CHAPTER 8 Taxable Event Supply Under GST I

CHAPTER - 8 Taxable Event & Supply Under GST

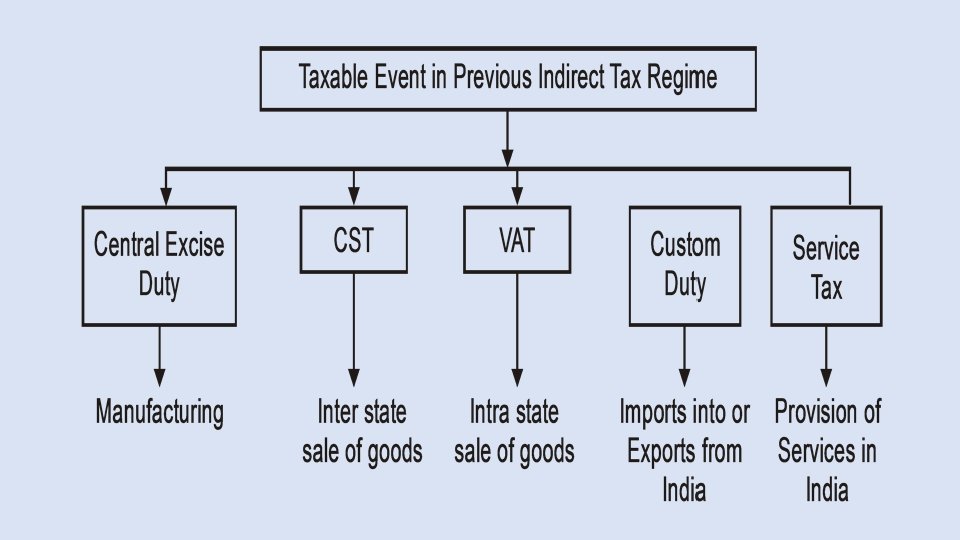

I. ADMINISTRATION BY CBIC : CGST & IGST • IMPACT OF TAX determines when tax is levied. Impact of tax determines the occurence of that particular event because of which the tax is levied on the event i. e. the taxable event. • INCIDENCE OF TAX determines on whom the burden of tax actually falls. In all Indirect Taxes - whether they were taxes prior to GST or GST - The incidence of tax always falls on Customers or Consumers

TAXABLE EVENT IN GST Taxable Event in GST = Supply of goods or Services or both Taxable Event is the event on the happening of which, the tax is levied. It is that event, which on its occurrence creates or attracts the liability to tax.

DETERMINATION OF THE NATURE OF TRANSACTION

Supply of Goods. Supply of goods can be both interstate (between states/UT’s) or")

a) Supply of Goods. Supply of goods can be both interstate (between states/UT’s) or Intrastate (within same state/UT). b) Supply of Services. Similarly, supply of services includes both inter state / UT and Intra state / UT. c) Supply of both Goods & Services

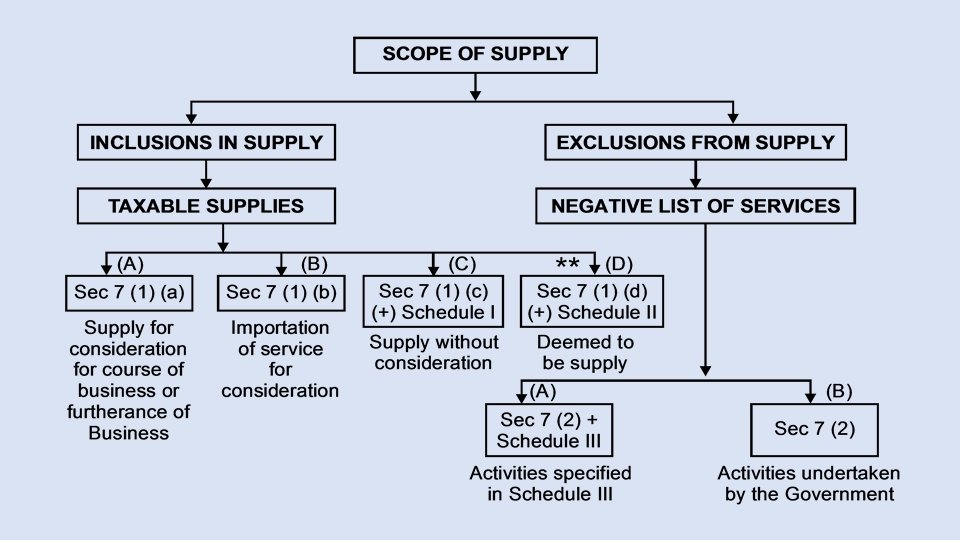

COMPOSITE SUPPLY MEANS A SUPPLY MADE BY A TAXABLE PERSON TO A RECIPIENT AND: • comprises two or more taxable supplies of goods or services or both, or any combination thereof. • are naturally bundled (because of natural necessities) and supplied in conjunction with each other, in the ordinary course of business • one of which is a principal supply Principal supply means the supply of goods or services which constitutes the predominant element of a composite supply and to which any other supply forming part of that composite supply is ancillary. [Section 2(90) of CGST Act] How to determine the tax liability on composite supplies? : A composite supply comprising of two or more supplies, one of which is a principal supply, shall be treated as a supply of such principal supply.

![MIXED SUPPLIES : [SEC 2(74) OF THE CGST ACT] Mixed supply means: • two](http://slidetodoc.com/presentation_image_h2/6d7e4b894975464c5e6926b7afc5c857/image-8.jpg "MIXED SUPPLIES : [SEC 2(74) OF THE CGST ACT] Mixed supply means: • two")

MIXED SUPPLIES : [SEC 2(74) OF THE CGST ACT] Mixed supply means: • two or more individual supplies of goods or services, or any combination thereof, made in conjunction with each other by a taxable person • for a single price where such supply does not constitute a composite supply. How to determine the tax liability on mixed supplies? . A mixed supply comprising of two or more supplies shall be treated as supply of that particular supply that attracts highest rate of tax.

WHAT IS SUPPLY UNDER GST ?

………… End of Chapter

- Slides: 11