Chapter 7 Depreciation and Income Taxes Income taxes

. •")

method. 2. Declining Balance (DB) Method.")

: constant amount of depreciation each year over the depreciable life of")

: a constant-percentage of the remaining BV is depreciated each year. The constant")

200% DB, R = 2/10 = 0. 2 d 1 = B (R)")

150% DB, R = 1. 5/10 = 0. 15 d 1 = 4000")

MACRS is the principle method for computing")

. 2.")

- Slides: 35

Chapter 7: Depreciation and Income Taxes Income taxes usually represent a significant cash outflow. In this chapter we describe how after-tax cash flows result in the after-tax cash flow (ATCF) procedure. Depreciation is an important element in finding after-tax cash flows.

• Depreciation is the decrease in value of physical properties with time. • It is an accounting concept, a non-cash cost, that establishes an annual deduction against before-tax income. • It is intended to approximate the yearly fraction of an asset’s value used in the production of income.

Property is depreciable if • it is used in business or held to produce income. • it has a determinable useful life, longer than one year. • it is something that wears out, decays, gets used up, or loses value from natural causes. • it is not inventory.

Depreciable property is • Tangible: (can be seen or touched; personal or real). • Intangible: (such as copyrights, patents). Depreciated, according to a depreciation schedule, when it is put in service (when it is ready and available for its specific use).

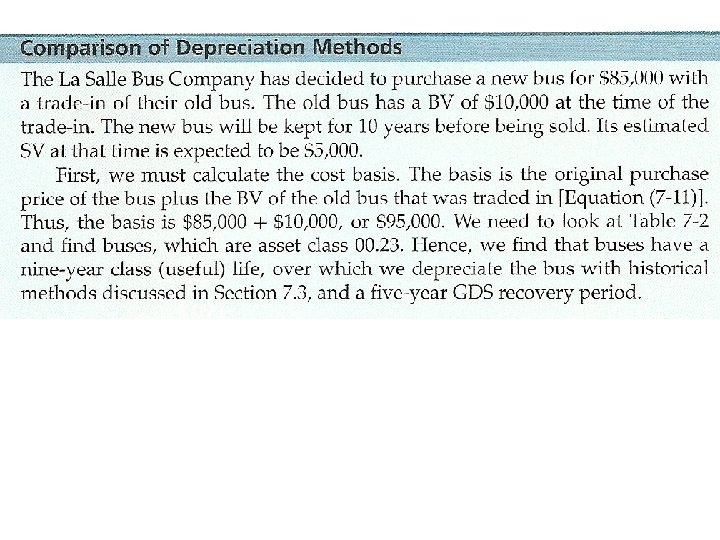

Definitions • Basis or Cost basis: The initial cost of acquiring an asset (Purchase price plus any sales taxes). • Adjusted Cost or Basis: The original cost basis of asset, adjusted by increase or decrease, is used to compute depreciation deduction. • Book Value (BV): The worth of a depreciable property as shown on the accounting record of a company. • Market Value (MV): The amount that will be paid by a buyer to a seller for a property. • Salvage Value (SV): The estimated value of a property at the end of its useful life. • Useful Life: The expected period that a property will be used in a trade or business to produce income.

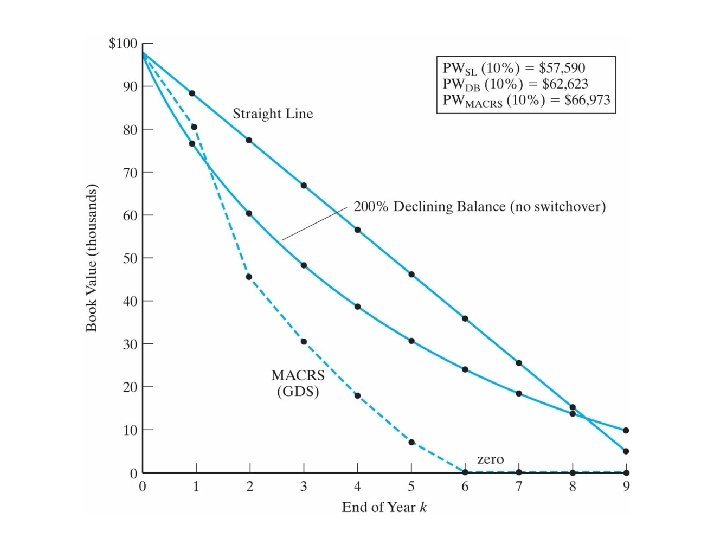

The Classical Depreciation Methods 1. Straight Line (SL) method. 2. Declining Balance (DB) Method. 3. DB with Switchover to SL method. 4. Units of Production Method.

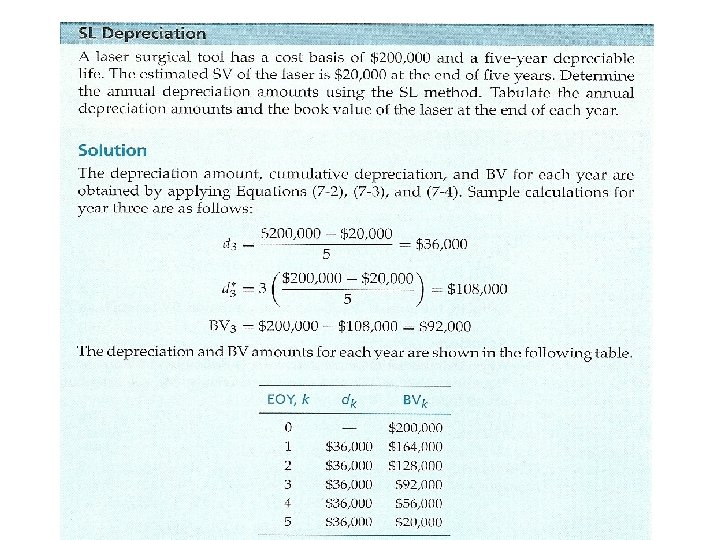

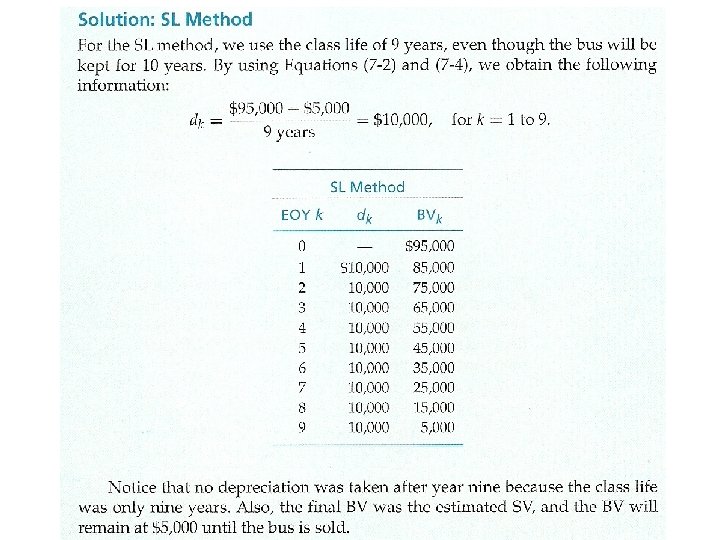

Straight line (SL): constant amount of depreciation each year over the depreciable life of the asset. • • • N = depreciable life B = cost basis BVk = book value at the end of year k SVN = salvage value at the end of year N dk = depreciation in year k d. K*= Cumulative depreciation through year k dk = (B - SVN) / N d. K*= k. dk BVk = B - d. K*

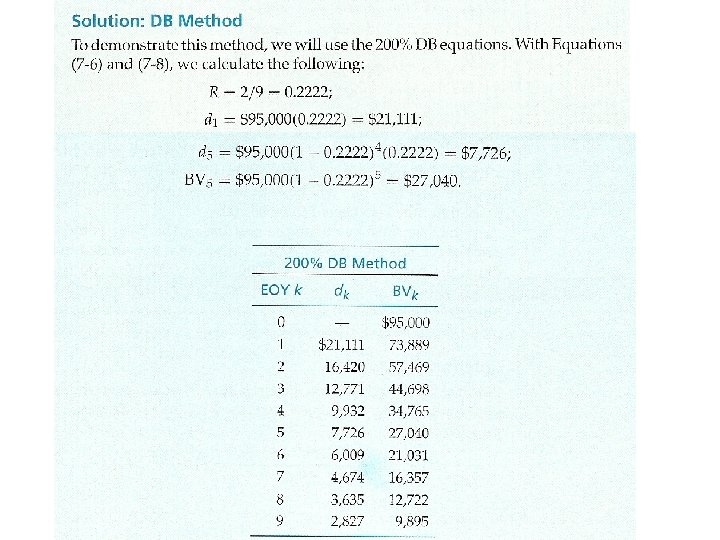

Declining-balance (DB): a constant-percentage of the remaining BV is depreciated each year. The constant percentage is determined by R, where R = 2/N when 200% declining balance is being used, R = 1. 5/N when 150% declining balance is being used. d 1 = B (R) k-1 dk = B (1 - R) (R) k d. K*= B [1 - (1 - R) ] BVk = B (1 - R) k

(a) 200% DB, R = 2/10 = 0. 2 d 1 = B (R) = 4000 (0. 2) = 800$ dk = B (1 - R)k-1(R), d 6 = 4000 (1 – 0. 2)6 -1(0. 2) = 262. 14$ d. K*= B [1 - (1 - R)k ], d 6*= 4000 [1 - (1 – 0. 2)6 ] = 2, 951. 42$ BVk = B (1 - R)k , BVk = 4000 (1 – 0. 2)6 = 1, 048. 58$

(b) 150% DB, R = 1. 5/10 = 0. 15 d 1 = 4000 (0. 15) = 600$ d 6 = 4000 (1 – 0. 15)6 -1(0. 15) = 266. 2$ d 6*= 4000 [1 - (1 – 0. 15)6 ] = 2, 491. 4$ BVk = 4000 (1 – 0. 15)6 = 1, 508. 6$

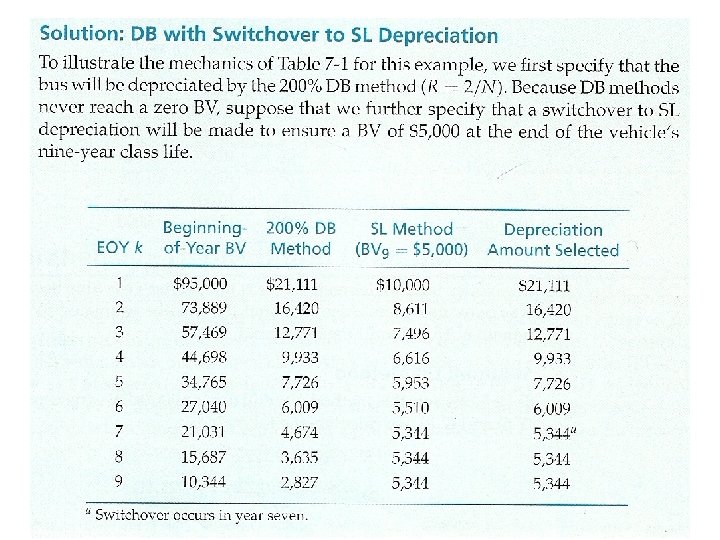

DB with Switchover to SL method.

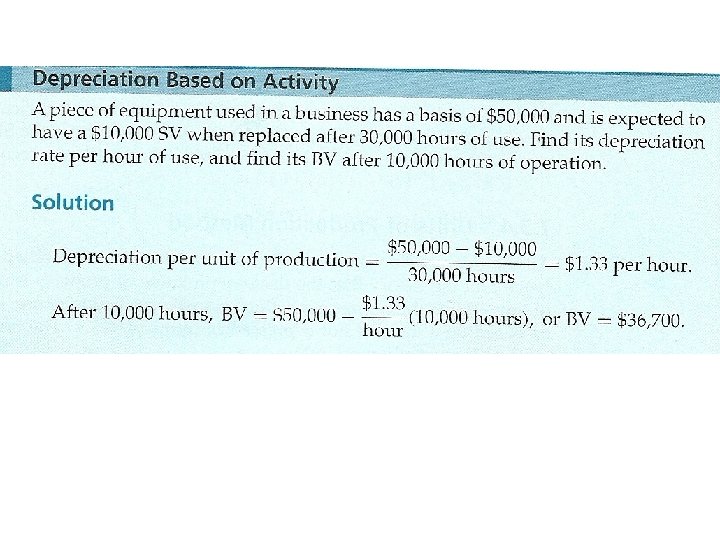

The Units of Production method: can be used when the decrease in value of the asset is mostly a function of use, instead of time. The cost basis is allocated equally over the number of units produced over the asset’s life. The depreciation per unit of production is found from the formula below.

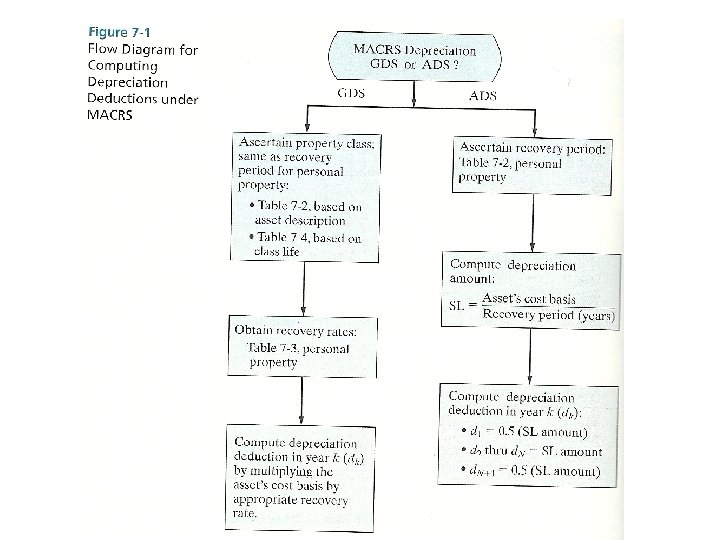

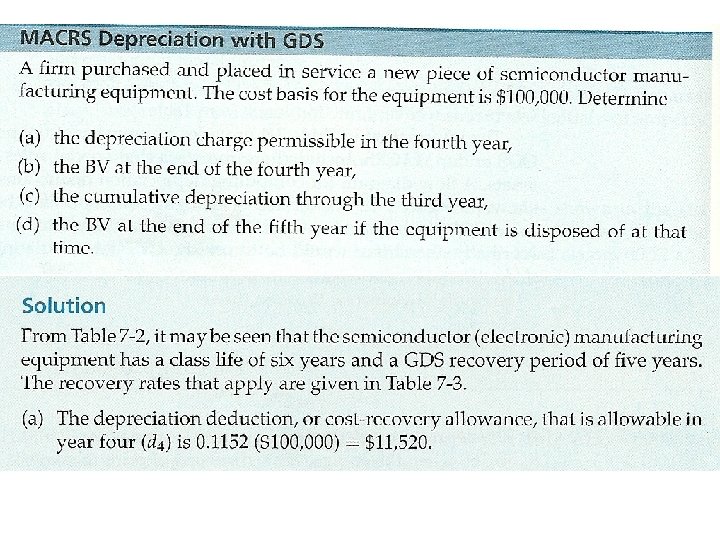

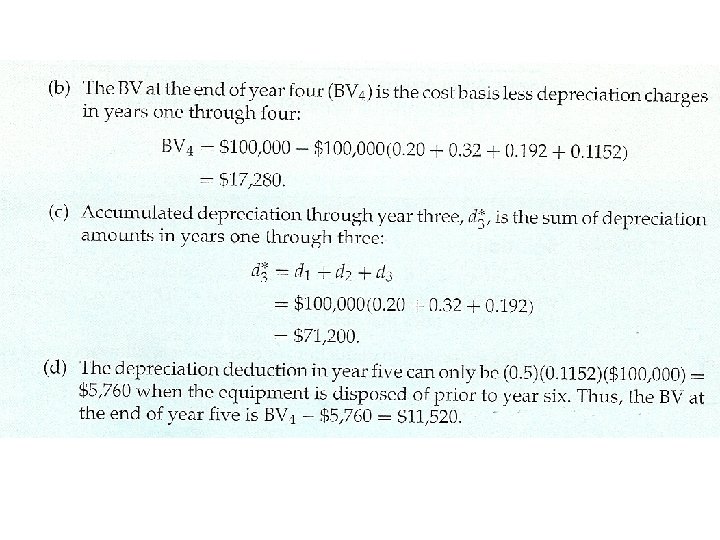

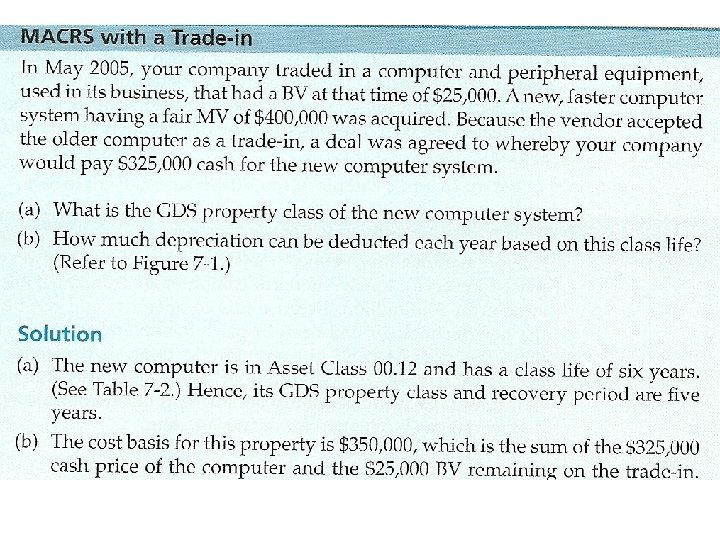

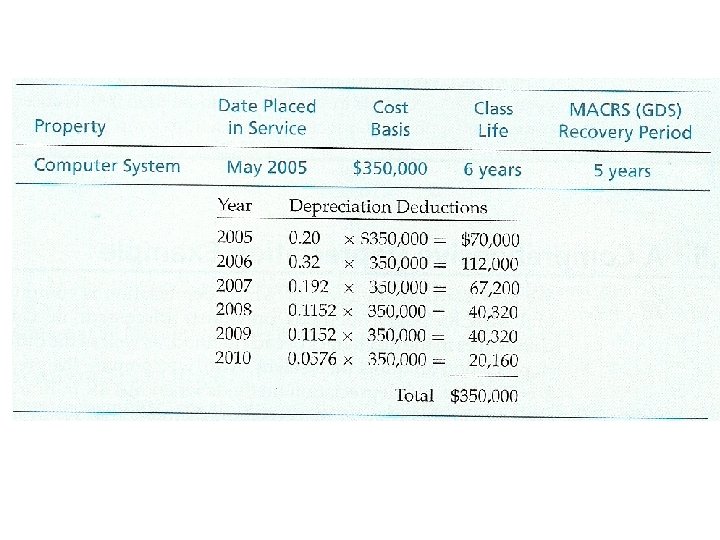

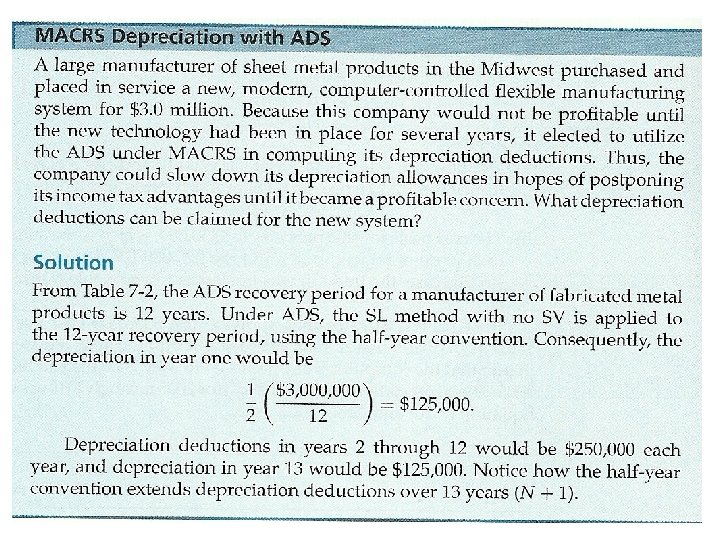

The Modified Accelerated Cost Recovery System (MACRS) MACRS is the principle method for computing depreciation for property in engineering projects. Applies to most tangible depreciable property placed in service after December 31, 1986. SVN is defined to be 0. It consists of two systems: 1. the General Depreciation System (GDS) 2. the Alternative Depreciation System (ADS).

Information Needed to Calculate MACRS Depreciation 1. The cost basis 2. The date the property was placed in service 3. The property class and recovery period 4. The MACRS depreciation used (GDS or ADS) 5. The time convention that applies (half year)

The property class and recovery period

Basic information of GDS: • Tangible depreciable property assigned to one of six personal property classes (3, 5, 7, 10, 15 and 20 -year) -Corresponds to GDS recovery period. • Personal depreciable property not corresponding to these periods is considered 7 -yr property class. • Real property ( ﺍﻣﻼﻙ ﺛﺎﺑﺘﻪ ) assigned to two real property classes : nonresidential real property( )ﻏﻴﺮ ﺳﻜﻨﻴﻪ residential rental property. ( )ﺍﻟﺴﻜﻨﻴﻪ ﺍﻟﻤﺆﺠﺮﻩ 3. GDS recovery period is 39 years for nonresidential real property (31. 5 years if in service before May 13, 1993) and 27. 5 years for residential rental property.

Basic information of ADS: • ADS recovery period for tangible personal property is normally the same as the class life of the property, with some exceptions ( i. e. , asset class 00. 12 and 00. 22 ) • Any tangible personal property that does not fit into one of the asset classes is depreciated using a 12 -year ADS recovery period. • ADS recovery period for nonresidential real property is 40 years.

Depreciation methods for MACRS: 1. GDS 3, 5, 7, and 10 years personal property class: 200% declining balance (DB) with switchover to Straight Line (SL). 2. GDS 15 and 20 years personal property class: 150% declining balance (DB) with switchover to Straight Line (SL). 3. GDS nonresidential real property and residential rental property: the SL method over GDS recovery periods. 4. ADS: the SL method for both personal and real property over the fixed ADS recovery periods.

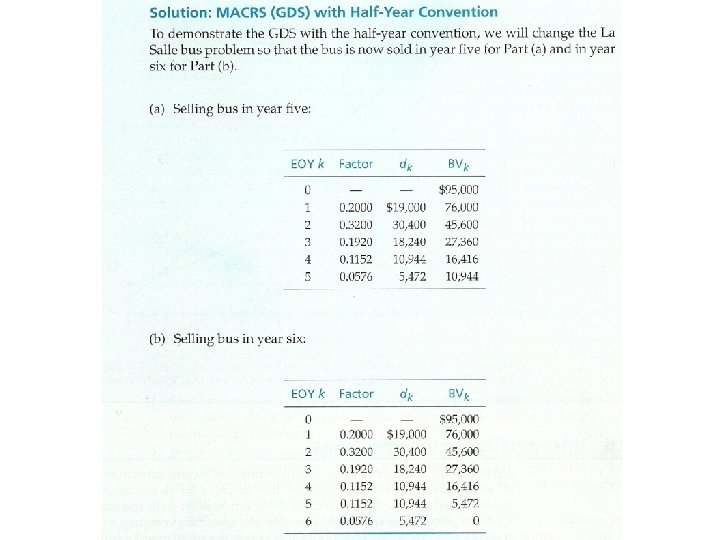

Half-Year Time Conventions For MACRS Depreciation Calculations • All assets placed in service during the year are treated as if use began in the middle of the year (1/2 -year depreciation is allowed). • If asset is disposed of before the full recovery period is used, only half of the normal depreciation deduction can be taken for that year.

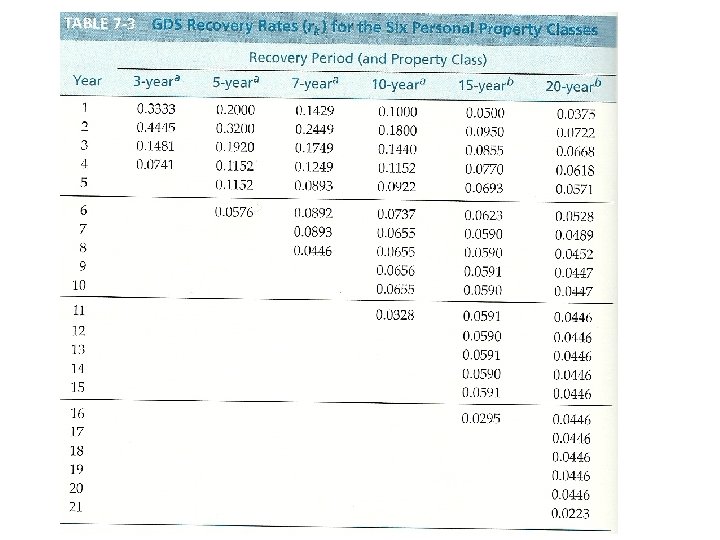

Using MACRS is easy! 1. Determine the asset’s recovery period (Table 7 -2). 2. Use the appropriate column from Table 7 -3 that matches the recovery period to find the recovery rate, rk, and compute the depreciation for each year as