMISSORY NOTES

Characteristics of Notes Receivable A note receivable, or promissory note, is a written document containing a promise to • pay: The maker is the party making the promise to pay. • The payee is the party to whom the note is payable. • The face amount is the amount the note is written • for on its face. The issuance date is the date a note is issued. (continued)

• The due date or maturity date is the")

Characteristics of Notes Receivable (continued) • The due date or maturity date is the date the note • • is to be paid. The term of the note is the amount of time between the issuance and due dates. The interest rate is that rate of interest that must be paid on the face amount for the term of the note.

Exhibit Promissory Note

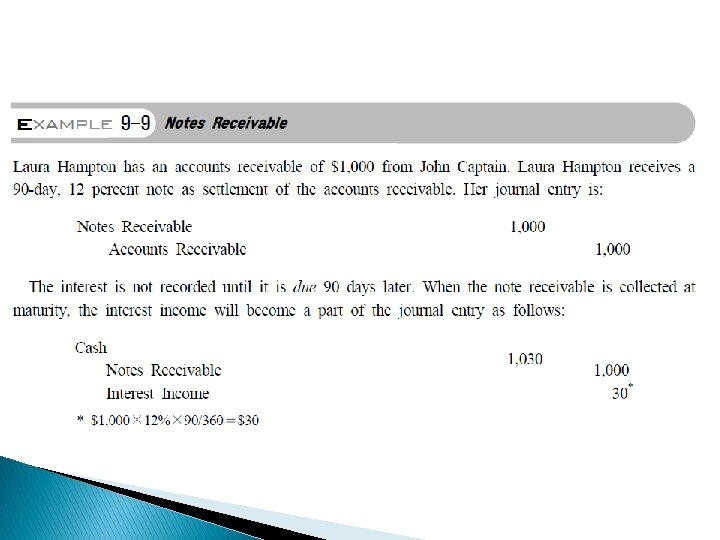

Interest on Notes Receivable Interest is usually computed on the basis of a 360 -day year (12 months× 30 days per month). The following formula is used: Interest=Principal × Interest Rate × Time The principal(원금) is the face value(액면금액) of the note. The interest rate (이자율) is the annual rate(연리) earned on the note. The time is the fraction of the year that the note is held. For example, if a $1, 000, 12 percent, 90 -day note is issued, then the interest is: $1, 000× 12%× 90/360=$30

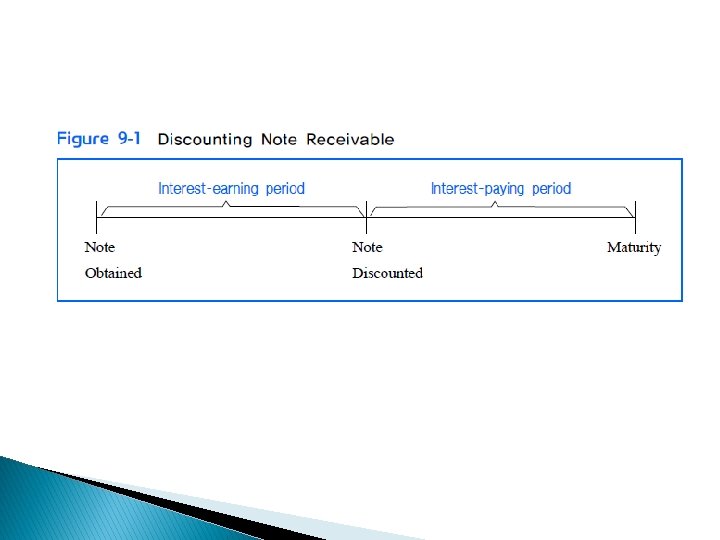

7 DISCOUNTING A NOTE RECEIVABLE

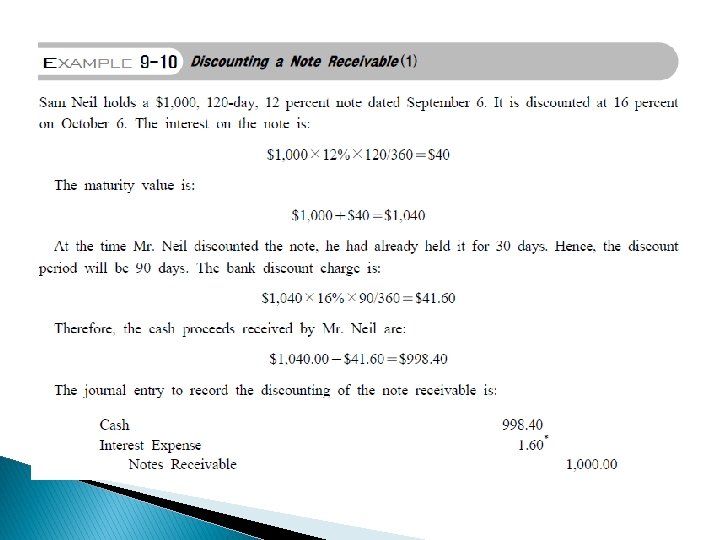

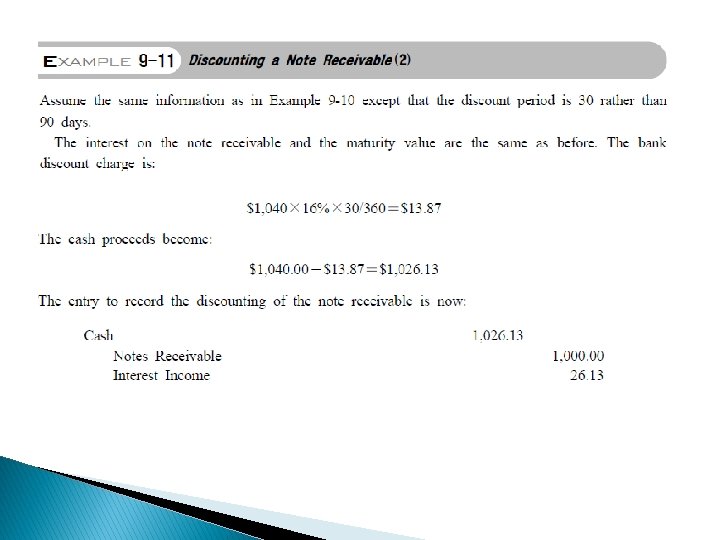

The holder of a note may expedite cash")

Discounting a Note Receivable (받을어음의 할인) The holder of a note may expedite cash receipt from the note by transferring it to a bank prior to maturity. This is referred to as ‘discounting a note receivable. ’ The proceeds received by the holder at the time the note is discounted is equal to the maturity value less the bank discount. They are calculated as follows: • Maturity Value (만기금액)=Face Value +Interest Income • Bank Discount (은행할인액)=Maturity Value × Discount Rate × Discount Period • Net Proceeds (현금수령액)=Maturity Value-Bank Discount

8 NOTES PAYABLE

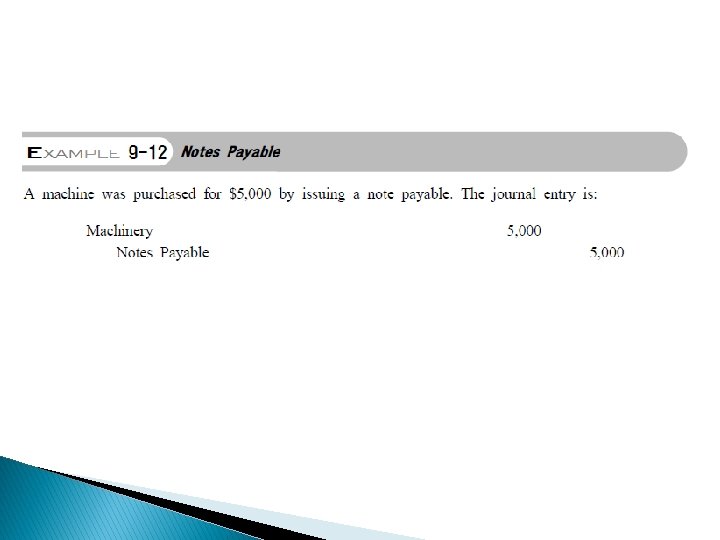

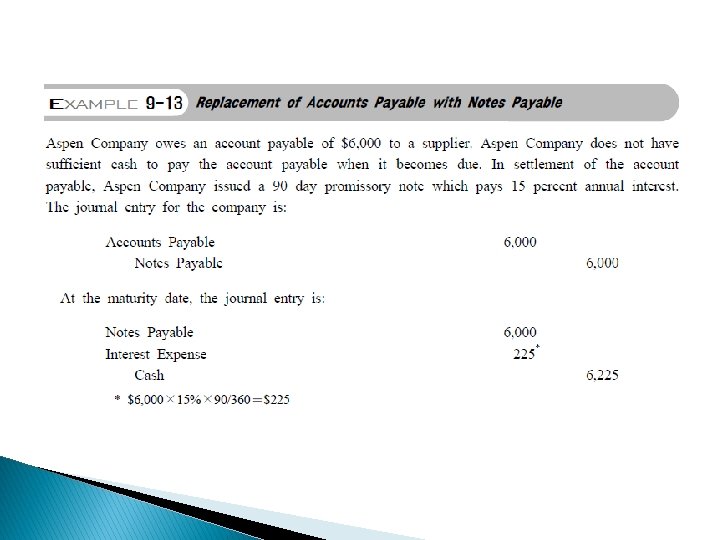

may be issued either to make")

A note payable (지 급 어 음 ) may be issued either to make a purchase, settle an account payable, or borrow from the bank. Accounting for notes payable is similar to that of notes receivable except that notes payable are liabilities.

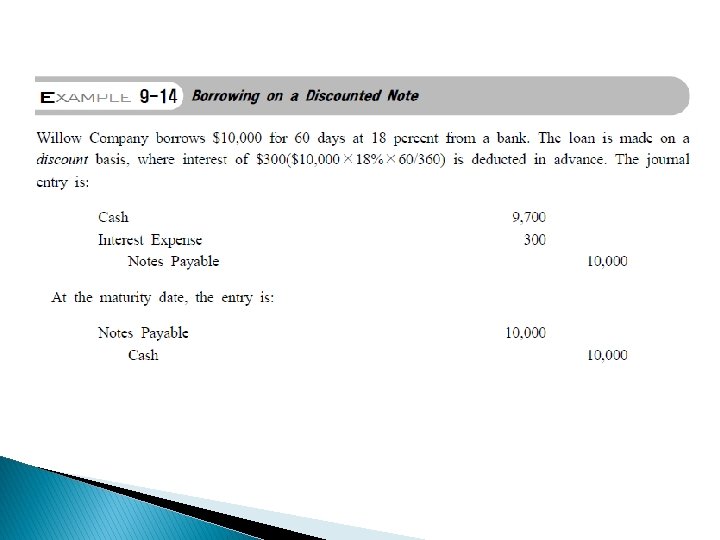

A note payable is typically issued to the bank")

Borrowing at a Discount (할인차입) A note payable is typically issued to the bank when money is borrowed. Often, the bank immediately deducts the interest on the loan from the face value of the note. The borrower receives the net proceeds. The term “borrowing at a discount (할 인 차 입 ) or “discounting a note payable” refers to the case where interest is paid in advance.

Two Ways to Pay Interests

Accounting Terminologies in Chapter 9 accounts receivable aging method allowance for uncollectible accounts allowance method annual rate balance sheet approach bank discount borrowing at a discount direct write-off method discounting notes receivable face value income statement approach 외상매출금 연령분석법 대손충당금 충당금설정법 연리 대차대조표접근법 은행할인액 할인차입 직접차감법 받을어음의 할인 액면금액 손익계산서접근법

Accounting Terminologies in Chapter 9 interest rate market rate of interest maturity value net credit sales net realizable value non-trade receivables 이자율 시장이자율 만기금액 순외상매출액 순실현가능가치 비매출채권 notes payable notes receivable on account open account percent of receivables method 어음상의채무(지급어음) 받을어음 외상, 신용 신용계정, 외상계정 채권잔액비례법

Accounting Terminologies in Chapter 9 percent of sales method 매출액비례법 principal priority lien proceeds promissory note provision receivables stated rate of interest trade receivables uncollectible accounts expense write-off 원금 선수위담보 현금수령액 약속어음 비용반영 수취채권 표시이자율 매출채권 대손상각비 제거

- Slides: 50