Chapter 8 An Economic Analysis of Financial Structure

”大国金融体系升级” 1 -7 © 2016 Pearson Education Ltd. All rights reserved.")

50.")

• Financial intermediaries have evolved to reduce transaction costs – Economies of")

• Adverse selection(相反選擇) occurs before the transaction • Moral hazard(道德危險) arises after")

: How Adverse Selection Influences Financial Structure • If quality")

” created by an institutional environment")

- Slides: 27

Chapter 8 An Economic Analysis of Financial Structure 20 -1 © 2016 Pearson Education Ltd. All rights reserved.

Preview • A healthy and vibrant economy requires a financial system that moves funds from people who save to people who have productive investment opportunities. 1 -2 © 2016 Pearson Education Ltd. All rights reserved.

Learning Objectives • Identify eight basic facts about the global financial system. • Summarize how transaction costs affect financial intermediaries. • Describe why asymmetric information leads to adverse selection and moral hazard. • Recognize adverse selection and summarize the ways in which they can be reduced. 1 -3 © 2016 Pearson Education Ltd. All rights reserved.

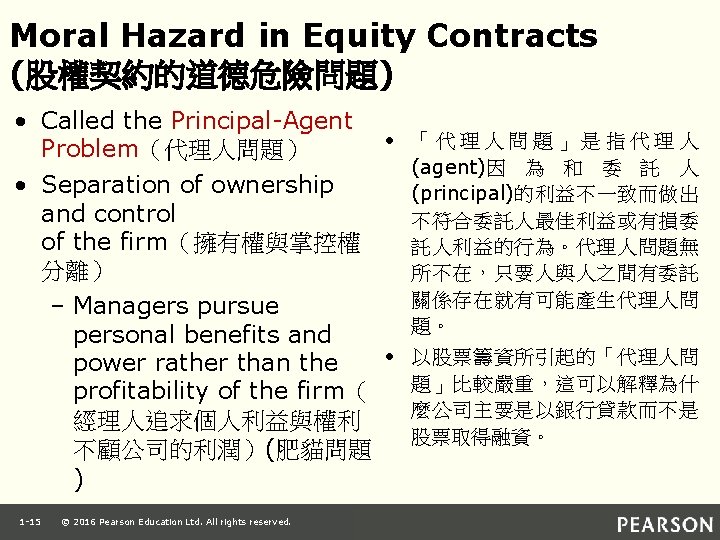

Learning Objectives • Recognize the principal-agent problem arising from moral hazard in equity contracts and summarize the methods for reducing it. • Summarize the methods used to reduce moral hazard in debt contracts 1 -4 © 2016 Pearson Education Ltd. All rights reserved.

Basic Facts about Financial Structure Throughout the World • This chapter provides an economic analysis of how our financial structure is designed to promote economic efficiency. • The bar chart in Figure 1 shows how American businesses financed their activities using external funds (those obtained from outside the business itself) in the period 1970– 2000 and compares U. S. data to those of Germany, Japan, and Canada. 1 -5 © 2016 Pearson Education Ltd. All rights reserved.

Figure 1 Sources of External Funds for Nonfinancial Businesses: A Comparison of the United States with Germany, Japan, and Canada Source: Andreas Hackethal and Reinhard H. Schmidt, “Financing Patterns: Measurement Concepts and Empirical Results, ” Johann Wolfgang Goethe-Universitat Working Paper No. 125, January 2004. The data are from 1970– 2000 and are gross flows as percentage of the total, not including trade and other credit data, which are not available. 1 -6 © 2016 Pearson Education Ltd. All rights reserved.

資料來源:任泽平(2019, 6)”大国金融体系升级” 1 -7 © 2016 Pearson Education Ltd. All rights reserved.

台灣的直接金融與間接金融 100. 00 90. 00 80. 00 70. 00 60. 00 間接金 融(%) 50. 00 40. 00 直接金 融(%) 30. 00 20. 00 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 0. 00 1 -8 © 2016 Pearson Education Ltd. All rights reserved.

Basic Facts about Financial Structure Throughout the World 1. Stocks are not the most important sources of external financing(外部融資) for businesses. 2. Issuing marketable debt and equity securities is not the primary way in which businesses finance their operations. 3. Indirect finance(直接金融) is many times more important than direct finance 4. Financial intermediaries, particularly banks, are the most important source of external funds used to finance businesses. 1 -9 © 2016 Pearson Education Ltd. All rights reserved.

Basic Facts about Financial Structure Throughout the World 5. The financial system is among the most heavily regulated(嚴厲規範) sectors of the economy. 6. Only large, well-established corporations (唯有 大型且建置完好公司) have easy access to securities markets to finance their activities. 7. Collateral(擔保品) is a prevalent feature of debt contracts for both households and businesses. 8. Debt contracts are extremely complicated legal documents that place substantial restrictive covenants(限制條款) on borrowers. 1 -10 © 2016 Pearson Education Ltd. All rights reserved.

Transaction Costs(交易成本) • Financial intermediaries have evolved to reduce transaction costs – Economies of scale(規模經濟) (use information(包括資訊系統、資料庫)、 over and over again) – Expertise(專業) 包括 lending、investment、liquidity …service 1 -11 © 2016 Pearson Education Ltd. All rights reserved.

Asymmetric Information(資訊不對稱) • Adverse selection(相反選擇) occurs before the transaction • Moral hazard(道德危險) arises after the transaction • Agency theory(代理人理論) analyses how asymmetric information problems affect economic behavior 1 -12 © 2016 Pearson Education Ltd. All rights reserved.

The Lemons Problem (酸檸檬問題) : How Adverse Selection Influences Financial Structure • If quality cannot be assessed, the buyer is willing to pay at most a price that reflects the average quality (買方支付的最高價格只能反應平均品質) • Sellers of good quality items will not want to sell at the price for average quality (擁有優良品質的賣方不 願意以平均價格賣出) • The buyer will decide not to buy at all because all that is left in the market is poor quality items(買方 決定不買因為剩下來的都是劣質品) • This problem explains fact 2 (證券市場不振)and partially explains fact 1(股市萎縮) 1 -13 © 2016 Pearson Education Ltd. All rights reserved.

Tools to Help Solve Adverse Selection Problems • Private production and sale of information – Free-rider problem (白搭便車問題) • Government regulation to increase information – Not always works(不見得有效) to solve the adverse selection problem, explains Fact 5 • Financial intermediation – Explains facts 3, 4, & 6 • Collateral and net worth – Explains fact 7 1 -14 © 2016 Pearson Education Ltd. All rights reserved.

Tools to Help Solve the Principal. Agent Problem • Monitoring (Costly State Verification (昂貴的認證程 序)) – Free-rider problem – Fact 1 • Government regulation to increase information – Fact 5 • Financial Intermediation – Fact 3 • Debt Contracts – Fact 1 1 -16 © 2016 Pearson Education Ltd. All rights reserved.

1 -17 © 2016 Pearson Education Ltd. All rights reserved.

1 -18 © 2016 Pearson Education Ltd. All rights reserved.

Moral Hazard in Debt Markets • Borrowers have incentives to take on projects that are riskier than the lenders would like. (借款人有誘因去冒貸款人所不喜歡 的更大風險) – This prevents the borrower from paying back the loan. (債務契約的道德危險將阻止借款人償還銀行貸款) 1 -19 © 2016 Pearson Education Ltd. All rights reserved.

1 -20 © 2016 Pearson Education Ltd. All rights reserved.

1 -21 © 2016 Pearson Education Ltd. All rights reserved.

1 -22 © 2016 Pearson Education Ltd. All rights reserved.

Tools to Help Solve Moral Hazard in Debt Contracts • Net worth and collateral – Incentive compatible (誘因一致) • Monitoring and enforcement of restrictive covenants – Discourage undesirable behavior – Encourage desirable behavior – Keep collateral valuable – Provide information • Financial intermediation – Facts 3 & 4 1 -23 © 2016 Pearson Education Ltd. All rights reserved.

1 -24 © 2016 Pearson Education Ltd. All rights reserved.

Summary Table 1 Asymmetric Information Problems and Tools to Solve Them 1 -25 © 2016 Pearson Education Ltd. All rights reserved.

Application: Financial Development and Economic Growth • “Financial repression(金融壓抑)” created by an institutional environment characterized by: – Poor system of property rights(糟糕的財產權制度) (unable to use collateral efficiently) – Poor legal system(糟糕的法律體系) (difficult for lenders to enforce restrictive covenants) – Weak accounting standards(脆弱的會計標準) (less access to good information) – Government intervention(政府干預) through directed credit programs and state owned banks( 公營銀行) (less incentive to proper channel funds to its most productive use). 1 -26 © 2016 Pearson Education Ltd. All rights reserved.

Application: Financial Development and Economic Growth • The financial systems in developing and transition countries(例如:蘇俄) face several difficulties that keep them from operating efficiently • In many developing countries, the system of property rights(財產權) (the rule of law(法律規範), constraints on government expropriation(政府徵收限 制), absence of corruption(貪腐減少)) functions poorly, making it hard to use these two tools effectively 1 -27 © 2016 Pearson Education Ltd. All rights reserved.